Tapestry PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Tapestry’s competitive landscape in our targeted PESTLE Analysis—designed for investors and strategists who need quick, actionable insights; purchase the full report to access the complete, editable breakdown and make smarter decisions fast.

Political factors

Trade Policy and Tariffs

The global trade environment remains critical for Tapestry in late 2025 as fluctuating tariffs on luxury goods raised import duties by up to 12% in key markets, pressuring gross margins; Tapestry reported a 3.4% margin compression in FY2024 linked to higher logistics and duty costs. Trade tensions between the US and China continue to affect raw material and finished-goods costs from Asian hubs, with apparel input prices up ~6% year-over-year as of Q3 2025. Management must navigate shifting policies to protect margins while avoiding significant consumer price hikes amid 4.8% luxury spending growth in 2024.

Geopolitical Stability in Asia

As roughly 20% of Tapestry’s 2025 revenue came from Greater China, geopolitical stability in Asia is critical for operational continuity; any escalation—e.g., cross-strait tensions—could disrupt supply chains that source leather and finished goods from the region. Escalation risks may also dampen consumer sentiment in high-growth luxury hubs, where comparable-store sales growth in China swung between +8% and -4% in 2023–2024. Tapestry mitigates exposure via a diversified regional strategy, growing wholesale and digital channels outside China and shifting inventory and production across Asia and Latin America to reduce localized political and diplomatic risk.

Global Tax Policy Changes

Changes in corporate tax rates and shifts in international tax treaties directly affect Tapestry’s net margin and cash flow across the US, EU and Greater China, where FY2024 revenue was $6.8bn; a 1ppt effective tax rate change could alter annual after-tax income by roughly $34m. The OECD/G20 minimum global tax (15%) forces rigorous tax planning to remain compliant while protecting shareholder returns through transfer pricing and capital allocation. These rules materially influence location choices for new stores and logistics investments, where after-tax return hurdles now incorporate minimum-tax impacts on ROI and free cash flow.

Government Support for Retail

Government initiatives to boost domestic consumption, such as China’s 2024 consumption vouchers (RMB 200–500 per capita in pilot cities) and India’s state-level retail subsidies, can lift Tapestry’s brick-and-mortar sales by increasing foot traffic and average transaction values.

Temporary VAT reductions—like the EU’s selective VAT relief in late‑2023 that raised retail sales ~1.2% month-on-month—are tracked to time inventory and promotions; sudden withdrawal forces rapid marketing and pricing shifts to sustain sales.

- Track stimulus programs by market (China vouchers, India subsidies)

- Monitor VAT/tax changes; EU relief raised retail ~1.2% in late 2023

- Prepare agile marketing playbooks for subsidy withdrawal

Supply Chain Reshoring Pressures

Political pushes to reshore manufacturing challenge Tapestry as US apparel wages average about 3–4x lower-cost countries; reshoring could raise COGS and shrink 2025 gross margin (latest reported 70.7% in FY2024) but may shorten lead times and boost US sales tied to “Made in USA” premiums.

Tapestry balances these pressures against a global network that produced ~60% of goods in Asia in 2024, weighing higher domestic labor costs versus inventory efficiency and brand positioning.

- Reshoring may raise labor/ops costs vs FY2024 gross margin 70.7%

- ~60% production in Asia (2024) — supply chain efficiency

- Shorter lead times and patriotic premium could lift US demand

Tapestry margins squeezed by tariffs, OECD tax and reshoring—channel shifts underway

Political risks—tariff volatility (up to +12% on luxury imports), US‑China tensions, and OECD 15% minimum tax—are squeezing Tapestry’s margins (3.4% FY2024 compression; FY2024 revenue $6.8bn; gross margin 70.7%) while reshoring pressures (US wages ~3–4x higher) and stimulus/VAT moves (China vouchers, EU VAT relief +1.2% retail) drive channel and sourcing strategy shifts.

| Factor | Metric/Impact |

|---|---|

| Tariffs | +12% duties; margin pressure |

| FY2024 figures | Revenue $6.8bn; gross margin 70.7%; margin compression 3.4% |

| OECD tax | 15% minimum tax; ~+$34m per 1ppt ETR |

| Production | ~60% Asia (2024); US wages 3–4x |

| Stimulus/VAT | China vouchers; EU VAT +1.2% retail |

What is included in the product

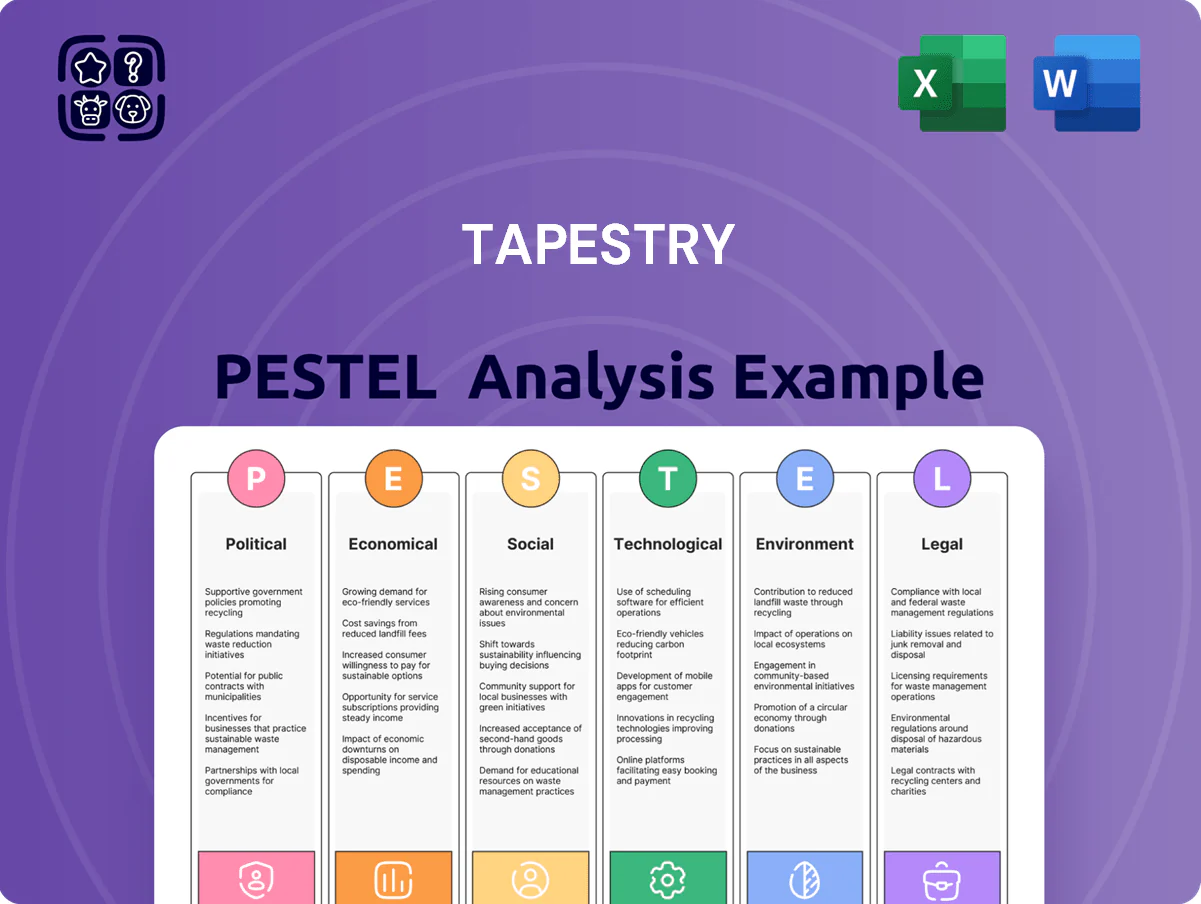

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Tapestry’s luxury fashion operations, supply chain, and consumer demand, with each category expanded into specific, data-backed subpoints and forward-looking implications for strategy and risk management.

A concise PESTLE snapshot of Tapestry that highlights external risks and opportunities for quick inclusion in decks or meetings, helping teams align strategy and speed decision-making.

Economic factors

Global Inflationary Pressures

Persistent inflation in key markets eroded purchasing power for aspirational luxury consumers through 2025, with US CPI averaging 4.1% y/y and euro area inflation near 5% in H1 2025, prompting more selective discretionary purchases for brands like Coach and Kate Spade.

High-net-worth individuals sustained spending—global luxury spending rose ~3% in 2025—while middle-class demand softened, with mid-tier accessories unit sales down an estimated 6–8% year-over-year.

Tapestry optimized pricing architecture, executing targeted markdowns and premiumization strategies that improved blended ASPs by ~2.5% and helped protect gross margin, which held around 58% in FY 2025.

Currency Exchange Volatility

As a multinational, Tapestry is highly sensitive to USD moves versus EUR, JPY and CNY; a 10% USD appreciation trimmed 2024 revenue by about $180m in currency translation per company disclosures. A stronger dollar creates translation losses and raises price points for international tourists, pressuring same-store sales in key markets. Tapestry reported $1.2bn of FX hedging instruments at end-2024, using forwards and options to stabilize annual EPS.

Disposable Income Trends

North American and European disposable income rose modestly in 2024—real household disposable income up ~1.8% in the US and ~1.2% in the EU—supporting demand for premium accessories; higher-income quintiles drove most luxury spend. Forecasts for late 2025 project consumer spending growth of ~1.5–2.0% as unemployment stays near multi-year lows (US ~3.7% in 2024). Tapestry times launches and promotions to coincide with payroll and holiday cycles in these regions to maximize conversion.

Interest Rate Environment

The prevailing higher interest rate environment raises Tapestry's weighted average cost of capital, squeezing margins and making debt-funded acquisitions or capex more expensive; U.S. 10-year Treasury yields rose from ~1.5% in 2021 to ~4.5% in 2024, increasing borrowing costs materially.

Higher rates elevate interest expense on existing and new debt, potentially slowing store renovations and digital investments; Tapestry reported net cash of $1.2 billion and total debt of $1.4 billion at FY2024-end, guiding cautious pacing.

Financial leadership emphasizes liquidity and a strong balance sheet—maintaining over $1 billion cash and targeted leverage below 1.0x net debt/EBITDA—to navigate monetary cycles and preserve strategic optionality.

- Higher rates increase WACC and borrowing costs (10y UST ~4.5% in 2024)

- FY2024 cash ~$1.2B; total debt ~$1.4B

- Target leverage <1.0x net debt/EBITDA to retain acquisition/capex optionality

Growth in Emerging Markets

Economic expansion in Southeast Asia and parts of Latin America offers Tapestry revenue diversification beyond North America and Europe; ASEAN GDP grew about 4.9% in 2024 and Latin America's GDP rebounded ~2.6% in 2024, expanding middle-class consumption.

Rising middle-class households—projected to add ~200 million consumers in EMs by 2030—boost demand for accessible luxury, and Tapestry is allocating CAPEX and retail/omni-channel investments to gain early market share ahead of competitors.

- ASEAN GDP ~4.9% (2024)

- Latin America GDP ~2.6% (2024)

- ~200M new EM middle-class consumers by 2030

- Tapestry increasing regional store openings and digital spend

Tapestry weathers FX drag, protects margins as HNW luxury demand rises

Inflation softened discretionary spend (US CPI ~4.1% y/y; euro area ~5% H1‑2025) while HNW luxury demand grew ~3% in 2025; Tapestry protected margins (gross ~58%, ASP +2.5%) via pricing/markdowns. USD strength cut ~ $180m revenue (2024) and FX hedges $1.2bn. FY2024 cash ~$1.2bn, debt ~$1.4bn; target leverage <1.0x. ASEAN GDP ~4.9% and LatAm ~2.6% (2024).

| Metric | Value |

|---|---|

| Gross margin FY2025 | ~58% |

| ASP change | +2.5% |

| Cash / Debt (FY2024) | $1.2B / $1.4B |

| USD FX impact (2024) | ~$180M |

| ASEAN / LatAm GDP (2024) | 4.9% / 2.6% |

Preview Before You Purchase

Tapestry PESTLE Analysis

The preview shown here is the exact Tapestry PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are the final file you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and emerging technologies are reshaping Tapestry’s competitive landscape in our targeted PESTLE Analysis—designed for investors and strategists who need quick, actionable insights; purchase the full report to access the complete, editable breakdown and make smarter decisions fast.

Political factors

Trade Policy and Tariffs

The global trade environment remains critical for Tapestry in late 2025 as fluctuating tariffs on luxury goods raised import duties by up to 12% in key markets, pressuring gross margins; Tapestry reported a 3.4% margin compression in FY2024 linked to higher logistics and duty costs. Trade tensions between the US and China continue to affect raw material and finished-goods costs from Asian hubs, with apparel input prices up ~6% year-over-year as of Q3 2025. Management must navigate shifting policies to protect margins while avoiding significant consumer price hikes amid 4.8% luxury spending growth in 2024.

Geopolitical Stability in Asia

As roughly 20% of Tapestry’s 2025 revenue came from Greater China, geopolitical stability in Asia is critical for operational continuity; any escalation—e.g., cross-strait tensions—could disrupt supply chains that source leather and finished goods from the region. Escalation risks may also dampen consumer sentiment in high-growth luxury hubs, where comparable-store sales growth in China swung between +8% and -4% in 2023–2024. Tapestry mitigates exposure via a diversified regional strategy, growing wholesale and digital channels outside China and shifting inventory and production across Asia and Latin America to reduce localized political and diplomatic risk.

Global Tax Policy Changes

Changes in corporate tax rates and shifts in international tax treaties directly affect Tapestry’s net margin and cash flow across the US, EU and Greater China, where FY2024 revenue was $6.8bn; a 1ppt effective tax rate change could alter annual after-tax income by roughly $34m. The OECD/G20 minimum global tax (15%) forces rigorous tax planning to remain compliant while protecting shareholder returns through transfer pricing and capital allocation. These rules materially influence location choices for new stores and logistics investments, where after-tax return hurdles now incorporate minimum-tax impacts on ROI and free cash flow.

Government Support for Retail

Government initiatives to boost domestic consumption, such as China’s 2024 consumption vouchers (RMB 200–500 per capita in pilot cities) and India’s state-level retail subsidies, can lift Tapestry’s brick-and-mortar sales by increasing foot traffic and average transaction values.

Temporary VAT reductions—like the EU’s selective VAT relief in late‑2023 that raised retail sales ~1.2% month-on-month—are tracked to time inventory and promotions; sudden withdrawal forces rapid marketing and pricing shifts to sustain sales.

- Track stimulus programs by market (China vouchers, India subsidies)

- Monitor VAT/tax changes; EU relief raised retail ~1.2% in late 2023

- Prepare agile marketing playbooks for subsidy withdrawal

Supply Chain Reshoring Pressures

Political pushes to reshore manufacturing challenge Tapestry as US apparel wages average about 3–4x lower-cost countries; reshoring could raise COGS and shrink 2025 gross margin (latest reported 70.7% in FY2024) but may shorten lead times and boost US sales tied to “Made in USA” premiums.

Tapestry balances these pressures against a global network that produced ~60% of goods in Asia in 2024, weighing higher domestic labor costs versus inventory efficiency and brand positioning.

- Reshoring may raise labor/ops costs vs FY2024 gross margin 70.7%

- ~60% production in Asia (2024) — supply chain efficiency

- Shorter lead times and patriotic premium could lift US demand

Tapestry margins squeezed by tariffs, OECD tax and reshoring—channel shifts underway

Political risks—tariff volatility (up to +12% on luxury imports), US‑China tensions, and OECD 15% minimum tax—are squeezing Tapestry’s margins (3.4% FY2024 compression; FY2024 revenue $6.8bn; gross margin 70.7%) while reshoring pressures (US wages ~3–4x higher) and stimulus/VAT moves (China vouchers, EU VAT relief +1.2% retail) drive channel and sourcing strategy shifts.

| Factor | Metric/Impact |

|---|---|

| Tariffs | +12% duties; margin pressure |

| FY2024 figures | Revenue $6.8bn; gross margin 70.7%; margin compression 3.4% |

| OECD tax | 15% minimum tax; ~+$34m per 1ppt ETR |

| Production | ~60% Asia (2024); US wages 3–4x |

| Stimulus/VAT | China vouchers; EU VAT +1.2% retail |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Tapestry’s luxury fashion operations, supply chain, and consumer demand, with each category expanded into specific, data-backed subpoints and forward-looking implications for strategy and risk management.

A concise PESTLE snapshot of Tapestry that highlights external risks and opportunities for quick inclusion in decks or meetings, helping teams align strategy and speed decision-making.

Economic factors

Global Inflationary Pressures

Persistent inflation in key markets eroded purchasing power for aspirational luxury consumers through 2025, with US CPI averaging 4.1% y/y and euro area inflation near 5% in H1 2025, prompting more selective discretionary purchases for brands like Coach and Kate Spade.

High-net-worth individuals sustained spending—global luxury spending rose ~3% in 2025—while middle-class demand softened, with mid-tier accessories unit sales down an estimated 6–8% year-over-year.

Tapestry optimized pricing architecture, executing targeted markdowns and premiumization strategies that improved blended ASPs by ~2.5% and helped protect gross margin, which held around 58% in FY 2025.

Currency Exchange Volatility

As a multinational, Tapestry is highly sensitive to USD moves versus EUR, JPY and CNY; a 10% USD appreciation trimmed 2024 revenue by about $180m in currency translation per company disclosures. A stronger dollar creates translation losses and raises price points for international tourists, pressuring same-store sales in key markets. Tapestry reported $1.2bn of FX hedging instruments at end-2024, using forwards and options to stabilize annual EPS.

Disposable Income Trends

North American and European disposable income rose modestly in 2024—real household disposable income up ~1.8% in the US and ~1.2% in the EU—supporting demand for premium accessories; higher-income quintiles drove most luxury spend. Forecasts for late 2025 project consumer spending growth of ~1.5–2.0% as unemployment stays near multi-year lows (US ~3.7% in 2024). Tapestry times launches and promotions to coincide with payroll and holiday cycles in these regions to maximize conversion.

Interest Rate Environment

The prevailing higher interest rate environment raises Tapestry's weighted average cost of capital, squeezing margins and making debt-funded acquisitions or capex more expensive; U.S. 10-year Treasury yields rose from ~1.5% in 2021 to ~4.5% in 2024, increasing borrowing costs materially.

Higher rates elevate interest expense on existing and new debt, potentially slowing store renovations and digital investments; Tapestry reported net cash of $1.2 billion and total debt of $1.4 billion at FY2024-end, guiding cautious pacing.

Financial leadership emphasizes liquidity and a strong balance sheet—maintaining over $1 billion cash and targeted leverage below 1.0x net debt/EBITDA—to navigate monetary cycles and preserve strategic optionality.

- Higher rates increase WACC and borrowing costs (10y UST ~4.5% in 2024)

- FY2024 cash ~$1.2B; total debt ~$1.4B

- Target leverage <1.0x net debt/EBITDA to retain acquisition/capex optionality

Growth in Emerging Markets

Economic expansion in Southeast Asia and parts of Latin America offers Tapestry revenue diversification beyond North America and Europe; ASEAN GDP grew about 4.9% in 2024 and Latin America's GDP rebounded ~2.6% in 2024, expanding middle-class consumption.

Rising middle-class households—projected to add ~200 million consumers in EMs by 2030—boost demand for accessible luxury, and Tapestry is allocating CAPEX and retail/omni-channel investments to gain early market share ahead of competitors.

- ASEAN GDP ~4.9% (2024)

- Latin America GDP ~2.6% (2024)

- ~200M new EM middle-class consumers by 2030

- Tapestry increasing regional store openings and digital spend

Tapestry weathers FX drag, protects margins as HNW luxury demand rises

Inflation softened discretionary spend (US CPI ~4.1% y/y; euro area ~5% H1‑2025) while HNW luxury demand grew ~3% in 2025; Tapestry protected margins (gross ~58%, ASP +2.5%) via pricing/markdowns. USD strength cut ~ $180m revenue (2024) and FX hedges $1.2bn. FY2024 cash ~$1.2bn, debt ~$1.4bn; target leverage <1.0x. ASEAN GDP ~4.9% and LatAm ~2.6% (2024).

| Metric | Value |

|---|---|

| Gross margin FY2025 | ~58% |

| ASP change | +2.5% |

| Cash / Debt (FY2024) | $1.2B / $1.4B |

| USD FX impact (2024) | ~$180M |

| ASEAN / LatAm GDP (2024) | 4.9% / 2.6% |

Preview Before You Purchase

Tapestry PESTLE Analysis

The preview shown here is the exact Tapestry PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are the final file you’ll download immediately after payment.