Synovus Marketing Mix

Ready-Made Marketing Analysis, Ready to Use

Discover how Synovus aligns product offerings, pricing tiers, distribution channels, and promotional tactics to win customers—this concise preview highlights key strengths and gaps; purchase the full 4Ps Marketing Mix Analysis for an editable, presentation-ready report packed with data, practical recommendations, and benchmarking tools to accelerate strategy and save hours of research.

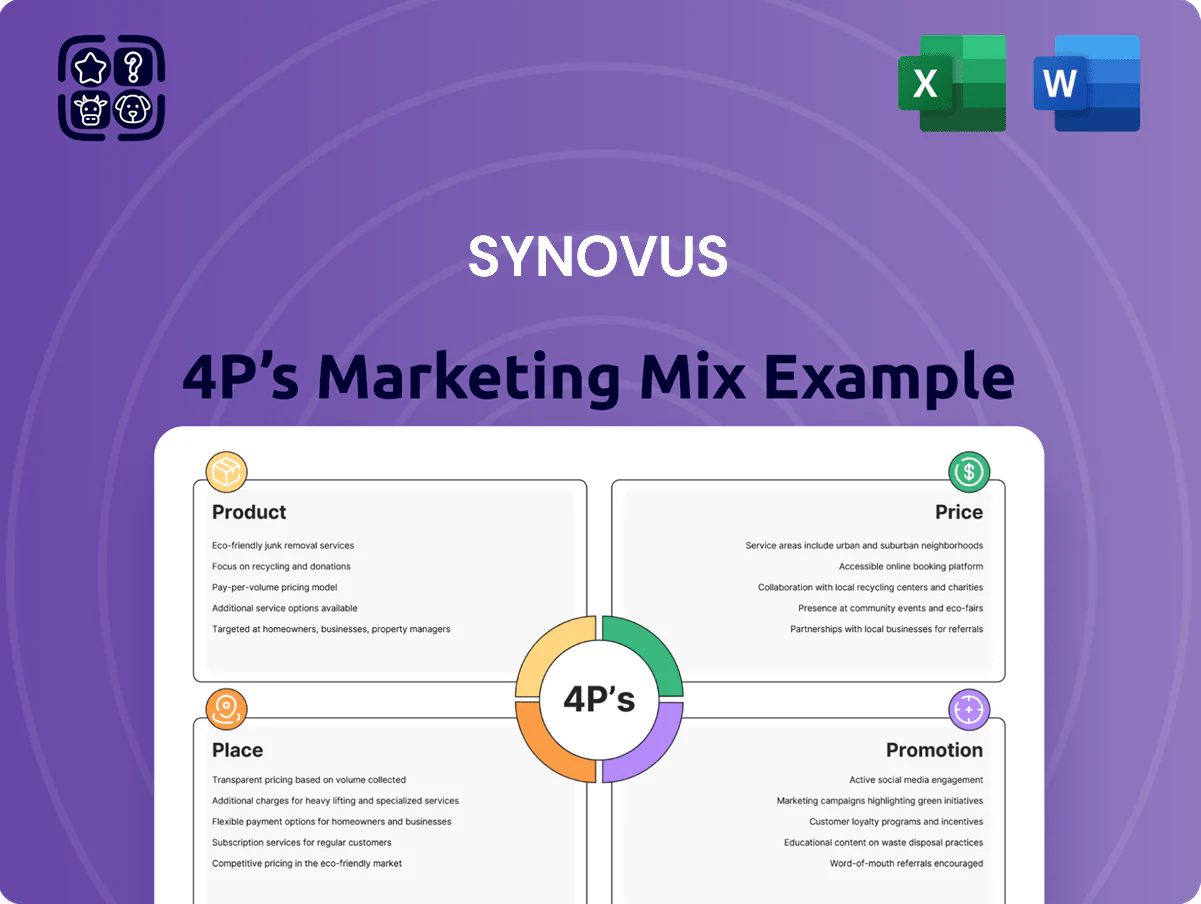

Product

Commercial Banking and Treasury Solutions

Synovus Commercial Banking offers term loans, revolving lines, and asset-based lending that funded $7.2 billion in business loans in 2024, targeting mid-market expansion across the Southeast.

The Treasury Solutions suite delivers cash‑flow optimization, electronic payables, and layered fraud protection, processing over $120 billion in payments in 2024 for corporate clients.

AP/AR and ERP integrations are standard, reducing reconciliation time by ~35% in client pilots and improving operational efficiency for regional enterprises.

Retail Banking and Deposit Accounts

Synovus retail offers checking, savings and money market accounts tailored to life stages, plus CDs with yields up to ~4.5% (2025 regional rates) and student/senior accounts stressing low fees; deposits totaled $38.2B in 2024, funding core lending and reducing cost of funds. These products drive long-term relationships—avg deposit tenure rising to ~6.1 years—and support liquidity and capital planning.

Wealth Management and Private Banking

Synovus Trust and Synovus Securities deliver investment management, estate planning, and brokerage for high-net-worth and institutional clients, managing roughly $26 billion in client assets as of 2025 year-end. Private banking offers high-touch personalized service with custom credit lines and tailored financial plans, averaging household loans above $1.2 million. The segment emphasizes preserving and growing wealth via a holistic balance-sheet approach that integrates liquidity, tax-aware strategies, and intergenerational planning.

Consumer Lending and Mortgage Services

Synovus offers residential mortgages, HELOCs, and personal loans, with 2025 mortgage originations around $3.1 billion, capturing stable retail assets and recurring fee income.

The mortgage unit provides fixed and adjustable rates plus first-time homebuyer and veteran programs; purchase loans made up ~62% of 2024 originations, boosting customer lifetime value.

- 2025 originations ≈ $3.1B

- 2024 purchase loans ≈ 62%

- Products: fixed, ARM, HELOC, personal loans

- Special programs: first-time buyers, veterans

Digital Banking and Fintech Integration

Synovus has upgraded its digital banking to match national rivals, delivering real-time alerts, mobile check deposit, and personal financial management (PFM) tools; as of 2025 mobile active users exceed 600,000 and digital transactions grew 18% YoY in 2024.

The digital layer targets tech-savvy customers and ensures 24/7 access, reducing branch visits by 22% and supporting cross-sell of deposit and lending products online.

- 600,000+ mobile users (2025)

- 18% digital transaction growth (2024)

- 22% fewer branch visits

- Real-time alerts, mobile deposit, PFM

Synovus: $7.2B loans, $120B payments, $38B deposits, $26B AUM, 600k+ digital users

Synovus product suite spans commercial loans ($7.2B funded in 2024), treasury processing ($120B payments in 2024), retail deposits ($38.2B in 2024; avg tenure 6.1 years), mortgages ($3.1B originations in 2025; 62% purchases), wealth AUM $26B (2025), and digital users 600k+ (2025).

| Metric | 2024/2025 |

|---|---|

| Commercial loans | $7.2B (2024) |

| Treasury payments | $120B (2024) |

| Deposits | $38.2B (2024) |

| Mortgages | $3.1B (2025) |

| Wealth AUM | $26B (2025) |

| Mobile users | 600k+ (2025) |

What is included in the product

Delivers a company-specific deep dive into Synovus’s Product, Price, Place, and Promotion strategies, grounded in actual brand practices and competitive context for realistic insights.

Condenses Synovus’s 4P marketing insights into a concise, leadership-friendly snapshot that’s perfect for presentations, quick alignment, or executive review.

Place

Southeastern Regional Branch Network

Synovus maintains a dense Southeastern Regional Branch Network with about 275 branches across Georgia, Alabama, Florida, South Carolina, and Tennessee, targeting fast-growing Sunbelt metros where regional GDP grew ~3.2% in 2024. This geographic focus helps Synovus capture rising commercial lending and deposit flows while preserving local relationships—branches accounted for ~35% of new client acquisitions in 2024. Physical locations remain key for complex commercial transactions and wealth management, even as digital channels handle routine banking; in 2024, digital adoption reached 78% of active customers, yet branch-originated commercial loans represented 58% of total commercial loan volume.

Community-Based Operating Model

Synovus uses a decentralized model where local leadership runs community bank divisions, enabling faster decisions and tailored responses to regional markets; in 2024 Synovus reported 80% of branches met local cash-flow targets within 30 days of market shifts. This localized approach yields a distribution edge—combining small-bank service with Synovus’s $55.6 billion in assets (2024) and centralized capital, helping retention and deposit growth in mid-sized cities.

Omnichannel Digital Platforms

Synovus has shifted distribution to omnichannel digital platforms—mobile apps and web portals—that let customers bank anywhere; as of Q4 2025 digital sessions rose 18% YoY and mobile users reached 1.9 million, cutting branch transactions 24%. These channels deliver consistent cross-device UX, keep services available 24/7, and lower cost-to-serve (estimated saving $40–60 per digital active customer annually), reducing dependence on physical branches while boosting convenience.

Relationship Manager and Advisory Network

Relationship managers and advisors deliver Synovus services primarily at client offices or private meeting spaces, acting as mobile distribution points that bring tailored expertise to commercial and wealth clients; this human-centric model drives satisfaction in high-value segments where personalized advice matters most.

In 2025 Synovus reported about 1,100 relationship managers across commercial and wealth lines, handling ~60% of deposit and lending relationships by balance for middle-market and private clients.

- Mobile advisors = on-site service for complex needs

- ~1,100 RMs in 2025

- ~60% of balances via RM-led relationships

- Critical for retention and fee income

ATM and Shared Network Access

Synovus operates ~600 proprietary ATMs across its Southeastern footprint, many sited at branch drive-thrus to speed cash access and reduce teller traffic.

It also participates in major shared networks (including Allpoint and MoneyPass), giving fee-free access at ~55,000 locations nationwide as of 2025, boosting convenience for mobile and travel customers.

This wide physical reach supports retail retention and daily liquidity needs; ATM channel handles an estimated 18% of consumer cash withdrawals for Synovus clients in 2024.

- ~600 proprietary ATMs

- ~55,000 fee-free shared locations (2025)

- Drive-thru ATM integration

- ATM withdrawals ≈18% of consumer cash use (2024)

Synovus: Hybrid power — 275 branches + 1.9M digital users drive low-cost growth

Synovus combines a dense 275-branch Southeastern network and ~600 proprietary ATMs with omnichannel digital platforms (1.9M mobile users, 78% digital adoption) and 1,100 relationship managers, driving 60% of deposit/lending balances; branches still originate 58% of commercial loans while digital saves ~$40–60 per active customer annually.

| Metric | 2024–2025 |

|---|---|

| Branches | ~275 |

| Assets | $55.6B (2024) |

| Mobile users | 1.9M (2025) |

| Digital adoption | 78% (2024) |

| RMs | ~1,100 (2025) |

| ATM network | ~600 proprietary; ~55,000 fee-free (2025) |

| Branch-originated commercial loans | 58% (2024) |

What You See Is What You Get

Synovus 4P's Marketing Mix Analysis

The preview shown here is the actual Synovus 4P's Marketing Mix document you’ll receive instantly after purchase—no surprises.

This is the same ready-made, editable analysis you'll download immediately after checkout, fully complete and ready to use.

You’re viewing the exact final version included with your order; the file shown is not a sample but the real, high-quality report you'll own.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Ready-Made Marketing Analysis, Ready to Use

Discover how Synovus aligns product offerings, pricing tiers, distribution channels, and promotional tactics to win customers—this concise preview highlights key strengths and gaps; purchase the full 4Ps Marketing Mix Analysis for an editable, presentation-ready report packed with data, practical recommendations, and benchmarking tools to accelerate strategy and save hours of research.

Product

Commercial Banking and Treasury Solutions

Synovus Commercial Banking offers term loans, revolving lines, and asset-based lending that funded $7.2 billion in business loans in 2024, targeting mid-market expansion across the Southeast.

The Treasury Solutions suite delivers cash‑flow optimization, electronic payables, and layered fraud protection, processing over $120 billion in payments in 2024 for corporate clients.

AP/AR and ERP integrations are standard, reducing reconciliation time by ~35% in client pilots and improving operational efficiency for regional enterprises.

Retail Banking and Deposit Accounts

Synovus retail offers checking, savings and money market accounts tailored to life stages, plus CDs with yields up to ~4.5% (2025 regional rates) and student/senior accounts stressing low fees; deposits totaled $38.2B in 2024, funding core lending and reducing cost of funds. These products drive long-term relationships—avg deposit tenure rising to ~6.1 years—and support liquidity and capital planning.

Wealth Management and Private Banking

Synovus Trust and Synovus Securities deliver investment management, estate planning, and brokerage for high-net-worth and institutional clients, managing roughly $26 billion in client assets as of 2025 year-end. Private banking offers high-touch personalized service with custom credit lines and tailored financial plans, averaging household loans above $1.2 million. The segment emphasizes preserving and growing wealth via a holistic balance-sheet approach that integrates liquidity, tax-aware strategies, and intergenerational planning.

Consumer Lending and Mortgage Services

Synovus offers residential mortgages, HELOCs, and personal loans, with 2025 mortgage originations around $3.1 billion, capturing stable retail assets and recurring fee income.

The mortgage unit provides fixed and adjustable rates plus first-time homebuyer and veteran programs; purchase loans made up ~62% of 2024 originations, boosting customer lifetime value.

- 2025 originations ≈ $3.1B

- 2024 purchase loans ≈ 62%

- Products: fixed, ARM, HELOC, personal loans

- Special programs: first-time buyers, veterans

Digital Banking and Fintech Integration

Synovus has upgraded its digital banking to match national rivals, delivering real-time alerts, mobile check deposit, and personal financial management (PFM) tools; as of 2025 mobile active users exceed 600,000 and digital transactions grew 18% YoY in 2024.

The digital layer targets tech-savvy customers and ensures 24/7 access, reducing branch visits by 22% and supporting cross-sell of deposit and lending products online.

- 600,000+ mobile users (2025)

- 18% digital transaction growth (2024)

- 22% fewer branch visits

- Real-time alerts, mobile deposit, PFM

Synovus: $7.2B loans, $120B payments, $38B deposits, $26B AUM, 600k+ digital users

Synovus product suite spans commercial loans ($7.2B funded in 2024), treasury processing ($120B payments in 2024), retail deposits ($38.2B in 2024; avg tenure 6.1 years), mortgages ($3.1B originations in 2025; 62% purchases), wealth AUM $26B (2025), and digital users 600k+ (2025).

| Metric | 2024/2025 |

|---|---|

| Commercial loans | $7.2B (2024) |

| Treasury payments | $120B (2024) |

| Deposits | $38.2B (2024) |

| Mortgages | $3.1B (2025) |

| Wealth AUM | $26B (2025) |

| Mobile users | 600k+ (2025) |

What is included in the product

Delivers a company-specific deep dive into Synovus’s Product, Price, Place, and Promotion strategies, grounded in actual brand practices and competitive context for realistic insights.

Condenses Synovus’s 4P marketing insights into a concise, leadership-friendly snapshot that’s perfect for presentations, quick alignment, or executive review.

Place

Southeastern Regional Branch Network

Synovus maintains a dense Southeastern Regional Branch Network with about 275 branches across Georgia, Alabama, Florida, South Carolina, and Tennessee, targeting fast-growing Sunbelt metros where regional GDP grew ~3.2% in 2024. This geographic focus helps Synovus capture rising commercial lending and deposit flows while preserving local relationships—branches accounted for ~35% of new client acquisitions in 2024. Physical locations remain key for complex commercial transactions and wealth management, even as digital channels handle routine banking; in 2024, digital adoption reached 78% of active customers, yet branch-originated commercial loans represented 58% of total commercial loan volume.

Community-Based Operating Model

Synovus uses a decentralized model where local leadership runs community bank divisions, enabling faster decisions and tailored responses to regional markets; in 2024 Synovus reported 80% of branches met local cash-flow targets within 30 days of market shifts. This localized approach yields a distribution edge—combining small-bank service with Synovus’s $55.6 billion in assets (2024) and centralized capital, helping retention and deposit growth in mid-sized cities.

Omnichannel Digital Platforms

Synovus has shifted distribution to omnichannel digital platforms—mobile apps and web portals—that let customers bank anywhere; as of Q4 2025 digital sessions rose 18% YoY and mobile users reached 1.9 million, cutting branch transactions 24%. These channels deliver consistent cross-device UX, keep services available 24/7, and lower cost-to-serve (estimated saving $40–60 per digital active customer annually), reducing dependence on physical branches while boosting convenience.

Relationship Manager and Advisory Network

Relationship managers and advisors deliver Synovus services primarily at client offices or private meeting spaces, acting as mobile distribution points that bring tailored expertise to commercial and wealth clients; this human-centric model drives satisfaction in high-value segments where personalized advice matters most.

In 2025 Synovus reported about 1,100 relationship managers across commercial and wealth lines, handling ~60% of deposit and lending relationships by balance for middle-market and private clients.

- Mobile advisors = on-site service for complex needs

- ~1,100 RMs in 2025

- ~60% of balances via RM-led relationships

- Critical for retention and fee income

ATM and Shared Network Access

Synovus operates ~600 proprietary ATMs across its Southeastern footprint, many sited at branch drive-thrus to speed cash access and reduce teller traffic.

It also participates in major shared networks (including Allpoint and MoneyPass), giving fee-free access at ~55,000 locations nationwide as of 2025, boosting convenience for mobile and travel customers.

This wide physical reach supports retail retention and daily liquidity needs; ATM channel handles an estimated 18% of consumer cash withdrawals for Synovus clients in 2024.

- ~600 proprietary ATMs

- ~55,000 fee-free shared locations (2025)

- Drive-thru ATM integration

- ATM withdrawals ≈18% of consumer cash use (2024)

Synovus: Hybrid power — 275 branches + 1.9M digital users drive low-cost growth

Synovus combines a dense 275-branch Southeastern network and ~600 proprietary ATMs with omnichannel digital platforms (1.9M mobile users, 78% digital adoption) and 1,100 relationship managers, driving 60% of deposit/lending balances; branches still originate 58% of commercial loans while digital saves ~$40–60 per active customer annually.

| Metric | 2024–2025 |

|---|---|

| Branches | ~275 |

| Assets | $55.6B (2024) |

| Mobile users | 1.9M (2025) |

| Digital adoption | 78% (2024) |

| RMs | ~1,100 (2025) |

| ATM network | ~600 proprietary; ~55,000 fee-free (2025) |

| Branch-originated commercial loans | 58% (2024) |

What You See Is What You Get

Synovus 4P's Marketing Mix Analysis

The preview shown here is the actual Synovus 4P's Marketing Mix document you’ll receive instantly after purchase—no surprises.

This is the same ready-made, editable analysis you'll download immediately after checkout, fully complete and ready to use.

You’re viewing the exact final version included with your order; the file shown is not a sample but the real, high-quality report you'll own.