Takara Bio Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

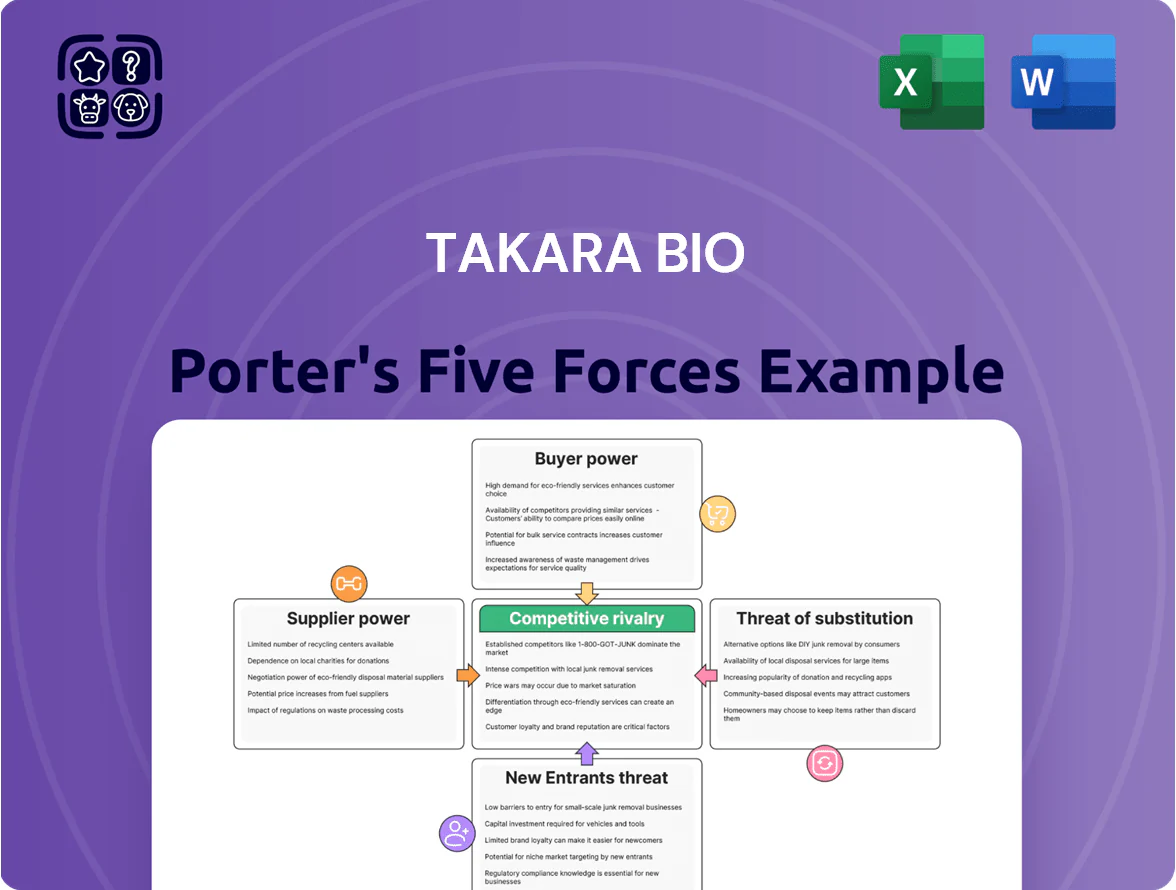

Takara Bio operates in a high-stakes biotech services market where supplier specialization, tech-driven differentiation, regulatory barriers, and growing customer sophistication shape competitive tension—this snapshot highlights key pressure points and strategic levers for the company.

Suppliers Bargaining Power

Specialized Raw Material Providers

Takara Bio relies on a small set of certified vendors for high-purity enzymes and clinical-grade reagents, giving specialized suppliers moderate bargaining power over prices and 4–12 week lead times; commoditized chemicals exert little pressure. Clinical and gene therapy quality rules mean supplier switches are costly, so by 2025 Takara had expanded vetted suppliers by ~35% and diversified sourcing across Asia, Europe, and North America to cut regional disruption risk.

Logistics and Cold Chain Partners

Many Takara Bio reagents need ultra-low temperature transport, so dependence on a handful of specialized cold-chain carriers raises supplier power; global ultra-cold logistics capacity tightened after 2021, with industry rates up ~15–25% by 2023 and spot surges during 2024 peak seasons. Fluctuations in fuel and electricity pushed cold-storage operating costs up about 8–12% in 2023, squeezing reagent margins. Takara Bio therefore signs multi-year agreements and pays premium surcharges to secure priority handling and stable pricing across 60+ export markets. This strategic buying reduces disruption risk but increases fixed distribution commitments.

Proprietary Technology Licensors

Takara Bio relies on patented tech and sequences from universities and biotech firms; licensing fees and contract terms act as supplier power that raise R&D costs and time to market.

Through 2025, CRISPR and viral vector patent access added an estimated 5–15% to early-stage program budgets industry-wide, so Takara factors these fees into pricing and pipeline decisions.

The company counters by investing in internal R&D—R&D spend was ¥29.4 billion in FY2024—aiming to create proprietary alternatives and cut external IP dependence.

Laboratory Equipment Manufacturers

Takara Bio depends on high-end bioreactors, sequencers, and automated liquid handlers; these suppliers exert strong bargaining power because their instruments require proprietary consumables and expensive maintenance—industry data shows consumables can be 20–40% of lifecycle costs and service contracts 5–10% annually.

Switching vendors risks six- to 12-month regulatory re-validation and CAPEX write-offs often exceeding $1–3M per line, so Takara secures long-term service agreements to stabilize costs and ensure uptime.

- Proprietary consumables: 20–40% lifecycle cost

- Service contracts: 5–10% annual cost

- Vendor switch: 6–12 months re-validation

- CAPEX risk: $1–3M per production line

- Mitigation: long-term service agreements

Global Chemical Commodity Pricing

- Commodity-driven plastics up 8–12% (2024–mid‑2025)

- Regulatory compliance added ~3–5% cost (late 2025)

- Bulk/forward buying reduces volatility ~60%

High supplier power: specialized inputs drive costs, lead times & regional risk

Supplier power is moderate-to-high: specialized enzyme/IP/cold-chain and proprietary instruments drive 5–40% added costs, 4–12 week lead times, and 6–12 month re-validation risks; Takara cut regional risk by +35% vetted suppliers by 2025, FY2024 R&D ¥29.4B, bulk/forward buying trims input variance ~60%, commodity plastics +8–12% (2024–mid‑2025), regs added ~3–5% (late 2025).

What is included in the product

Tailored exclusively for Takara Bio, this Porter's Five Forces overview uncovers key competitive drivers, supplier/buyer influence, entry barriers, substitutes, and emerging threats that shape its pricing power and strategic positioning.

Quick five-forces snapshot tailored to Takara Bio—ideal for rapid strategic decisions and investor briefs.

Customers Bargaining Power

Large Pharmaceutical and Biotech Corporations

Major pharma and biotech buyers (e.g., Pfizer, Roche) buy reagents and CDMO services in large volumes, giving them strong bargaining power through bulk discounts and strict SLAs that press Takara Bio’s margins; top 10 pharma account for roughly 40% of industry CDMO spend in 2024.

Academic and Government Research Institutions

Academic and government researchers form a large, price-sensitive segment for Takara Bio, often limited by fixed grant funds—US NIH budgets were about $48.5B in FY2024—so individual labs have low bargaining power. Still, collective influence via institutional procurement portals and competitive bidding pressures list prices down; academic customers are highly mobile and will switch if lower-cost products match performance. Takara defends premiums with extensive technical support and proven high-performance kits, keeping renewal rates above industry averages (typically 70–85%).

Clinical Research Organizations and CDMO Clients

Clients seeking CDMO services for cell and gene therapies wield strong bargaining power via strict selection: 78% of sponsors audit facilities and 64% list regulatory compliance and prior viral vector runs as top criteria (2024 industry survey).

Switching mid-trial is prohibitively costly—average tech transfer and delay costs exceed $15–30M and 6–12 months—so bargaining peaks at initial vendor choice.

Takara Bio counters by securing long-term contracts, demonstrating a 22% year-over-year retention rate for cell/gene clients in 2024 and investing in audit-ready GMP suites to keep clients inside its ecosystem.

Switching Costs and Brand Loyalty

Switching reagents risks inconsistent results, creating technical lock-in that lowers immediate customer bargaining power for labs standardized on Takara Bio kits.

In 2025, open-platform instruments rose ~18% in academic labs, easing trials of alternatives, slightly increasing buyer leverage.

Takara Bio counters by rolling product updates and QC; its reagent reliability claims cut customer churn—company reported 6% revenue growth in 2024 from core kits.

- Technical lock-in reduces short-term buyer power

- Open-platform uptake +18% in 2025 raises switching tests

- Takara’s continuous innovation +6% 2024 kit revenue

Consolidation of Healthcare and Research Systems

Consolidation of hospital systems and research networks has boosted centralized purchasing: by 2024, the top 100 US health systems accounted for ~60% of inpatient admissions, increasing buyers’ leverage.

These large groups push master service agreements across sites, forcing Takara Bio to lower prices and offer integrated digital procurement and service bundles.

Takara Bio created dedicated account teams in 2023 to manage high-volume institutional contracts and speed onboarding.

- Top 100 US systems ≈60% inpatient share

- Master agreements cover multi-site procurement

- Price and digital integration pressure on Takara Bio

- Dedicated accounts teams launched 2023

Concentrated buyers vs. Takara’s technical lock‑in cushions pricing pressure

Customers hold mixed bargaining power: big pharma/CDMO sponsors (top 10 ≈40% CDMO spend) and consolidated health systems (top 100 US ≈60% inpatient share) drive strong leverage on price and SLAs, while individual academic labs (NIH ~$48.5B FY2024) have low power but are price-sensitive; technical lock-in and Takara’s 22% cell/gene retention (2024) and 6% kit revenue growth (2024) mitigate buyer pressure.

| Metric | Value |

|---|---|

| Top10 share CDMO spend (2024) | ≈40% |

| NIH budget (FY2024) | $48.5B |

| Top100 US inpatient share (2024) | ≈60% |

| Cell/gene client retention (2024) | 22% YoY |

| Kit revenue growth (2024) | 6% YoY |

Preview the Actual Deliverable

Takara Bio Porter's Five Forces Analysis

This preview shows the exact Takara Bio Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

You're previewing the final deliverable: ready for immediate use with comprehensive insights into competitive rivalry, supplier and buyer power, threats of new entrants and substitutes.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Takara Bio operates in a high-stakes biotech services market where supplier specialization, tech-driven differentiation, regulatory barriers, and growing customer sophistication shape competitive tension—this snapshot highlights key pressure points and strategic levers for the company.

Suppliers Bargaining Power

Specialized Raw Material Providers

Takara Bio relies on a small set of certified vendors for high-purity enzymes and clinical-grade reagents, giving specialized suppliers moderate bargaining power over prices and 4–12 week lead times; commoditized chemicals exert little pressure. Clinical and gene therapy quality rules mean supplier switches are costly, so by 2025 Takara had expanded vetted suppliers by ~35% and diversified sourcing across Asia, Europe, and North America to cut regional disruption risk.

Logistics and Cold Chain Partners

Many Takara Bio reagents need ultra-low temperature transport, so dependence on a handful of specialized cold-chain carriers raises supplier power; global ultra-cold logistics capacity tightened after 2021, with industry rates up ~15–25% by 2023 and spot surges during 2024 peak seasons. Fluctuations in fuel and electricity pushed cold-storage operating costs up about 8–12% in 2023, squeezing reagent margins. Takara Bio therefore signs multi-year agreements and pays premium surcharges to secure priority handling and stable pricing across 60+ export markets. This strategic buying reduces disruption risk but increases fixed distribution commitments.

Proprietary Technology Licensors

Takara Bio relies on patented tech and sequences from universities and biotech firms; licensing fees and contract terms act as supplier power that raise R&D costs and time to market.

Through 2025, CRISPR and viral vector patent access added an estimated 5–15% to early-stage program budgets industry-wide, so Takara factors these fees into pricing and pipeline decisions.

The company counters by investing in internal R&D—R&D spend was ¥29.4 billion in FY2024—aiming to create proprietary alternatives and cut external IP dependence.

Laboratory Equipment Manufacturers

Takara Bio depends on high-end bioreactors, sequencers, and automated liquid handlers; these suppliers exert strong bargaining power because their instruments require proprietary consumables and expensive maintenance—industry data shows consumables can be 20–40% of lifecycle costs and service contracts 5–10% annually.

Switching vendors risks six- to 12-month regulatory re-validation and CAPEX write-offs often exceeding $1–3M per line, so Takara secures long-term service agreements to stabilize costs and ensure uptime.

- Proprietary consumables: 20–40% lifecycle cost

- Service contracts: 5–10% annual cost

- Vendor switch: 6–12 months re-validation

- CAPEX risk: $1–3M per production line

- Mitigation: long-term service agreements

Global Chemical Commodity Pricing

- Commodity-driven plastics up 8–12% (2024–mid‑2025)

- Regulatory compliance added ~3–5% cost (late 2025)

- Bulk/forward buying reduces volatility ~60%

High supplier power: specialized inputs drive costs, lead times & regional risk

Supplier power is moderate-to-high: specialized enzyme/IP/cold-chain and proprietary instruments drive 5–40% added costs, 4–12 week lead times, and 6–12 month re-validation risks; Takara cut regional risk by +35% vetted suppliers by 2025, FY2024 R&D ¥29.4B, bulk/forward buying trims input variance ~60%, commodity plastics +8–12% (2024–mid‑2025), regs added ~3–5% (late 2025).

What is included in the product

Tailored exclusively for Takara Bio, this Porter's Five Forces overview uncovers key competitive drivers, supplier/buyer influence, entry barriers, substitutes, and emerging threats that shape its pricing power and strategic positioning.

Quick five-forces snapshot tailored to Takara Bio—ideal for rapid strategic decisions and investor briefs.

Customers Bargaining Power

Large Pharmaceutical and Biotech Corporations

Major pharma and biotech buyers (e.g., Pfizer, Roche) buy reagents and CDMO services in large volumes, giving them strong bargaining power through bulk discounts and strict SLAs that press Takara Bio’s margins; top 10 pharma account for roughly 40% of industry CDMO spend in 2024.

Academic and Government Research Institutions

Academic and government researchers form a large, price-sensitive segment for Takara Bio, often limited by fixed grant funds—US NIH budgets were about $48.5B in FY2024—so individual labs have low bargaining power. Still, collective influence via institutional procurement portals and competitive bidding pressures list prices down; academic customers are highly mobile and will switch if lower-cost products match performance. Takara defends premiums with extensive technical support and proven high-performance kits, keeping renewal rates above industry averages (typically 70–85%).

Clinical Research Organizations and CDMO Clients

Clients seeking CDMO services for cell and gene therapies wield strong bargaining power via strict selection: 78% of sponsors audit facilities and 64% list regulatory compliance and prior viral vector runs as top criteria (2024 industry survey).

Switching mid-trial is prohibitively costly—average tech transfer and delay costs exceed $15–30M and 6–12 months—so bargaining peaks at initial vendor choice.

Takara Bio counters by securing long-term contracts, demonstrating a 22% year-over-year retention rate for cell/gene clients in 2024 and investing in audit-ready GMP suites to keep clients inside its ecosystem.

Switching Costs and Brand Loyalty

Switching reagents risks inconsistent results, creating technical lock-in that lowers immediate customer bargaining power for labs standardized on Takara Bio kits.

In 2025, open-platform instruments rose ~18% in academic labs, easing trials of alternatives, slightly increasing buyer leverage.

Takara Bio counters by rolling product updates and QC; its reagent reliability claims cut customer churn—company reported 6% revenue growth in 2024 from core kits.

- Technical lock-in reduces short-term buyer power

- Open-platform uptake +18% in 2025 raises switching tests

- Takara’s continuous innovation +6% 2024 kit revenue

Consolidation of Healthcare and Research Systems

Consolidation of hospital systems and research networks has boosted centralized purchasing: by 2024, the top 100 US health systems accounted for ~60% of inpatient admissions, increasing buyers’ leverage.

These large groups push master service agreements across sites, forcing Takara Bio to lower prices and offer integrated digital procurement and service bundles.

Takara Bio created dedicated account teams in 2023 to manage high-volume institutional contracts and speed onboarding.

- Top 100 US systems ≈60% inpatient share

- Master agreements cover multi-site procurement

- Price and digital integration pressure on Takara Bio

- Dedicated accounts teams launched 2023

Concentrated buyers vs. Takara’s technical lock‑in cushions pricing pressure

Customers hold mixed bargaining power: big pharma/CDMO sponsors (top 10 ≈40% CDMO spend) and consolidated health systems (top 100 US ≈60% inpatient share) drive strong leverage on price and SLAs, while individual academic labs (NIH ~$48.5B FY2024) have low power but are price-sensitive; technical lock-in and Takara’s 22% cell/gene retention (2024) and 6% kit revenue growth (2024) mitigate buyer pressure.

| Metric | Value |

|---|---|

| Top10 share CDMO spend (2024) | ≈40% |

| NIH budget (FY2024) | $48.5B |

| Top100 US inpatient share (2024) | ≈60% |

| Cell/gene client retention (2024) | 22% YoY |

| Kit revenue growth (2024) | 6% YoY |

Preview the Actual Deliverable

Takara Bio Porter's Five Forces Analysis

This preview shows the exact Takara Bio Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you'll be able to download and use the moment you buy.

You're previewing the final deliverable: ready for immediate use with comprehensive insights into competitive rivalry, supplier and buyer power, threats of new entrants and substitutes.