Tanger Factory Outlet Centers PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, consumer spending trends, and sustainability regulations are reshaping Tanger Factory Outlet Centers’ growth prospects—our concise PESTLE preview highlights key external drivers and risks to watch. Purchase the full PESTLE analysis for a complete, actionable breakdown with ready-to-use insights for investors, strategists, and advisors.

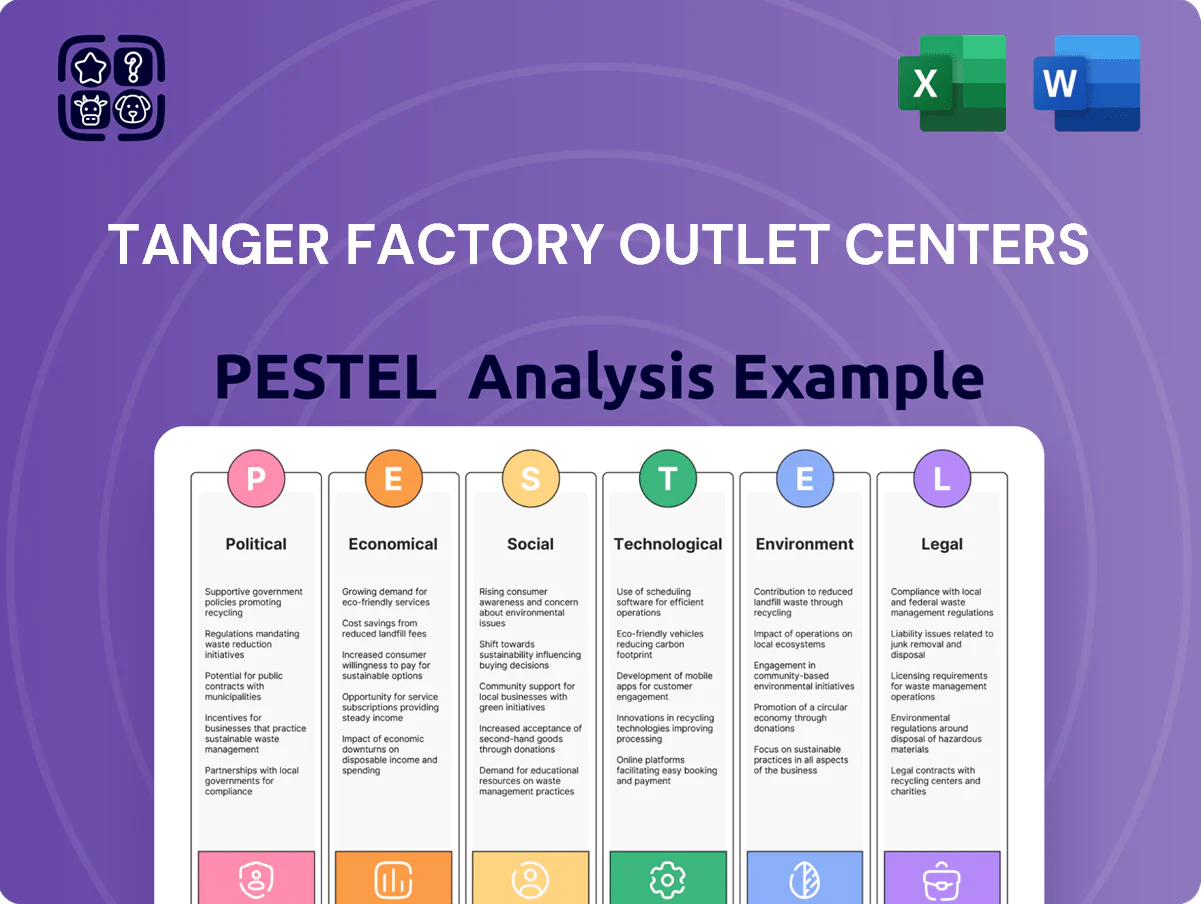

Political factors

Trade Policy and Import Tariffs

Changes in international trade agreements and tariffs directly affect cost of goods for Tanger tenants; import tariffs rising 5-10% in 2024–2025 increased landed costs for apparel brands, pressuring margins and potentially raising retail prices.

Shifts toward protectionism in late 2025 risk further price inflation for designer apparel/accessories, which could reduce tenant gross margins (industry average apparel margin fell to ~48% in 2024 from 51% in 2021) and dampen consumer demand.

Tanger must monitor geopolitical developments—US-China tariff fluctuations and US trade policy revisions—since supply-chain disruptions and inventory delays for global brands occupying Tanger centers can increase stockouts and operating volatility.

REIT Tax Legislation and Compliance

Tanger operates as a REIT, enjoying pass-through taxation but faces federal legislative risk; Congressional proposals through 2025 could change tax rates on REITs or tighten rules for pass-through entities, affecting after-tax yields for holders.

Adjustments to capital gains treatment or Section 199A-like provisions by end-2025 could reduce institutional demand; REITs accounted for about 2.6% of U.S. equity market cap in 2024, signaling sensitivity to tax shifts.

Maintaining 90% distribution compliance is essential to keep corporate tax exemption, and failure to meet payout rules would trigger full corporate taxation and materially impair cash flows and shareholder returns.

Local Zoning and Land Use Policies

Local zoning boards and planning committees materially affect Tanger Factory Outlet Centers expansion: municipal approvals can delay redevelopment timelines by 12–24 months, increasing project costs by an estimated 10–18% per industry studies. Navigating permitting and community hearings is essential for adding mixed-use components (residential/office) to modernize centers and retain NOI growth. Stable local politics keeps multi-year pipelines predictable, protecting capex efficiency and IRR assumptions.

Geopolitical Stability and Supply Chains

Global political tensions—notably supply disruptions from China and the Red Sea routes—threaten manufacturing for many of Tanger’s brand tenants; 2024 container throughput delays increased U.S. retail stockouts by ~12%, pressuring tenant sales and rent coverage ratios.

Instability in key regions in 2025 could exacerbate inventory shortages, reducing tenant same-store sales and raising tenant delinquency risk; Tanger’s net lease model is indirectly exposed through tenant revenue declines.

- 2024 U.S. retail stockouts up ~12%

- Container delays increased lead times by ~15–20%

- Tenant sales declines raise rent default risk

Government Infrastructure Spending

State and federal funding for highways and public transit directly affects Tanger foot traffic; the U.S. enacted $120B for highways in FY2024 via the Infrastructure Investment and Jobs Act allocations, benefiting regional corridors near several Tanger sites.

Political prioritization of corridors can expand a location’s catchment and sales; Tanger reported 2024 same-center sales growth of 5.8%, partly tied to improved access at renovated sites.

Conversely, prolonged construction or deferred maintenance reduces visits and leasing demand, making local government advocacy essential for site performance.

- Infrastructure funding: $120B federal highway allocations (2024)

- Impact on sales: Tanger 2024 same-center sales +5.8%

- Risk: construction/neglect can depress traffic and leasing

- Action: prioritize local government advocacy

Political risks, tariffs and supply shocks squeeze tenant margins and Tanger NOI

Political risks—tariffs (+5–10% landed costs 2024–25), protectionism, supply-chain disruptions (2024 U.S. retail stockouts +12%, lead times +15–20%) and potential REIT tax rule changes—pressure tenant margins, sales and Tanger cash flows; local zoning and infrastructure funding (FY2024 $120B highways) materially affect redevelopment timelines, foot traffic and NOI.

| Metric | Value |

|---|---|

| Tariff impact | +5–10% |

| Stockouts | +12% (2024) |

| Lead times | +15–20% |

| Highway funding | $120B (FY2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Tanger Factory Outlet Centers, using current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE snapshot of Tanger Factory Outlet Centers that highlights regulatory, economic, and consumer trends to streamline meeting prep and support quick risk/positioning decisions.

Economic factors

Interest Rate Environment and Cost of Capital

As a capital-intensive REIT, Tanger is highly sensitive to Federal Reserve rate cycles through 2025; the fed funds rate rose to 5.25–5.50% in 2023–24, lifting average borrowing costs and pushing Tanger’s secured debt yields higher, increasing financing costs for acquisitions and capex.

Higher rates raise Tanger’s cost of debt and pressure net interest expense—Tanger had $1.1B total debt at YE 2024—while lower rates compress cap rates and can revalue properties upward, boosting NAV.

Tanger’s ability to refinance $300–400M of maturing debt over 2025 at favorable spreads is critical to sustaining FFO and its $0.32 quarterly dividend.

Consumer Discretionary Spending Trends

The outlet model depends on consumers seeking brand goods at discounts, so Tanger's traffic is tied to disposable income; U.S. real median household income rose 2.6% in 2024 but wage growth slowed to about 3.2% Y/Y by Q4 2025, affecting spending power. Household debt service ratios climbed to ~13.2% by end-2025, constraining big-ticket discretionary buys and reducing trip frequency. Historically Tanger shows counter-cyclical strength—Q3 2020 footfall fell less than full-price malls as shoppers traded down—supporting resilience during moderate downturns.

Inflationary Pressures on Operational Costs

Persistent inflation drove US CPI to 3.4% in 2024 and raised property management costs—wages, insurance, and maintenance—by mid-single digits, squeezing margins. Tanger’s triple-net leases transfer many operating expenses to tenants, but sustained inflation contributed to national retail vacancy pressures (shopping-center vacancy ~6.1% in 2024), risking tenant distress. Managing rent escalations without eroding tenant profitability is a material strategic challenge for Tanger.

Employment Rates and Labor Market Dynamics

The U.S. unemployment rate stood at 3.7% in December 2025, supporting consumer spending that underpins outlet traffic and discretionary purchases at Tanger centers.

Tight labor markets have pushed retail job openings above 1.6 million in late 2025, risking staffing shortages for Tanger tenants, reduced hours, and weaker in-store service.

Monitoring regional unemployment—ranging from under 3% in some Sun Belt metros to over 6% in certain Rust Belt areas—helps Tanger gauge localized demand resilience and tenant performance.

- US unemployment 3.7% (Dec 2025)

- Retail job openings ~1.6M (Q4 2025)

- Regional unemployment variance 3%–6%+

E-commerce Penetration and Retail Parity

As of late 2025, growing e-commerce share (U.S. online retail ~19.5% of total retail sales in 2024–25) pressures Tanger to keep outlet price spreads large enough to offset average consumer travel costs (~$9–$12 per trip) and rising last-mile logistics volatility.

The experiential value—immediate purchase, perceived bargains, and in-person clearance—remains Tanger’s chief economic defense versus digital discount giants that captured ~25–30% of off-price sales by 2024.

- U.S. e-commerce penetration ~19.5% (2024–25)

- Consumer travel cost per outlet visit estimated $9–$12

- Digital channels hold ~25–30% of off-price market share (2024)

- Need to maintain price spread and experiential draws to justify trips

Tanger pressured by higher rates, $1.1B debt and e‑commerce headwinds

Tanger faces higher financing costs after Fed hikes (fed funds 5.25–5.50% in 2024), $1.1B debt (YE 2024), and $300–400M maturities in 2025; consumer demand is supported by 3.7% unemployment (Dec 2025) but constrained by rising DSR (~13.2%) and 3.4% CPI (2024). E-commerce (19.5% of retail) and off-price digital share (25–30%) pressure foot traffic; triple-net leases partly mitigate inflationary cost pass-through.

| Metric | Value |

|---|---|

| Total debt (YE 2024) | $1.1B |

| Fed funds | 5.25–5.50% (2024) |

| Unemployment | 3.7% (Dec 2025) |

| CPI | 3.4% (2024) |

| E-commerce | 19.5% (2024–25) |

Preview the Actual Deliverable

Tanger Factory Outlet Centers PESTLE Analysis

The preview shown here is the exact PESTLE analysis for Tanger Factory Outlet Centers you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, consumer spending trends, and sustainability regulations are reshaping Tanger Factory Outlet Centers’ growth prospects—our concise PESTLE preview highlights key external drivers and risks to watch. Purchase the full PESTLE analysis for a complete, actionable breakdown with ready-to-use insights for investors, strategists, and advisors.

Political factors

Trade Policy and Import Tariffs

Changes in international trade agreements and tariffs directly affect cost of goods for Tanger tenants; import tariffs rising 5-10% in 2024–2025 increased landed costs for apparel brands, pressuring margins and potentially raising retail prices.

Shifts toward protectionism in late 2025 risk further price inflation for designer apparel/accessories, which could reduce tenant gross margins (industry average apparel margin fell to ~48% in 2024 from 51% in 2021) and dampen consumer demand.

Tanger must monitor geopolitical developments—US-China tariff fluctuations and US trade policy revisions—since supply-chain disruptions and inventory delays for global brands occupying Tanger centers can increase stockouts and operating volatility.

REIT Tax Legislation and Compliance

Tanger operates as a REIT, enjoying pass-through taxation but faces federal legislative risk; Congressional proposals through 2025 could change tax rates on REITs or tighten rules for pass-through entities, affecting after-tax yields for holders.

Adjustments to capital gains treatment or Section 199A-like provisions by end-2025 could reduce institutional demand; REITs accounted for about 2.6% of U.S. equity market cap in 2024, signaling sensitivity to tax shifts.

Maintaining 90% distribution compliance is essential to keep corporate tax exemption, and failure to meet payout rules would trigger full corporate taxation and materially impair cash flows and shareholder returns.

Local Zoning and Land Use Policies

Local zoning boards and planning committees materially affect Tanger Factory Outlet Centers expansion: municipal approvals can delay redevelopment timelines by 12–24 months, increasing project costs by an estimated 10–18% per industry studies. Navigating permitting and community hearings is essential for adding mixed-use components (residential/office) to modernize centers and retain NOI growth. Stable local politics keeps multi-year pipelines predictable, protecting capex efficiency and IRR assumptions.

Geopolitical Stability and Supply Chains

Global political tensions—notably supply disruptions from China and the Red Sea routes—threaten manufacturing for many of Tanger’s brand tenants; 2024 container throughput delays increased U.S. retail stockouts by ~12%, pressuring tenant sales and rent coverage ratios.

Instability in key regions in 2025 could exacerbate inventory shortages, reducing tenant same-store sales and raising tenant delinquency risk; Tanger’s net lease model is indirectly exposed through tenant revenue declines.

- 2024 U.S. retail stockouts up ~12%

- Container delays increased lead times by ~15–20%

- Tenant sales declines raise rent default risk

Government Infrastructure Spending

State and federal funding for highways and public transit directly affects Tanger foot traffic; the U.S. enacted $120B for highways in FY2024 via the Infrastructure Investment and Jobs Act allocations, benefiting regional corridors near several Tanger sites.

Political prioritization of corridors can expand a location’s catchment and sales; Tanger reported 2024 same-center sales growth of 5.8%, partly tied to improved access at renovated sites.

Conversely, prolonged construction or deferred maintenance reduces visits and leasing demand, making local government advocacy essential for site performance.

- Infrastructure funding: $120B federal highway allocations (2024)

- Impact on sales: Tanger 2024 same-center sales +5.8%

- Risk: construction/neglect can depress traffic and leasing

- Action: prioritize local government advocacy

Political risks, tariffs and supply shocks squeeze tenant margins and Tanger NOI

Political risks—tariffs (+5–10% landed costs 2024–25), protectionism, supply-chain disruptions (2024 U.S. retail stockouts +12%, lead times +15–20%) and potential REIT tax rule changes—pressure tenant margins, sales and Tanger cash flows; local zoning and infrastructure funding (FY2024 $120B highways) materially affect redevelopment timelines, foot traffic and NOI.

| Metric | Value |

|---|---|

| Tariff impact | +5–10% |

| Stockouts | +12% (2024) |

| Lead times | +15–20% |

| Highway funding | $120B (FY2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Tanger Factory Outlet Centers, using current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE snapshot of Tanger Factory Outlet Centers that highlights regulatory, economic, and consumer trends to streamline meeting prep and support quick risk/positioning decisions.

Economic factors

Interest Rate Environment and Cost of Capital

As a capital-intensive REIT, Tanger is highly sensitive to Federal Reserve rate cycles through 2025; the fed funds rate rose to 5.25–5.50% in 2023–24, lifting average borrowing costs and pushing Tanger’s secured debt yields higher, increasing financing costs for acquisitions and capex.

Higher rates raise Tanger’s cost of debt and pressure net interest expense—Tanger had $1.1B total debt at YE 2024—while lower rates compress cap rates and can revalue properties upward, boosting NAV.

Tanger’s ability to refinance $300–400M of maturing debt over 2025 at favorable spreads is critical to sustaining FFO and its $0.32 quarterly dividend.

Consumer Discretionary Spending Trends

The outlet model depends on consumers seeking brand goods at discounts, so Tanger's traffic is tied to disposable income; U.S. real median household income rose 2.6% in 2024 but wage growth slowed to about 3.2% Y/Y by Q4 2025, affecting spending power. Household debt service ratios climbed to ~13.2% by end-2025, constraining big-ticket discretionary buys and reducing trip frequency. Historically Tanger shows counter-cyclical strength—Q3 2020 footfall fell less than full-price malls as shoppers traded down—supporting resilience during moderate downturns.

Inflationary Pressures on Operational Costs

Persistent inflation drove US CPI to 3.4% in 2024 and raised property management costs—wages, insurance, and maintenance—by mid-single digits, squeezing margins. Tanger’s triple-net leases transfer many operating expenses to tenants, but sustained inflation contributed to national retail vacancy pressures (shopping-center vacancy ~6.1% in 2024), risking tenant distress. Managing rent escalations without eroding tenant profitability is a material strategic challenge for Tanger.

Employment Rates and Labor Market Dynamics

The U.S. unemployment rate stood at 3.7% in December 2025, supporting consumer spending that underpins outlet traffic and discretionary purchases at Tanger centers.

Tight labor markets have pushed retail job openings above 1.6 million in late 2025, risking staffing shortages for Tanger tenants, reduced hours, and weaker in-store service.

Monitoring regional unemployment—ranging from under 3% in some Sun Belt metros to over 6% in certain Rust Belt areas—helps Tanger gauge localized demand resilience and tenant performance.

- US unemployment 3.7% (Dec 2025)

- Retail job openings ~1.6M (Q4 2025)

- Regional unemployment variance 3%–6%+

E-commerce Penetration and Retail Parity

As of late 2025, growing e-commerce share (U.S. online retail ~19.5% of total retail sales in 2024–25) pressures Tanger to keep outlet price spreads large enough to offset average consumer travel costs (~$9–$12 per trip) and rising last-mile logistics volatility.

The experiential value—immediate purchase, perceived bargains, and in-person clearance—remains Tanger’s chief economic defense versus digital discount giants that captured ~25–30% of off-price sales by 2024.

- U.S. e-commerce penetration ~19.5% (2024–25)

- Consumer travel cost per outlet visit estimated $9–$12

- Digital channels hold ~25–30% of off-price market share (2024)

- Need to maintain price spread and experiential draws to justify trips

Tanger pressured by higher rates, $1.1B debt and e‑commerce headwinds

Tanger faces higher financing costs after Fed hikes (fed funds 5.25–5.50% in 2024), $1.1B debt (YE 2024), and $300–400M maturities in 2025; consumer demand is supported by 3.7% unemployment (Dec 2025) but constrained by rising DSR (~13.2%) and 3.4% CPI (2024). E-commerce (19.5% of retail) and off-price digital share (25–30%) pressure foot traffic; triple-net leases partly mitigate inflationary cost pass-through.

| Metric | Value |

|---|---|

| Total debt (YE 2024) | $1.1B |

| Fed funds | 5.25–5.50% (2024) |

| Unemployment | 3.7% (Dec 2025) |

| CPI | 3.4% (2024) |

| E-commerce | 19.5% (2024–25) |

Preview the Actual Deliverable

Tanger Factory Outlet Centers PESTLE Analysis

The preview shown here is the exact PESTLE analysis for Tanger Factory Outlet Centers you’ll receive after purchase—fully formatted, professionally structured, and ready to use.