Synchronoss PESTLE Analysis

Skip the Research. Get the Strategy.

Understand how political, economic, and technological forces are shaping Synchronoss's outlook with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable intelligence; purchase the full analysis to access the complete, editable report and make better-informed decisions today.

Political factors

Data Sovereignty and National Security Policies

Governments in over 60 countries now enforce data residency laws, pressuring Synchronoss to localize storage for its cloud and messaging services to remain compliant and avoid fines that can reach up to 4% of global revenue under some regimes; Synchronoss reported $150m revenue in FY2024, making compliance penalties material. The company must map diverse legal regimes across key markets (EU, India, Brazil) and redesign delivery to support localized infrastructure while preserving platform consistency. This creates capital expenditure and operational complexity as localized data centers and partnerships raise costs and elongate deployment timelines.

Geopolitical Trade Relations

Ongoing trade tensions between the US, China and EU risk disrupting supply chains for telecommunications hardware and chips that Synchronoss depends on, with global semiconductor export controls causing supply volatility—worldwide chip shipments fell 6% in 2024 versus 2023 per WSTS, raising component costs. New export controls and tariffs on cloud software and SaaS increases market entry costs and could compress gross margins by several percentage points. Political instability in markets like Latin America and parts of EMEA has led to abrupt contract cancellations by state-owned telcos, contributing to regional revenue volatility—EMEA revenue swung ±12% in 2024 for comparable vendors.

Government Digital Identity Mandates

Many nations are adopting standardized digital identity frameworks—over 70 countries had national eID programs by 2024—creating demand for identity management solutions; Synchronoss can target public-sector contracts, tapping markets where government IT spending exceeded $600B globally in 2024. Aligning products to government mandates offers revenue upside but shifting political priorities and evolving technical standards require agile development and modular architectures to mitigate rework risk.

Telecommunications Infrastructure Subsidies

Government grants and subsidies expanding US and EU broadband and 5G — e.g., US BEAD program $42.5B and EU Recovery Fund allocations — can raise Synchronoss’s TAM by enabling millions of new high-speed subscribers, boosting demand for cloud storage and advanced messaging.

As connectivity improves, enterprise and consumer uptake of cloud-based messaging typically grows; Synchronoss should track infrastructure spending shifts to target partnerships in high-subsidy regions.

- BEAD $42.5B (US) and EU digital funds increase addressable users

- Higher 5G penetration correlates with rising cloud/messaging usage

- Monitor political shifts to identify partnership and market-entry zones

Regulatory Scrutiny of Big Tech

Political pressure to curb Big Tech dominance can open market share for niche firms like Synchronoss; EU antitrust actions led to fines exceeding €9bn for major firms in 2023–24, signaling regulator teeth.

Focus on interoperability and fair competition—e.g., DMA in EU (effective 2024) mandates platform openness—may ease integration of Synchronoss services with carriers.

However, broad tech rules raise compliance costs; estimated average compliance spend for mid-size tech firms rose ~18% in 2024, potentially squeezing margins.

- EU DMA (2024) increases interoperability—opportunity for integrations

- Major antitrust fines €9bn+ in 2023–24—regulatory momentum

- Compliance costs up ~18% for mid-size tech firms in 2024—risk to margins

Compliance costs bite as data-residency fines, chip shortages and EU rules squeeze Synchronoss

Regulatory data-residency laws in 60+ countries and potential fines up to 4% of revenue force Synchronoss to localize infrastructure; FY2024 revenue $150m makes penalties material. Trade tensions and 2024 semiconductor supply drops (WSTS −6%) raise component costs and compress margins. Government eID adoption (70+ countries) and US BEAD $42.5B expand TAM, while EU DMA (2024) and €9bn+ antitrust actions create both opportunity and higher compliance spend (~+18% 2024).

| Metric | Value |

|---|---|

| FY2024 Revenue | $150m |

| Data-residency jurisdictions | 60+ |

| Potential fine cap | Up to 4% revenue |

| Chip shipment change 2024 vs 2023 | −6% |

| eID national programs | 70+ |

| US BEAD fund | $42.5B |

| Antitrust fines 2023–24 | €9bn+ |

| Compliance cost increase (mid-size tech) | ~18% |

What is included in the product

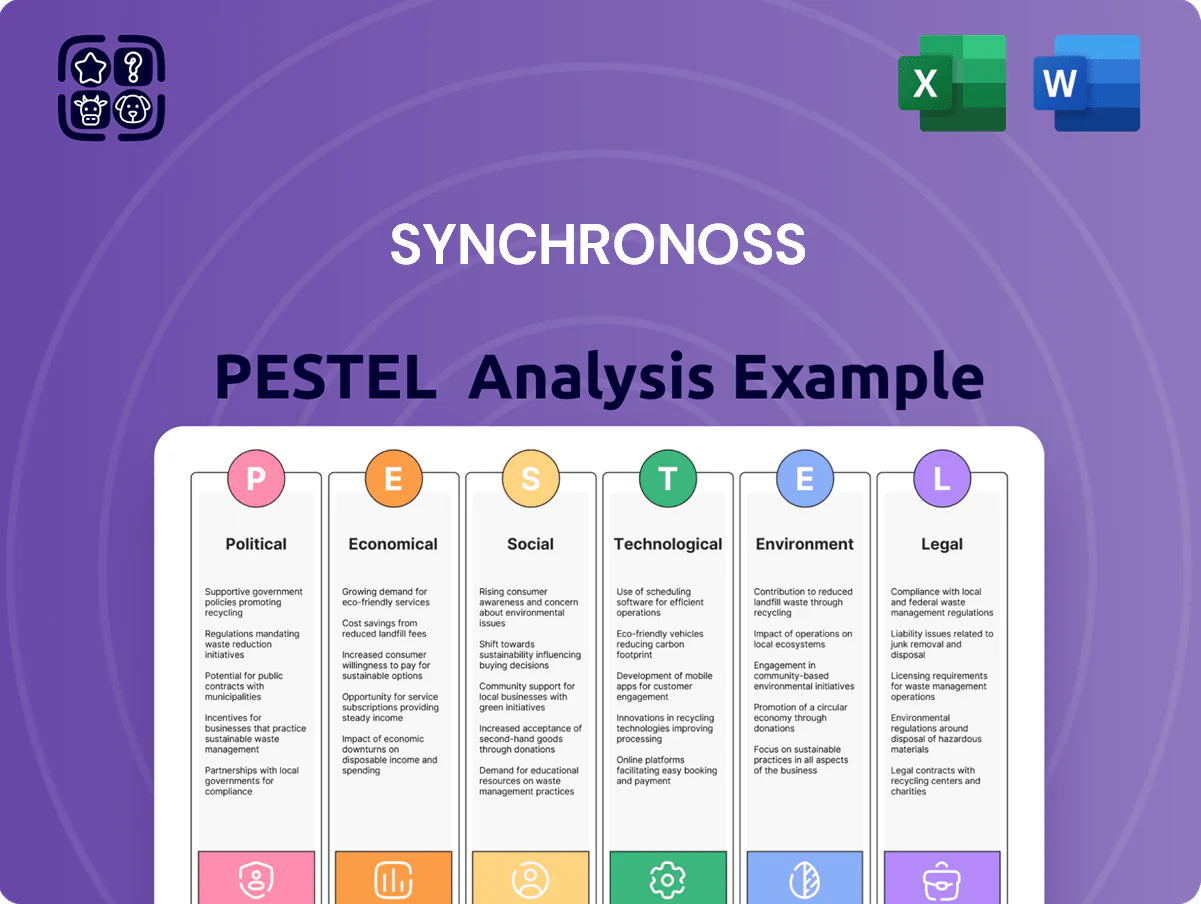

Explores how external macro-environmental factors uniquely affect Synchronoss across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a concise, shareable PESTLE snapshot of Synchronoss—visually segmented and written in plain language to speed alignment in meetings, presentations, or client reports.

Economic factors

Interest Rate and Capital Access

The late-2025 interest rate environment, with US benchmark fed funds around 5.25–5.50%, raises the cost of capital for tech firms funding innovation or acquisitions, increasing weighted average borrowing costs for Synchronoss compared with low-rate 2010s. Synchronoss must manage debt maturities and capex decisions to mitigate higher interest expense, as its cash and equivalents and available credit lines determine liquidity flexibility. Financial leaders are optimizing leverage ratios—targeting conservative net debt/EBITDA—to preserve investment capacity while pursuing growth.

Global Inflationary Pressures

Persistent global inflation—US CPI 3.4% YoY (Dec 2025) and global core services inflation ~4%—raises Synchronoss operational costs for talent and data-center energy/maintenance, squeezing margins.

To protect profitability, Synchronoss may need to adjust pricing with telco partners; telecom capex growth slowed to 1–2% in 2024, pressuring contract renegotiations.

Declining consumer purchasing power (real wages underperforming CPI in 2024) could push subscribers to drop premium cloud features, reducing ARPU.

Currency Exchange Rate Volatility

As a company with a large international footprint, Synchronoss faces FX risk: in 2024 roughly 35% of revenue was dollar-linked, so a 10% appreciation of the US dollar versus major currencies could erode reported revenue by ~3.5%. A strong dollar can make services pricier for overseas clients, slowing expansion in EMEA and APAC where 2024 growth targets were mid-single digits. Synchronoss uses forward contracts and localized pricing; hedging reduced FX translation losses to $12m in FY2024, cushioning consolidated results.

Subscription Economy Resilience

The shift to recurring revenue gives Synchronoss greater predictability: subscription and cloud services represented over 65% of revenue in 2024, cushioning cash flows during downturns.

Investors favor subscription models for lower churn—industry average churn for cloud messaging sits near 5–7% annually versus higher rates for hardware—supporting valuation stability.

Still, Synchronoss must prove ROI to carriers: in 2024, telecom capex cuts of 8–12% forced vendors to justify spend or be labeled discretionary.

- Recurring revenue share >65% (2024)

- Cloud messaging churn ~5–7% annually

- Telecom capex down 8–12% in 2024

Telecom Industry CAPEX Trends

The telecom sector’s CAPEX guides digital transformation spend; global operator CAPEX fell 3% in 2024 to about $270B, pressuring upgrades to cloud and messaging platforms.

During carrier headwinds—AT&T cut 2024 capex ~6%, Deutsche Telekom paused some cloud projects—providers defer nonessential rollouts to preserve cash.

Synchronoss must tie offerings to cost-savings and revenue uplift (e.g., reducing churn or ARPU gains) to stay prioritized.

- 2024 global telco CAPEX ≈ $270B, down 3%

- Major carriers trimming capex: AT&T −6% (2024)

- Sell cost-savings + revenue-driving KPIs (churn, ARPU)

Higher rates, rising costs squeeze Synchronoss; >65% recurring revenue cushions outlook

Higher rates (Fed funds ~5.25–5.50% late-2025) raise Synchronoss' cost of capital; net debt/EBITDA targets tightened. Inflation (US CPI ~3.4% Dec‑2025) lifts labor and data-center costs, squeezing margins. Recurring revenue >65% (2024) cushions cash flow; telecom CAPEX fell ~3% in 2024 to $270B, increasing vendor scrutiny.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| US CPI (Dec‑2025) | 3.4% YoY |

| Recurring rev (2024) | >65% |

| Global telco CAPEX (2024) | $270B (−3%) |

Full Version Awaits

Synchronoss PESTLE Analysis

The preview shown here is the exact Synchronoss PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in the preview are identical to the downloadable file you’ll get immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Understand how political, economic, and technological forces are shaping Synchronoss's outlook with our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable intelligence; purchase the full analysis to access the complete, editable report and make better-informed decisions today.

Political factors

Data Sovereignty and National Security Policies

Governments in over 60 countries now enforce data residency laws, pressuring Synchronoss to localize storage for its cloud and messaging services to remain compliant and avoid fines that can reach up to 4% of global revenue under some regimes; Synchronoss reported $150m revenue in FY2024, making compliance penalties material. The company must map diverse legal regimes across key markets (EU, India, Brazil) and redesign delivery to support localized infrastructure while preserving platform consistency. This creates capital expenditure and operational complexity as localized data centers and partnerships raise costs and elongate deployment timelines.

Geopolitical Trade Relations

Ongoing trade tensions between the US, China and EU risk disrupting supply chains for telecommunications hardware and chips that Synchronoss depends on, with global semiconductor export controls causing supply volatility—worldwide chip shipments fell 6% in 2024 versus 2023 per WSTS, raising component costs. New export controls and tariffs on cloud software and SaaS increases market entry costs and could compress gross margins by several percentage points. Political instability in markets like Latin America and parts of EMEA has led to abrupt contract cancellations by state-owned telcos, contributing to regional revenue volatility—EMEA revenue swung ±12% in 2024 for comparable vendors.

Government Digital Identity Mandates

Many nations are adopting standardized digital identity frameworks—over 70 countries had national eID programs by 2024—creating demand for identity management solutions; Synchronoss can target public-sector contracts, tapping markets where government IT spending exceeded $600B globally in 2024. Aligning products to government mandates offers revenue upside but shifting political priorities and evolving technical standards require agile development and modular architectures to mitigate rework risk.

Telecommunications Infrastructure Subsidies

Government grants and subsidies expanding US and EU broadband and 5G — e.g., US BEAD program $42.5B and EU Recovery Fund allocations — can raise Synchronoss’s TAM by enabling millions of new high-speed subscribers, boosting demand for cloud storage and advanced messaging.

As connectivity improves, enterprise and consumer uptake of cloud-based messaging typically grows; Synchronoss should track infrastructure spending shifts to target partnerships in high-subsidy regions.

- BEAD $42.5B (US) and EU digital funds increase addressable users

- Higher 5G penetration correlates with rising cloud/messaging usage

- Monitor political shifts to identify partnership and market-entry zones

Regulatory Scrutiny of Big Tech

Political pressure to curb Big Tech dominance can open market share for niche firms like Synchronoss; EU antitrust actions led to fines exceeding €9bn for major firms in 2023–24, signaling regulator teeth.

Focus on interoperability and fair competition—e.g., DMA in EU (effective 2024) mandates platform openness—may ease integration of Synchronoss services with carriers.

However, broad tech rules raise compliance costs; estimated average compliance spend for mid-size tech firms rose ~18% in 2024, potentially squeezing margins.

- EU DMA (2024) increases interoperability—opportunity for integrations

- Major antitrust fines €9bn+ in 2023–24—regulatory momentum

- Compliance costs up ~18% for mid-size tech firms in 2024—risk to margins

Compliance costs bite as data-residency fines, chip shortages and EU rules squeeze Synchronoss

Regulatory data-residency laws in 60+ countries and potential fines up to 4% of revenue force Synchronoss to localize infrastructure; FY2024 revenue $150m makes penalties material. Trade tensions and 2024 semiconductor supply drops (WSTS −6%) raise component costs and compress margins. Government eID adoption (70+ countries) and US BEAD $42.5B expand TAM, while EU DMA (2024) and €9bn+ antitrust actions create both opportunity and higher compliance spend (~+18% 2024).

| Metric | Value |

|---|---|

| FY2024 Revenue | $150m |

| Data-residency jurisdictions | 60+ |

| Potential fine cap | Up to 4% revenue |

| Chip shipment change 2024 vs 2023 | −6% |

| eID national programs | 70+ |

| US BEAD fund | $42.5B |

| Antitrust fines 2023–24 | €9bn+ |

| Compliance cost increase (mid-size tech) | ~18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Synchronoss across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a concise, shareable PESTLE snapshot of Synchronoss—visually segmented and written in plain language to speed alignment in meetings, presentations, or client reports.

Economic factors

Interest Rate and Capital Access

The late-2025 interest rate environment, with US benchmark fed funds around 5.25–5.50%, raises the cost of capital for tech firms funding innovation or acquisitions, increasing weighted average borrowing costs for Synchronoss compared with low-rate 2010s. Synchronoss must manage debt maturities and capex decisions to mitigate higher interest expense, as its cash and equivalents and available credit lines determine liquidity flexibility. Financial leaders are optimizing leverage ratios—targeting conservative net debt/EBITDA—to preserve investment capacity while pursuing growth.

Global Inflationary Pressures

Persistent global inflation—US CPI 3.4% YoY (Dec 2025) and global core services inflation ~4%—raises Synchronoss operational costs for talent and data-center energy/maintenance, squeezing margins.

To protect profitability, Synchronoss may need to adjust pricing with telco partners; telecom capex growth slowed to 1–2% in 2024, pressuring contract renegotiations.

Declining consumer purchasing power (real wages underperforming CPI in 2024) could push subscribers to drop premium cloud features, reducing ARPU.

Currency Exchange Rate Volatility

As a company with a large international footprint, Synchronoss faces FX risk: in 2024 roughly 35% of revenue was dollar-linked, so a 10% appreciation of the US dollar versus major currencies could erode reported revenue by ~3.5%. A strong dollar can make services pricier for overseas clients, slowing expansion in EMEA and APAC where 2024 growth targets were mid-single digits. Synchronoss uses forward contracts and localized pricing; hedging reduced FX translation losses to $12m in FY2024, cushioning consolidated results.

Subscription Economy Resilience

The shift to recurring revenue gives Synchronoss greater predictability: subscription and cloud services represented over 65% of revenue in 2024, cushioning cash flows during downturns.

Investors favor subscription models for lower churn—industry average churn for cloud messaging sits near 5–7% annually versus higher rates for hardware—supporting valuation stability.

Still, Synchronoss must prove ROI to carriers: in 2024, telecom capex cuts of 8–12% forced vendors to justify spend or be labeled discretionary.

- Recurring revenue share >65% (2024)

- Cloud messaging churn ~5–7% annually

- Telecom capex down 8–12% in 2024

Telecom Industry CAPEX Trends

The telecom sector’s CAPEX guides digital transformation spend; global operator CAPEX fell 3% in 2024 to about $270B, pressuring upgrades to cloud and messaging platforms.

During carrier headwinds—AT&T cut 2024 capex ~6%, Deutsche Telekom paused some cloud projects—providers defer nonessential rollouts to preserve cash.

Synchronoss must tie offerings to cost-savings and revenue uplift (e.g., reducing churn or ARPU gains) to stay prioritized.

- 2024 global telco CAPEX ≈ $270B, down 3%

- Major carriers trimming capex: AT&T −6% (2024)

- Sell cost-savings + revenue-driving KPIs (churn, ARPU)

Higher rates, rising costs squeeze Synchronoss; >65% recurring revenue cushions outlook

Higher rates (Fed funds ~5.25–5.50% late-2025) raise Synchronoss' cost of capital; net debt/EBITDA targets tightened. Inflation (US CPI ~3.4% Dec‑2025) lifts labor and data-center costs, squeezing margins. Recurring revenue >65% (2024) cushions cash flow; telecom CAPEX fell ~3% in 2024 to $270B, increasing vendor scrutiny.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% |

| US CPI (Dec‑2025) | 3.4% YoY |

| Recurring rev (2024) | >65% |

| Global telco CAPEX (2024) | $270B (−3%) |

Full Version Awaits

Synchronoss PESTLE Analysis

The preview shown here is the exact Synchronoss PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in the preview are identical to the downloadable file you’ll get immediately after payment.