Taiheiyo Cement Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

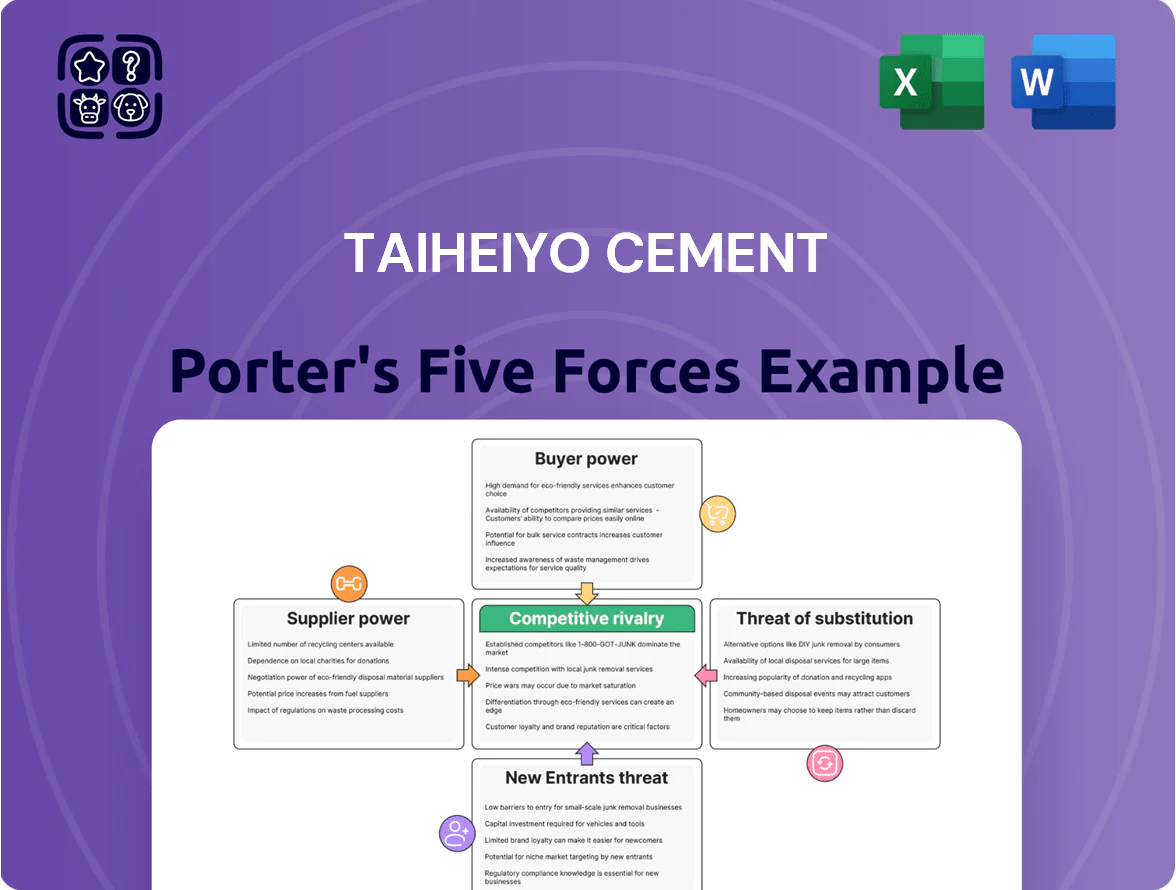

Taiheiyo Cement operates in a capital‑intensive, regionally concentrated market where supplier ties, heavy regulation, and scale advantages limit new entrants but intensify rivalry among incumbents, while substitutes and buyer negotiating power create margin pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiheiyo Cement’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy and Fuel Price Volatility

Energy-intensive cement production depends on coal, electricity, and alternative fuels; as of Q4 2025 Taiheiyo Cement faced coal import cost swings of ±18% year-on-year and Japan retail electricity tariff rises of ~7% in 2024–25, leaving margins exposed to geopolitics.

Waste-derived fuels cut thermal coal use by about 12% in 2025, lowering fuel spend but not enough to erase supplier leverage; major energy suppliers still influence operating EBITDA, which fell 2.3 percentage points in 2025 on higher fuel costs.

Raw Material Resource Ownership

Taiheiyo Cement reduces supplier power by owning about 1.2 billion tonnes of limestone reserves (company disclosure 2024), securing clinker feedstock and cutting raw-mineral purchase needs versus peers.

That vertical integration lowers bargaining leverage of external mineral suppliers, making input cost exposure more stable; clinker input share ~70% of production cost.

Still, specialised additives and gypsum—sourced from a few chemical/industrial suppliers—retain pricing power and accounted for roughly 8–12% of COGS in FY2024, so supply-price risk persists.

Logistics and Distribution Dependencies

Taiheiyo Cement depends on shipping, trucking and rail to move heavy clinker and cement; logistics account for roughly 8–12% of cement COGS industry-wide, so transport disruption hits margins fast.

Labor shortages in Japan’s logistics sector raised driver and dock-worker wages ~6–9% by 2025, boosting transportation providers’ bargaining power and raising spot freight rates.

Taiheiyo must offset higher external transport costs against internal fleet and terminal investments; owning more distribution assets could trim per-ton logistics cost by an estimated 10–15%.

Decarbonization Technology Providers

Suppliers of CCUS (carbon capture, utilization, storage) technologies exert growing leverage as Taiheiyo Cement pursues GX targets; only a handful of global firms supply proven large-scale systems, pushing up prices and lead times. Taiheiyo needs specialized equipment and EPC services to cut CO2 by ~30% by 2030 (company target), so vendor switching costs and certification barriers raise supplier bargaining power. CCUS capital intensity (plant CAPEX often >$200/ton CO2 capacity) tightens supplier influence.

- Few global CCUS vendors — limited competition

- High CAPEX: ~$200+/t CO2 capacity

- Long lead times, skilled EPC needs

- Vendor lock via certification and O&M

Environmental Compliance and Carbon Credits

Regulatory bodies act as indirect suppliers by issuing carbon credits and permits, effectively selling the right to operate; in FY2025 Japan’s carbon price floor reached about ¥7,000/ton CO2 (≈$47), making emissions a non-negotiable input cost for Taiheiyo Cement.

This fixed supply-side constraint forces Taiheiyo to follow government-set carbon pricing and strict environmental standards, reducing bargaining room and squeezing margins unless emissions fall.

- FY2025 Japan carbon price floor ≈ ¥7,000/ton CO2

- Emissions cost treated as fixed input, not negotiable

- Permits/carbon credits = operational gatekeepers

- Taiheiyo must absorb or pass on costs; little supplier leverage

Suppliers wield material power: input shocks cut 2025 EBITDA margin 2.3ppt

Suppliers hold moderate-to-high power: energy and transport swings cut 2025 EBITDA margin 2.3ppt; coal import cost volatility ±18% YoY and Japan electricity tariffs +7% in 2024–25; vertical limestone reserves (1.2bn t, 2024) reduce mineral leverage, but additives/gypsum (8–12% COGS), logistics (8–12% COGS) and scarce CCUS vendors (CAPEX ≈$200+/t CO2) keep supplier risk material.

| Input | Metric | 2024–25 |

|---|---|---|

| Coal cost volatility | ±YoY | ±18% |

| Electricity tariffs | change | +7% |

| Limestone reserves | company disclosure | 1.2bn t |

| Additives/gypsum | % of COGS | 8–12% |

| Logistics | % of COGS | 8–12% |

| CCUS CAPEX | $ per t CO2 | ≈200+ |

What is included in the product

Tailored exclusively for Taiheiyo Cement, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—highlighting impacts on pricing, margins, and strategic positioning for investors and strategists.

A concise Porter's Five Forces snapshot for Taiheiyo Cement—distills competitive pressures into one-sheet clarity for faster strategic decisions.

Customers Bargaining Power

Concentration of Major Construction Firms

Commodity Nature of Standard Cement

Standard Portland cement is treated as a commodity, with little brand differentiation for general construction, so 72% of Japanese buyers cite price and delivery as top switches drivers in a 2024 JCI survey.

Customers face low technical barriers to change suppliers, letting them shift volumes rapidly; Taiheiyo Cement (2024 sales ¥1.1 trillion) must thus match price moves and 95% on-time delivery benchmarks to keep share.

Public Sector Infrastructure Procurement

Government agencies for public works—bridges, roads, coastal defenses—are major buyers of cement for Taiheiyo Cement; Japan’s public investment in social capital was ¥15.8 trillion in FY2024, keeping demand steady. Procurement uses competitive bidding and often requires environmental certifications like CASBEE or low-CO2 concrete specs, which pushes suppliers to match low prices and standards. Transparent rules and fixed budgets limit Taiheiyo’s pricing power on state projects.

Growth of Green Building Standards

By end-2025, demand for LEED and low-carbon materials rises: 48% of global developers target net-zero construction, pushing buyers to insist on eco-friendly cement at competitive prices; customers can now leverage volume and spec requirements to secure lower margins from suppliers.

Taiheiyo Cement must fast-track low-CO2 blends and CCUS-linked products or risk losing 10–20% of high-margin institutional contracts to nimble rivals; R&D and capex reallocation are urgent.

- 48% developers target net-zero by 2025

- Buyers demand low-carbon cement, price pressure rises

- 10–20% high-margin contract risk for Taiheiyo

- Action: accelerate low-CO2 blends, CCUS, R&D

Low Switching Costs for Private Developers

Low switching costs let many residential and commercial developers pivot from Taiheiyo Cement to rivals like Mitsubishi UBE Cement if price gaps exceed a few percent; Japan construction procurement often awards on price and delivery, and a 2024 trade report showed price sensitivity rising as margins fell below 5% for small builders.

This forces Taiheiyo to sustain high customer service and technical support—on-site mix design, QC labs, and 24/7 logistics—to protect share and keep repeat purchases.

- Developers switch easily if price gap >~3–5%

- Compliance with national codes equalizes suppliers

- Service, technical support, and logistics drive loyalty

Buyers' Price Power Threatens 10–20% High‑Margin Contracts as Net‑Zero Push Grows

| Metric | Value |

|---|---|

| FY2024 sales | ¥1.1tn |

| Contractor revenue share | 28% JP / 12% US |

| Buyer price sensitivity | 72% (JCI 2024) |

| Public capex FY2024 | ¥15.8trn |

| Net-zero developers by 2025 | 48% |

What You See Is What You Get

Taiheiyo Cement Porter's Five Forces Analysis

This preview shows the exact Taiheiyo Cement Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: the analysis shown is the final deliverable, ready for immediate use upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Taiheiyo Cement operates in a capital‑intensive, regionally concentrated market where supplier ties, heavy regulation, and scale advantages limit new entrants but intensify rivalry among incumbents, while substitutes and buyer negotiating power create margin pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Taiheiyo Cement’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy and Fuel Price Volatility

Energy-intensive cement production depends on coal, electricity, and alternative fuels; as of Q4 2025 Taiheiyo Cement faced coal import cost swings of ±18% year-on-year and Japan retail electricity tariff rises of ~7% in 2024–25, leaving margins exposed to geopolitics.

Waste-derived fuels cut thermal coal use by about 12% in 2025, lowering fuel spend but not enough to erase supplier leverage; major energy suppliers still influence operating EBITDA, which fell 2.3 percentage points in 2025 on higher fuel costs.

Raw Material Resource Ownership

Taiheiyo Cement reduces supplier power by owning about 1.2 billion tonnes of limestone reserves (company disclosure 2024), securing clinker feedstock and cutting raw-mineral purchase needs versus peers.

That vertical integration lowers bargaining leverage of external mineral suppliers, making input cost exposure more stable; clinker input share ~70% of production cost.

Still, specialised additives and gypsum—sourced from a few chemical/industrial suppliers—retain pricing power and accounted for roughly 8–12% of COGS in FY2024, so supply-price risk persists.

Logistics and Distribution Dependencies

Taiheiyo Cement depends on shipping, trucking and rail to move heavy clinker and cement; logistics account for roughly 8–12% of cement COGS industry-wide, so transport disruption hits margins fast.

Labor shortages in Japan’s logistics sector raised driver and dock-worker wages ~6–9% by 2025, boosting transportation providers’ bargaining power and raising spot freight rates.

Taiheiyo must offset higher external transport costs against internal fleet and terminal investments; owning more distribution assets could trim per-ton logistics cost by an estimated 10–15%.

Decarbonization Technology Providers

Suppliers of CCUS (carbon capture, utilization, storage) technologies exert growing leverage as Taiheiyo Cement pursues GX targets; only a handful of global firms supply proven large-scale systems, pushing up prices and lead times. Taiheiyo needs specialized equipment and EPC services to cut CO2 by ~30% by 2030 (company target), so vendor switching costs and certification barriers raise supplier bargaining power. CCUS capital intensity (plant CAPEX often >$200/ton CO2 capacity) tightens supplier influence.

- Few global CCUS vendors — limited competition

- High CAPEX: ~$200+/t CO2 capacity

- Long lead times, skilled EPC needs

- Vendor lock via certification and O&M

Environmental Compliance and Carbon Credits

Regulatory bodies act as indirect suppliers by issuing carbon credits and permits, effectively selling the right to operate; in FY2025 Japan’s carbon price floor reached about ¥7,000/ton CO2 (≈$47), making emissions a non-negotiable input cost for Taiheiyo Cement.

This fixed supply-side constraint forces Taiheiyo to follow government-set carbon pricing and strict environmental standards, reducing bargaining room and squeezing margins unless emissions fall.

- FY2025 Japan carbon price floor ≈ ¥7,000/ton CO2

- Emissions cost treated as fixed input, not negotiable

- Permits/carbon credits = operational gatekeepers

- Taiheiyo must absorb or pass on costs; little supplier leverage

Suppliers wield material power: input shocks cut 2025 EBITDA margin 2.3ppt

Suppliers hold moderate-to-high power: energy and transport swings cut 2025 EBITDA margin 2.3ppt; coal import cost volatility ±18% YoY and Japan electricity tariffs +7% in 2024–25; vertical limestone reserves (1.2bn t, 2024) reduce mineral leverage, but additives/gypsum (8–12% COGS), logistics (8–12% COGS) and scarce CCUS vendors (CAPEX ≈$200+/t CO2) keep supplier risk material.

| Input | Metric | 2024–25 |

|---|---|---|

| Coal cost volatility | ±YoY | ±18% |

| Electricity tariffs | change | +7% |

| Limestone reserves | company disclosure | 1.2bn t |

| Additives/gypsum | % of COGS | 8–12% |

| Logistics | % of COGS | 8–12% |

| CCUS CAPEX | $ per t CO2 | ≈200+ |

What is included in the product

Tailored exclusively for Taiheiyo Cement, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats—highlighting impacts on pricing, margins, and strategic positioning for investors and strategists.

A concise Porter's Five Forces snapshot for Taiheiyo Cement—distills competitive pressures into one-sheet clarity for faster strategic decisions.

Customers Bargaining Power

Concentration of Major Construction Firms

Commodity Nature of Standard Cement

Standard Portland cement is treated as a commodity, with little brand differentiation for general construction, so 72% of Japanese buyers cite price and delivery as top switches drivers in a 2024 JCI survey.

Customers face low technical barriers to change suppliers, letting them shift volumes rapidly; Taiheiyo Cement (2024 sales ¥1.1 trillion) must thus match price moves and 95% on-time delivery benchmarks to keep share.

Public Sector Infrastructure Procurement

Government agencies for public works—bridges, roads, coastal defenses—are major buyers of cement for Taiheiyo Cement; Japan’s public investment in social capital was ¥15.8 trillion in FY2024, keeping demand steady. Procurement uses competitive bidding and often requires environmental certifications like CASBEE or low-CO2 concrete specs, which pushes suppliers to match low prices and standards. Transparent rules and fixed budgets limit Taiheiyo’s pricing power on state projects.

Growth of Green Building Standards

By end-2025, demand for LEED and low-carbon materials rises: 48% of global developers target net-zero construction, pushing buyers to insist on eco-friendly cement at competitive prices; customers can now leverage volume and spec requirements to secure lower margins from suppliers.

Taiheiyo Cement must fast-track low-CO2 blends and CCUS-linked products or risk losing 10–20% of high-margin institutional contracts to nimble rivals; R&D and capex reallocation are urgent.

- 48% developers target net-zero by 2025

- Buyers demand low-carbon cement, price pressure rises

- 10–20% high-margin contract risk for Taiheiyo

- Action: accelerate low-CO2 blends, CCUS, R&D

Low Switching Costs for Private Developers

Low switching costs let many residential and commercial developers pivot from Taiheiyo Cement to rivals like Mitsubishi UBE Cement if price gaps exceed a few percent; Japan construction procurement often awards on price and delivery, and a 2024 trade report showed price sensitivity rising as margins fell below 5% for small builders.

This forces Taiheiyo to sustain high customer service and technical support—on-site mix design, QC labs, and 24/7 logistics—to protect share and keep repeat purchases.

- Developers switch easily if price gap >~3–5%

- Compliance with national codes equalizes suppliers

- Service, technical support, and logistics drive loyalty

Buyers' Price Power Threatens 10–20% High‑Margin Contracts as Net‑Zero Push Grows

| Metric | Value |

|---|---|

| FY2024 sales | ¥1.1tn |

| Contractor revenue share | 28% JP / 12% US |

| Buyer price sensitivity | 72% (JCI 2024) |

| Public capex FY2024 | ¥15.8trn |

| Net-zero developers by 2025 | 48% |

What You See Is What You Get

Taiheiyo Cement Porter's Five Forces Analysis

This preview shows the exact Taiheiyo Cement Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full, professionally formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: the analysis shown is the final deliverable, ready for immediate use upon payment.