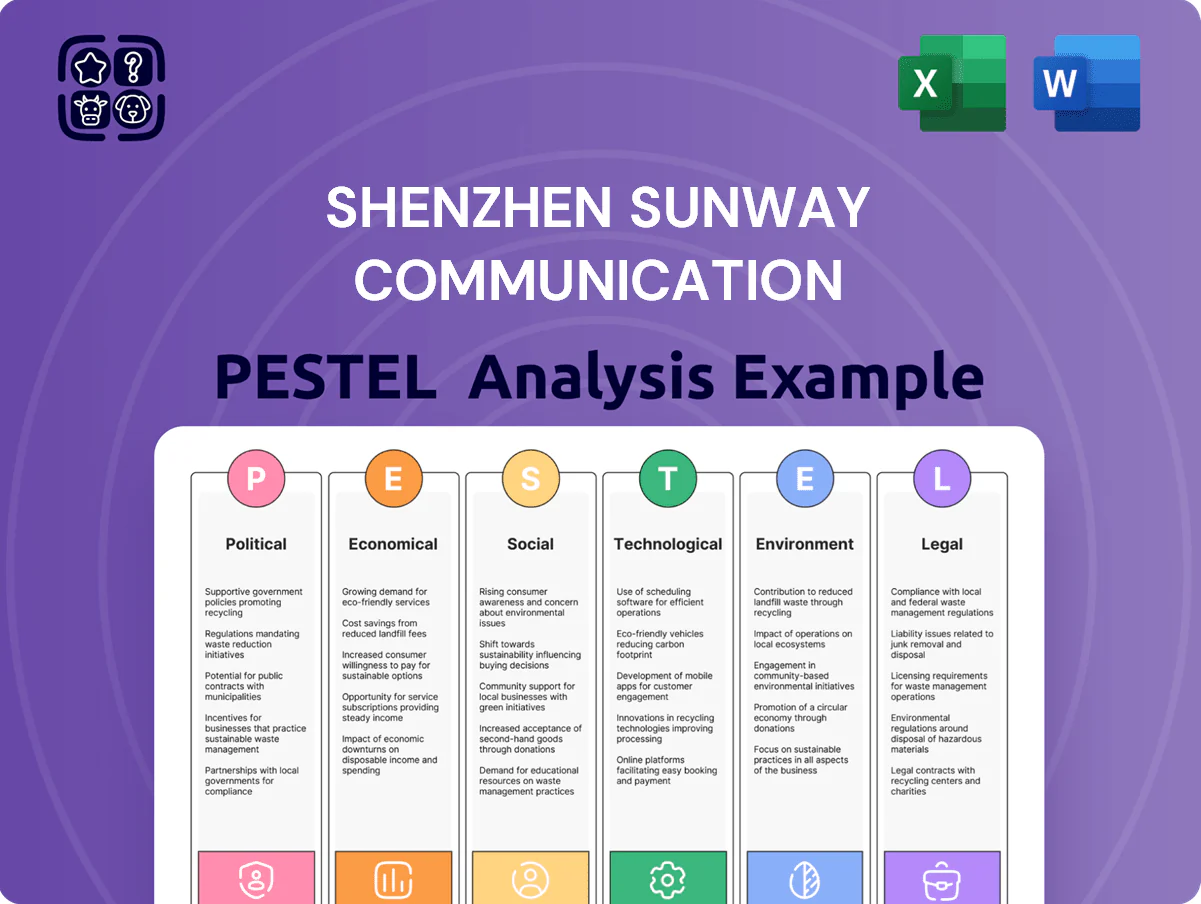

Shenzhen Sunway Communication PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how regulatory shifts, supply-chain dynamics, and rapid tech adoption are shaping Shenzhen Sunway Communication’s competitive outlook—our PESTLE highlights risks and openings you can act on today. Ideal for investors and strategists, the full analysis delivers granular evidence and tactical recommendations. Buy the complete PESTLE now to get immediately usable insights and model-ready data.

Political factors

Geopolitical trade tensions and export controls

The ongoing US-China trade friction through 2025 continues to impact Shenzhen Sunway Communication; US export controls on advanced semiconductors and RF components have cut available imports by an estimated 18% for Chinese device makers in 2024–25, forcing Sunway to accelerate domestic sourcing. The company reported redirecting 32% of procurement to Chinese suppliers in FY2024 and is investing in in-house RF testing to reduce foreign dependency. Navigating diplomatic restrictions remains key to sustaining its role in the global consumer-electronics supply chain.

Government support for high-tech manufacturing

China’s 2024 policy framework allocates over CNY 300 billion to high-tech manufacturing and core telecom components, and Sunway captures subsidy flows and tax incentives tied to domestic 5G/6G supply-chain priorities. National initiatives aiming for technological independence boost Sunway’s R&D spend, reflected in a 2024–25 internal plan to raise R&D investment to 8–10% of revenue (vs. 5.6% in 2023). Political incentives also support capital access and pilot procurements for next-gen antenna systems and RF modules, lowering time-to-market and unit costs.

International telecommunications standardization

Political influence in bodies like the ITU and 3GPP shapes global standards; in 2025 ITU/3GPP decisions influenced markets worth over $1.2 trillion in mobile infrastructure, directly affecting Shenzhen Sunway Communication’s product specs and certification timelines.

As a major Chinese vendor, Sunway faces geopolitical maneuvering over 6G protocols—estimates project 6G-capable equipment market to reach $150–200 billion by 2030—impacting export approvals and partner adoption.

Sunway’s ability to align with evolving standards and secure participation in standards-setting reduces non-tariff barriers; failure could cut addressable export markets by an estimated 10–25% per region based on recent trade-restriction case studies.

Regional industrial cluster policies

The Shenzhen government offers tax breaks and capital support for electronics; in 2024 the Greater Bay Area allocated CNY 48.6 billion to industrial parks and infrastructure, benefiting RF/component clusters.

Specialized parks (over 120 in Shenzhen) and incentives lower Sunway’s effective tax rate and enable shared R&D/logistics, trimming lead times and production costs.

Sunway uses these cluster advantages to optimize output and supply-chain efficiency within the Greater Bay Area.

- 2024 GBA industrial fund CNY 48.6bn

- 120+ specialized parks in Shenzhen

- Reduced taxes and shared R&D/logistics for Sunway

Global supply chain diversification mandates

- Target 15–25% capacity shift outside China by 2026

- Focus regions: Vietnam, Mexico

- Over 60% of top smartphone and 70% of Tier 1 auto OEMs require diversification (2024)

Sunway pivots: 32% domestic sourcing, 18% RF import cut, R&D to 8–10%

US export controls reduced advanced RF imports ~18% in 2024–25; Sunway shifted 32% procurement to domestic suppliers in FY2024 and plans 15–25% capacity shift to Vietnam/Mexico by 2026. China allocated CNY 300bn+ to high-tech manufacturing; GBA provided CNY 48.6bn in 2024. Sunway raising R&D to 8–10% of revenue (2024–25 plan) from 5.6% in 2023.

| Metric | 2023 | 2024–25 |

|---|---|---|

| Domestic procurement | — | 32% |

| Import reduction (RF) | — | 18% |

| R&D spend (% revenue) | 5.6% | 8–10% |

| GBA fund | — | CNY 48.6bn |

| National high-tech allocation | — | CNY 300bn+ |

What is included in the product

Explores how macro-environmental factors uniquely impact Shenzhen Sunway Communication across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to inform executives, investors, and strategists.

A concise, visually segmented PESTLE summary of Shenzhen Sunway Communication that’s ready to drop into presentations or planning sessions, easing cross-team alignment on regulatory, technological, economic and market risks.

Economic factors

Recovery of the consumer electronics market

By end-2025 global smartphone shipments recovered to about 1.3 billion units (up ~4% YoY) and PC shipments ticked up 2–3%, driving higher demand for Sunway’s antennas and wireless charging modules; FY2025 component revenue for tier-1 suppliers rose ~6–8% per industry reports. Improved consumer sentiment in the US, EU and China supported greater adoption of premium devices that use advanced RF components, boosting ASPs for complex modules by mid-single digits. Higher 5G handset penetration (≈55% of global base) directly expands TAM for Sunway’s RF product lines.

Growth in the automotive electronics sector

The global EV stock surpassed 26 million in 2024, and rising ADAS/ autonomous vehicle deployments boost demand for high-end antenna arrays and sensors, offering Shenzhen Sunway Communication sizable revenue diversification into automotive electronics; per Q3 2025 industry forecasts, per-vehicle antenna/sensor content is expected to grow 3–5x by 2030, supporting Sunway’s shift to automotive-grade components and reducing exposure to mobile-phone market volatility, which saw smartphone shipments decline ~8% in 2024.

Currency exchange rate fluctuations

As a firm with roughly 45% of 2024 revenue from overseas markets, Shenzhen Sunway is highly sensitive to RMB/USD moves; the RMB fell about 3.8% vs USD in 2024, squeezing export margins and lifting imported component costs by an estimated 2–4% per point of depreciation. Currency swings can alter Sunway’s competitiveness; management reported hedging covering ~60% of forecasted FX exposure in 2024 using forwards and options to protect margins.

Fluctuating raw material and energy costs

The price of copper rose ~15% in 2024 and rare earths surged ~22% amid supply tightness, directly raising RF component costs for Sunway and pressuring gross margins.

Global demand swings and shipping disruptions in 2024–2025 caused spot metal premiums of up to 10–18%, prompting volatility in production overheads.

Sunway pursues process optimization, yield improvements and multi-year supplier contracts covering ~60% of purchases to hedge inflationary risk.

- 2024 copper +15%, rare earths +22%

- Spot premiums: 10–18% during 2024–2025

- Long-term contracts cover ~60% of procurement

Interest rate environments and capital expenditure

Global interest rate trends raised Sunway’s average borrowing cost to about 4.2% in 2024–2025, increasing capex hurdle rates for its capacity expansion and advanced manufacturing projects.

Although rates stabilized late 2025, projected WACC for new projects remains near 8–9%, keeping cost of capital a key gating factor for large-scale investments.

Sunway’s disciplined debt management—net debt/EBITDA around 1.1x in FY2025—supports sustainable growth despite a higher-rate backdrop.

- Avg borrowing cost ~4.2% (2024–25)

- Implied WACC for new projects ~8–9%

- Net debt/EBITDA ≈1.1x (FY2025)

Sunway: TAM expands on device & EV boom; margin squeeze from commodities, FX, higher WACC

Favorable 2024–25 device recovery (smartphones ~1.3bn, 5G penetration ~55%) and EV growth (>26m stock) expand Sunway’s TAM; commodity inflation (copper +15%, rare earths +22%) and RMB -3.8% vs USD compressed margins; borrowing cost ~4.2% raised project WACC to ~8–9% while net debt/EBITDA ≈1.1x.

| Metric | 2024–25 |

|---|---|

| Smartphones | ~1.3bn |

| 5G pen. | ~55% |

| EV stock | >26m |

| Copper | +15% |

| Rare earths | +22% |

| RMB vs USD | -3.8% |

| Borrowing cost | ~4.2% |

| WACC | 8–9% |

| Net debt/EBITDA | ≈1.1x |

Preview Before You Purchase

Shenzhen Sunway Communication PESTLE Analysis

The preview shown here is the exact Shenzhen Sunway Communication PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or reporting.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how regulatory shifts, supply-chain dynamics, and rapid tech adoption are shaping Shenzhen Sunway Communication’s competitive outlook—our PESTLE highlights risks and openings you can act on today. Ideal for investors and strategists, the full analysis delivers granular evidence and tactical recommendations. Buy the complete PESTLE now to get immediately usable insights and model-ready data.

Political factors

Geopolitical trade tensions and export controls

The ongoing US-China trade friction through 2025 continues to impact Shenzhen Sunway Communication; US export controls on advanced semiconductors and RF components have cut available imports by an estimated 18% for Chinese device makers in 2024–25, forcing Sunway to accelerate domestic sourcing. The company reported redirecting 32% of procurement to Chinese suppliers in FY2024 and is investing in in-house RF testing to reduce foreign dependency. Navigating diplomatic restrictions remains key to sustaining its role in the global consumer-electronics supply chain.

Government support for high-tech manufacturing

China’s 2024 policy framework allocates over CNY 300 billion to high-tech manufacturing and core telecom components, and Sunway captures subsidy flows and tax incentives tied to domestic 5G/6G supply-chain priorities. National initiatives aiming for technological independence boost Sunway’s R&D spend, reflected in a 2024–25 internal plan to raise R&D investment to 8–10% of revenue (vs. 5.6% in 2023). Political incentives also support capital access and pilot procurements for next-gen antenna systems and RF modules, lowering time-to-market and unit costs.

International telecommunications standardization

Political influence in bodies like the ITU and 3GPP shapes global standards; in 2025 ITU/3GPP decisions influenced markets worth over $1.2 trillion in mobile infrastructure, directly affecting Shenzhen Sunway Communication’s product specs and certification timelines.

As a major Chinese vendor, Sunway faces geopolitical maneuvering over 6G protocols—estimates project 6G-capable equipment market to reach $150–200 billion by 2030—impacting export approvals and partner adoption.

Sunway’s ability to align with evolving standards and secure participation in standards-setting reduces non-tariff barriers; failure could cut addressable export markets by an estimated 10–25% per region based on recent trade-restriction case studies.

Regional industrial cluster policies

The Shenzhen government offers tax breaks and capital support for electronics; in 2024 the Greater Bay Area allocated CNY 48.6 billion to industrial parks and infrastructure, benefiting RF/component clusters.

Specialized parks (over 120 in Shenzhen) and incentives lower Sunway’s effective tax rate and enable shared R&D/logistics, trimming lead times and production costs.

Sunway uses these cluster advantages to optimize output and supply-chain efficiency within the Greater Bay Area.

- 2024 GBA industrial fund CNY 48.6bn

- 120+ specialized parks in Shenzhen

- Reduced taxes and shared R&D/logistics for Sunway

Global supply chain diversification mandates

- Target 15–25% capacity shift outside China by 2026

- Focus regions: Vietnam, Mexico

- Over 60% of top smartphone and 70% of Tier 1 auto OEMs require diversification (2024)

Sunway pivots: 32% domestic sourcing, 18% RF import cut, R&D to 8–10%

US export controls reduced advanced RF imports ~18% in 2024–25; Sunway shifted 32% procurement to domestic suppliers in FY2024 and plans 15–25% capacity shift to Vietnam/Mexico by 2026. China allocated CNY 300bn+ to high-tech manufacturing; GBA provided CNY 48.6bn in 2024. Sunway raising R&D to 8–10% of revenue (2024–25 plan) from 5.6% in 2023.

| Metric | 2023 | 2024–25 |

|---|---|---|

| Domestic procurement | — | 32% |

| Import reduction (RF) | — | 18% |

| R&D spend (% revenue) | 5.6% | 8–10% |

| GBA fund | — | CNY 48.6bn |

| National high-tech allocation | — | CNY 300bn+ |

What is included in the product

Explores how macro-environmental factors uniquely impact Shenzhen Sunway Communication across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to inform executives, investors, and strategists.

A concise, visually segmented PESTLE summary of Shenzhen Sunway Communication that’s ready to drop into presentations or planning sessions, easing cross-team alignment on regulatory, technological, economic and market risks.

Economic factors

Recovery of the consumer electronics market

By end-2025 global smartphone shipments recovered to about 1.3 billion units (up ~4% YoY) and PC shipments ticked up 2–3%, driving higher demand for Sunway’s antennas and wireless charging modules; FY2025 component revenue for tier-1 suppliers rose ~6–8% per industry reports. Improved consumer sentiment in the US, EU and China supported greater adoption of premium devices that use advanced RF components, boosting ASPs for complex modules by mid-single digits. Higher 5G handset penetration (≈55% of global base) directly expands TAM for Sunway’s RF product lines.

Growth in the automotive electronics sector

The global EV stock surpassed 26 million in 2024, and rising ADAS/ autonomous vehicle deployments boost demand for high-end antenna arrays and sensors, offering Shenzhen Sunway Communication sizable revenue diversification into automotive electronics; per Q3 2025 industry forecasts, per-vehicle antenna/sensor content is expected to grow 3–5x by 2030, supporting Sunway’s shift to automotive-grade components and reducing exposure to mobile-phone market volatility, which saw smartphone shipments decline ~8% in 2024.

Currency exchange rate fluctuations

As a firm with roughly 45% of 2024 revenue from overseas markets, Shenzhen Sunway is highly sensitive to RMB/USD moves; the RMB fell about 3.8% vs USD in 2024, squeezing export margins and lifting imported component costs by an estimated 2–4% per point of depreciation. Currency swings can alter Sunway’s competitiveness; management reported hedging covering ~60% of forecasted FX exposure in 2024 using forwards and options to protect margins.

Fluctuating raw material and energy costs

The price of copper rose ~15% in 2024 and rare earths surged ~22% amid supply tightness, directly raising RF component costs for Sunway and pressuring gross margins.

Global demand swings and shipping disruptions in 2024–2025 caused spot metal premiums of up to 10–18%, prompting volatility in production overheads.

Sunway pursues process optimization, yield improvements and multi-year supplier contracts covering ~60% of purchases to hedge inflationary risk.

- 2024 copper +15%, rare earths +22%

- Spot premiums: 10–18% during 2024–2025

- Long-term contracts cover ~60% of procurement

Interest rate environments and capital expenditure

Global interest rate trends raised Sunway’s average borrowing cost to about 4.2% in 2024–2025, increasing capex hurdle rates for its capacity expansion and advanced manufacturing projects.

Although rates stabilized late 2025, projected WACC for new projects remains near 8–9%, keeping cost of capital a key gating factor for large-scale investments.

Sunway’s disciplined debt management—net debt/EBITDA around 1.1x in FY2025—supports sustainable growth despite a higher-rate backdrop.

- Avg borrowing cost ~4.2% (2024–25)

- Implied WACC for new projects ~8–9%

- Net debt/EBITDA ≈1.1x (FY2025)

Sunway: TAM expands on device & EV boom; margin squeeze from commodities, FX, higher WACC

Favorable 2024–25 device recovery (smartphones ~1.3bn, 5G penetration ~55%) and EV growth (>26m stock) expand Sunway’s TAM; commodity inflation (copper +15%, rare earths +22%) and RMB -3.8% vs USD compressed margins; borrowing cost ~4.2% raised project WACC to ~8–9% while net debt/EBITDA ≈1.1x.

| Metric | 2024–25 |

|---|---|

| Smartphones | ~1.3bn |

| 5G pen. | ~55% |

| EV stock | >26m |

| Copper | +15% |

| Rare earths | +22% |

| RMB vs USD | -3.8% |

| Borrowing cost | ~4.2% |

| WACC | 8–9% |

| Net debt/EBITDA | ≈1.1x |

Preview Before You Purchase

Shenzhen Sunway Communication PESTLE Analysis

The preview shown here is the exact Shenzhen Sunway Communication PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or reporting.