TaskUs Porter's Five Forces Analysis

From Overview to Strategy Blueprint

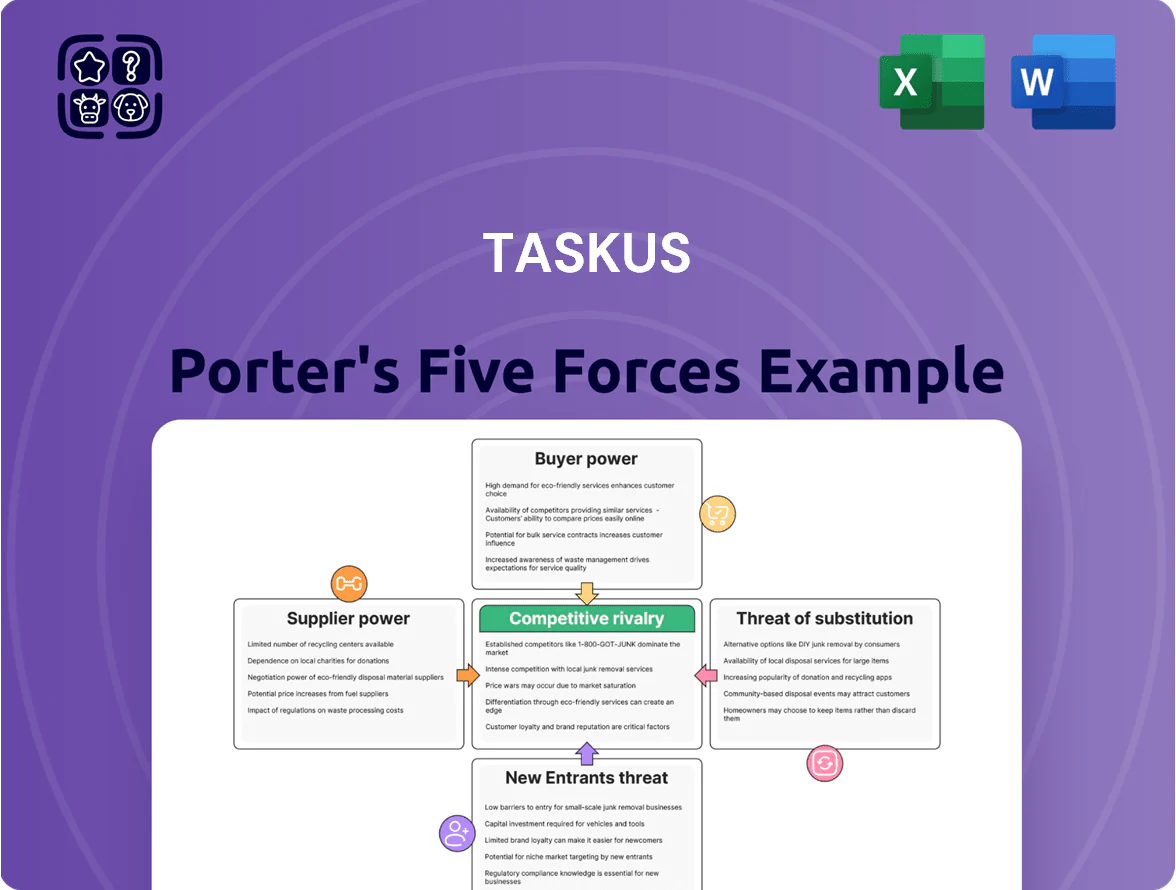

TaskUs faces nuanced competitive pressures across supplier leverage, buyer power, new entrant threats, substitute services, and rival intensity—this snapshot highlights key dynamics but only scratches the surface.

Suppliers Bargaining Power

Specialized AI talent pool

The global shortage of AI talent tightened in 2024–25: LinkedIn reported 34% annual growth in AI roles and Glassdoor showed AI engineer median pay rose ~22% to ~$150k in the US by 2025, giving specialized data scientists outsized bargaining power over TaskUs as it scales AI services.

Cloud infrastructure dependency

TaskUs depends on AWS and Azure for core hosting and AI workloads, raising supplier power since switching clouds incurs migration costs often >$1m for enterprise setups and months of downtime risk. Public-cloud pricing rose ~9–12% in 2023–2024 for compute and storage, so vendor hikes flow straight into TaskUs opex and gross margins. If providers add sustained price increases of 5%+, project feasibility and pricing competitiveness could be materially squeezed.

Proprietary software vendors

TaskUs relies on third-party proprietary tools for content moderation and CRM, and while many vendors exist, deeply integrated enterprise platforms create lock-in that gives suppliers moderate bargaining power; global enterprise software spending hit $1.2 trillion in 2024, so vendor pricing shifts can meaningfully raise TaskUs’s tech costs. TaskUs must trade higher licensing spend—often 10–20% of tech budgets—against client demands for advanced AI-driven moderation to retain contracts.

Global real estate developers

Global real estate developers exert moderate supplier power over TaskUs because specialized office hubs in the Philippines and India meet security and connectivity needs; Manila and Cebu vacancy rates were 6.5% and 4.2% in 2024, tightening supply.

Hybrid work reduced dependence on large leases—TaskUs kept smaller physical footprints—so developer leverage is lower than in 2019, though premium data-center-like office spaces still command 10–25% rent premiums.

- Manila vacancy 6.5% (2024)

- Cebu vacancy 4.2% (2024)

- Premium space rent +10–25%

- Hybrid work reduces full-time space needs

Recruitment and training agencies

Recruitment and training agencies hold moderate to high bargaining power for TaskUs because they supply tens of thousands of frontline teammates across 20+ countries; in 2024 TaskUs reported ~45,000 employees, so timely access to multilingual and niche-skilled hires is critical.

Agencies command leverage via specialized talent pools and local labor-market knowledge, impacting unit labor costs and time-to-fill; a 2023 industry survey showed median agency fees of 15–25% for skilled placements.

Rising AI talent and cloud costs squeeze suppliers—wider tech budget pressure

Suppliers exert moderate-to-high power: AI talent shortages (AI roles +34% y/y; US AI engineer pay +22% to ~$150k by 2025) and cloud/provider lock-in (AWS/Azure migration >$1m; public-cloud pricing +9–12% in 2023–24) raise costs; software licensing (10–20% of tech budgets) and local real estate tightness (Manila vac 6.5%, Cebu 4.2% in 2024) add pressure.

| Metric | 2024–25 |

|---|---|

| AI roles growth | +34% y/y |

| AI engineer pay (US) | ~$150k (+22%) |

| Cloud price change | +9–12% |

| Manila vacancy | 6.5% |

What is included in the product

Tailored Porter's Five Forces analysis for TaskUs that uncovers competitive drivers, buyer and supplier leverage, entry barriers, substitutes, and emerging threats to inform strategic positioning and investor materials.

A concise Porter's Five Forces one-sheet for TaskUs that highlights competitive pressures and relief strategies—ideal for fast, boardroom-ready decisions.

Customers Bargaining Power

High client concentration risk

TaskUs often derives 30–45% of revenue from its top three clients (FY2024: top client ~18%, top three ~42%), creating high client concentration risk; those customers can demand price cuts or tighter SLAs.

If a top-tier client churns, TaskUs could see an immediate EBITDA hit—roughly 10–20 percentage points depending on gross margin—plus share-price pressure seen in past vendor exits.

Low switching costs for buyers

TaskUs faces low switching costs: despite integration into client workflows, outsourced services let clients shift vendors at contract renewal, and many move to peers like Concentrix or Teleperformance with moderate effort; industry churn averages ~12–18% annually per Everest Group 2024, so TaskUs must innovate and boost value—Client revenue retention fell 3.4% in FY2024 when service gaps appeared—otherwise long-term contracts erode.

Demand for AI-driven efficiency

By late 2025, major TaskUs clients demand AI-integrated workflows that cut headcount and lower costs per interaction; 63% of enterprise buyers in a 2024 survey said AI savings must appear in renewals. Buyers can force price and scope changes at renewal, shifting innovation costs to TaskUs and pressuring capex and R&D—TaskUs reported 18% YoY tech spend growth in 2024 to meet lower per-interaction targets.

Price sensitivity in the tech sector

Many startup and mid-market tech clients TaskUs serves face intense profitability pressure, making them highly price-sensitive for outsourced support and moderation; 2024 VC data show 42% fewer late-stage deals, raising cost-cutting urgency.

Clients routinely run competitive bids to lower unit costs—TaskUs pricing faces downward pressure as buyers demand sub-$1.00 per contact metrics in some US/EMEA deals.

Internalization of core functions

Large tech clients may internalize next-gen ops if seen as core IP; in 2024, 32% of enterprise AI projects moved in-house within 18 months per McKinsey, raising this risk for TaskUs.

As AI drives CX, buyers building internal ML teams (avg. $1.2M annual runrate per in-house model at Fortune 500 firms) reduce outsourcing demand and pressure margins.

The vertical-integration threat forces TaskUs to keep prices tight and service SLAs strong; loss of one 10% revenue client could cut EBITDA margin by ~2–3pp.

- 32% of enterprise AI projects moved in-house (2024)

- Avg $1.2M annual runrate per in-house model at Fortune 500

- One 10% client loss ≈ 2–3pp EBITDA impact

High client concentration & AI insourcing risk threatens margins and retention

High client concentration (FY2024: top client ~18%, top three ~42%) gives buyers strong leverage to demand price cuts, tighter SLAs, and AI-driven savings; industry churn ~12–18% (Everest Group 2024) and TaskUs’ 3.4% FY2024 retention dip heighten risk. Large clients may insource—32% of enterprise AI projects moved in-house within 18 months (McKinsey 2024)—pressuring margins and forcing >18% YoY tech spend growth (TaskUs 2024).

| Metric | Value |

|---|---|

| Top client (FY2024) | ~18% |

| Top 3 clients | ~42% |

| Industry churn | 12–18% (2024) |

| Client retention change | -3.4% (FY2024) |

| AI insource rate | 32% (2024) |

| TaskUs tech spend growth | ~18% YoY (2024) |

What You See Is What You Get

TaskUs Porter's Five Forces Analysis

This preview shows the exact TaskUs Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; fully formatted and ready for use. The document displayed here is the final deliverable, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. Once you buy, you’ll get instant access to this same file for download and application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

TaskUs faces nuanced competitive pressures across supplier leverage, buyer power, new entrant threats, substitute services, and rival intensity—this snapshot highlights key dynamics but only scratches the surface.

Suppliers Bargaining Power

Specialized AI talent pool

The global shortage of AI talent tightened in 2024–25: LinkedIn reported 34% annual growth in AI roles and Glassdoor showed AI engineer median pay rose ~22% to ~$150k in the US by 2025, giving specialized data scientists outsized bargaining power over TaskUs as it scales AI services.

Cloud infrastructure dependency

TaskUs depends on AWS and Azure for core hosting and AI workloads, raising supplier power since switching clouds incurs migration costs often >$1m for enterprise setups and months of downtime risk. Public-cloud pricing rose ~9–12% in 2023–2024 for compute and storage, so vendor hikes flow straight into TaskUs opex and gross margins. If providers add sustained price increases of 5%+, project feasibility and pricing competitiveness could be materially squeezed.

Proprietary software vendors

TaskUs relies on third-party proprietary tools for content moderation and CRM, and while many vendors exist, deeply integrated enterprise platforms create lock-in that gives suppliers moderate bargaining power; global enterprise software spending hit $1.2 trillion in 2024, so vendor pricing shifts can meaningfully raise TaskUs’s tech costs. TaskUs must trade higher licensing spend—often 10–20% of tech budgets—against client demands for advanced AI-driven moderation to retain contracts.

Global real estate developers

Global real estate developers exert moderate supplier power over TaskUs because specialized office hubs in the Philippines and India meet security and connectivity needs; Manila and Cebu vacancy rates were 6.5% and 4.2% in 2024, tightening supply.

Hybrid work reduced dependence on large leases—TaskUs kept smaller physical footprints—so developer leverage is lower than in 2019, though premium data-center-like office spaces still command 10–25% rent premiums.

- Manila vacancy 6.5% (2024)

- Cebu vacancy 4.2% (2024)

- Premium space rent +10–25%

- Hybrid work reduces full-time space needs

Recruitment and training agencies

Recruitment and training agencies hold moderate to high bargaining power for TaskUs because they supply tens of thousands of frontline teammates across 20+ countries; in 2024 TaskUs reported ~45,000 employees, so timely access to multilingual and niche-skilled hires is critical.

Agencies command leverage via specialized talent pools and local labor-market knowledge, impacting unit labor costs and time-to-fill; a 2023 industry survey showed median agency fees of 15–25% for skilled placements.

Rising AI talent and cloud costs squeeze suppliers—wider tech budget pressure

Suppliers exert moderate-to-high power: AI talent shortages (AI roles +34% y/y; US AI engineer pay +22% to ~$150k by 2025) and cloud/provider lock-in (AWS/Azure migration >$1m; public-cloud pricing +9–12% in 2023–24) raise costs; software licensing (10–20% of tech budgets) and local real estate tightness (Manila vac 6.5%, Cebu 4.2% in 2024) add pressure.

| Metric | 2024–25 |

|---|---|

| AI roles growth | +34% y/y |

| AI engineer pay (US) | ~$150k (+22%) |

| Cloud price change | +9–12% |

| Manila vacancy | 6.5% |

What is included in the product

Tailored Porter's Five Forces analysis for TaskUs that uncovers competitive drivers, buyer and supplier leverage, entry barriers, substitutes, and emerging threats to inform strategic positioning and investor materials.

A concise Porter's Five Forces one-sheet for TaskUs that highlights competitive pressures and relief strategies—ideal for fast, boardroom-ready decisions.

Customers Bargaining Power

High client concentration risk

TaskUs often derives 30–45% of revenue from its top three clients (FY2024: top client ~18%, top three ~42%), creating high client concentration risk; those customers can demand price cuts or tighter SLAs.

If a top-tier client churns, TaskUs could see an immediate EBITDA hit—roughly 10–20 percentage points depending on gross margin—plus share-price pressure seen in past vendor exits.

Low switching costs for buyers

TaskUs faces low switching costs: despite integration into client workflows, outsourced services let clients shift vendors at contract renewal, and many move to peers like Concentrix or Teleperformance with moderate effort; industry churn averages ~12–18% annually per Everest Group 2024, so TaskUs must innovate and boost value—Client revenue retention fell 3.4% in FY2024 when service gaps appeared—otherwise long-term contracts erode.

Demand for AI-driven efficiency

By late 2025, major TaskUs clients demand AI-integrated workflows that cut headcount and lower costs per interaction; 63% of enterprise buyers in a 2024 survey said AI savings must appear in renewals. Buyers can force price and scope changes at renewal, shifting innovation costs to TaskUs and pressuring capex and R&D—TaskUs reported 18% YoY tech spend growth in 2024 to meet lower per-interaction targets.

Price sensitivity in the tech sector

Many startup and mid-market tech clients TaskUs serves face intense profitability pressure, making them highly price-sensitive for outsourced support and moderation; 2024 VC data show 42% fewer late-stage deals, raising cost-cutting urgency.

Clients routinely run competitive bids to lower unit costs—TaskUs pricing faces downward pressure as buyers demand sub-$1.00 per contact metrics in some US/EMEA deals.

Internalization of core functions

Large tech clients may internalize next-gen ops if seen as core IP; in 2024, 32% of enterprise AI projects moved in-house within 18 months per McKinsey, raising this risk for TaskUs.

As AI drives CX, buyers building internal ML teams (avg. $1.2M annual runrate per in-house model at Fortune 500 firms) reduce outsourcing demand and pressure margins.

The vertical-integration threat forces TaskUs to keep prices tight and service SLAs strong; loss of one 10% revenue client could cut EBITDA margin by ~2–3pp.

- 32% of enterprise AI projects moved in-house (2024)

- Avg $1.2M annual runrate per in-house model at Fortune 500

- One 10% client loss ≈ 2–3pp EBITDA impact

High client concentration & AI insourcing risk threatens margins and retention

High client concentration (FY2024: top client ~18%, top three ~42%) gives buyers strong leverage to demand price cuts, tighter SLAs, and AI-driven savings; industry churn ~12–18% (Everest Group 2024) and TaskUs’ 3.4% FY2024 retention dip heighten risk. Large clients may insource—32% of enterprise AI projects moved in-house within 18 months (McKinsey 2024)—pressuring margins and forcing >18% YoY tech spend growth (TaskUs 2024).

| Metric | Value |

|---|---|

| Top client (FY2024) | ~18% |

| Top 3 clients | ~42% |

| Industry churn | 12–18% (2024) |

| Client retention change | -3.4% (FY2024) |

| AI insource rate | 32% (2024) |

| TaskUs tech spend growth | ~18% YoY (2024) |

What You See Is What You Get

TaskUs Porter's Five Forces Analysis

This preview shows the exact TaskUs Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; fully formatted and ready for use. The document displayed here is the final deliverable, covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. Once you buy, you’ll get instant access to this same file for download and application.