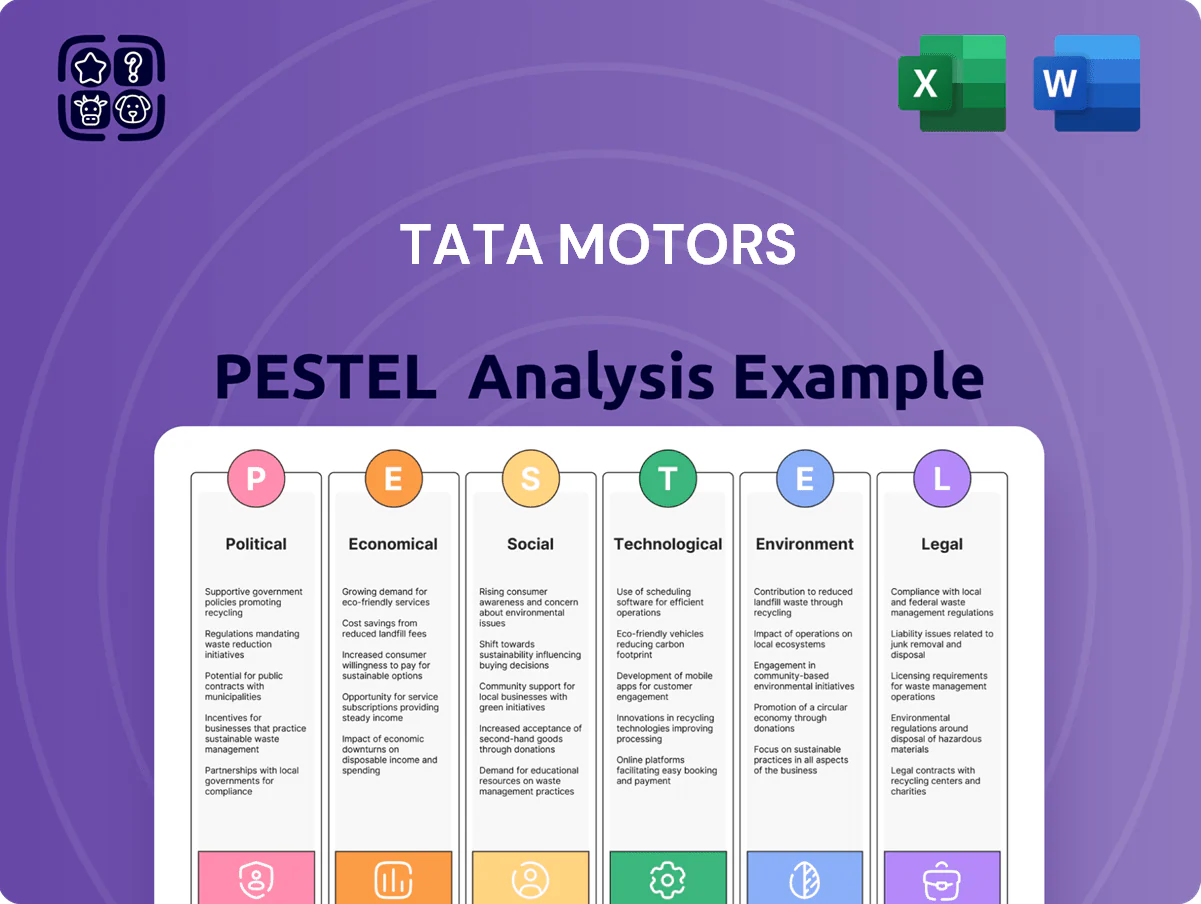

Tata Motors PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Understand how political shifts, supply‑chain pressures, and accelerating EV tech are shaping Tata Motors’ strategic path—our concise PESTLE snapshot highlights risks and opportunities you can act on immediately. Purchase the full PESTLE analysis to access a detailed, ready‑to‑use report with data‑backed insights, scenario implications, and strategic recommendations tailored for investors and decision‑makers.

Political factors

Government Incentives for Green Mobility

The Indian government continued prioritizing EV adoption into late 2025, extending FAME and PLI schemes that drove a 28% YoY rise in EV registrations in FY2024–25 and allocated ~Rs 20,000 crore for incentives and charging infrastructure.

Tata Motors gained cost advantages from subsidies and PLI-linked localisation, lowering EV unit costs by an estimated 8–12% and supporting a 2025 EV market share near 40% in passenger EVs.

Maintaining strong ties with policymakers remains crucial to secure further support for nationwide charging networks and domestic battery manufacturing, where India targeted 50 GWh battery capacity by 2027.

Geopolitical Trade Relations and Supply Chains

Ongoing tensions in Eastern Europe and the Middle East have raised freight rates—container rates to Europe rose ~45% in 2024—and increased component import costs for Jaguar Land Rover, squeezing margins; Tata Motors must manage potential tariffs between India, the UK and EU after UK-EU trade frictions, where tariffs could add 1–3% on auto parts. Strategic supply‑chain diversification, including nearshoring and multi‑sourcing, aims to cut disruption risk and inventory days (currently ~55 days) by 10–15%.

Defense Sector Procurement Policies

India’s Atmanirbhar Bharat push has increased defense procurement from domestic firms, with capital acquisition for defence rising 11% to INR 1.57 lakh crore in Budget 2024–25, boosting opportunities for Tata Motors’ commercial and defence vehicle divisions.

Tata Motors’ multi-decade military partnerships helped win contracts worth over INR 2,000 crore for logistics and armored vehicles in 2023–24, reinforcing its role in specialized defense supply chains.

Policy shifts favoring domestic manufacturing—offsetting up to 70% of procurement preference in recent tenders—create a regulatory moat that limits foreign competition in India’s defense vehicle market.

UK and EU Regulatory Alignment

UK-EU post-Brexit trade rules and regulatory alignment directly affect Tata Motors via Jaguar Land Rover; tariffs and rules of origin impact margins—JLR exported £12.1bn of vehicles from UK in 2023, with EU a key market.

EU carbon targets and ICE phase-out (EU aims for zero-emission new cars by 2035) accelerate JLR's shift to electric, influencing capex; JLR pledged £15bn electrification investment through 2030.

Political stability in UK/EU is vital for long-term investments and workforce planning at UK plants employing ~40,000 people; uncertainty raises risk premiums on projects.

- £12.1bn JLR UK exports 2023 to EU-important markets

- EU 2035 ICE ban drives electrification

- JLR £15bn electrification capex through 2030

- ~40,000 UK workforce—sensitive to policy/stability

Infrastructure Spending and Public Transport

- Rs 2.4 trillion national transport allocation (2025–26)

- Target: 10,000 H2 buses, 50,000 electric transit vehicles by 2026

- 100,000 km rural roads scheme expanding LCV demand

- Tata Motors ~40% domestic LCV market share (FY2024)

Tata Motors gains from Rs20kcr EV incentives, rising EV share; JLR faces £15bn electrification

Strong pro‑EV and localisation policies (FAME/PLI, ~Rs20,000cr incentives) lifted Tata Motors’ EV share to ~40% (passenger EVs) and cut EV unit costs ~8–12%; defence and transport budgets (INR1.57 lakh crore defence capex 2024–25; Rs2.4trn transport 2025–26) and rural road/urban transit schemes expand CV/LCV demand (~40% LCV share FY2024), while UK/EU trade and EU 2035 ICE ban drive JLR’s £15bn electrification capex and exposure to tariffs.

| Metric | Value |

|---|---|

| EV incentives | ~Rs20,000 crore |

| Tata EV share (passenger) | ~40% |

| EV unit cost reduction | 8–12% |

| Defence capex | INR1.57 lakh crore (2024–25) |

| Transport allocation | Rs2.4 trillion (2025–26) |

| JLR electrification capex | £15 billion through 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tata Motors across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, support executives and investors, and provide forward-looking insights for strategy, scenario planning, and funding confidence.

A concise, visually segmented Tata Motors PESTLE summary that’s easy to drop into presentations or strategy folders, streamlining meeting prep and cross-team alignment by highlighting key external risks and opportunities in simple, shareable language.

Economic factors

Interest Rate Environment and Financing

By end-2025, RBI policy rate at 6.5% raised retail EMIs and pushed average auto loan yields to ~12–13%, reducing passenger car affordability and slowing discretionary demand; commercial borrowers faced higher fleet financing costs as corporate lending rates rose ~150 bps year-on-year. High borrowing costs increased Tata Motors’ weighted average cost of capital, pressuring margins for EV and ICE investments. Tata Motors responded by expanding in-house financing via Tata Motors Finance, offering subsidized rates and 0–3 year tenure deals to sustain sales momentum across segments.

Raw Material Price Volatility

Raw material price volatility—notably lithium, cobalt, steel and aluminium—directly squeezes Tata Motors margins; lithium carbonate rose ~45% in 2023 before moderating in 2024, while steel plate prices in India averaged ~INR 62,000/ton in 2024, up ~10% YoY, increasing production costs. Global cobalt prices spiked intermittently (over 60% in 2021–23 cycles), prompting Tata to deploy hedging and long-term supply contracts to stabilize input costs. Transitioning to cheaper battery chemistries (LFP adoption and higher NMC efficiency) is crucial to offset raw material inflation and protect EV gross margins.

Currency Exchange Rate Fluctuations

As a global firm with major operations in the UK and exports worldwide, Tata Motors is exposed to volatility in GBP, USD and INR; a 10% depreciation of the INR vs GBP in 2024 would have materially reduced reported JLR sterling earnings when consolidated into INR. Exchange moves affect JLR reported revenue (JLR revenue £19.1bn in 2023) and raise costs for imported components for Indian production, squeezing margins. Management uses hedging, natural offsets and increased local sourcing—Tata reported sourcing ~60% locally in India in 2024—to mitigate currency devaluation effects on the consolidated balance sheet.

Consumer Purchasing Power and Inflation

Rising inflation in India (wholesale inflation around 5.9% and CPI ~6.4% in 2024) compresses household disposable income and corporate operating budgets, reducing near-term demand for passenger and commercial vehicles.

Tata Motors mitigates this via a broad portfolio from entry-level Tiago/Altroz to premium Jaguar Land Rover models, allowing shifts in focus across segments as affordability changes.

By tracking GDP growth (India ~7% in 2024) and industrial output, Tata adjusts production to prevent inventory pile-up or stockouts, as seen in Q3 2024 where JLR supply-demand realignments improved margins.

- Inflation: CPI ~6.4% (2024)

- GDP growth: ~7% (India, 2024)

- Product range: entry to luxury (Tiago to JLR)

- Operational response: production adjustments to manage inventory

Growth Trends in Emerging Markets

Economic expansion in Africa, Southeast Asia, and Latin America—projected regional GDP growth of ~3.5–5% in 2024–25 (IMF estimates)—boosts demand for rugged, cost-effective commercial vehicles, matching Tata Motors’ core strengths; exports rose 12% YoY in FY2024, highlighting traction in these markets.

Shifting sales toward high-growth economies can cut reliance on saturated Indian and European markets, where growth slowed to ~2%–3%, supporting portfolio diversification and higher-margin export opportunities.

- Regional GDP growth 2024–25: ~3.5–5% (IMF)

- Tata Motors exports: +12% YoY FY2024

- Domestic/Europe growth: ~2%–3%

- Strong fit: demand for rugged, low-cost commercial vehicles

Rising rates, raw‑material pain and FX risk dent margins; exports offer respite

Higher rates (RBI policy 6.5% end‑2025) raised auto loan yields (~12–13%) and borrowing costs; raw material inflation (steel ~INR62,000/t 2024; lithium +45% 2023) squeezed margins; FX exposure (JLR £19.1bn rev 2023; INR depreciation risk) and India CPI ~6.4%/GDP ~7% 2024 affect demand; exports +12% FY2024 support diversification.

| Metric | 2024/25 |

|---|---|

| RBI rate | 6.5% |

| Auto loan yield | ~12–13% |

| CPI | 6.4% |

| India GDP | ~7% |

| Steel | INR62,000/t |

| Exports | +12% FY2024 |

Same Document Delivered

Tata Motors PESTLE Analysis

The preview shown here is the exact Tata Motors PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Understand how political shifts, supply‑chain pressures, and accelerating EV tech are shaping Tata Motors’ strategic path—our concise PESTLE snapshot highlights risks and opportunities you can act on immediately. Purchase the full PESTLE analysis to access a detailed, ready‑to‑use report with data‑backed insights, scenario implications, and strategic recommendations tailored for investors and decision‑makers.

Political factors

Government Incentives for Green Mobility

The Indian government continued prioritizing EV adoption into late 2025, extending FAME and PLI schemes that drove a 28% YoY rise in EV registrations in FY2024–25 and allocated ~Rs 20,000 crore for incentives and charging infrastructure.

Tata Motors gained cost advantages from subsidies and PLI-linked localisation, lowering EV unit costs by an estimated 8–12% and supporting a 2025 EV market share near 40% in passenger EVs.

Maintaining strong ties with policymakers remains crucial to secure further support for nationwide charging networks and domestic battery manufacturing, where India targeted 50 GWh battery capacity by 2027.

Geopolitical Trade Relations and Supply Chains

Ongoing tensions in Eastern Europe and the Middle East have raised freight rates—container rates to Europe rose ~45% in 2024—and increased component import costs for Jaguar Land Rover, squeezing margins; Tata Motors must manage potential tariffs between India, the UK and EU after UK-EU trade frictions, where tariffs could add 1–3% on auto parts. Strategic supply‑chain diversification, including nearshoring and multi‑sourcing, aims to cut disruption risk and inventory days (currently ~55 days) by 10–15%.

Defense Sector Procurement Policies

India’s Atmanirbhar Bharat push has increased defense procurement from domestic firms, with capital acquisition for defence rising 11% to INR 1.57 lakh crore in Budget 2024–25, boosting opportunities for Tata Motors’ commercial and defence vehicle divisions.

Tata Motors’ multi-decade military partnerships helped win contracts worth over INR 2,000 crore for logistics and armored vehicles in 2023–24, reinforcing its role in specialized defense supply chains.

Policy shifts favoring domestic manufacturing—offsetting up to 70% of procurement preference in recent tenders—create a regulatory moat that limits foreign competition in India’s defense vehicle market.

UK and EU Regulatory Alignment

UK-EU post-Brexit trade rules and regulatory alignment directly affect Tata Motors via Jaguar Land Rover; tariffs and rules of origin impact margins—JLR exported £12.1bn of vehicles from UK in 2023, with EU a key market.

EU carbon targets and ICE phase-out (EU aims for zero-emission new cars by 2035) accelerate JLR's shift to electric, influencing capex; JLR pledged £15bn electrification investment through 2030.

Political stability in UK/EU is vital for long-term investments and workforce planning at UK plants employing ~40,000 people; uncertainty raises risk premiums on projects.

- £12.1bn JLR UK exports 2023 to EU-important markets

- EU 2035 ICE ban drives electrification

- JLR £15bn electrification capex through 2030

- ~40,000 UK workforce—sensitive to policy/stability

Infrastructure Spending and Public Transport

- Rs 2.4 trillion national transport allocation (2025–26)

- Target: 10,000 H2 buses, 50,000 electric transit vehicles by 2026

- 100,000 km rural roads scheme expanding LCV demand

- Tata Motors ~40% domestic LCV market share (FY2024)

Tata Motors gains from Rs20kcr EV incentives, rising EV share; JLR faces £15bn electrification

Strong pro‑EV and localisation policies (FAME/PLI, ~Rs20,000cr incentives) lifted Tata Motors’ EV share to ~40% (passenger EVs) and cut EV unit costs ~8–12%; defence and transport budgets (INR1.57 lakh crore defence capex 2024–25; Rs2.4trn transport 2025–26) and rural road/urban transit schemes expand CV/LCV demand (~40% LCV share FY2024), while UK/EU trade and EU 2035 ICE ban drive JLR’s £15bn electrification capex and exposure to tariffs.

| Metric | Value |

|---|---|

| EV incentives | ~Rs20,000 crore |

| Tata EV share (passenger) | ~40% |

| EV unit cost reduction | 8–12% |

| Defence capex | INR1.57 lakh crore (2024–25) |

| Transport allocation | Rs2.4 trillion (2025–26) |

| JLR electrification capex | £15 billion through 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect Tata Motors across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities, support executives and investors, and provide forward-looking insights for strategy, scenario planning, and funding confidence.

A concise, visually segmented Tata Motors PESTLE summary that’s easy to drop into presentations or strategy folders, streamlining meeting prep and cross-team alignment by highlighting key external risks and opportunities in simple, shareable language.

Economic factors

Interest Rate Environment and Financing

By end-2025, RBI policy rate at 6.5% raised retail EMIs and pushed average auto loan yields to ~12–13%, reducing passenger car affordability and slowing discretionary demand; commercial borrowers faced higher fleet financing costs as corporate lending rates rose ~150 bps year-on-year. High borrowing costs increased Tata Motors’ weighted average cost of capital, pressuring margins for EV and ICE investments. Tata Motors responded by expanding in-house financing via Tata Motors Finance, offering subsidized rates and 0–3 year tenure deals to sustain sales momentum across segments.

Raw Material Price Volatility

Raw material price volatility—notably lithium, cobalt, steel and aluminium—directly squeezes Tata Motors margins; lithium carbonate rose ~45% in 2023 before moderating in 2024, while steel plate prices in India averaged ~INR 62,000/ton in 2024, up ~10% YoY, increasing production costs. Global cobalt prices spiked intermittently (over 60% in 2021–23 cycles), prompting Tata to deploy hedging and long-term supply contracts to stabilize input costs. Transitioning to cheaper battery chemistries (LFP adoption and higher NMC efficiency) is crucial to offset raw material inflation and protect EV gross margins.

Currency Exchange Rate Fluctuations

As a global firm with major operations in the UK and exports worldwide, Tata Motors is exposed to volatility in GBP, USD and INR; a 10% depreciation of the INR vs GBP in 2024 would have materially reduced reported JLR sterling earnings when consolidated into INR. Exchange moves affect JLR reported revenue (JLR revenue £19.1bn in 2023) and raise costs for imported components for Indian production, squeezing margins. Management uses hedging, natural offsets and increased local sourcing—Tata reported sourcing ~60% locally in India in 2024—to mitigate currency devaluation effects on the consolidated balance sheet.

Consumer Purchasing Power and Inflation

Rising inflation in India (wholesale inflation around 5.9% and CPI ~6.4% in 2024) compresses household disposable income and corporate operating budgets, reducing near-term demand for passenger and commercial vehicles.

Tata Motors mitigates this via a broad portfolio from entry-level Tiago/Altroz to premium Jaguar Land Rover models, allowing shifts in focus across segments as affordability changes.

By tracking GDP growth (India ~7% in 2024) and industrial output, Tata adjusts production to prevent inventory pile-up or stockouts, as seen in Q3 2024 where JLR supply-demand realignments improved margins.

- Inflation: CPI ~6.4% (2024)

- GDP growth: ~7% (India, 2024)

- Product range: entry to luxury (Tiago to JLR)

- Operational response: production adjustments to manage inventory

Growth Trends in Emerging Markets

Economic expansion in Africa, Southeast Asia, and Latin America—projected regional GDP growth of ~3.5–5% in 2024–25 (IMF estimates)—boosts demand for rugged, cost-effective commercial vehicles, matching Tata Motors’ core strengths; exports rose 12% YoY in FY2024, highlighting traction in these markets.

Shifting sales toward high-growth economies can cut reliance on saturated Indian and European markets, where growth slowed to ~2%–3%, supporting portfolio diversification and higher-margin export opportunities.

- Regional GDP growth 2024–25: ~3.5–5% (IMF)

- Tata Motors exports: +12% YoY FY2024

- Domestic/Europe growth: ~2%–3%

- Strong fit: demand for rugged, low-cost commercial vehicles

Rising rates, raw‑material pain and FX risk dent margins; exports offer respite

Higher rates (RBI policy 6.5% end‑2025) raised auto loan yields (~12–13%) and borrowing costs; raw material inflation (steel ~INR62,000/t 2024; lithium +45% 2023) squeezed margins; FX exposure (JLR £19.1bn rev 2023; INR depreciation risk) and India CPI ~6.4%/GDP ~7% 2024 affect demand; exports +12% FY2024 support diversification.

| Metric | 2024/25 |

|---|---|

| RBI rate | 6.5% |

| Auto loan yield | ~12–13% |

| CPI | 6.4% |

| India GDP | ~7% |

| Steel | INR62,000/t |

| Exports | +12% FY2024 |

Same Document Delivered

Tata Motors PESTLE Analysis

The preview shown here is the exact Tata Motors PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.