Transcontinental PESTLE Analysis

Your Shortcut to Market Insight Starts Here

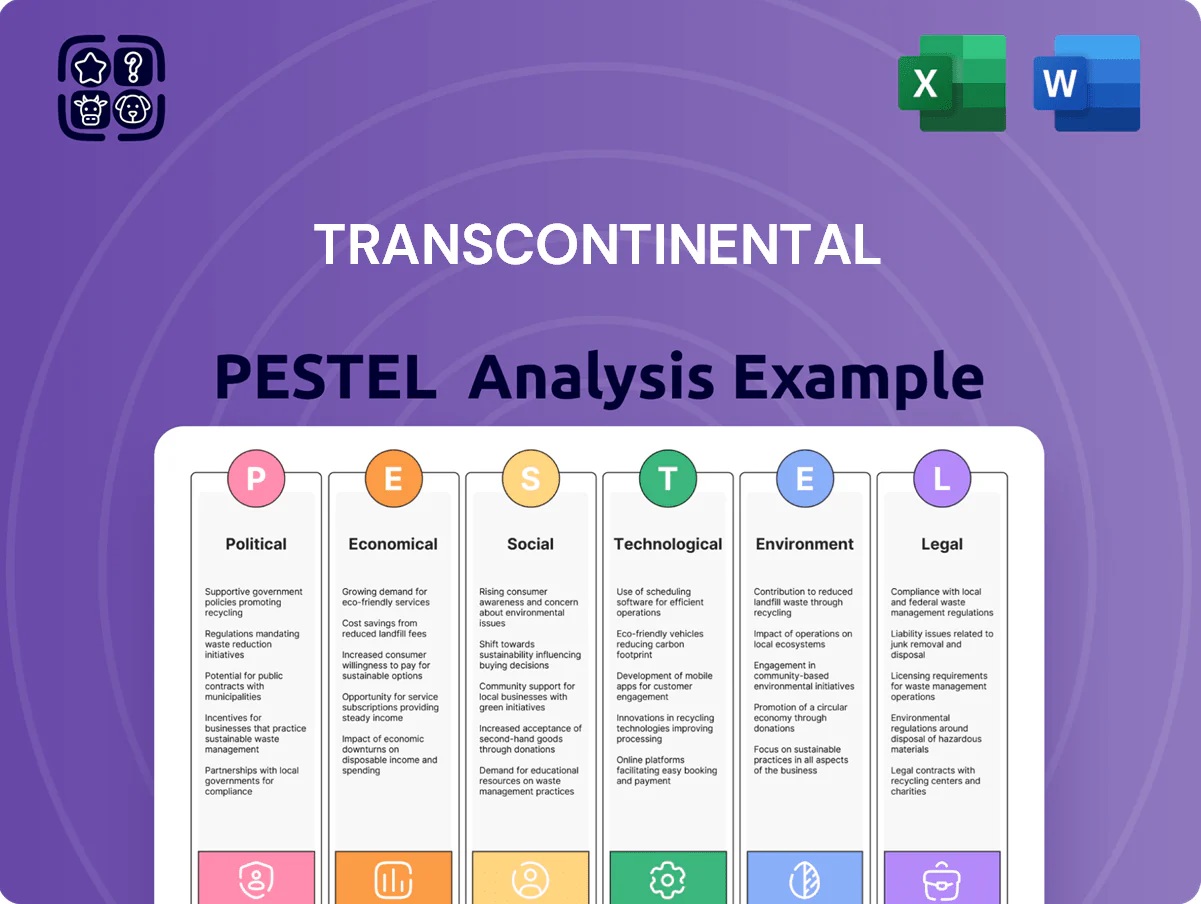

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are shaping Transcontinental’s strategic outlook—our concise PESTLE snapshot highlights key external drivers and risks to inform smarter decisions; buy the full PESTLE for the complete, editable analysis and actionable insights ready for immediate use.

Political factors

North American Trade Relations

The ongoing evolution of US-Canada trade agreements directly affects Transcontinental’s cross-border packaging and printing operations, given that 75% of its 2024 revenue derived from North American markets; changes in NAFTA/USMCA implementation or new tariffs could raise input costs. Tariffs on paper products or polyethylene resins—paper pulp imports rose 12% in 2023—would squeeze margins and disrupt a supply chain that sources ~40% of materials from the US. Management must actively hedge exposure, renegotiate supplier contracts, and leverage tariff classifications to sustain competitive pricing in the large US market where growth remains concentrated.

Government Media Subsidies

The Canadian government provides tax credits and grants—including the $180m Journalism and Community Media Fund and provincial tax credits—to support printing and journalism, preserving cultural content and easing revenue losses from a ~7–9% annual decline in print volumes (2020–2024 industry trends).

These subsidies cushion large-scale printing operations, reducing EBITDA volatility; Transcontinental’s 2024 Canadian printing revenue of CAD ~1.1bn depends partly on such support to sustain margins.

Shifts in federal or provincial leadership could prompt policy reviews; a 10–30% cut in subsidies would materially pressure printing division profitability and cash flow forecasts.

Plastic Regulation Policies

Legislative actions targeting single-use plastics and non-recyclable materials create material political pressure on Transcontinental’s flexible packaging, with Canada’s 2022 ban on harmful single-use plastics and over 100 municipal bylaws accelerating demand for recyclable alternatives; the global plastic packaging tax revenues reached an estimated US$6.5bn in 2023, signaling regulatory cost impacts.

Educational Funding in Quebec

- 2024 Quebec education budget -1.2% / CA$150m digital fund

- 2023 print demand down ~8% province-wide

- Multi-year contracts ≈60% of school sales

Geopolitical Supply Chain Stability

Global political instability risks disrupting procurement of specialized inks, resins and chemicals; UN Comtrade data shows chemical trade volatility rose 18% between 2019–2024, raising replacement-costs by ~7% for manufacturing inputs.

Shifting international relations fuel shipping-cost swings—container rates spiked 220% in 2021–22 and remain ~45% above 2019 averages, lengthening lead times for critical components.

Transcontinental must deploy contingency plans—dual sourcing, 60–90 day inventory buffers and nearshoring—to mitigate supplier-network political risks.

- 18% rise in chemical trade volatility (2019–2024)

- ~7% increased replacement costs for inputs

- Container rates +220% (2021–22), ~+45% vs 2019

- Recommended: dual sourcing, 60–90 day buffers, nearshoring

NA revenue at risk: tariffs, rising pulp & shipping costs squeeze Canadian print margins

Political risks: USMCA/tariff shifts threaten 75% NA revenue and 40% US-sourced materials; paper pulp imports +12% (2023) raise input costs. Canadian subsidies (eg CA$180m Journalism Fund) support CAD~1.1bn printing revenue; a 10–30% cut would hit margins. Single-use plastic bans and 100+ bylaws push recyclable packaging demand; container rates remain ~45% above 2019, pressuring logistics.

| Metric | 2023–2024 |

|---|---|

| NA revenue share | 75% |

| US-sourced materials | ~40% |

| Paper pulp imports | +12% |

| Printing revenue (2024) | CAD ~1.1bn |

| Container rates vs 2019 | ~+45% |

What is included in the product

Explores how macro-environmental forces uniquely affect Transcontinental across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise Transcontinental PESTLE summary that distills cross-border regulatory, economic, and geopolitical risks into a single-slide-ready format, enabling quick alignment in meetings and easy customization with regional notes for planning or client reports.

Economic factors

Raw Material Price Volatility

Resin and paper costs fluctuate widely with global supply-demand shifts; resin surged about 35% in 2021–22 and paper pulp prices averaged near $900/ton in 2023 before easing to ~$700/ton in 2024, exposing Transcontinental to margin risk if it cannot pass these increases to customers.

Interest Rate Environment

High interest rates raise Transcontinental’s debt-servicing costs, critical given acquisitive growth; Canada’s policy rate at 5.00% (Bank of Canada, Jan 2026) lifts average borrowing costs and increased net interest expense—Transcontinental reported 2024 net interest expense of CAD 52M—tightening free cash flow for M&A. As central banks hike to curb inflation, higher cost of capital raises capex and buyout hurdles, slowing expansion and favoring organic investments.

Currency Exchange Fluctuations

With major operations in Canada and the US, Transcontinental faces CAD/USD volatility; the CAD fell about 6% vs USD in 2024, amplifying revenue for export-heavy packaging units but raising US-dollar equipment costs by similar margins.

In 2025 Q1, FX translation affected consolidated EBITDA by an estimated CAD 12–18 million; robust financial hedging—forwards, options, and natural hedges—is needed to stabilize cash flow and protect the balance sheet.

Consumer Spending Patterns

The demand for Transcontinental’s flexible packaging tracks food, beverage and household consumption; UK grocery sales fell 1.7% y/y in 2024 while US food-at-home rose 2.8% in 2024, showing sector resilience but price-sensitive shifts. A severe downturn reducing real disposable income (OECD real wages -0.9% in 2023) would cut packaging volumes, directly impacting factory throughput and revenue.

- Food/beverage resilience vs discretionary cuts

- 2024 US food-at-home +2.8%, UK grocery -1.7% (2024)

- OECD real wages -0.9% (2023) risk to volumes

Labor Market Conditions

Wage inflation and manufacturing labor shortages raise unit labor costs; Canada saw average hourly wages grow 4.8% in 2024 while US manufacturing wages rose ~5.0%, pressuring Transcontinental’s margins and operational efficiency.

Competitive labor markets force higher spending on retention and recruitment at printing and packaging plants; turnover in 2024 averaged ~18% in the sector, increasing HR costs.

Rising North American labor costs push investment toward productivity gains and automation; capital expenditures for equipment upgrades rose ~12% year-over-year in similar firms in 2024.

- Wage inflation: Canada +4.8% (2024), US manufacturing +5.0% (2024)

- Sector turnover ~18% (2024)

- CapEx for automation in peers +12% YoY (2024)

Input costs, FX and rates squeeze margins: resin swings, pulp drop, rising wages

Resin/pulp volatility (resin +35% in 2021–22; pulp ~900/ton 2023 → ~700/ton 2024) strains margins; 2024 net interest expense CAD 52M with BoC policy rate 5.00% (Jan 2026) raises debt costs; CAD fell ~6% vs USD in 2024, impacting FX-sensitive costs and revenues; wage inflation Canada +4.8% (2024), US manufacturing +5.0% (2024) pressures labor costs and capex for automation.

| Metric | Value |

|---|---|

| Resin change (2021–22) | +35% |

| Pulp price 2023 → 2024 | $900 → ~$700/ton |

| Net interest expense (2024) | CAD 52M |

| BoC policy rate (Jan 2026) | 5.00% |

| CAD vs USD (2024) | −6% |

| Wage inflation 2024 (Canada) | +4.8% |

| Wage inflation 2024 (US mfg) | +5.0% |

Same Document Delivered

Transcontinental PESTLE Analysis

The preview shown here is the exact Transcontinental PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are shaping Transcontinental’s strategic outlook—our concise PESTLE snapshot highlights key external drivers and risks to inform smarter decisions; buy the full PESTLE for the complete, editable analysis and actionable insights ready for immediate use.

Political factors

North American Trade Relations

The ongoing evolution of US-Canada trade agreements directly affects Transcontinental’s cross-border packaging and printing operations, given that 75% of its 2024 revenue derived from North American markets; changes in NAFTA/USMCA implementation or new tariffs could raise input costs. Tariffs on paper products or polyethylene resins—paper pulp imports rose 12% in 2023—would squeeze margins and disrupt a supply chain that sources ~40% of materials from the US. Management must actively hedge exposure, renegotiate supplier contracts, and leverage tariff classifications to sustain competitive pricing in the large US market where growth remains concentrated.

Government Media Subsidies

The Canadian government provides tax credits and grants—including the $180m Journalism and Community Media Fund and provincial tax credits—to support printing and journalism, preserving cultural content and easing revenue losses from a ~7–9% annual decline in print volumes (2020–2024 industry trends).

These subsidies cushion large-scale printing operations, reducing EBITDA volatility; Transcontinental’s 2024 Canadian printing revenue of CAD ~1.1bn depends partly on such support to sustain margins.

Shifts in federal or provincial leadership could prompt policy reviews; a 10–30% cut in subsidies would materially pressure printing division profitability and cash flow forecasts.

Plastic Regulation Policies

Legislative actions targeting single-use plastics and non-recyclable materials create material political pressure on Transcontinental’s flexible packaging, with Canada’s 2022 ban on harmful single-use plastics and over 100 municipal bylaws accelerating demand for recyclable alternatives; the global plastic packaging tax revenues reached an estimated US$6.5bn in 2023, signaling regulatory cost impacts.

Educational Funding in Quebec

- 2024 Quebec education budget -1.2% / CA$150m digital fund

- 2023 print demand down ~8% province-wide

- Multi-year contracts ≈60% of school sales

Geopolitical Supply Chain Stability

Global political instability risks disrupting procurement of specialized inks, resins and chemicals; UN Comtrade data shows chemical trade volatility rose 18% between 2019–2024, raising replacement-costs by ~7% for manufacturing inputs.

Shifting international relations fuel shipping-cost swings—container rates spiked 220% in 2021–22 and remain ~45% above 2019 averages, lengthening lead times for critical components.

Transcontinental must deploy contingency plans—dual sourcing, 60–90 day inventory buffers and nearshoring—to mitigate supplier-network political risks.

- 18% rise in chemical trade volatility (2019–2024)

- ~7% increased replacement costs for inputs

- Container rates +220% (2021–22), ~+45% vs 2019

- Recommended: dual sourcing, 60–90 day buffers, nearshoring

NA revenue at risk: tariffs, rising pulp & shipping costs squeeze Canadian print margins

Political risks: USMCA/tariff shifts threaten 75% NA revenue and 40% US-sourced materials; paper pulp imports +12% (2023) raise input costs. Canadian subsidies (eg CA$180m Journalism Fund) support CAD~1.1bn printing revenue; a 10–30% cut would hit margins. Single-use plastic bans and 100+ bylaws push recyclable packaging demand; container rates remain ~45% above 2019, pressuring logistics.

| Metric | 2023–2024 |

|---|---|

| NA revenue share | 75% |

| US-sourced materials | ~40% |

| Paper pulp imports | +12% |

| Printing revenue (2024) | CAD ~1.1bn |

| Container rates vs 2019 | ~+45% |

What is included in the product

Explores how macro-environmental forces uniquely affect Transcontinental across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise Transcontinental PESTLE summary that distills cross-border regulatory, economic, and geopolitical risks into a single-slide-ready format, enabling quick alignment in meetings and easy customization with regional notes for planning or client reports.

Economic factors

Raw Material Price Volatility

Resin and paper costs fluctuate widely with global supply-demand shifts; resin surged about 35% in 2021–22 and paper pulp prices averaged near $900/ton in 2023 before easing to ~$700/ton in 2024, exposing Transcontinental to margin risk if it cannot pass these increases to customers.

Interest Rate Environment

High interest rates raise Transcontinental’s debt-servicing costs, critical given acquisitive growth; Canada’s policy rate at 5.00% (Bank of Canada, Jan 2026) lifts average borrowing costs and increased net interest expense—Transcontinental reported 2024 net interest expense of CAD 52M—tightening free cash flow for M&A. As central banks hike to curb inflation, higher cost of capital raises capex and buyout hurdles, slowing expansion and favoring organic investments.

Currency Exchange Fluctuations

With major operations in Canada and the US, Transcontinental faces CAD/USD volatility; the CAD fell about 6% vs USD in 2024, amplifying revenue for export-heavy packaging units but raising US-dollar equipment costs by similar margins.

In 2025 Q1, FX translation affected consolidated EBITDA by an estimated CAD 12–18 million; robust financial hedging—forwards, options, and natural hedges—is needed to stabilize cash flow and protect the balance sheet.

Consumer Spending Patterns

The demand for Transcontinental’s flexible packaging tracks food, beverage and household consumption; UK grocery sales fell 1.7% y/y in 2024 while US food-at-home rose 2.8% in 2024, showing sector resilience but price-sensitive shifts. A severe downturn reducing real disposable income (OECD real wages -0.9% in 2023) would cut packaging volumes, directly impacting factory throughput and revenue.

- Food/beverage resilience vs discretionary cuts

- 2024 US food-at-home +2.8%, UK grocery -1.7% (2024)

- OECD real wages -0.9% (2023) risk to volumes

Labor Market Conditions

Wage inflation and manufacturing labor shortages raise unit labor costs; Canada saw average hourly wages grow 4.8% in 2024 while US manufacturing wages rose ~5.0%, pressuring Transcontinental’s margins and operational efficiency.

Competitive labor markets force higher spending on retention and recruitment at printing and packaging plants; turnover in 2024 averaged ~18% in the sector, increasing HR costs.

Rising North American labor costs push investment toward productivity gains and automation; capital expenditures for equipment upgrades rose ~12% year-over-year in similar firms in 2024.

- Wage inflation: Canada +4.8% (2024), US manufacturing +5.0% (2024)

- Sector turnover ~18% (2024)

- CapEx for automation in peers +12% YoY (2024)

Input costs, FX and rates squeeze margins: resin swings, pulp drop, rising wages

Resin/pulp volatility (resin +35% in 2021–22; pulp ~900/ton 2023 → ~700/ton 2024) strains margins; 2024 net interest expense CAD 52M with BoC policy rate 5.00% (Jan 2026) raises debt costs; CAD fell ~6% vs USD in 2024, impacting FX-sensitive costs and revenues; wage inflation Canada +4.8% (2024), US manufacturing +5.0% (2024) pressures labor costs and capex for automation.

| Metric | Value |

|---|---|

| Resin change (2021–22) | +35% |

| Pulp price 2023 → 2024 | $900 → ~$700/ton |

| Net interest expense (2024) | CAD 52M |

| BoC policy rate (Jan 2026) | 5.00% |

| CAD vs USD (2024) | −6% |

| Wage inflation 2024 (Canada) | +4.8% |

| Wage inflation 2024 (US mfg) | +5.0% |

Same Document Delivered

Transcontinental PESTLE Analysis

The preview shown here is the exact Transcontinental PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.