Transcontinental Boston Consulting Group Matrix

See the Bigger Picture

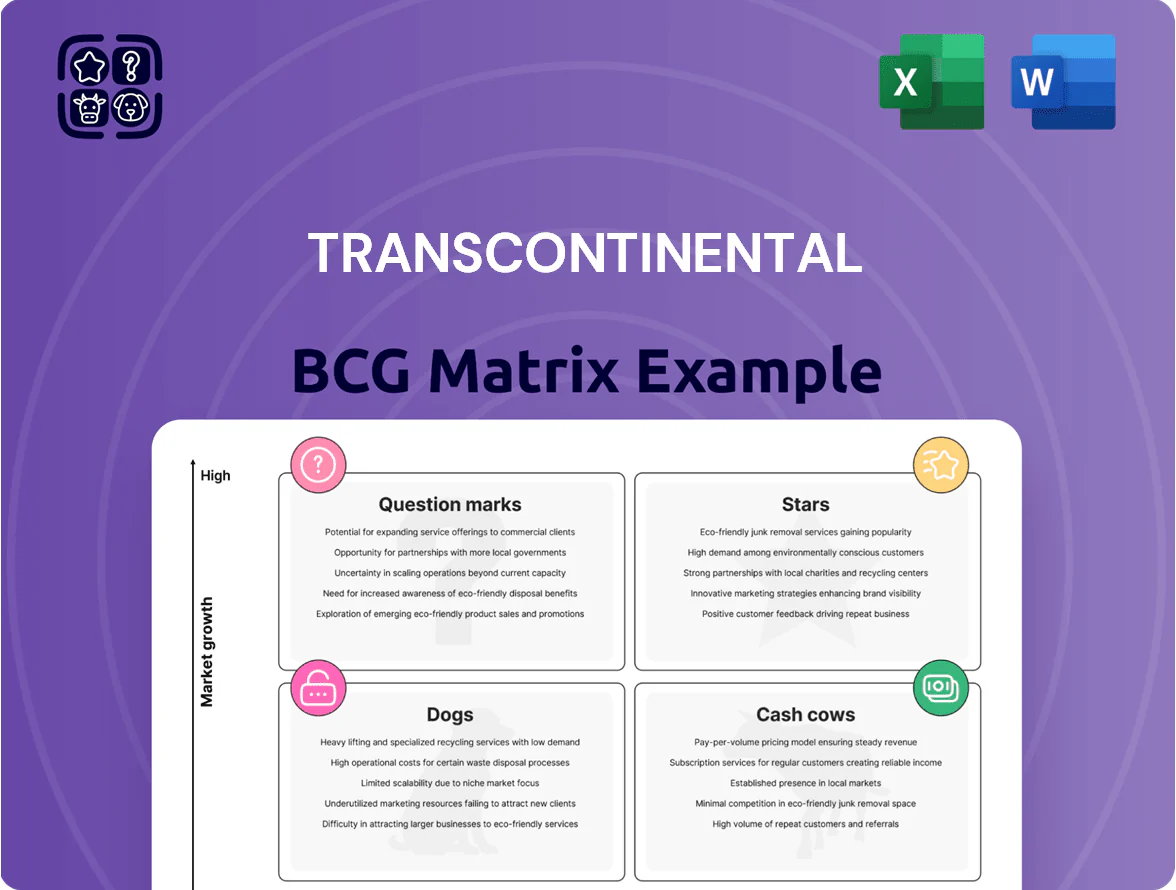

Transcontinental’s BCG Matrix snapshot shows a dynamic mix of mature cash generators and emerging contenders—spotting which divisions fuel free cash flow and which need strategic reinvestment or divestment. This concise preview highlights key quadrant trends but only scratches the surface; the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and tactical moves tailored to Transcontinental’s market realities. Purchase the complete report to get a ready-to-use Word analysis plus an Excel summary that guides capital allocation, portfolio pruning, and growth prioritization.

Stars

Sustainable Flexible Packaging

As of late 2025, TC Transcontinental has positioned its recyclable and compostable flexible packaging as a Stars segment in North America, driving 28% year-on-year revenue growth and capturing ~12% market share among mono-material film buyers.

After an US$80 million investment in a mono-material polyethylene film line announced 2024–2025, the unit increased EBITDA margin to 18% in 2025 while winning contracts with 35 national brands shifting to circular-economy mandates.

The segment needs high reinvestment—capex of US$40–60 million planned 2026–2027—to retain tech leadership, and it remains TC Transcontinental’s primary engine for projected organic growth of ~15% CAGR to 2028.

Book Printing Services

In 2025 Transcontinental’s Book Printing Services became a Star, posting >4% revenue growth quarter-over-quarter and lifting annual printing revenue to roughly CAD 420M, while many print segments fell double-digits.

As Canada’s largest printer, Transcontinental used specialized North American facilities to capture a 22% share of Canadian book print volume and a rising US demand for local sourcing.

The unit’s dominant market position and renewed demand for printed educational and trade books drove strong margins—EBIT margin around 11% in 2025—keeping it in the Star quadrant.

In-Store Marketing (ISM) and Point-of-Purchase

Following 2025 acquisitions of Middleton Group, Mirazed, and Intergraphics, TC Transcontinental scaled in-store marketing (ISM) to serve 45% more retail locations, boosting annual ISM revenue to ~CAD 220M in 2025 and growing at ~18% CAGR—classifying it as a Star in the BCG matrix.

The ISM segment targets a high-growth retail analytics and physical branding market projected to reach USD 38B in North America by 2027; TC is investing CAD 60M in 2025–26 to integrate platforms and capture share across Canada and the US.

Digital Educational Publishing

The educational publishing arm is becoming a Star as it shifts from print to digital learning platforms and immersive content, targeting the global digital education market growing ~12% CAGR (2021–2026) and projected to reach US$404B by 2025.

TC Transcontinental leverages leadership in French-language school materials to win digital-first contracts in Quebec and Canada, citing education segment revenue stability and mid-single-digit contribution to company sales in 2024.

High barriers to entry—localized curriculum expertise, content licensing, and platform integration—plus rising hybrid learning demand position this unit for high revenue growth and margin expansion.

- Global digital education ~12% CAGR; market ~US$404B by 2025

- TC Transcontinental: French-language leadership, digital pivot 2023–25

- High entry barriers: curriculum, licensing, integration

- Target markets: Quebec and Canada; strong hybrid demand

Specialty Solutions Packaging

Specialty Solutions Packaging targets high-barrier films for cheese, dairy, and proteins, with volume up 6.8% in fiscal 2025 and North America share ~42%, driven by demand for fresh, long-shelf-life foods.

It requires ongoing R&D spending—about CAD 18m in 2025—to meet new EU/Canada environmental regs, but strong margins (EBITDA margin ~19% in 2025) and market leadership make it a Star in Transcontinental’s industrial portfolio.

- Volume growth fiscal 2025: +6.8%

- North America market share: ~42%

- R&D spend 2025: CAD 18m

- EBITDA margin 2025: ~19%

High-growth packaging & ISM: strong margins, hefty capex and R&D fueling expansion

Stars: Flexible packaging (28% YoY, ~12% share; EBITDA 18%; US$80M capex 2024–25; US$40–60M planned 2026–27), Book printing (annual CAD 420M; EBIT ~11%; 22% Canada share), In-store marketing (CAD 220M; +18% CAGR; CAD 60M integration spend), Specialty packaging (vol +6.8% 2025; NA share ~42%; R&D CAD 18M; EBITDA ~19%).

| Unit | 2025 Rev/Key | Margin | Capex/R&D |

|---|---|---|---|

| Flexible packaging | 28% YoY; ~12% share | EBITDA 18% | US$80M(24–25); US$40–60M(26–27) |

| Book printing | CAD 420M; 22% Canada | EBIT ~11% | — |

| ISM | CAD 220M; +18% CAGR | — | CAD 60M(25–26) |

| Specialty packaging | vol +6.8%; NA ~42% | EBITDA ~19% | R&D CAD 18M(2025) |

What is included in the product

Comprehensive BCG Matrix review of Transcontinental’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Transcontinental BCG Matrix placing each business unit in a quadrant for fast executive decisions.

Cash Cows

Retail Flyer Printing and Distribution

Despite a global print decline, TC Transcontinental controls ~70% of Canadian flyer distribution via its raddar digital-to-print platform, generating roughly CAD 220–240 million EBITDA from print/distribution in 2024, with margins near 18%—steady cash flows from a mature network needing minimal new capital.

These predictable cash flows fund corporate debt service—TC reported CAD 1.2 billion net debt at Dec 31, 2024—and bankroll aggressive moves into sustainable packaging, financing 2025 capex and recent acquisitions without equity raises.

Newspaper and Magazine Printing

As Canada’s largest printer, Transcontinental holds multi‑year, high‑volume contracts—often 10+ years—with publishers like The Globe and Mail, securing steady revenue streams of roughly CAD 350–420 million annually from print in 2024.

The print market is mature and declining ~5–7% annual volume, but scale drives 12–16% operating margins, classifying this segment as a Cash Cow.

Cash flows fund dividends and finance the 2025 CSR program, budgeted at CAD 15 million.

Premedia and Creative Services

Transcontinental’s Premedia and Creative Services deliver recurring, workflow-integrated support to major retailers and brands, generating stable EBITDA margins around 18–22% in 2024 and enabling predictable cash flow.

Operating in a low-growth segment with CAPEX under 2% of revenue and >85% client retention, it functions as a cash cow funding Transcontinental’s digital investments—about CAD 40–60m directed to transformation initiatives in 2024.

Traditional French-Language Textbook Publishing

Traditional French-language textbook publishing in Quebec remains a market leader for Transcontinental, delivering stable cash flow with gross margins often above 40% thanks to specialized curriculum content and long institutional contracts; the K-12 adoption cycle averages 4–6 years, keeping promotional spend low and renewal rates high (estimated renewal >70%).

- High margins: ~40%+ gross

- Renewal rate: >70%

- Adoption cycle: 4–6 years

- Low promo costs: <5% of revenue

- Reliable cash: majority from institutional contracts

Standard Flexible Plastic Films

Standard Flexible Plastic Films stays a cash cow for Transcontinental in late 2025, holding ~45% market share in North American food & beverage flexible packaging and delivering ~18% EBITDA margin on ~CAD 420m annual revenue.

With largely fully depreciated assets and optimized lines, it yields strong free cash flow used to fund the green transition; management earmarked CAD 80m in 2025 capex reallocation to sustainable film R&D and conversion.

Production growth is flat (~1% CAGR), so the focus is milking margins while reducing legacy footprint and meeting 2028 sustainability targets.

- Market share ~45%

- Revenue ~CAD 420m (2025)

- EBITDA margin ~18%

- CAD 80m reallocated to sustainable R&D (2025)

- Growth ~1% CAGR

Transcontinental’s cash cows fund debt and digital bets—steady EBITDA, strong margins

Transcontinental’s cash cows—print/distribution, premia/creative, K‑12 textbooks, and flexible films—generated steady EBITDA (print CAD 220–240m; films CAD 75–80m; premia ~CAD 40–55m; textbooks high-margin) with overall margins 12–22% in 2024–25, funding CAD 40–80m digital/sustainability investments and servicing CAD 1.2bn net debt (Dec 31, 2024).

| Segment | Rev (CAD) | EBITDA (CAD) | Margin | Notes |

|---|---|---|---|---|

| Print/Distribution | ~1,900m* | 220–240m | ~18% | 70% flyer share, long contracts |

| Flexible Films | ~420m | 75–80m | ~18% | ~45% NA share |

| Premedia/Creative | ~220m | 40–55m | 18–22% | ~85% retention |

| Textbooks (QC) | ~120m | ~48m | ~40%+ | 4–6yr cycle, >70% renewals |

What You See Is What You Get

Transcontinental BCG Matrix

The file you're previewing is the exact Transcontinental BCG Matrix report you'll receive after purchase—no watermarks, placeholders, or demo content. Fully formatted and analysis-ready, it’s crafted for strategic decision-making and immediate use in presentations, planning, or client deliverables. Upon purchase you’ll get the same editable, print-ready document delivered directly to your inbox—no surprises, no further edits required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Transcontinental’s BCG Matrix snapshot shows a dynamic mix of mature cash generators and emerging contenders—spotting which divisions fuel free cash flow and which need strategic reinvestment or divestment. This concise preview highlights key quadrant trends but only scratches the surface; the full BCG Matrix delivers quadrant-by-quadrant placements, data-driven recommendations, and tactical moves tailored to Transcontinental’s market realities. Purchase the complete report to get a ready-to-use Word analysis plus an Excel summary that guides capital allocation, portfolio pruning, and growth prioritization.

Stars

Sustainable Flexible Packaging

As of late 2025, TC Transcontinental has positioned its recyclable and compostable flexible packaging as a Stars segment in North America, driving 28% year-on-year revenue growth and capturing ~12% market share among mono-material film buyers.

After an US$80 million investment in a mono-material polyethylene film line announced 2024–2025, the unit increased EBITDA margin to 18% in 2025 while winning contracts with 35 national brands shifting to circular-economy mandates.

The segment needs high reinvestment—capex of US$40–60 million planned 2026–2027—to retain tech leadership, and it remains TC Transcontinental’s primary engine for projected organic growth of ~15% CAGR to 2028.

Book Printing Services

In 2025 Transcontinental’s Book Printing Services became a Star, posting >4% revenue growth quarter-over-quarter and lifting annual printing revenue to roughly CAD 420M, while many print segments fell double-digits.

As Canada’s largest printer, Transcontinental used specialized North American facilities to capture a 22% share of Canadian book print volume and a rising US demand for local sourcing.

The unit’s dominant market position and renewed demand for printed educational and trade books drove strong margins—EBIT margin around 11% in 2025—keeping it in the Star quadrant.

In-Store Marketing (ISM) and Point-of-Purchase

Following 2025 acquisitions of Middleton Group, Mirazed, and Intergraphics, TC Transcontinental scaled in-store marketing (ISM) to serve 45% more retail locations, boosting annual ISM revenue to ~CAD 220M in 2025 and growing at ~18% CAGR—classifying it as a Star in the BCG matrix.

The ISM segment targets a high-growth retail analytics and physical branding market projected to reach USD 38B in North America by 2027; TC is investing CAD 60M in 2025–26 to integrate platforms and capture share across Canada and the US.

Digital Educational Publishing

The educational publishing arm is becoming a Star as it shifts from print to digital learning platforms and immersive content, targeting the global digital education market growing ~12% CAGR (2021–2026) and projected to reach US$404B by 2025.

TC Transcontinental leverages leadership in French-language school materials to win digital-first contracts in Quebec and Canada, citing education segment revenue stability and mid-single-digit contribution to company sales in 2024.

High barriers to entry—localized curriculum expertise, content licensing, and platform integration—plus rising hybrid learning demand position this unit for high revenue growth and margin expansion.

- Global digital education ~12% CAGR; market ~US$404B by 2025

- TC Transcontinental: French-language leadership, digital pivot 2023–25

- High entry barriers: curriculum, licensing, integration

- Target markets: Quebec and Canada; strong hybrid demand

Specialty Solutions Packaging

Specialty Solutions Packaging targets high-barrier films for cheese, dairy, and proteins, with volume up 6.8% in fiscal 2025 and North America share ~42%, driven by demand for fresh, long-shelf-life foods.

It requires ongoing R&D spending—about CAD 18m in 2025—to meet new EU/Canada environmental regs, but strong margins (EBITDA margin ~19% in 2025) and market leadership make it a Star in Transcontinental’s industrial portfolio.

- Volume growth fiscal 2025: +6.8%

- North America market share: ~42%

- R&D spend 2025: CAD 18m

- EBITDA margin 2025: ~19%

High-growth packaging & ISM: strong margins, hefty capex and R&D fueling expansion

Stars: Flexible packaging (28% YoY, ~12% share; EBITDA 18%; US$80M capex 2024–25; US$40–60M planned 2026–27), Book printing (annual CAD 420M; EBIT ~11%; 22% Canada share), In-store marketing (CAD 220M; +18% CAGR; CAD 60M integration spend), Specialty packaging (vol +6.8% 2025; NA share ~42%; R&D CAD 18M; EBITDA ~19%).

| Unit | 2025 Rev/Key | Margin | Capex/R&D |

|---|---|---|---|

| Flexible packaging | 28% YoY; ~12% share | EBITDA 18% | US$80M(24–25); US$40–60M(26–27) |

| Book printing | CAD 420M; 22% Canada | EBIT ~11% | — |

| ISM | CAD 220M; +18% CAGR | — | CAD 60M(25–26) |

| Specialty packaging | vol +6.8%; NA ~42% | EBITDA ~19% | R&D CAD 18M(2025) |

What is included in the product

Comprehensive BCG Matrix review of Transcontinental’s units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Transcontinental BCG Matrix placing each business unit in a quadrant for fast executive decisions.

Cash Cows

Retail Flyer Printing and Distribution

Despite a global print decline, TC Transcontinental controls ~70% of Canadian flyer distribution via its raddar digital-to-print platform, generating roughly CAD 220–240 million EBITDA from print/distribution in 2024, with margins near 18%—steady cash flows from a mature network needing minimal new capital.

These predictable cash flows fund corporate debt service—TC reported CAD 1.2 billion net debt at Dec 31, 2024—and bankroll aggressive moves into sustainable packaging, financing 2025 capex and recent acquisitions without equity raises.

Newspaper and Magazine Printing

As Canada’s largest printer, Transcontinental holds multi‑year, high‑volume contracts—often 10+ years—with publishers like The Globe and Mail, securing steady revenue streams of roughly CAD 350–420 million annually from print in 2024.

The print market is mature and declining ~5–7% annual volume, but scale drives 12–16% operating margins, classifying this segment as a Cash Cow.

Cash flows fund dividends and finance the 2025 CSR program, budgeted at CAD 15 million.

Premedia and Creative Services

Transcontinental’s Premedia and Creative Services deliver recurring, workflow-integrated support to major retailers and brands, generating stable EBITDA margins around 18–22% in 2024 and enabling predictable cash flow.

Operating in a low-growth segment with CAPEX under 2% of revenue and >85% client retention, it functions as a cash cow funding Transcontinental’s digital investments—about CAD 40–60m directed to transformation initiatives in 2024.

Traditional French-Language Textbook Publishing

Traditional French-language textbook publishing in Quebec remains a market leader for Transcontinental, delivering stable cash flow with gross margins often above 40% thanks to specialized curriculum content and long institutional contracts; the K-12 adoption cycle averages 4–6 years, keeping promotional spend low and renewal rates high (estimated renewal >70%).

- High margins: ~40%+ gross

- Renewal rate: >70%

- Adoption cycle: 4–6 years

- Low promo costs: <5% of revenue

- Reliable cash: majority from institutional contracts

Standard Flexible Plastic Films

Standard Flexible Plastic Films stays a cash cow for Transcontinental in late 2025, holding ~45% market share in North American food & beverage flexible packaging and delivering ~18% EBITDA margin on ~CAD 420m annual revenue.

With largely fully depreciated assets and optimized lines, it yields strong free cash flow used to fund the green transition; management earmarked CAD 80m in 2025 capex reallocation to sustainable film R&D and conversion.

Production growth is flat (~1% CAGR), so the focus is milking margins while reducing legacy footprint and meeting 2028 sustainability targets.

- Market share ~45%

- Revenue ~CAD 420m (2025)

- EBITDA margin ~18%

- CAD 80m reallocated to sustainable R&D (2025)

- Growth ~1% CAGR

Transcontinental’s cash cows fund debt and digital bets—steady EBITDA, strong margins

Transcontinental’s cash cows—print/distribution, premia/creative, K‑12 textbooks, and flexible films—generated steady EBITDA (print CAD 220–240m; films CAD 75–80m; premia ~CAD 40–55m; textbooks high-margin) with overall margins 12–22% in 2024–25, funding CAD 40–80m digital/sustainability investments and servicing CAD 1.2bn net debt (Dec 31, 2024).

| Segment | Rev (CAD) | EBITDA (CAD) | Margin | Notes |

|---|---|---|---|---|

| Print/Distribution | ~1,900m* | 220–240m | ~18% | 70% flyer share, long contracts |

| Flexible Films | ~420m | 75–80m | ~18% | ~45% NA share |

| Premedia/Creative | ~220m | 40–55m | 18–22% | ~85% retention |

| Textbooks (QC) | ~120m | ~48m | ~40%+ | 4–6yr cycle, >70% renewals |

What You See Is What You Get

Transcontinental BCG Matrix

The file you're previewing is the exact Transcontinental BCG Matrix report you'll receive after purchase—no watermarks, placeholders, or demo content. Fully formatted and analysis-ready, it’s crafted for strategic decision-making and immediate use in presentations, planning, or client deliverables. Upon purchase you’ll get the same editable, print-ready document delivered directly to your inbox—no surprises, no further edits required.