Synchrony Financial Marketing Mix

Your Shortcut to a Strategic 4Ps Breakdown

Discover how Synchrony Financial aligns product offerings, pricing structures, distribution channels, and promotions to capture consumer finance share—this concise preview highlights strategic strengths and gaps; get the full 4Ps Marketing Mix Analysis in an editable, presentation-ready format to save hours of research and apply expert-backed insights to your business, client work, or coursework.

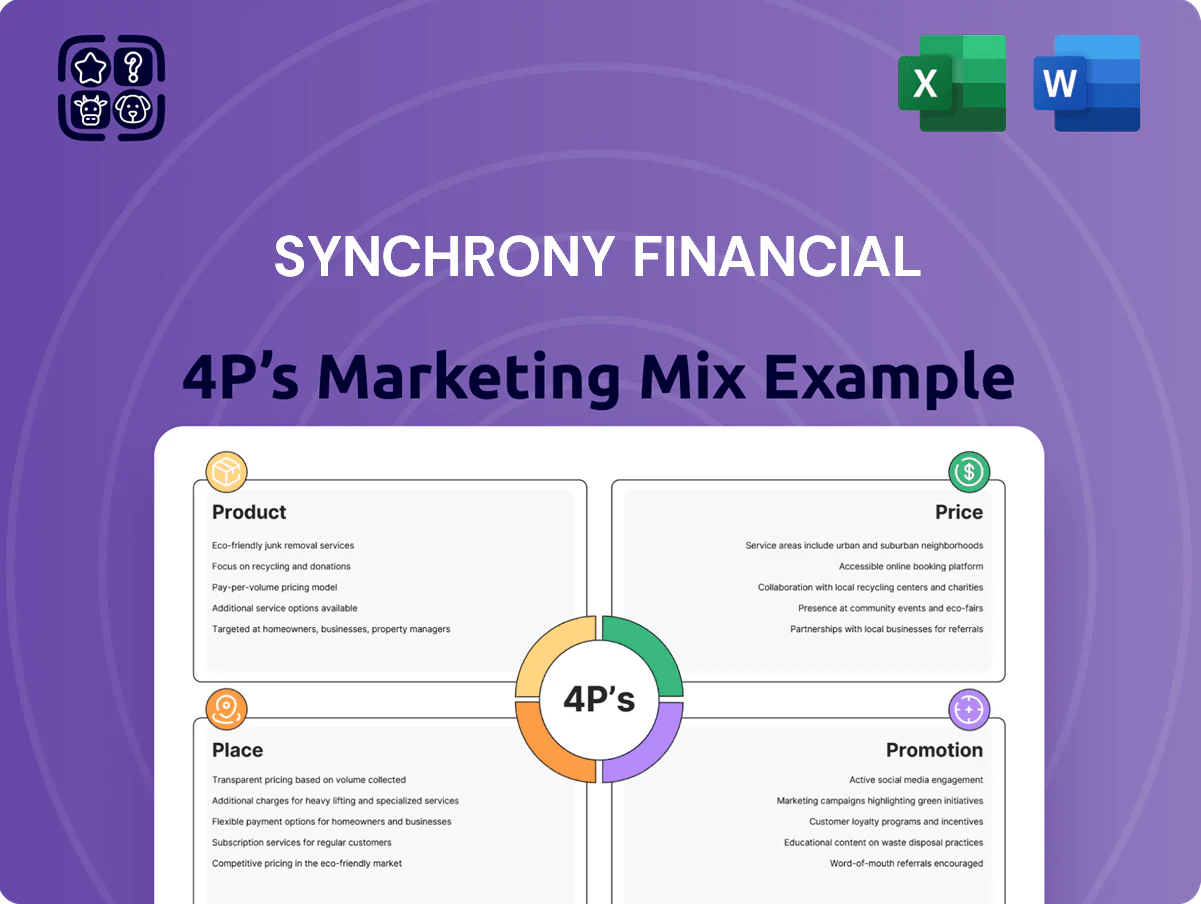

Product

Tailored Private Label Credit Cards

Synchrony’s tailored private-label credit cards embed into retailer ecosystems like JCPenney and Sam’s Club, driving purchase frequency via co-branded rewards and exclusive financing; private-label receivables made up about $26.4B of total loans in 2025, a core revenue stream.

Co-branded and Network Credit Cards

Synchrony issues co-branded network cards carrying Visa, Mastercard, or American Express, letting holders spend at partner stores plus 50M+ merchants globally where the networks are accepted; this widens utility while keeping partner affinity through tiered rewards that boost partner spend by ~18% annually. In 2025 Synchrony expanded into travel, launching airline deals that target a projected $300M incremental loan receivables growth and higher APR yields.

CareCredit Health and Wellness Financing

CareCredit, a Synchrony Financial revolving credit line, covers health, veterinary, and wellness costs often missed by insurance and is accepted at over 270,000 provider locations; as of Q3 2025 it supported roughly $9.2 billion in receivables on Synchrony’s balance sheet.

Synchrony SetPay Installment Loans

Synchrony SetPay Installment Loans lets shoppers split purchases into fixed monthly payments, positioning it as a BNPL alternative to revolving credit and targeting high-ticket, structured-debt buyers.

To fight fintech rivals, SetPay emphasizes predictable terms, underwriting, and fraud controls; by end-2025 it’s integrated in checkout flows for top partners including Amazon and Walmart, capturing a growing share of POS lending volume.

- Predictable monthly payments

- Alternative to revolving credit

- Integrated with Amazon, Walmart by 2025

- Targets high-ticket purchases, reduces churn

High-Yield Digital Banking Products

Through Synchrony Bank, Synchrony Financial offers FDIC-insured, digital-first high-yield savings, CDs, and money market accounts that attract retail deposits to fund lending while charging no monthly fees.

In 2025 these products advertise competitive APYs—savings and money market near 4.50% and CDs up to 5.25%—positioning them as high-liquidity, low-volatility options amid rate shifts.

They support deposit growth: Synchrony held about $85 billion in consumer deposits at year-end 2024, providing stable funding and lower-cost capital for lending.

- FDIC-insured digital savings, CDs, MMAs

- No monthly fees; competitive APYs (~4.50%–5.25%)

- High liquidity; funds retail lending

- $85B consumer deposits (2024)

Synchrony: $26B Private‑Label, $9.2B CareCredit, SetPay on Amazon/Walmart, $85B Deposits

Synchrony’s product mix centers on private-label cards (~$26.4B receivables in 2025), co-branded network cards, CareCredit (~$9.2B Q3 2025), SetPay BNPL (integrated at Amazon/Walmart by end-2025), and FDIC-insured deposits (~$85B consumer deposits 2024) with savings APYs ~4.50%–5.25%.

| Product | Key metric | 2024/2025 |

|---|---|---|

| Private-label cards | Receivables | $26.4B (2025) |

| CareCredit | Receivables | $9.2B (Q3 2025) |

| SetPay | Checkout integrations | Amazon, Walmart (end-2025) |

| Deposit products | Consumer deposits / APY | $85B (2024) / 4.50%–5.25% |

What is included in the product

Delivers a concise, company-specific deep dive into Synchrony Financial’s Product, Price, Place, and Promotion strategies, ideal for managers and consultants needing a clear breakdown of its marketing positioning grounded in real practices and competitive context.

Condenses Synchrony Financial’s 4P marketing insights into a concise, at-a-glance format that leadership can use for quick decision-making and cross-functional alignment.

Place

Strategic Retail Partner Network

Synchrony’s primary distribution runs through ~1.5 million retail locations via partners (2025), where sales associates submit instant credit apps at point-of-sale to close purchases immediately.

These storefronts drive high-ticket categories: in 2024 Synchrony financed $59 billion in home improvement and $18 billion in automotive-related receivables, and physical presence stayed crucial for in-person consults.

E-commerce and API Integrations

Synchrony embeds its consumer financing into checkout via APIs on major retailers, surfacing pay-over-time offers at point of sale to cut friction and boost conversion; API calls now handle 85% of digital financings. By end-2025, enhanced marketplace and mobile app integrations drove double-digit growth—online visits +18% and digital sales +22% year-over-year—supporting a 12% rise in receivables from e-commerce channels.

CareCredit Provider Locations

CareCredit distributes locally through 225,000+ provider locations across medical, dental, and veterinary practices in the US, reaching patients at point of care where staff offer applications via integrated POS and EMR tools like Clover and Athenahealth.

Proprietary Digital and Mobile Platforms

Synchrony runs centralized digital portals and mobile apps where customers manage multiple credit accounts and find financing offers; these channels handled roughly 40% of active customer interactions in 2025, per company disclosures.

They act as direct-to-consumer channels using AI-driven insights (personalization, propensity models) to boost cross-product engagement and increase digital sales conversion rates by double digits.

By 2025 these proprietary platforms are key to retaining customers beyond partner purchases, supporting retention and NPS improvements.

- 2025: ~40% customer interactions via platforms

- AI personalization: double-digit uplift in conversions

- Platform role: retention, cross-sell, NPS gains

Digital Wallet and Mobile Provisioning

Synchrony provisions its credit cards into Apple Pay and Google Pay so cardholders can use Synchrony-issued credit for contactless purchases even at non-partner merchants, boosting card utility.

By late 2025 unique active users provisioning Synchrony cards in digital wallets rose ~38% year-over-year, signaling a clear shift to mobile-first payments and higher on-the-go spend.

- Provisioning: Apple Pay, Google Pay

- Use case: Contactless at non-partner locations

- Metric: ~38% YoY rise in unique active wallet users by Q4 2025

Synchrony: 1.5M+ partners, $77B receivables, 85% API financings, digital +22%

Synchrony distributes via ~1.5M retail partners (2025) plus 225k CareCredit providers, finances $59B home improvement and $18B auto receivables (2024), digital APIs handle 85% of online financings, platforms drove +18% visits/+22% digital sales in 2025, 40% customer interactions via apps, and wallet provisioning rose ~38% YoY by Q4 2025.

| Metric | Value |

|---|---|

| Retail partners | ~1.5M (2025) |

| CareCredit providers | 225k+ |

| Home improvement financing | $59B (2024) |

| Auto-related receivables | $18B (2024) |

| API share of digital financings | 85% |

| Digital visits / sales growth | +18% / +22% (2025) |

| Platform interactions | 40% (2025) |

| Wallet provisioning growth | ~38% YoY (Q4 2025) |

What You See Is What You Get

Synchrony Financial 4P's Marketing Mix Analysis

The preview shown here is the actual Synchrony Financial 4P's Marketing Mix analysis you’ll receive instantly after purchase—no surprises; it’s the full, editable document ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to a Strategic 4Ps Breakdown

Discover how Synchrony Financial aligns product offerings, pricing structures, distribution channels, and promotions to capture consumer finance share—this concise preview highlights strategic strengths and gaps; get the full 4Ps Marketing Mix Analysis in an editable, presentation-ready format to save hours of research and apply expert-backed insights to your business, client work, or coursework.

Product

Tailored Private Label Credit Cards

Synchrony’s tailored private-label credit cards embed into retailer ecosystems like JCPenney and Sam’s Club, driving purchase frequency via co-branded rewards and exclusive financing; private-label receivables made up about $26.4B of total loans in 2025, a core revenue stream.

Co-branded and Network Credit Cards

Synchrony issues co-branded network cards carrying Visa, Mastercard, or American Express, letting holders spend at partner stores plus 50M+ merchants globally where the networks are accepted; this widens utility while keeping partner affinity through tiered rewards that boost partner spend by ~18% annually. In 2025 Synchrony expanded into travel, launching airline deals that target a projected $300M incremental loan receivables growth and higher APR yields.

CareCredit Health and Wellness Financing

CareCredit, a Synchrony Financial revolving credit line, covers health, veterinary, and wellness costs often missed by insurance and is accepted at over 270,000 provider locations; as of Q3 2025 it supported roughly $9.2 billion in receivables on Synchrony’s balance sheet.

Synchrony SetPay Installment Loans

Synchrony SetPay Installment Loans lets shoppers split purchases into fixed monthly payments, positioning it as a BNPL alternative to revolving credit and targeting high-ticket, structured-debt buyers.

To fight fintech rivals, SetPay emphasizes predictable terms, underwriting, and fraud controls; by end-2025 it’s integrated in checkout flows for top partners including Amazon and Walmart, capturing a growing share of POS lending volume.

- Predictable monthly payments

- Alternative to revolving credit

- Integrated with Amazon, Walmart by 2025

- Targets high-ticket purchases, reduces churn

High-Yield Digital Banking Products

Through Synchrony Bank, Synchrony Financial offers FDIC-insured, digital-first high-yield savings, CDs, and money market accounts that attract retail deposits to fund lending while charging no monthly fees.

In 2025 these products advertise competitive APYs—savings and money market near 4.50% and CDs up to 5.25%—positioning them as high-liquidity, low-volatility options amid rate shifts.

They support deposit growth: Synchrony held about $85 billion in consumer deposits at year-end 2024, providing stable funding and lower-cost capital for lending.

- FDIC-insured digital savings, CDs, MMAs

- No monthly fees; competitive APYs (~4.50%–5.25%)

- High liquidity; funds retail lending

- $85B consumer deposits (2024)

Synchrony: $26B Private‑Label, $9.2B CareCredit, SetPay on Amazon/Walmart, $85B Deposits

Synchrony’s product mix centers on private-label cards (~$26.4B receivables in 2025), co-branded network cards, CareCredit (~$9.2B Q3 2025), SetPay BNPL (integrated at Amazon/Walmart by end-2025), and FDIC-insured deposits (~$85B consumer deposits 2024) with savings APYs ~4.50%–5.25%.

| Product | Key metric | 2024/2025 |

|---|---|---|

| Private-label cards | Receivables | $26.4B (2025) |

| CareCredit | Receivables | $9.2B (Q3 2025) |

| SetPay | Checkout integrations | Amazon, Walmart (end-2025) |

| Deposit products | Consumer deposits / APY | $85B (2024) / 4.50%–5.25% |

What is included in the product

Delivers a concise, company-specific deep dive into Synchrony Financial’s Product, Price, Place, and Promotion strategies, ideal for managers and consultants needing a clear breakdown of its marketing positioning grounded in real practices and competitive context.

Condenses Synchrony Financial’s 4P marketing insights into a concise, at-a-glance format that leadership can use for quick decision-making and cross-functional alignment.

Place

Strategic Retail Partner Network

Synchrony’s primary distribution runs through ~1.5 million retail locations via partners (2025), where sales associates submit instant credit apps at point-of-sale to close purchases immediately.

These storefronts drive high-ticket categories: in 2024 Synchrony financed $59 billion in home improvement and $18 billion in automotive-related receivables, and physical presence stayed crucial for in-person consults.

E-commerce and API Integrations

Synchrony embeds its consumer financing into checkout via APIs on major retailers, surfacing pay-over-time offers at point of sale to cut friction and boost conversion; API calls now handle 85% of digital financings. By end-2025, enhanced marketplace and mobile app integrations drove double-digit growth—online visits +18% and digital sales +22% year-over-year—supporting a 12% rise in receivables from e-commerce channels.

CareCredit Provider Locations

CareCredit distributes locally through 225,000+ provider locations across medical, dental, and veterinary practices in the US, reaching patients at point of care where staff offer applications via integrated POS and EMR tools like Clover and Athenahealth.

Proprietary Digital and Mobile Platforms

Synchrony runs centralized digital portals and mobile apps where customers manage multiple credit accounts and find financing offers; these channels handled roughly 40% of active customer interactions in 2025, per company disclosures.

They act as direct-to-consumer channels using AI-driven insights (personalization, propensity models) to boost cross-product engagement and increase digital sales conversion rates by double digits.

By 2025 these proprietary platforms are key to retaining customers beyond partner purchases, supporting retention and NPS improvements.

- 2025: ~40% customer interactions via platforms

- AI personalization: double-digit uplift in conversions

- Platform role: retention, cross-sell, NPS gains

Digital Wallet and Mobile Provisioning

Synchrony provisions its credit cards into Apple Pay and Google Pay so cardholders can use Synchrony-issued credit for contactless purchases even at non-partner merchants, boosting card utility.

By late 2025 unique active users provisioning Synchrony cards in digital wallets rose ~38% year-over-year, signaling a clear shift to mobile-first payments and higher on-the-go spend.

- Provisioning: Apple Pay, Google Pay

- Use case: Contactless at non-partner locations

- Metric: ~38% YoY rise in unique active wallet users by Q4 2025

Synchrony: 1.5M+ partners, $77B receivables, 85% API financings, digital +22%

Synchrony distributes via ~1.5M retail partners (2025) plus 225k CareCredit providers, finances $59B home improvement and $18B auto receivables (2024), digital APIs handle 85% of online financings, platforms drove +18% visits/+22% digital sales in 2025, 40% customer interactions via apps, and wallet provisioning rose ~38% YoY by Q4 2025.

| Metric | Value |

|---|---|

| Retail partners | ~1.5M (2025) |

| CareCredit providers | 225k+ |

| Home improvement financing | $59B (2024) |

| Auto-related receivables | $18B (2024) |

| API share of digital financings | 85% |

| Digital visits / sales growth | +18% / +22% (2025) |

| Platform interactions | 40% (2025) |

| Wallet provisioning growth | ~38% YoY (Q4 2025) |

What You See Is What You Get

Synchrony Financial 4P's Marketing Mix Analysis

The preview shown here is the actual Synchrony Financial 4P's Marketing Mix analysis you’ll receive instantly after purchase—no surprises; it’s the full, editable document ready for immediate use.