Talgo Porter's Five Forces Analysis

From Overview to Strategy Blueprint

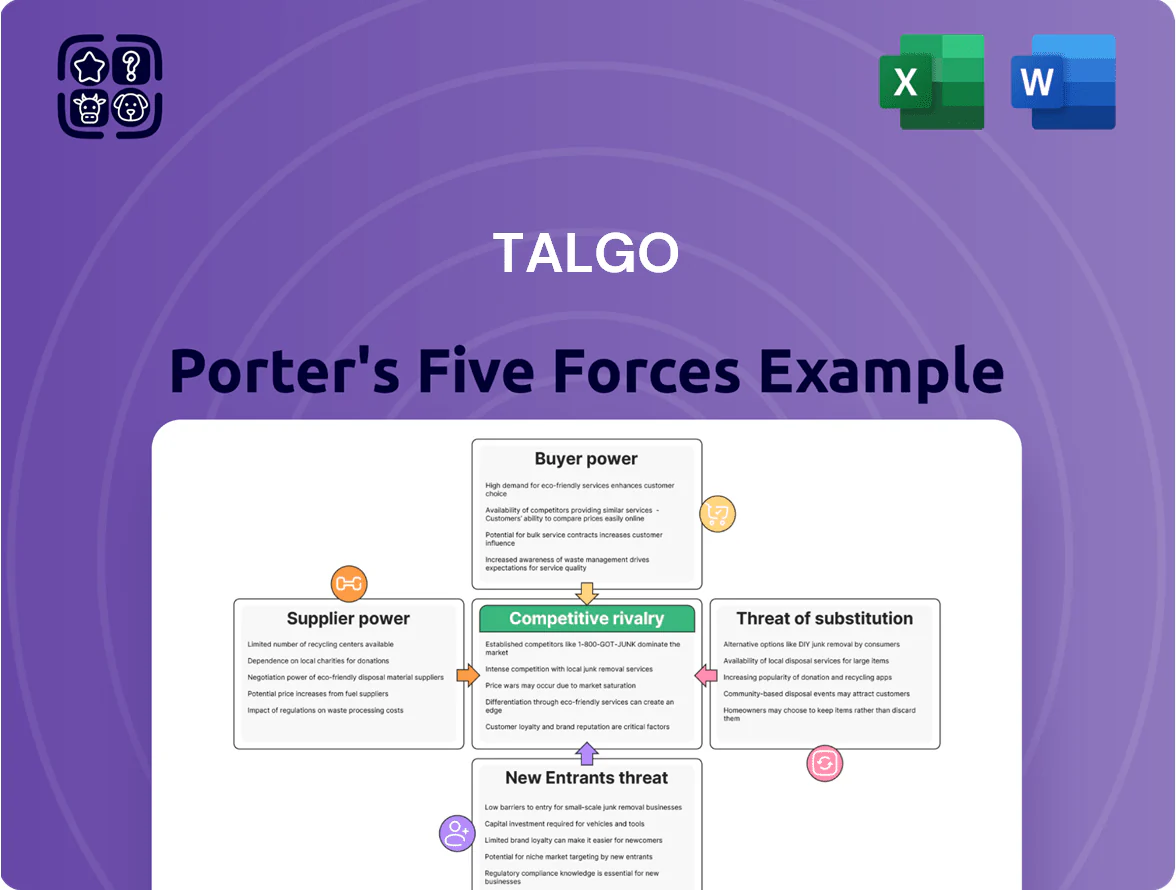

Talgo faces moderate supplier power and niche buyer segments, while capital intensity and regulatory barriers curb new entrants; rivalry is fierce among European and Asian rolling-stock manufacturers, with technology and service differentiation reducing substitute threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Talgo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component dependency

Talgo depends on niche suppliers for specialized bogies, couplers and traction motors, often sourced from fewer than 5 global high-tech firms, giving suppliers strong pricing power; in 2024 Talgo reported 18% of procurement spend tied to single-source components. Replacing a vendor can take 12–36 months and cost 8–15% of project value due to certification and testing, so supplier leverage materially raises input risk.

Raw material price volatility

Talgo relies on aluminum and high-grade steel for lightweight car bodies; aluminum prices rose ~45% from Jan 2020 to Dec 2021 and averaged $2,200/ton in 2024, while Eurostoxx steel indices climbed 18% in 2023, squeezing margins.

Commodity swings feed directly into Talgo’s cost structure and in 2024 materials accounted for ~38% of COGS, so sudden price hikes cut gross margin.

With multi-year fixed-price contracts, Talgo cannot immediately pass spikes to clients, raising working-capital needs and hedging costs.

Switching costs for proprietary tech

Many Talgo train subsystems use third-party proprietary hardware and software, so switching suppliers demands major redesigns and fresh safety certification (typically 12–24 months and €2–5M per subsystem based on EU rail safety cases in 2023), raising integration costs and delaying deployment.

Energy costs for manufacturing

Energy costs heavily affect Talgo; EU industrial electricity prices averaged €0.22/kWh in 2024 vs €0.16/kWh in 2019, raising manufacturing overheads and squeezing margins.

Suppliers of steel and aluminum, plus carbon-intensive suppliers, raised prices 8–12% in 2023–24 due to EU ETS (emissions trading) tightening, increasing Talgo’s input cost risk.

Talgo must hedge energy, pursue efficiency, and pass limited costs to clients to protect its competitive pricing model.

- EU industrial electricity €0.22/kWh (2024)

- Input-price rises 8–12% (2023–24)

- EU ETS tightening increased carbon costs

- Need for hedging, efficiency, selective pass-through

Highly skilled labor scarcity

The specialized nature of rail engineering makes expert labor a critical input; Talgo faces strong pressure from engineering unions and niche technical staff who command bargaining power.

Global rail engineering vacancy rates hit 8.1% in 2024 and Spain’s skilled rail workforce shrank 3.4% year-over-year, letting suppliers demand pay premiums—Talgo reported 12% higher R&D staff costs in 2024 versus 2022.

Higher compensation and better terms raise operating costs and delay projects, squeezing margins on rolling-stock contracts.

- 8.1% global vacancy rate (2024)

- Spain rail skilled workforce -3.4% YoY (2024)

- Talgo R&D staff costs +12% (2024 vs 2022)

Talgo faces supplier squeeze: high single-source risk, rising input and labor costs

Suppliers hold high bargaining power for Talgo due to limited niche vendors for bogies/traction (fewer than 5 firms), 12–36 month switch times, and single-source spend of 18% in 2024, while materials/energy (38% of COGS; EU electricity €0.22/kWh in 2024) and skilled-labor shortages (8.1% vacancy globally, Spain −3.4% YoY) raise input costs and integration risk.

| Metric | Value |

|---|---|

| Single-source spend (2024) | 18% |

| Materials share of COGS | 38% |

| EU industrial electricity (2024) | €0.22/kWh |

| Supplier switch time | 12–36 months |

| Global rail vacancy (2024) | 8.1% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, entry threats, and substitutes specifically for Talgo, highlighting strategic vulnerabilities, market barriers, and opportunities to protect or expand its rail-industry position.

A concise Porter's Five Forces snapshot for Talgo—quickly highlights competitive pressures and strategic levers for faster, data-driven decisions.

Customers Bargaining Power

Concentration of state-owned buyers

National operators like Renfe (Spain) and Deutsche Bahn (Germany) are Talgo’s main buyers, acting as monopsonies/oligopsonies that drive hard bargains; Renfe’s 2024 rolling-stock capex was ~€1.2bn and DB’s fleet budget ~€2.5bn, so each contract represents a material share of Talgo’s revenue.

Their large procurement pools let them extract price cuts, longer payment terms, and heavier warranty/service demands, squeezing Talgo’s margins and forcing scale or diversification to offset negotiation leverage.

Large-scale contract reliance

Talgo relies on a few multi-year contracts—its 2024 revenue of €387m showed volatility from winning or losing large tenders—so losing one major bid can cut backlog and revenue sharply and force idle capacity. Buyers gain leverage late in procurement because a single contract can represent 20–40% of an annual order book for years; that bargaining power pressures margins, payment terms, and delivery schedules.

Stringent technical specifications

Customers demand highly customized trains to meet national safety and track standards, forcing Talgo into R&D runs that can exceed €20–40m per project; in 2024 Talgo spent €27.3m on R&D, reflecting this pressure. Buyers’ bespoke specifications give them leverage to delay payments or renegotiate margins, squeezing Talgo’s EBITDA (2.8% in 2023). If deliveries miss exact parameters, contracts often include penalties of up to 5–10% of order value, shifting risk to Talgo.

Availability of global competitors

Talgo’s niche tilting technology is distinctive, but buyers can choose global giants—Alstom, Siemens Mobility, and CRRC—who together held over 60% of rolling-stock revenues in 2024 (Alstom €17.4bn, Siemens Mobility €7.6bn, CRRC RMB 160bn).

These alternatives let procurement agencies pit manufacturers against each other in competitive bids, pressuring margins and driving contract prices down; Talgo’s premium is often negotiated away.

The competitive bidding market keeps the buyer as the dominant party—large contracts (typical €100m+ regional tenders) shift leverage to customers with strict cost and delivery requirements.

- Buyers can switch among major suppliers

- Top rivals captured 60%+ rolling-stock revenue 2024

- Large tenders (≈€100m+) favor buyer leverage

Political and budgetary constraints

Most Talgo buyers are state-linked, so purchases track government budgets and election cycles; Spain’s 2024 rail capex fell 7.5% year-on-year to €1.15bn, showing sensitivity to fiscal shifts.

Policy changes or austerity can delay or cancel multi-year contracts—e.g., a €200m regional train order postponed in 2023—forcing Talgo to revise prices and timelines.

Talgo often offers flexible payment terms, phased deliveries, and contract clauses tied to sovereign funding windows to reduce cancellation risk.

- State buyers dominate—high budget sensitivity

- 2024 Spanish rail capex €1.15bn (-7.5%)

- €200m 2023 regional order postponed

- Mitigations: flexible pricing, phased delivery, funding-linked clauses

Oligopsony buyers squeeze Talgo: big capex gives Renfe/DB leverage, margins under pressure

Large state operators (Renfe, DB) act as oligopsonies; their 2024 capex (Renfe ~€1.2bn, DB ~€2.5bn) makes single tenders material to Talgo (2024 rev €387m), giving buyers strong price, payment and warranty leverage that compresses Talgo’s margins and forces scale/diversification.

| Metric | 2024 |

|---|---|

| Talgo revenue | €387m |

| Renfe capex | €1.2bn |

| DB fleet budget | €2.5bn |

| Top rivals share | 60%+ |

Full Version Awaits

Talgo Porter's Five Forces Analysis

This preview shows the exact Talgo Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Talgo faces moderate supplier power and niche buyer segments, while capital intensity and regulatory barriers curb new entrants; rivalry is fierce among European and Asian rolling-stock manufacturers, with technology and service differentiation reducing substitute threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Talgo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component dependency

Talgo depends on niche suppliers for specialized bogies, couplers and traction motors, often sourced from fewer than 5 global high-tech firms, giving suppliers strong pricing power; in 2024 Talgo reported 18% of procurement spend tied to single-source components. Replacing a vendor can take 12–36 months and cost 8–15% of project value due to certification and testing, so supplier leverage materially raises input risk.

Raw material price volatility

Talgo relies on aluminum and high-grade steel for lightweight car bodies; aluminum prices rose ~45% from Jan 2020 to Dec 2021 and averaged $2,200/ton in 2024, while Eurostoxx steel indices climbed 18% in 2023, squeezing margins.

Commodity swings feed directly into Talgo’s cost structure and in 2024 materials accounted for ~38% of COGS, so sudden price hikes cut gross margin.

With multi-year fixed-price contracts, Talgo cannot immediately pass spikes to clients, raising working-capital needs and hedging costs.

Switching costs for proprietary tech

Many Talgo train subsystems use third-party proprietary hardware and software, so switching suppliers demands major redesigns and fresh safety certification (typically 12–24 months and €2–5M per subsystem based on EU rail safety cases in 2023), raising integration costs and delaying deployment.

Energy costs for manufacturing

Energy costs heavily affect Talgo; EU industrial electricity prices averaged €0.22/kWh in 2024 vs €0.16/kWh in 2019, raising manufacturing overheads and squeezing margins.

Suppliers of steel and aluminum, plus carbon-intensive suppliers, raised prices 8–12% in 2023–24 due to EU ETS (emissions trading) tightening, increasing Talgo’s input cost risk.

Talgo must hedge energy, pursue efficiency, and pass limited costs to clients to protect its competitive pricing model.

- EU industrial electricity €0.22/kWh (2024)

- Input-price rises 8–12% (2023–24)

- EU ETS tightening increased carbon costs

- Need for hedging, efficiency, selective pass-through

Highly skilled labor scarcity

The specialized nature of rail engineering makes expert labor a critical input; Talgo faces strong pressure from engineering unions and niche technical staff who command bargaining power.

Global rail engineering vacancy rates hit 8.1% in 2024 and Spain’s skilled rail workforce shrank 3.4% year-over-year, letting suppliers demand pay premiums—Talgo reported 12% higher R&D staff costs in 2024 versus 2022.

Higher compensation and better terms raise operating costs and delay projects, squeezing margins on rolling-stock contracts.

- 8.1% global vacancy rate (2024)

- Spain rail skilled workforce -3.4% YoY (2024)

- Talgo R&D staff costs +12% (2024 vs 2022)

Talgo faces supplier squeeze: high single-source risk, rising input and labor costs

Suppliers hold high bargaining power for Talgo due to limited niche vendors for bogies/traction (fewer than 5 firms), 12–36 month switch times, and single-source spend of 18% in 2024, while materials/energy (38% of COGS; EU electricity €0.22/kWh in 2024) and skilled-labor shortages (8.1% vacancy globally, Spain −3.4% YoY) raise input costs and integration risk.

| Metric | Value |

|---|---|

| Single-source spend (2024) | 18% |

| Materials share of COGS | 38% |

| EU industrial electricity (2024) | €0.22/kWh |

| Supplier switch time | 12–36 months |

| Global rail vacancy (2024) | 8.1% |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, entry threats, and substitutes specifically for Talgo, highlighting strategic vulnerabilities, market barriers, and opportunities to protect or expand its rail-industry position.

A concise Porter's Five Forces snapshot for Talgo—quickly highlights competitive pressures and strategic levers for faster, data-driven decisions.

Customers Bargaining Power

Concentration of state-owned buyers

National operators like Renfe (Spain) and Deutsche Bahn (Germany) are Talgo’s main buyers, acting as monopsonies/oligopsonies that drive hard bargains; Renfe’s 2024 rolling-stock capex was ~€1.2bn and DB’s fleet budget ~€2.5bn, so each contract represents a material share of Talgo’s revenue.

Their large procurement pools let them extract price cuts, longer payment terms, and heavier warranty/service demands, squeezing Talgo’s margins and forcing scale or diversification to offset negotiation leverage.

Large-scale contract reliance

Talgo relies on a few multi-year contracts—its 2024 revenue of €387m showed volatility from winning or losing large tenders—so losing one major bid can cut backlog and revenue sharply and force idle capacity. Buyers gain leverage late in procurement because a single contract can represent 20–40% of an annual order book for years; that bargaining power pressures margins, payment terms, and delivery schedules.

Stringent technical specifications

Customers demand highly customized trains to meet national safety and track standards, forcing Talgo into R&D runs that can exceed €20–40m per project; in 2024 Talgo spent €27.3m on R&D, reflecting this pressure. Buyers’ bespoke specifications give them leverage to delay payments or renegotiate margins, squeezing Talgo’s EBITDA (2.8% in 2023). If deliveries miss exact parameters, contracts often include penalties of up to 5–10% of order value, shifting risk to Talgo.

Availability of global competitors

Talgo’s niche tilting technology is distinctive, but buyers can choose global giants—Alstom, Siemens Mobility, and CRRC—who together held over 60% of rolling-stock revenues in 2024 (Alstom €17.4bn, Siemens Mobility €7.6bn, CRRC RMB 160bn).

These alternatives let procurement agencies pit manufacturers against each other in competitive bids, pressuring margins and driving contract prices down; Talgo’s premium is often negotiated away.

The competitive bidding market keeps the buyer as the dominant party—large contracts (typical €100m+ regional tenders) shift leverage to customers with strict cost and delivery requirements.

- Buyers can switch among major suppliers

- Top rivals captured 60%+ rolling-stock revenue 2024

- Large tenders (≈€100m+) favor buyer leverage

Political and budgetary constraints

Most Talgo buyers are state-linked, so purchases track government budgets and election cycles; Spain’s 2024 rail capex fell 7.5% year-on-year to €1.15bn, showing sensitivity to fiscal shifts.

Policy changes or austerity can delay or cancel multi-year contracts—e.g., a €200m regional train order postponed in 2023—forcing Talgo to revise prices and timelines.

Talgo often offers flexible payment terms, phased deliveries, and contract clauses tied to sovereign funding windows to reduce cancellation risk.

- State buyers dominate—high budget sensitivity

- 2024 Spanish rail capex €1.15bn (-7.5%)

- €200m 2023 regional order postponed

- Mitigations: flexible pricing, phased delivery, funding-linked clauses

Oligopsony buyers squeeze Talgo: big capex gives Renfe/DB leverage, margins under pressure

Large state operators (Renfe, DB) act as oligopsonies; their 2024 capex (Renfe ~€1.2bn, DB ~€2.5bn) makes single tenders material to Talgo (2024 rev €387m), giving buyers strong price, payment and warranty leverage that compresses Talgo’s margins and forces scale/diversification.

| Metric | 2024 |

|---|---|

| Talgo revenue | €387m |

| Renfe capex | €1.2bn |

| DB fleet budget | €2.5bn |

| Top rivals share | 60%+ |

Full Version Awaits

Talgo Porter's Five Forces Analysis

This preview shows the exact Talgo Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.