Taiwan Cooperative Financial PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our PESTLE Analysis of Taiwan Cooperative Financial—uncover how political shifts, economic cycles, social trends, technological advances, legal updates, and environmental factors will shape its future performance; buy the full report to get actionable insights, ready-to-use charts, and strategic recommendations for investors and planners.

Political factors

Cross-Strait Geopolitical Stability

The ongoing Taiwan–Mainland China relationship remains a primary risk for financial institutions through 2025; cross-strait tensions raised Taiwan’s implied sovereign CDS to about 120–140 bps in 2024, increasing market volatility and trade-finance disruption risk for Taiwan Cooperative Financial Holding. The bank must stress-test credit and FX portfolios under scenarios that mirror 2019–2024 stress, ensuring CET1 ratios stay above regulatory buffers (target >10.5%) and maintaining liquid assets covering at least 6–9 months of wholesale funding.

Government Ownership and Policy Alignment

As a state-affiliated financial holding company, Taiwan Cooperative Financial is closely guided by governmental administrative goals, with roughly 28% of its loan portfolio in 2024 directed to government-priority sectors like SMEs and urban renewal. The bank aligns strategies with national initiatives—supporting over NT$45 billion in SME credit lines and participating in NT$12.3 billion worth of urban renewal projects in 2024. This public linkage offers stability through policy backing and implicit sovereign support, but management must balance these objectives with delivering competitive ROE (5.8% in FY2024) to shareholders.

International Trade Policy Impacts

Changes in global trade agreements and Taiwan’s deeper engagement in regional blocs like CPTPP and RCEP-linked dialogues alter corporate lending dynamics; export sectors (electronics, machinery)—which accounted for 69% of Taiwan’s 2024 merchandise exports—face tariff shifts and supply‑chain realignments that require revised credit models. Rising exports to ASEAN under the New Southbound Policy (ASEAN share ~28% of 2024 exports) pushes the bank to adjust country risk limits and support cross‑border financing for clients expanding in Southeast Asia.

Financial Sector Liberalization

- Reforms through 2025 increase foreign competition and consolidation pressure

- Target ROE uplift from 6.2% toward 8–9%; cost-to-income improvement needed

- Maintain ~12% regional deposit share while modernizing operations

Geopolitical Diversification Strategy

Political mandates to reduce market concentration have pushed Taiwan Cooperative Financial to expand into Southeast Asia and North America, where it opened 12 new branches and 3 subsidiaries between 2022–2025, lowering Taiwan exposure from 88% to 72% of total assets by end-2025.

This geographic diversification reduces vulnerability to localized instability and aligns with government goals to cut domestic concentration risk to under 70% by 2027.

- 12 new branches, 3 subsidiaries (2022–2025)

- Domestic asset exposure down from 88% to 72% (end-2025)

- Target: under 70% domestic concentration by 2027

Stress-tested bank eyes efficiency, liquidity as CDS spikes to 120–140bps

Cross-strait tensions raised implied sovereign CDS to ~120–140 bps in 2024, prompting stress tests to keep CET1 >10.5% and liquidity for 6–9 months; 2024 ROE 5.8% vs industry 8–9% pressures efficiency gains (cost-to-income target <45%). Policy-driven expansion cut domestic asset share from 88% to 72% by end-2025; goal <70% by 2027.

| Metric | 2024/2025 |

|---|---|

| Implied CDS | 120–140 bps (2024) |

| CET1 target | >10.5% |

| ROE | 5.8% (2024) |

| Cost-to-income | Goal <45% |

| Domestic asset share | 72% (end-2025) |

What is included in the product

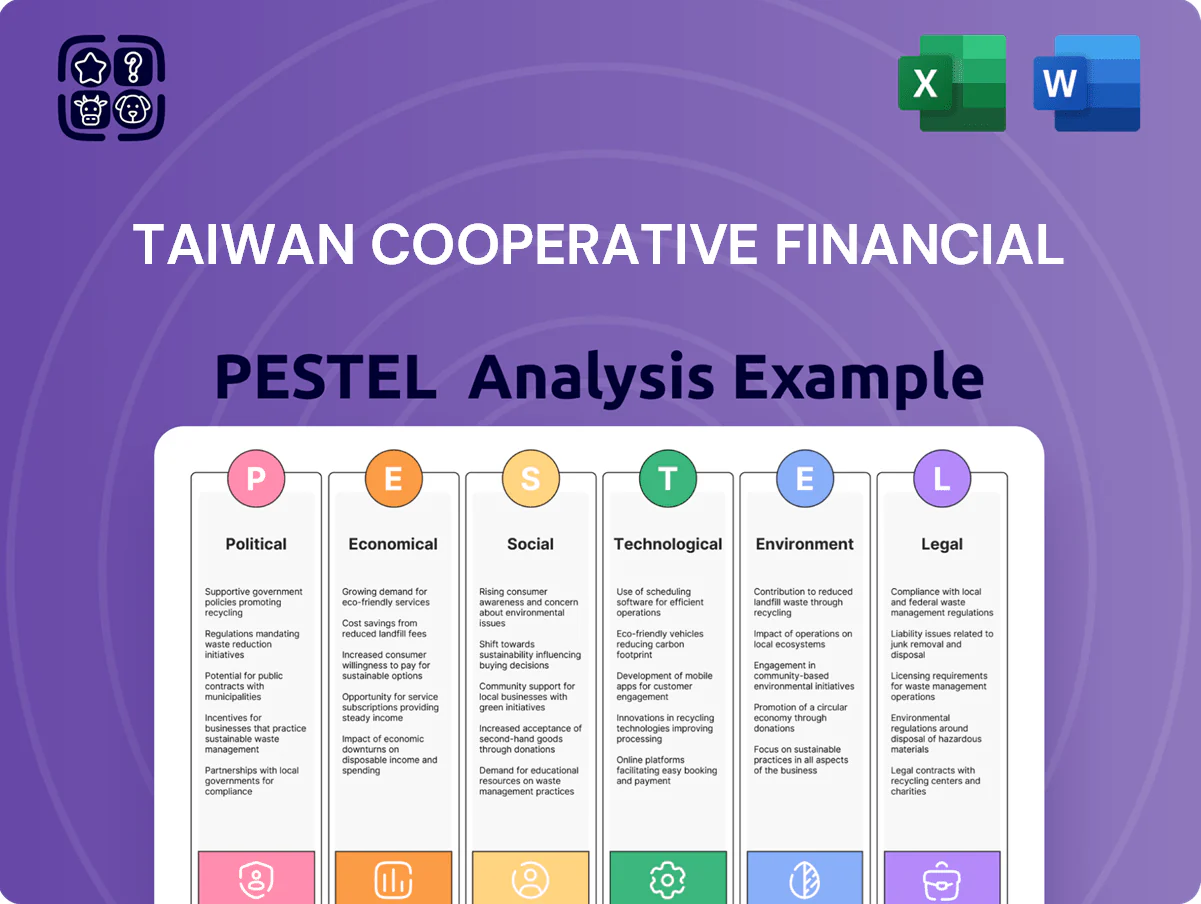

Explores how macro-environmental forces uniquely affect Taiwan Cooperative Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications to inform strategy, risk mitigation, and opportunity capture for executives, investors, and advisors.

A condensed PESTLE snapshot for Taiwan Cooperative Financial that highlights key political, economic, social, technological, legal, and environmental drivers—ideal for quick reference in meetings or presentations.

Economic factors

Central Bank Monetary Policy

The Central Bank of the Republic of China’s policy rates set Taiwan Cooperative Financial’s net interest margin trajectory; the policy rate fell from 2.5% in mid-2024 to 1.75% by December 2025, compressing margins and pressuring NIMs that averaged ~1.6% in 2024.

Export-Driven Economic Performance

Taiwan's GDP growth remains export-driven, with semiconductors/electronics accounting for about 40% of exports and contributing to GDP growth of 2.8% in 2024, directly affecting corporate loan quality at Taiwan Cooperative Financial as clients' cashflows hinge on chip demand.

Global chip softness in 2023–24 cut industry capex by an estimated 15–20%, causing variable financing needs across the bank's corporate portfolio and higher credit monitoring intensity.

The bank tracks indicators such as global semiconductor equipment spending (down ~12% YoY in 2024), Taiwan export orders, and US/China demand to preempt domestic industrial shifts and adjust provisioning and lending strategies.

Inflationary Pressures and Operating Costs

Persistent inflation through 2024–2025—CPI averaging about 2.8–3.2% in Taiwan in 2024 and core inflation near 2.6%—has eroded retail customers’ purchasing power and raised internal cost bases for Taiwan Cooperative Financial.

Higher labor costs (minimum wage rises to NT$26,400 in 2024) and utility inflation (+6–8% in energy costs 2024) push the bank to tighten cost controls and accelerate digital automation to protect margins.

Inflation also increases the present value of the insurance subsidiary’s long-term liabilities and reduces demand for fixed-income products as real yields remain compressed versus nominal yields.

Currency Exchange Rate Volatility

- NTD vs USD: ~4.1% change (2023–2024)

- Hedging coverage: >65% of major exposures (2024)

- Monthly FX volume: ~NT$120 billion (2024)

Real Estate Market Dynamics

As a major mortgage lender, Taiwan Cooperative Financial is highly exposed to property price trends and government cooling measures; Taiwan housing prices fell about 2.1% year-on-year in 2025 Q3, pressuring new loan demand.

Shifts in affordability and potential property tax reforms affect mortgage origination and collateral values; a 2024 policy tightening reduced mortgage approvals by ~6% nationwide.

The bank keeps conservative LTVs—typically under 70%—to protect capital against market corrections and rising NPL risk.

- Exposure to 2025 Q3 house price drop −2.1% YoY

- 2024 mortgage approvals down ~6% after cooling measures

- Conservative LTVs ~70% to limit downside

Taiwan: Easing Cuts Rates to 1.75% as Chips Drive Growth, NIMs & Housing Slide

Monetary easing cut policy rate from 2.5% (mid‑2024) to 1.75% (Dec‑2025), compressing NIMs (~1.6% in 2024); GDP growth 2.8% (2024) driven by semiconductors (~40% exports) with capex down ~15–20%; CPI ~2.8–3.2% (2024) and minimum wage NT$26,400 (2024) raise costs; NTD weakened ~4.1% vs USD (2023–24); mortgages hit by −2.1% house prices (2025 Q3), LTVs ≤70%.

| Metric | Value |

|---|---|

| Policy rate | 1.75% (Dec‑2025) |

| NIM | ~1.6% (2024) |

| GDP growth | 2.8% (2024) |

| Semiconductor export share | ~40% |

| CPI | 2.8–3.2% (2024) |

| NTD vs USD | −4.1% (2023–24) |

| House prices | −2.1% YoY (2025 Q3) |

Preview the Actual Deliverable

Taiwan Cooperative Financial PESTLE Analysis

The preview shown here is the exact Taiwan Cooperative Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professional, and ready to use.

The layout, content, and structure visible in this preview are identical to the final file you’ll download immediately after payment—no placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic edge with our PESTLE Analysis of Taiwan Cooperative Financial—uncover how political shifts, economic cycles, social trends, technological advances, legal updates, and environmental factors will shape its future performance; buy the full report to get actionable insights, ready-to-use charts, and strategic recommendations for investors and planners.

Political factors

Cross-Strait Geopolitical Stability

The ongoing Taiwan–Mainland China relationship remains a primary risk for financial institutions through 2025; cross-strait tensions raised Taiwan’s implied sovereign CDS to about 120–140 bps in 2024, increasing market volatility and trade-finance disruption risk for Taiwan Cooperative Financial Holding. The bank must stress-test credit and FX portfolios under scenarios that mirror 2019–2024 stress, ensuring CET1 ratios stay above regulatory buffers (target >10.5%) and maintaining liquid assets covering at least 6–9 months of wholesale funding.

Government Ownership and Policy Alignment

As a state-affiliated financial holding company, Taiwan Cooperative Financial is closely guided by governmental administrative goals, with roughly 28% of its loan portfolio in 2024 directed to government-priority sectors like SMEs and urban renewal. The bank aligns strategies with national initiatives—supporting over NT$45 billion in SME credit lines and participating in NT$12.3 billion worth of urban renewal projects in 2024. This public linkage offers stability through policy backing and implicit sovereign support, but management must balance these objectives with delivering competitive ROE (5.8% in FY2024) to shareholders.

International Trade Policy Impacts

Changes in global trade agreements and Taiwan’s deeper engagement in regional blocs like CPTPP and RCEP-linked dialogues alter corporate lending dynamics; export sectors (electronics, machinery)—which accounted for 69% of Taiwan’s 2024 merchandise exports—face tariff shifts and supply‑chain realignments that require revised credit models. Rising exports to ASEAN under the New Southbound Policy (ASEAN share ~28% of 2024 exports) pushes the bank to adjust country risk limits and support cross‑border financing for clients expanding in Southeast Asia.

Financial Sector Liberalization

- Reforms through 2025 increase foreign competition and consolidation pressure

- Target ROE uplift from 6.2% toward 8–9%; cost-to-income improvement needed

- Maintain ~12% regional deposit share while modernizing operations

Geopolitical Diversification Strategy

Political mandates to reduce market concentration have pushed Taiwan Cooperative Financial to expand into Southeast Asia and North America, where it opened 12 new branches and 3 subsidiaries between 2022–2025, lowering Taiwan exposure from 88% to 72% of total assets by end-2025.

This geographic diversification reduces vulnerability to localized instability and aligns with government goals to cut domestic concentration risk to under 70% by 2027.

- 12 new branches, 3 subsidiaries (2022–2025)

- Domestic asset exposure down from 88% to 72% (end-2025)

- Target: under 70% domestic concentration by 2027

Stress-tested bank eyes efficiency, liquidity as CDS spikes to 120–140bps

Cross-strait tensions raised implied sovereign CDS to ~120–140 bps in 2024, prompting stress tests to keep CET1 >10.5% and liquidity for 6–9 months; 2024 ROE 5.8% vs industry 8–9% pressures efficiency gains (cost-to-income target <45%). Policy-driven expansion cut domestic asset share from 88% to 72% by end-2025; goal <70% by 2027.

| Metric | 2024/2025 |

|---|---|

| Implied CDS | 120–140 bps (2024) |

| CET1 target | >10.5% |

| ROE | 5.8% (2024) |

| Cost-to-income | Goal <45% |

| Domestic asset share | 72% (end-2025) |

What is included in the product

Explores how macro-environmental forces uniquely affect Taiwan Cooperative Financial across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications to inform strategy, risk mitigation, and opportunity capture for executives, investors, and advisors.

A condensed PESTLE snapshot for Taiwan Cooperative Financial that highlights key political, economic, social, technological, legal, and environmental drivers—ideal for quick reference in meetings or presentations.

Economic factors

Central Bank Monetary Policy

The Central Bank of the Republic of China’s policy rates set Taiwan Cooperative Financial’s net interest margin trajectory; the policy rate fell from 2.5% in mid-2024 to 1.75% by December 2025, compressing margins and pressuring NIMs that averaged ~1.6% in 2024.

Export-Driven Economic Performance

Taiwan's GDP growth remains export-driven, with semiconductors/electronics accounting for about 40% of exports and contributing to GDP growth of 2.8% in 2024, directly affecting corporate loan quality at Taiwan Cooperative Financial as clients' cashflows hinge on chip demand.

Global chip softness in 2023–24 cut industry capex by an estimated 15–20%, causing variable financing needs across the bank's corporate portfolio and higher credit monitoring intensity.

The bank tracks indicators such as global semiconductor equipment spending (down ~12% YoY in 2024), Taiwan export orders, and US/China demand to preempt domestic industrial shifts and adjust provisioning and lending strategies.

Inflationary Pressures and Operating Costs

Persistent inflation through 2024–2025—CPI averaging about 2.8–3.2% in Taiwan in 2024 and core inflation near 2.6%—has eroded retail customers’ purchasing power and raised internal cost bases for Taiwan Cooperative Financial.

Higher labor costs (minimum wage rises to NT$26,400 in 2024) and utility inflation (+6–8% in energy costs 2024) push the bank to tighten cost controls and accelerate digital automation to protect margins.

Inflation also increases the present value of the insurance subsidiary’s long-term liabilities and reduces demand for fixed-income products as real yields remain compressed versus nominal yields.

Currency Exchange Rate Volatility

- NTD vs USD: ~4.1% change (2023–2024)

- Hedging coverage: >65% of major exposures (2024)

- Monthly FX volume: ~NT$120 billion (2024)

Real Estate Market Dynamics

As a major mortgage lender, Taiwan Cooperative Financial is highly exposed to property price trends and government cooling measures; Taiwan housing prices fell about 2.1% year-on-year in 2025 Q3, pressuring new loan demand.

Shifts in affordability and potential property tax reforms affect mortgage origination and collateral values; a 2024 policy tightening reduced mortgage approvals by ~6% nationwide.

The bank keeps conservative LTVs—typically under 70%—to protect capital against market corrections and rising NPL risk.

- Exposure to 2025 Q3 house price drop −2.1% YoY

- 2024 mortgage approvals down ~6% after cooling measures

- Conservative LTVs ~70% to limit downside

Taiwan: Easing Cuts Rates to 1.75% as Chips Drive Growth, NIMs & Housing Slide

Monetary easing cut policy rate from 2.5% (mid‑2024) to 1.75% (Dec‑2025), compressing NIMs (~1.6% in 2024); GDP growth 2.8% (2024) driven by semiconductors (~40% exports) with capex down ~15–20%; CPI ~2.8–3.2% (2024) and minimum wage NT$26,400 (2024) raise costs; NTD weakened ~4.1% vs USD (2023–24); mortgages hit by −2.1% house prices (2025 Q3), LTVs ≤70%.

| Metric | Value |

|---|---|

| Policy rate | 1.75% (Dec‑2025) |

| NIM | ~1.6% (2024) |

| GDP growth | 2.8% (2024) |

| Semiconductor export share | ~40% |

| CPI | 2.8–3.2% (2024) |

| NTD vs USD | −4.1% (2023–24) |

| House prices | −2.1% YoY (2025 Q3) |

Preview the Actual Deliverable

Taiwan Cooperative Financial PESTLE Analysis

The preview shown here is the exact Taiwan Cooperative Financial PESTLE Analysis document you’ll receive after purchase—fully formatted, professional, and ready to use.

The layout, content, and structure visible in this preview are identical to the final file you’ll download immediately after payment—no placeholders, no surprises.