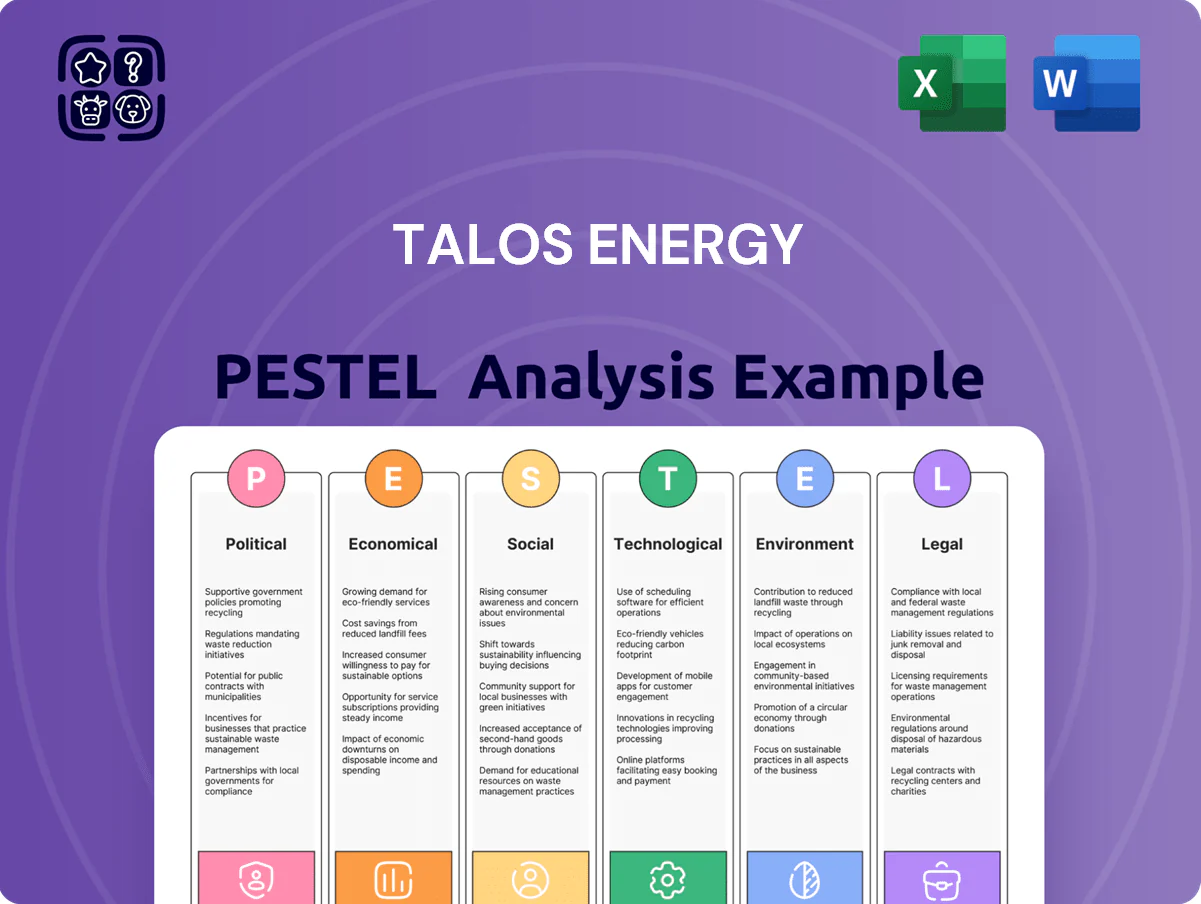

Talos Energy PESTLE Analysis

Your Competitive Advantage Starts with This Report

Assess how regulatory shifts, commodity cycles, and tech-driven exploration are reshaping Talos Energy’s outlook with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context. Purchase the full PESTLE Analysis to access a detailed, editable report that highlights risks, opportunities, and strategic implications you can apply immediately.

Political factors

US Federal Leasing Policy

The US Gulf offshore regulatory landscape is driven by federal leasing schedules and permit timelines; DOI's 2024-2029 leasing program canceled several Gulf lease sales, trimming potential acreage and contributing to a 15% industry-wide backlog in permits as of Q4 2024. Changes in administration or DOI priorities can pause lease sales or impose stricter environmental reviews, raising project delays and development costs for operators like Talos. Talos must actively engage Interior, BOEM, and BSEE to protect access to core Gulf blocks and to keep its multi-billion dollar exploration pipeline—estimated at over $1.2 billion in 2025 capex—viable under shifting political mandates.

Mexican Energy Sovereignty and Policy

Operations in offshore Mexico are exposed to swings in energy policy between liberalization and resource nationalism; Talos’s 2024 Mexican assets (approx. 30,000 boe/d pre-2025 targets) depend on legal certainty for production sharing and permits.

The López Obrador-era shifts reduced foreign scope, while 2023–25 regulatory clarifications restored some investor confidence; foreign participation rules directly affect contract stability and JV terms.

Political shifts in Mexico City influence pipeline and port permits, affecting capex timelines—delays can compress expected free cash flow and repatriation, with Mexican fiscal regimes taking up to 30% of gross production value in royalties and taxes in recent contracts.

Geopolitical Stability and Global Oil Supply

Political instability in major oil-producing regions drives price volatility, with Brent crude swinging 28% in 2024 amid Middle East conflicts and Russia-Ukraine tensions, complicating Talos Energy’s production planning and hedging costs.

OPEC+ production cuts in 2024 removed roughly 3.0 mb/d from the market, tightening supply and elevating realized prices for independents like Talos but increasing revenue uncertainty.

Talos must monitor diplomatic shifts and sanctions that can alter U.S. Gulf of Mexico export dynamics, as a $70–90/bbl Brent range in 2024–25 materially affects project IRRs and capital allocation.

Carbon Capture and Sequestration Subsidies

The Inflation Reduction Act allocates up to $85/ton tax credits (45Q) rising to $180/ton for direct air capture under recent IRS guidance, underpinning Talos Energy’s CCS economics for its Gulf of Mexico projects and aiding a potential CCS segment targeting ~0.5–1.0 MTCO2/year by 2030.

Continued bipartisan support is critical; repeal or scaling back of these credits would force Talos to reassess capital allocation, project IRRs, and long-term transition plans given current project NPV sensitivity to credit levels.

- 45Q credits: $85–$180/ton (per 2024–2025 IRS updates)

- Talos CCS target: ~0.5–1.0 MTCO2/yr by 2030 (project-level estimate)

- Policy risk: repeal would materially reduce project IRR and NPV

International Trade and Sanctions

International trade rules and sanctions influence global oil flows and the cost of specialized deepwater equipment; 2024 US tariffs on certain steel and 2025 export controls on subsea tech raised component prices by an estimated 8–12%, squeezing margins for Gulf of Mexico operators like Talos Energy.

Political tariffs and sanctions can delay shipments and increase lead times for rigs and subsea trees, forcing Talos to absorb higher capex or pass costs to JV partners while managing supply-chain diversification.

Energy supply squeeze: permit backlogs, OPEC+ cuts, volatile Brent and rising costs

US Gulf permit backlogs ~15% (Q4 2024); DOI 2024–29 leasing cuts reduced acreage and delayed projects; Mexico assets ~30,000 boe/d pre-2025 reliant on stable PSPs; Brent volatility ±28% (2024) and OPEC+ cuts ~3.0 mb/d tightened markets; 45Q credits $85–$180/t supporting CCS ~0.5–1.0 MTCO2/yr by 2030; tariffs/export controls raised equipment costs ~8–12% (2024–25).

| Metric | Value |

|---|---|

| Permit backlog (Q4 2024) | 15% |

| Mexico production (pre-2025) | ~30,000 boe/d |

| Brent volatility (2024) | ±28% |

| OPEC+ cut (2024) | ~3.0 mb/d |

| 45Q credit | $85–$180/t |

| CCS target | 0.5–1.0 MTCO2/yr |

| Equipment cost rise | 8–12% |

What is included in the product

Explores how macro-environmental forces uniquely impact Talos Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current trends and regional market dynamics.

A concise, visually segmented Talos Energy PESTLE summary designed for quick reference in meetings or presentations, easily editable for region- or business-specific notes and shareable across teams for fast alignment on external risks and market positioning.

Economic factors

Global Commodity Price Fluctuations

The financial performance of Talos Energy is tightly tied to Brent and Henry Hub price movements; Brent averaged about 96 USD/bbl in 2024, directly affecting realized oil revenues from Gulf of Mexico assets.

High inflation or a 2023–24 US slowdown pressured demand, contributing to Q4 2024 realized oil prices near 85 USD/bbl and reduced gas offtake, compressing margins.

Talos reported using commodity hedges covering a portion of 2024–2025 volumes; realized hedge gains totaled roughly 120 million USD in 2024, stabilizing cash flow and capital spending through price downturns.

Cost of Capital and Interest Rate Environment

As a capital-intensive E&P firm, Talos Energy depends on debt and equity markets to fund exploration and M&A; rising U.S. Fed-driven rates pushed the 10-year Treasury from ~3.5% in 2023 to about 4.6% by late 2025, lifting corporate borrowing costs and average syndicated loan spreads by ~120–150 bps. Higher rates increase debt servicing and raise hurdle rates for new offshore projects, pressuring returns when breakeven prices and project IRRs must exceed a higher weighted average cost of capital. In late 2025 Talos needs disciplined balance-sheet management—maintaining net debt/EBITDA targets and preserving liquidity—to ensure financed projects achieve IRRs above the elevated cost of capital.

Offshore Service Cost Inflation

Offshore service costs—labor, specialized rigs, and subsea equipment—rose sharply in 2024, with rig dayrates up ~25% YoY and subsea equipment prices rising ~15–20%, squeezing margins despite Brent averaging ~$85/bbl in 2024; Talos counters via cost-saving ops, long‑term service contracts and joint procurement, aiming to preserve EBITDA margins near its 2023 pro forma target of ~40%.

Strategic M and A Integration Economics

- 2024 pro forma production ~120 mboe/d; synergies target $100–200M/year

- Reservoir decline rates often 20–30%/yr for mature fields

- Abandonment costs $1–3M/well; Talos ARO estimated $300–400M (2024)

CCS Commercialization and Revenue Streams

The economic viability of CCS hinges on a developed carbon credit market and demand for decarbonization services; global voluntary carbon market value rose to about $1.5bn in 2023 while compliance markets exceed $70bn in 2024, shaping price signals for sequestration.

Talos is shifting from pure E&P to include recurring carbon storage fees, targeting offshore saline storage and prospective revenue streams as projects move from pilot to commercial scale.

Progress depends on industrial emitters' willingness to pay under current conditions: 2024 EU ETS prices averaged ~€90/tCO2, US 45Q tax credits up to $85/tCO2 still drive project economics and determine commercialization pace.

- Market size: compliance markets >$70bn (2024); voluntary ~$1.5bn (2023)

- Price signals: EU ETS ~€90/tCO2 (2024); US 45Q up to $85/tCO2

- Talos strategy: add recurring carbon storage fees to E&P revenues

- Key dependency: industrial buyers' willingness to pay given regulations and credits

Talos: 2024 hedge gains cushion cash as costs, rates lift breakevens and AROs

Talos’ revenues remain Brent- and Henry Hub-linked (Brent avg ~96 USD/bbl 2024; realized ~85 USD/bbl Q4 2024); 2024 hedge gains ≈120M USD supported cash flow. Rising rates (10y Treasury ~4.6% by late‑2025) and higher offshore service costs (rig dayrates +25% in 2024) raised project breakevens and capex needs; 2024 pro forma production ~120 mboe/d, ARO ~300–400M USD.

| Metric | 2024/2025 |

|---|---|

| Brent avg | 96 USD/bbl (2024) |

| Q4 realized oil | ~85 USD/bbl |

| Hedge gains | ~120M USD (2024) |

| Pro forma production | ~120 mboe/d (2024) |

| Rig dayrates | +25% YoY (2024) |

| 10y Treasury | ~4.6% (late 2025) |

| ARO | ~300–400M USD (2024) |

Same Document Delivered

Talos Energy PESTLE Analysis

The preview shown here is the exact Talos Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decisions and reporting.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Assess how regulatory shifts, commodity cycles, and tech-driven exploration are reshaping Talos Energy’s outlook with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context. Purchase the full PESTLE Analysis to access a detailed, editable report that highlights risks, opportunities, and strategic implications you can apply immediately.

Political factors

US Federal Leasing Policy

The US Gulf offshore regulatory landscape is driven by federal leasing schedules and permit timelines; DOI's 2024-2029 leasing program canceled several Gulf lease sales, trimming potential acreage and contributing to a 15% industry-wide backlog in permits as of Q4 2024. Changes in administration or DOI priorities can pause lease sales or impose stricter environmental reviews, raising project delays and development costs for operators like Talos. Talos must actively engage Interior, BOEM, and BSEE to protect access to core Gulf blocks and to keep its multi-billion dollar exploration pipeline—estimated at over $1.2 billion in 2025 capex—viable under shifting political mandates.

Mexican Energy Sovereignty and Policy

Operations in offshore Mexico are exposed to swings in energy policy between liberalization and resource nationalism; Talos’s 2024 Mexican assets (approx. 30,000 boe/d pre-2025 targets) depend on legal certainty for production sharing and permits.

The López Obrador-era shifts reduced foreign scope, while 2023–25 regulatory clarifications restored some investor confidence; foreign participation rules directly affect contract stability and JV terms.

Political shifts in Mexico City influence pipeline and port permits, affecting capex timelines—delays can compress expected free cash flow and repatriation, with Mexican fiscal regimes taking up to 30% of gross production value in royalties and taxes in recent contracts.

Geopolitical Stability and Global Oil Supply

Political instability in major oil-producing regions drives price volatility, with Brent crude swinging 28% in 2024 amid Middle East conflicts and Russia-Ukraine tensions, complicating Talos Energy’s production planning and hedging costs.

OPEC+ production cuts in 2024 removed roughly 3.0 mb/d from the market, tightening supply and elevating realized prices for independents like Talos but increasing revenue uncertainty.

Talos must monitor diplomatic shifts and sanctions that can alter U.S. Gulf of Mexico export dynamics, as a $70–90/bbl Brent range in 2024–25 materially affects project IRRs and capital allocation.

Carbon Capture and Sequestration Subsidies

The Inflation Reduction Act allocates up to $85/ton tax credits (45Q) rising to $180/ton for direct air capture under recent IRS guidance, underpinning Talos Energy’s CCS economics for its Gulf of Mexico projects and aiding a potential CCS segment targeting ~0.5–1.0 MTCO2/year by 2030.

Continued bipartisan support is critical; repeal or scaling back of these credits would force Talos to reassess capital allocation, project IRRs, and long-term transition plans given current project NPV sensitivity to credit levels.

- 45Q credits: $85–$180/ton (per 2024–2025 IRS updates)

- Talos CCS target: ~0.5–1.0 MTCO2/yr by 2030 (project-level estimate)

- Policy risk: repeal would materially reduce project IRR and NPV

International Trade and Sanctions

International trade rules and sanctions influence global oil flows and the cost of specialized deepwater equipment; 2024 US tariffs on certain steel and 2025 export controls on subsea tech raised component prices by an estimated 8–12%, squeezing margins for Gulf of Mexico operators like Talos Energy.

Political tariffs and sanctions can delay shipments and increase lead times for rigs and subsea trees, forcing Talos to absorb higher capex or pass costs to JV partners while managing supply-chain diversification.

Energy supply squeeze: permit backlogs, OPEC+ cuts, volatile Brent and rising costs

US Gulf permit backlogs ~15% (Q4 2024); DOI 2024–29 leasing cuts reduced acreage and delayed projects; Mexico assets ~30,000 boe/d pre-2025 reliant on stable PSPs; Brent volatility ±28% (2024) and OPEC+ cuts ~3.0 mb/d tightened markets; 45Q credits $85–$180/t supporting CCS ~0.5–1.0 MTCO2/yr by 2030; tariffs/export controls raised equipment costs ~8–12% (2024–25).

| Metric | Value |

|---|---|

| Permit backlog (Q4 2024) | 15% |

| Mexico production (pre-2025) | ~30,000 boe/d |

| Brent volatility (2024) | ±28% |

| OPEC+ cut (2024) | ~3.0 mb/d |

| 45Q credit | $85–$180/t |

| CCS target | 0.5–1.0 MTCO2/yr |

| Equipment cost rise | 8–12% |

What is included in the product

Explores how macro-environmental forces uniquely impact Talos Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current trends and regional market dynamics.

A concise, visually segmented Talos Energy PESTLE summary designed for quick reference in meetings or presentations, easily editable for region- or business-specific notes and shareable across teams for fast alignment on external risks and market positioning.

Economic factors

Global Commodity Price Fluctuations

The financial performance of Talos Energy is tightly tied to Brent and Henry Hub price movements; Brent averaged about 96 USD/bbl in 2024, directly affecting realized oil revenues from Gulf of Mexico assets.

High inflation or a 2023–24 US slowdown pressured demand, contributing to Q4 2024 realized oil prices near 85 USD/bbl and reduced gas offtake, compressing margins.

Talos reported using commodity hedges covering a portion of 2024–2025 volumes; realized hedge gains totaled roughly 120 million USD in 2024, stabilizing cash flow and capital spending through price downturns.

Cost of Capital and Interest Rate Environment

As a capital-intensive E&P firm, Talos Energy depends on debt and equity markets to fund exploration and M&A; rising U.S. Fed-driven rates pushed the 10-year Treasury from ~3.5% in 2023 to about 4.6% by late 2025, lifting corporate borrowing costs and average syndicated loan spreads by ~120–150 bps. Higher rates increase debt servicing and raise hurdle rates for new offshore projects, pressuring returns when breakeven prices and project IRRs must exceed a higher weighted average cost of capital. In late 2025 Talos needs disciplined balance-sheet management—maintaining net debt/EBITDA targets and preserving liquidity—to ensure financed projects achieve IRRs above the elevated cost of capital.

Offshore Service Cost Inflation

Offshore service costs—labor, specialized rigs, and subsea equipment—rose sharply in 2024, with rig dayrates up ~25% YoY and subsea equipment prices rising ~15–20%, squeezing margins despite Brent averaging ~$85/bbl in 2024; Talos counters via cost-saving ops, long‑term service contracts and joint procurement, aiming to preserve EBITDA margins near its 2023 pro forma target of ~40%.

Strategic M and A Integration Economics

- 2024 pro forma production ~120 mboe/d; synergies target $100–200M/year

- Reservoir decline rates often 20–30%/yr for mature fields

- Abandonment costs $1–3M/well; Talos ARO estimated $300–400M (2024)

CCS Commercialization and Revenue Streams

The economic viability of CCS hinges on a developed carbon credit market and demand for decarbonization services; global voluntary carbon market value rose to about $1.5bn in 2023 while compliance markets exceed $70bn in 2024, shaping price signals for sequestration.

Talos is shifting from pure E&P to include recurring carbon storage fees, targeting offshore saline storage and prospective revenue streams as projects move from pilot to commercial scale.

Progress depends on industrial emitters' willingness to pay under current conditions: 2024 EU ETS prices averaged ~€90/tCO2, US 45Q tax credits up to $85/tCO2 still drive project economics and determine commercialization pace.

- Market size: compliance markets >$70bn (2024); voluntary ~$1.5bn (2023)

- Price signals: EU ETS ~€90/tCO2 (2024); US 45Q up to $85/tCO2

- Talos strategy: add recurring carbon storage fees to E&P revenues

- Key dependency: industrial buyers' willingness to pay given regulations and credits

Talos: 2024 hedge gains cushion cash as costs, rates lift breakevens and AROs

Talos’ revenues remain Brent- and Henry Hub-linked (Brent avg ~96 USD/bbl 2024; realized ~85 USD/bbl Q4 2024); 2024 hedge gains ≈120M USD supported cash flow. Rising rates (10y Treasury ~4.6% by late‑2025) and higher offshore service costs (rig dayrates +25% in 2024) raised project breakevens and capex needs; 2024 pro forma production ~120 mboe/d, ARO ~300–400M USD.

| Metric | 2024/2025 |

|---|---|

| Brent avg | 96 USD/bbl (2024) |

| Q4 realized oil | ~85 USD/bbl |

| Hedge gains | ~120M USD (2024) |

| Pro forma production | ~120 mboe/d (2024) |

| Rig dayrates | +25% YoY (2024) |

| 10y Treasury | ~4.6% (late 2025) |

| ARO | ~300–400M USD (2024) |

Same Document Delivered

Talos Energy PESTLE Analysis

The preview shown here is the exact Talos Energy PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic decisions and reporting.