Talgo Boston Consulting Group Matrix

Unlock Strategic Clarity

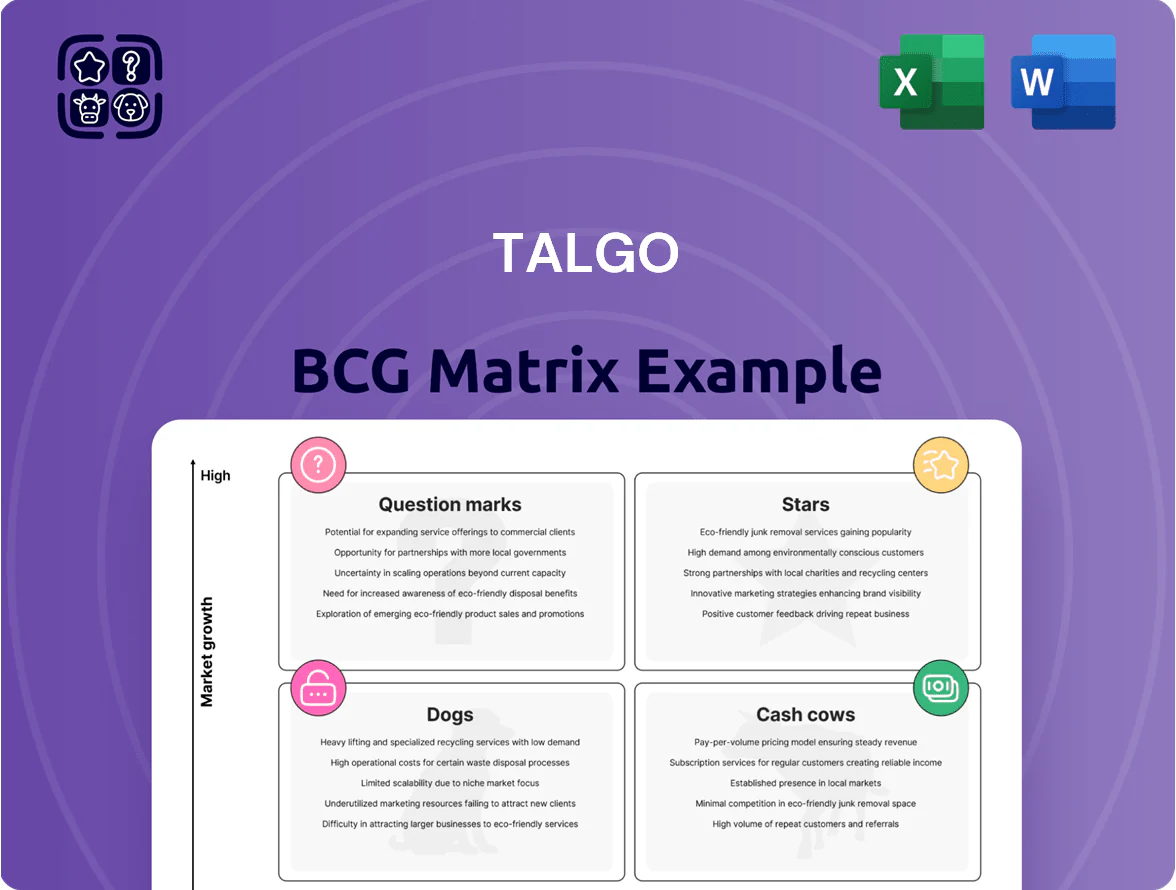

Talgo’s BCG Matrix snapshot highlights how its rail technology and rolling-stock lines perform across market growth and share—identifying which offerings drive cash, which need investment, and which may be phased out. This preview maps product roles and strategic tension points to guide quick decisions. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and actionable strategies in ready-to-use Word and Excel formats to accelerate capital allocation and growth planning.

Stars

Very High-Speed Trains (Talgo Avril)

The Avril platform is Talgo's flagship, high-growth product and a Star in the BCG matrix, capturing roughly 35% of new European high-speed orders by units through Q4 2025.

As of Dec 2025, Avril leads in efficiency and capacity with its 3+2 seating layout and multi-voltage systems, delivering ~10% lower energy/km and 12% higher seats per train vs competitors.

Scaling Avril needs heavy capex—Talgo invested €120m in 2024–25 to expand assembly and expects unit production cost cuts of 18% by 2027.

These trains drive Talgo's edge in cross-border services, contributing ~45% of 2025 rolling-stock revenue and lifting EBITDA margin by an estimated 3 percentage points.

International Maintenance Expansion

Maintenance services for high-speed fleets in high-growth regions like the Middle East now drive Talgo’s revenue, accounting for about 28% of service sales in 2024 and growing at ~18% CAGR since 2021.

By securing multi-year contracts tied to new projects—e.g., 10-year SLAs signed in 2023 worth €240m—Talgo locks steady, high-growth cash inflows and backlog visibility.

This stars segment needs ongoing technical support and €30–50m local capex per major hub to sustain market leadership and meet SLAs.

Multi-System Interoperability Solutions

Talgo’s automatic track-gauge changeover tech is a Star: it addresses cross-border barriers between Iberian, standard, and Russian gauges and saw orders rise 38% from 2021–2024, driven by EU TEN-T projects and a €420m 2025 pipeline for cross-border services.

Lightweight Rolling Stock for Decarbonization

Talgo’s lightweight aluminum trains sit in the Stars quadrant: global green transport demand grew 18% in 2024, and Talgo’s designs cut energy use by ~15–25% versus steel rivals, matching ESG tender criteria in EU and US procurements.

Keeping leadership needs high R&D: Talgo spent €48M on R&D in 2024, and must sustain similar or higher spend to outpace Alstom and Siemens, which invest €1.5B+ and €1.3B respectively.

- High growth: +18% market growth 2024

- Energy savings: 15–25% vs steel

- Talgo R&D: €48M (2024)

- Competitor R&D: Alstom €1.5B, Siemens €1.3B (2024)

Middle East High-Speed Infrastructure Projects

Following the Haramain High Speed Railway success (operational since 2018), Talgo holds a leading market share in desert-adapted trains, capturing ~30–40% of regional contracts by value as of 2025 and winning follow-on maintenance deals worth >€120m over 5 years.

Neighboring Gulf states (UAE, Qatar, Oman, Kuwait) expanded rail master plans in 2023–25, driving a regional market growth forecast of ~12% CAGR to 2030 and capital expenditures exceeding $25bn; Talgo invests heavily in heat-resistant materials and sealed HVAC systems.

Significant capital is deployed: Talgo allocated ~€45m in R&D and modular rolling-stock adaptation capex in 2024–25 to meet - dust, +50°C and sandstorm specs while targeting >€600m in regional order book potential by 2028.

- Market share: ~30–40% in desert-adapted trains (2025)

- Maintenance/contracts: >€120m secured (5yr)

- Regional CAPEX pipeline: >$25bn (2023–2030)

- Talgo R&D/adaptation spend: ~€45m (2024–25)

- Order book potential: >€600m by 2028

Avril and gauge tech power growth: 45% revenue, €420m pipeline, 35% EU HS share

Avril and gauge-change tech are Stars: Avril drove ~45% of 2025 rolling-stock revenue, 35% share of new EU high-speed orders (to Q4 2025), and Talgo cut unit cost projection 18% by 2027 after €120m 2024–25 capex; gauge tech orders rose 38% (2021–24) with a €420m 2025 pipeline. R&D was €48m (2024); regional desert trains: 30–40% share, >€120m maintenance deals.

| Metric | Value |

|---|---|

| Avril rev % (2025) | 45% |

| EU HS order share | 35% |

| Capex 2024–25 | €120m |

| R&D 2024 | €48m |

| Gauge pipeline 2025 | €420m |

What is included in the product

Concise BCG analysis of Talgo’s units: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page Talgo BCG Matrix placing rolling stock units in quadrants for fast strategic decisions.

Cash Cows

Traditional Intercity Passenger Coaches

Talgo’s traditional articulated intercity coaches hold high market share in Spain (≈60% of domestic high-speed/IC coach orders through 2024) and parts of Central Europe, supplying steady revenue of about €120–150M annually from aftersales and fleet renewals in 2023–2024.

Proven tech means low incremental R&D and marketing spend—estimated <€5M p.a.—so operating margins stay high (~18–22%), freeing cash to fund new projects.

Domestic Maintenance Contracts (Renfe)

Long-standing maintenance contracts with Renfe generate ~€120m annual revenue for Talgo (2024), delivering ~25% operating margin and steady cash flow.

In Spain Talgo holds near-monopoly on its own rolling-stock servicing—>80% share—so revenue is predictable and resilient in a mature market.

These cash cows fund debt service (net debt €220m at end-2024) and finance Avril production line expansion, reducing external funding need.

Standard Gauge Tilting Technology

Standard Gauge Tilting Technology, a mature natural-tilt system, lets Talgo trains run up to 30% faster on existing track without major upgrades, cutting CAPEX; operators report up to 15% higher ticket yield on tilted services (RENFE trials, 2023).

Growth has stabilized near 3% CAGR in installed base (2019–2024); low R&D spend (estimated <2% of product revenue in 2024) keeps gross margins high—reported operating margins ~22% for Talgo’s tilt products in FY2024.

Refurbishment and Life-Cycle Services

Refurbishment and life-cycle services are a mature, low-growth cash cow for Talgo, where the company’s strong reputation and maintenance contracts deliver predictable revenue; Talgo reported €210m in services revenue in 2024, roughly 28% of total group sales.

As operators favor extending fleet life—EU operators deferred ~15% of new train orders in 2023–24—Talgo’s overhaul projects generate steady margins and backlog; the services order book stood at ~€480m at end-2024.

The segment’s stable cash flow offsets market stagnation: services EBITDA margins near 12–15% and multi-year maintenance contracts provide visibility and working capital generation.

- Strong brand, mature market

- €210m services revenue (2024)

- €480m services backlog (end-2024)

- 12–15% EBITDA margin

Equipment and Tooling for Rail Workshops

Talgo’s Equipment and Tooling for Rail Workshops segment—specialized pit lathes and heavy maintenance machinery sold to third-party workshops—holds a dominant share in a mature, low-growth market, generating steady margins that funded about 8–10% of Talgo’s 2024 operating expenses (Talgo annual report 2024).

This cash cow returns stable EBIT margins near 18% (2023–24 average), sees <2% annual volume growth, and supplies predictable free cash flow used for R&D and corporate overhead.

- High market share in niche industrial tooling

- Slow growth: ~0–2% p.a.

- EBIT margin ~18%

- Funds ~8–10% of 2024 operating costs

Talgo’s €330–360M service engine fuels Avril growth, covers debt with 12–18% EBITDA

Talgo’s cash cows—after-sales services, refurbishments, and equipment—generated ~€330–360M revenue in 2024 (services €210M; maintenance backlog €480M), EBITDA margins 12–18%, funding debt service (net debt €220M end-2024) and Avril expansion with low R&D spend (<€5M p.a.).

| Metric | 2024 |

|---|---|

| Services revenue | €210M |

| Services backlog | €480M |

| Segment revenue | €330–360M |

| EBITDA margin | 12–18% |

| Net debt | €220M |

Preview = Final Product

Talgo BCG Matrix

The file you're previewing is the exact Talgo BCG Matrix report you'll receive after purchase—no watermarks, no draft notes—just a fully formatted, analysis-ready document designed for strategic decision-making. This preview mirrors the final deliverable, crafted with market-informed insights and clear visual mapping of product/service positioning. Upon purchase the full file is immediately downloadable and editable for presentations, planning, or client use. Expect a polished, professional report ready to deploy without further modification.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Talgo’s BCG Matrix snapshot highlights how its rail technology and rolling-stock lines perform across market growth and share—identifying which offerings drive cash, which need investment, and which may be phased out. This preview maps product roles and strategic tension points to guide quick decisions. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and actionable strategies in ready-to-use Word and Excel formats to accelerate capital allocation and growth planning.

Stars

Very High-Speed Trains (Talgo Avril)

The Avril platform is Talgo's flagship, high-growth product and a Star in the BCG matrix, capturing roughly 35% of new European high-speed orders by units through Q4 2025.

As of Dec 2025, Avril leads in efficiency and capacity with its 3+2 seating layout and multi-voltage systems, delivering ~10% lower energy/km and 12% higher seats per train vs competitors.

Scaling Avril needs heavy capex—Talgo invested €120m in 2024–25 to expand assembly and expects unit production cost cuts of 18% by 2027.

These trains drive Talgo's edge in cross-border services, contributing ~45% of 2025 rolling-stock revenue and lifting EBITDA margin by an estimated 3 percentage points.

International Maintenance Expansion

Maintenance services for high-speed fleets in high-growth regions like the Middle East now drive Talgo’s revenue, accounting for about 28% of service sales in 2024 and growing at ~18% CAGR since 2021.

By securing multi-year contracts tied to new projects—e.g., 10-year SLAs signed in 2023 worth €240m—Talgo locks steady, high-growth cash inflows and backlog visibility.

This stars segment needs ongoing technical support and €30–50m local capex per major hub to sustain market leadership and meet SLAs.

Multi-System Interoperability Solutions

Talgo’s automatic track-gauge changeover tech is a Star: it addresses cross-border barriers between Iberian, standard, and Russian gauges and saw orders rise 38% from 2021–2024, driven by EU TEN-T projects and a €420m 2025 pipeline for cross-border services.

Lightweight Rolling Stock for Decarbonization

Talgo’s lightweight aluminum trains sit in the Stars quadrant: global green transport demand grew 18% in 2024, and Talgo’s designs cut energy use by ~15–25% versus steel rivals, matching ESG tender criteria in EU and US procurements.

Keeping leadership needs high R&D: Talgo spent €48M on R&D in 2024, and must sustain similar or higher spend to outpace Alstom and Siemens, which invest €1.5B+ and €1.3B respectively.

- High growth: +18% market growth 2024

- Energy savings: 15–25% vs steel

- Talgo R&D: €48M (2024)

- Competitor R&D: Alstom €1.5B, Siemens €1.3B (2024)

Middle East High-Speed Infrastructure Projects

Following the Haramain High Speed Railway success (operational since 2018), Talgo holds a leading market share in desert-adapted trains, capturing ~30–40% of regional contracts by value as of 2025 and winning follow-on maintenance deals worth >€120m over 5 years.

Neighboring Gulf states (UAE, Qatar, Oman, Kuwait) expanded rail master plans in 2023–25, driving a regional market growth forecast of ~12% CAGR to 2030 and capital expenditures exceeding $25bn; Talgo invests heavily in heat-resistant materials and sealed HVAC systems.

Significant capital is deployed: Talgo allocated ~€45m in R&D and modular rolling-stock adaptation capex in 2024–25 to meet - dust, +50°C and sandstorm specs while targeting >€600m in regional order book potential by 2028.

- Market share: ~30–40% in desert-adapted trains (2025)

- Maintenance/contracts: >€120m secured (5yr)

- Regional CAPEX pipeline: >$25bn (2023–2030)

- Talgo R&D/adaptation spend: ~€45m (2024–25)

- Order book potential: >€600m by 2028

Avril and gauge tech power growth: 45% revenue, €420m pipeline, 35% EU HS share

Avril and gauge-change tech are Stars: Avril drove ~45% of 2025 rolling-stock revenue, 35% share of new EU high-speed orders (to Q4 2025), and Talgo cut unit cost projection 18% by 2027 after €120m 2024–25 capex; gauge tech orders rose 38% (2021–24) with a €420m 2025 pipeline. R&D was €48m (2024); regional desert trains: 30–40% share, >€120m maintenance deals.

| Metric | Value |

|---|---|

| Avril rev % (2025) | 45% |

| EU HS order share | 35% |

| Capex 2024–25 | €120m |

| R&D 2024 | €48m |

| Gauge pipeline 2025 | €420m |

What is included in the product

Concise BCG analysis of Talgo’s units: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page Talgo BCG Matrix placing rolling stock units in quadrants for fast strategic decisions.

Cash Cows

Traditional Intercity Passenger Coaches

Talgo’s traditional articulated intercity coaches hold high market share in Spain (≈60% of domestic high-speed/IC coach orders through 2024) and parts of Central Europe, supplying steady revenue of about €120–150M annually from aftersales and fleet renewals in 2023–2024.

Proven tech means low incremental R&D and marketing spend—estimated <€5M p.a.—so operating margins stay high (~18–22%), freeing cash to fund new projects.

Domestic Maintenance Contracts (Renfe)

Long-standing maintenance contracts with Renfe generate ~€120m annual revenue for Talgo (2024), delivering ~25% operating margin and steady cash flow.

In Spain Talgo holds near-monopoly on its own rolling-stock servicing—>80% share—so revenue is predictable and resilient in a mature market.

These cash cows fund debt service (net debt €220m at end-2024) and finance Avril production line expansion, reducing external funding need.

Standard Gauge Tilting Technology

Standard Gauge Tilting Technology, a mature natural-tilt system, lets Talgo trains run up to 30% faster on existing track without major upgrades, cutting CAPEX; operators report up to 15% higher ticket yield on tilted services (RENFE trials, 2023).

Growth has stabilized near 3% CAGR in installed base (2019–2024); low R&D spend (estimated <2% of product revenue in 2024) keeps gross margins high—reported operating margins ~22% for Talgo’s tilt products in FY2024.

Refurbishment and Life-Cycle Services

Refurbishment and life-cycle services are a mature, low-growth cash cow for Talgo, where the company’s strong reputation and maintenance contracts deliver predictable revenue; Talgo reported €210m in services revenue in 2024, roughly 28% of total group sales.

As operators favor extending fleet life—EU operators deferred ~15% of new train orders in 2023–24—Talgo’s overhaul projects generate steady margins and backlog; the services order book stood at ~€480m at end-2024.

The segment’s stable cash flow offsets market stagnation: services EBITDA margins near 12–15% and multi-year maintenance contracts provide visibility and working capital generation.

- Strong brand, mature market

- €210m services revenue (2024)

- €480m services backlog (end-2024)

- 12–15% EBITDA margin

Equipment and Tooling for Rail Workshops

Talgo’s Equipment and Tooling for Rail Workshops segment—specialized pit lathes and heavy maintenance machinery sold to third-party workshops—holds a dominant share in a mature, low-growth market, generating steady margins that funded about 8–10% of Talgo’s 2024 operating expenses (Talgo annual report 2024).

This cash cow returns stable EBIT margins near 18% (2023–24 average), sees <2% annual volume growth, and supplies predictable free cash flow used for R&D and corporate overhead.

- High market share in niche industrial tooling

- Slow growth: ~0–2% p.a.

- EBIT margin ~18%

- Funds ~8–10% of 2024 operating costs

Talgo’s €330–360M service engine fuels Avril growth, covers debt with 12–18% EBITDA

Talgo’s cash cows—after-sales services, refurbishments, and equipment—generated ~€330–360M revenue in 2024 (services €210M; maintenance backlog €480M), EBITDA margins 12–18%, funding debt service (net debt €220M end-2024) and Avril expansion with low R&D spend (<€5M p.a.).

| Metric | 2024 |

|---|---|

| Services revenue | €210M |

| Services backlog | €480M |

| Segment revenue | €330–360M |

| EBITDA margin | 12–18% |

| Net debt | €220M |

Preview = Final Product

Talgo BCG Matrix

The file you're previewing is the exact Talgo BCG Matrix report you'll receive after purchase—no watermarks, no draft notes—just a fully formatted, analysis-ready document designed for strategic decision-making. This preview mirrors the final deliverable, crafted with market-informed insights and clear visual mapping of product/service positioning. Upon purchase the full file is immediately downloadable and editable for presentations, planning, or client use. Expect a polished, professional report ready to deploy without further modification.