Telephone & Data Systems Boston Consulting Group Matrix

Download Your Competitive Advantage

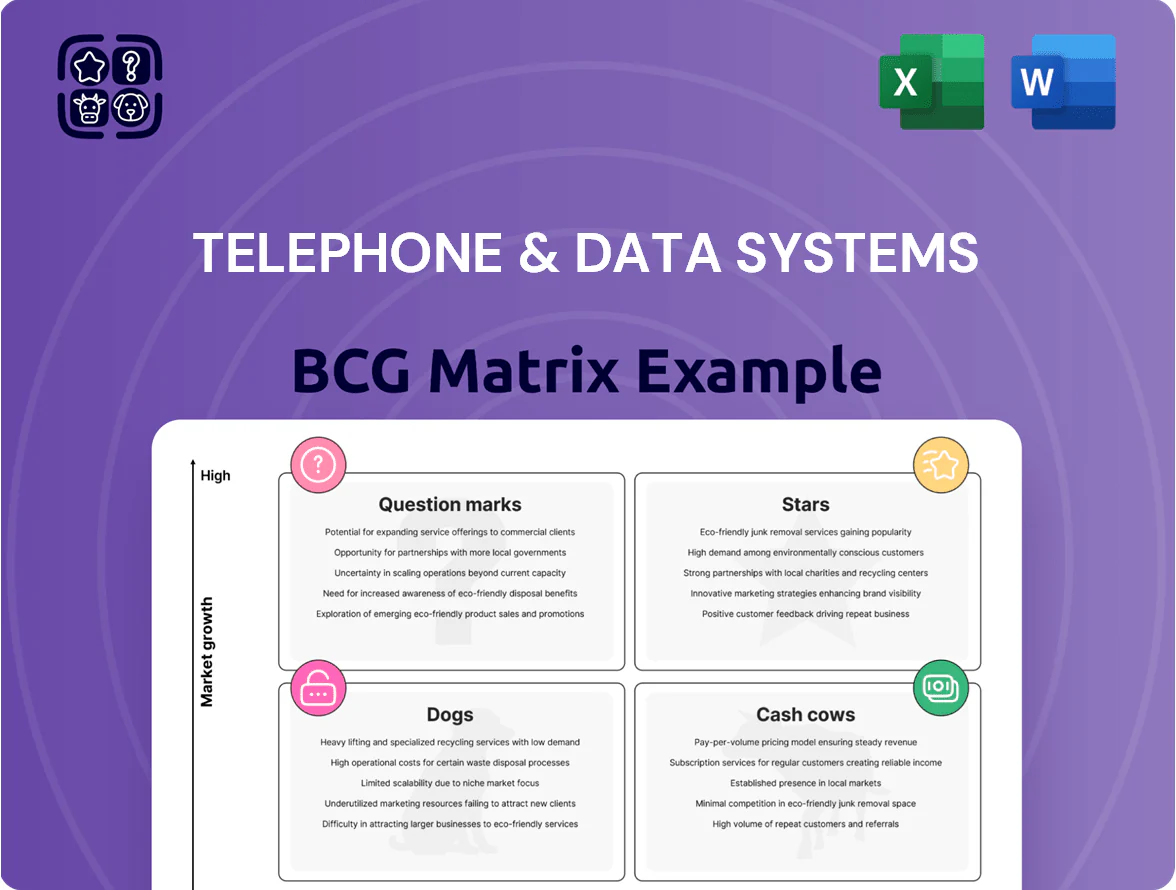

Discover how Telephone & Data Systems maps across the BCG Matrix—identifying which segments are Stars driving growth, Cash Cows funding stability, Dogs draining resources, or Question Marks needing investment decisions; this snapshot highlights strategic priorities and competitive positioning. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables to inform capital allocation and product strategy.

Stars

Fiber-to-the-Home (FTTH) Expansion

TDS Telecom has pushed into fiber-to-the-home, adding over 540,000 fiber passings since 2019 and reaching ~1.2 million passings by year-end 2024, capturing strong share in mid-size and rural builds.

Demand for symmetrical gigabit plans fuels high growth: fiber revenue grew ~18% CAGR 2021–2024 as residential ARPU rose to about $62 in 2024 from $51 in 2021.

Capex remains heavy—TDS spent $540 million on fiber capex in 2024—but these fiber footprints are the main growth engine driving longer-term valuation upside.

Enterprise Managed Services

TDS Network Services' Enterprise Managed Services sits in the BCG Matrix as a Star: enterprise customers drove 18% revenue growth in 2024, with managed security and hosted IT now 27% of business services revenue.

5G Mid-Band Spectrum Deployment

Through U.S. Cellular, Telephone & Data Systems (TDS) has deployed mid-band 2.5 GHz and C-band spectrum covering key regional hubs, investing roughly $1.1 billion in spectrum and network capex from 2023–2025 to deliver 5G speeds comparable to national carriers in markets like Milwaukee and Des Moines.

This asset is a Star in the BCG Matrix: it holds double-digit local share in those hubs while operating in the wireless data segment, which grew ~14% CAGR U.S. mobile data traffic 2019–2024 (Ericsson Mobility Report).

Maintaining parity requires continued capex—TDS guided $500–550 million annual network spend for 2025—so sustained investment is needed to capture rising mobile bandwidth demand and protect market share.

Fixed Wireless Access (FWA)

Fixed Wireless Access (FWA) via U.S. Cellular is a Star: rapid revenue growth and share gains in rural broadband where fiber lags; FWA adds ~$225–270 ARPU per household and TDS reported ~120k FWA subscribers by end-2024, driving double-digit YoY broadband adds.

FWA sits between wireless and wireline, using existing towers to deliver gig-capable speeds in many markets but needs ongoing capital for densification—TDS guided $1.1–1.3B capex for 2025 to support tower upgrades and spectrum.

- ~120k FWA subs (end-2024)

- ARPU ~$225–270 per FWA household

- 2025 capex guidance $1.1–1.3B

- High growth, requires network densification

Public Sector Infrastructure Contracts

TDS (Telephone & Data Systems) holds a leading role in public sector infrastructure, supplying high-speed fiber and managed networking to municipalities and schools; in 2024 TDS reported $420m revenue from fixed broadband and public sector services, up 8% year-over-year as smart-city and K–12 upgrades drove demand.

The segment shows high growth potential—US municipal broadband and smart-city spending is forecast at $12.8bn in 2025—and TDS’s local presence wins ~65% win-rate on regional RFPs versus national carriers for contracts >$1m.

Localized engineering, faster permitting, and education-focused SLAs let TDS capture high-share, high-margin projects, reducing churn and boosting average contract value to $1.2m per deal in 2024.

- 2024 public-sector revenue: $420m

- Win-rate on regional RFPs: ~65%

- Avg contract value 2024: $1.2m

- US smart-city spend forecast 2025: $12.8bn

TDS Growth Surge: Fiber, 5G/FWA, Enterprise & Public Sector Fuel $1.1B+ Capex Push

TDS Stars: fiber, enterprise managed services, U.S. Cellular 5G/FWA and public-sector services show high growth and share; 2019–2024 fiber passings +540k to ~1.2M, fiber revenue CAGR ~18%, 2024 fiber capex $540M, U.S. Cellular spectrum/network spend 2023–25 ~$1.1B, FWA ~120k subs end-2024, public-sector revenue $420M (2024), 2025 capex guidance $1.1–1.3B.

| Metric | Value |

|---|---|

| Fiber passings (2024) | ~1.2M |

| Fiber rev CAGR 2021–24 | ~18% |

| FWA subs (end-2024) | ~120k |

| Public-sector rev (2024) | $420M |

| 2025 capex guidance | $1.1–1.3B |

What is included in the product

BCG Matrix mapping of Telephone & Data Systems’ units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs amid market trends.

One-page BCG Matrix placing TDS business units in clear quadrants for fast C-level decisions and slide-ready export.

Cash Cows

Legacy Wireline Voice Services

Legacy copper-based voice services still deliver steady cash for Telephone & Data Systems, generating roughly $120–150 million in annual EBITDA as of 2025 despite declining subscriber counts, because the plant is largely fully depreciated and incremental opex is low.

Postpaid Wireless Subscriptions

U.S. Cellulars core postpaid base drives stable monthly recurring revenue—about 4.7 million subscribers at year-end 2024, supporting predictable cash flow and a 2024 postpaid ARPU near $58 per month.

In its mature regional markets the carrier holds above 30% share in key rural counties with churn around 1.1% quarterly for long-term customers, keeping retention strong.

This segment needs mainly maintenance capex—capital intensity under 15% of revenue in 2024—making it the primary liquidity source for dividends, debt service, and selective growth.

Wholesale Roaming Revenue

U.S. Cellular’s wholesale roaming revenue—about $175 million in 2024, roughly 12% of total operating revenue—comes from leasing regional tower access to national carriers where their coverage is thin.

This high-margin stream, with EBITDA margins near 60% in key corridors, dominates roaming in rural Midwest and Mountain regions, giving it a cash-cow profile.

That predictable cash funds debt service (net debt about $1.1 billion end-2024) and supports steady dividends and network upkeep.

Cable Broadband in Mature Markets

Cable broadband in TDS Telecom’s mature U.S. territories holds high market share and stable ARPU; as of FY 2025 TDS reported cable broadband revenue roughly $620M and mid-single-digit annual price growth, yielding predictable free cash flow that funds higher-risk Question Marks.

These markets need little promotion, show high entry barriers (capex for last-mile fiber >$1,000/customer), and deliver steady margins that underpin corporate growth investments.

- FY 2025 cable broadband revenue ≈ $620M

- Mid-single-digit annual price growth (2023–25)

- High barriers: >$1,000/customer fiber build

- Stable cash flow funds Question Marks

Tower Portfolio Leasing

TDS owns and leases ~7,500 physical towers and rooftop sites, generating steady rental cash flow concentrated in rural US markets where TDS holds high share; towers sit in a mature, low-growth segment with national tower REITs growing faster but rural penetration giving TDS pricing power.

Rental income is largely passive and high-margin—tower EBITDA margins often exceed 70%—with negligible operational overhead; in 2024 tower segment contributed an estimated $120–150m annual EBITDA to TDS parent results.

- High rural share: ~60–70% of sites in low-competition areas

- Mature market: single-digit annual growth

- Passive, high-margin cash: ~70%+ EBITDA

- Estimated 2024 tower EBITDA: $120–150m

Stable cash cows: $1.1–1.3B revenue, $520–570M EBITDA fuels dividends & growth

Cash cows: legacy copper voice, U.S. Cellular postpaid, cable broadband, roaming and tower rentals together generated ~ $1.1–1.3B revenue and ~$520–570M EBITDA in 2024–25, funding dividends, debt service (net debt ~$1.1B end-2024) and selective growth.

| Segment | Rev 2024–25 | EBITDA | Key metric |

|---|---|---|---|

| Copper voice | — | $120–150M | Low opex, depreciated plant |

| U.S. Cellular postpaid | — | — | 4.7M subs, ARPU $58 |

| Roaming | $175M | ~60% margin | 12% of rev |

| Cable broadband | $620M | mid-single-digit growth | High share, low capex % |

| Towers | — | $120–150M | ~7,500 sites, ~70% EBITDA |

Preview = Final Product

Telephone & Data Systems BCG Matrix

The file you're previewing is the exact Telephone & Data Systems BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just the fully formatted, analysis-ready document designed for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Discover how Telephone & Data Systems maps across the BCG Matrix—identifying which segments are Stars driving growth, Cash Cows funding stability, Dogs draining resources, or Question Marks needing investment decisions; this snapshot highlights strategic priorities and competitive positioning. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables to inform capital allocation and product strategy.

Stars

Fiber-to-the-Home (FTTH) Expansion

TDS Telecom has pushed into fiber-to-the-home, adding over 540,000 fiber passings since 2019 and reaching ~1.2 million passings by year-end 2024, capturing strong share in mid-size and rural builds.

Demand for symmetrical gigabit plans fuels high growth: fiber revenue grew ~18% CAGR 2021–2024 as residential ARPU rose to about $62 in 2024 from $51 in 2021.

Capex remains heavy—TDS spent $540 million on fiber capex in 2024—but these fiber footprints are the main growth engine driving longer-term valuation upside.

Enterprise Managed Services

TDS Network Services' Enterprise Managed Services sits in the BCG Matrix as a Star: enterprise customers drove 18% revenue growth in 2024, with managed security and hosted IT now 27% of business services revenue.

5G Mid-Band Spectrum Deployment

Through U.S. Cellular, Telephone & Data Systems (TDS) has deployed mid-band 2.5 GHz and C-band spectrum covering key regional hubs, investing roughly $1.1 billion in spectrum and network capex from 2023–2025 to deliver 5G speeds comparable to national carriers in markets like Milwaukee and Des Moines.

This asset is a Star in the BCG Matrix: it holds double-digit local share in those hubs while operating in the wireless data segment, which grew ~14% CAGR U.S. mobile data traffic 2019–2024 (Ericsson Mobility Report).

Maintaining parity requires continued capex—TDS guided $500–550 million annual network spend for 2025—so sustained investment is needed to capture rising mobile bandwidth demand and protect market share.

Fixed Wireless Access (FWA)

Fixed Wireless Access (FWA) via U.S. Cellular is a Star: rapid revenue growth and share gains in rural broadband where fiber lags; FWA adds ~$225–270 ARPU per household and TDS reported ~120k FWA subscribers by end-2024, driving double-digit YoY broadband adds.

FWA sits between wireless and wireline, using existing towers to deliver gig-capable speeds in many markets but needs ongoing capital for densification—TDS guided $1.1–1.3B capex for 2025 to support tower upgrades and spectrum.

- ~120k FWA subs (end-2024)

- ARPU ~$225–270 per FWA household

- 2025 capex guidance $1.1–1.3B

- High growth, requires network densification

Public Sector Infrastructure Contracts

TDS (Telephone & Data Systems) holds a leading role in public sector infrastructure, supplying high-speed fiber and managed networking to municipalities and schools; in 2024 TDS reported $420m revenue from fixed broadband and public sector services, up 8% year-over-year as smart-city and K–12 upgrades drove demand.

The segment shows high growth potential—US municipal broadband and smart-city spending is forecast at $12.8bn in 2025—and TDS’s local presence wins ~65% win-rate on regional RFPs versus national carriers for contracts >$1m.

Localized engineering, faster permitting, and education-focused SLAs let TDS capture high-share, high-margin projects, reducing churn and boosting average contract value to $1.2m per deal in 2024.

- 2024 public-sector revenue: $420m

- Win-rate on regional RFPs: ~65%

- Avg contract value 2024: $1.2m

- US smart-city spend forecast 2025: $12.8bn

TDS Growth Surge: Fiber, 5G/FWA, Enterprise & Public Sector Fuel $1.1B+ Capex Push

TDS Stars: fiber, enterprise managed services, U.S. Cellular 5G/FWA and public-sector services show high growth and share; 2019–2024 fiber passings +540k to ~1.2M, fiber revenue CAGR ~18%, 2024 fiber capex $540M, U.S. Cellular spectrum/network spend 2023–25 ~$1.1B, FWA ~120k subs end-2024, public-sector revenue $420M (2024), 2025 capex guidance $1.1–1.3B.

| Metric | Value |

|---|---|

| Fiber passings (2024) | ~1.2M |

| Fiber rev CAGR 2021–24 | ~18% |

| FWA subs (end-2024) | ~120k |

| Public-sector rev (2024) | $420M |

| 2025 capex guidance | $1.1–1.3B |

What is included in the product

BCG Matrix mapping of Telephone & Data Systems’ units with strategic moves for Stars, Cash Cows, Question Marks, and Dogs amid market trends.

One-page BCG Matrix placing TDS business units in clear quadrants for fast C-level decisions and slide-ready export.

Cash Cows

Legacy Wireline Voice Services

Legacy copper-based voice services still deliver steady cash for Telephone & Data Systems, generating roughly $120–150 million in annual EBITDA as of 2025 despite declining subscriber counts, because the plant is largely fully depreciated and incremental opex is low.

Postpaid Wireless Subscriptions

U.S. Cellulars core postpaid base drives stable monthly recurring revenue—about 4.7 million subscribers at year-end 2024, supporting predictable cash flow and a 2024 postpaid ARPU near $58 per month.

In its mature regional markets the carrier holds above 30% share in key rural counties with churn around 1.1% quarterly for long-term customers, keeping retention strong.

This segment needs mainly maintenance capex—capital intensity under 15% of revenue in 2024—making it the primary liquidity source for dividends, debt service, and selective growth.

Wholesale Roaming Revenue

U.S. Cellular’s wholesale roaming revenue—about $175 million in 2024, roughly 12% of total operating revenue—comes from leasing regional tower access to national carriers where their coverage is thin.

This high-margin stream, with EBITDA margins near 60% in key corridors, dominates roaming in rural Midwest and Mountain regions, giving it a cash-cow profile.

That predictable cash funds debt service (net debt about $1.1 billion end-2024) and supports steady dividends and network upkeep.

Cable Broadband in Mature Markets

Cable broadband in TDS Telecom’s mature U.S. territories holds high market share and stable ARPU; as of FY 2025 TDS reported cable broadband revenue roughly $620M and mid-single-digit annual price growth, yielding predictable free cash flow that funds higher-risk Question Marks.

These markets need little promotion, show high entry barriers (capex for last-mile fiber >$1,000/customer), and deliver steady margins that underpin corporate growth investments.

- FY 2025 cable broadband revenue ≈ $620M

- Mid-single-digit annual price growth (2023–25)

- High barriers: >$1,000/customer fiber build

- Stable cash flow funds Question Marks

Tower Portfolio Leasing

TDS owns and leases ~7,500 physical towers and rooftop sites, generating steady rental cash flow concentrated in rural US markets where TDS holds high share; towers sit in a mature, low-growth segment with national tower REITs growing faster but rural penetration giving TDS pricing power.

Rental income is largely passive and high-margin—tower EBITDA margins often exceed 70%—with negligible operational overhead; in 2024 tower segment contributed an estimated $120–150m annual EBITDA to TDS parent results.

- High rural share: ~60–70% of sites in low-competition areas

- Mature market: single-digit annual growth

- Passive, high-margin cash: ~70%+ EBITDA

- Estimated 2024 tower EBITDA: $120–150m

Stable cash cows: $1.1–1.3B revenue, $520–570M EBITDA fuels dividends & growth

Cash cows: legacy copper voice, U.S. Cellular postpaid, cable broadband, roaming and tower rentals together generated ~ $1.1–1.3B revenue and ~$520–570M EBITDA in 2024–25, funding dividends, debt service (net debt ~$1.1B end-2024) and selective growth.

| Segment | Rev 2024–25 | EBITDA | Key metric |

|---|---|---|---|

| Copper voice | — | $120–150M | Low opex, depreciated plant |

| U.S. Cellular postpaid | — | — | 4.7M subs, ARPU $58 |

| Roaming | $175M | ~60% margin | 12% of rev |

| Cable broadband | $620M | mid-single-digit growth | High share, low capex % |

| Towers | — | $120–150M | ~7,500 sites, ~70% EBITDA |

Preview = Final Product

Telephone & Data Systems BCG Matrix

The file you're previewing is the exact Telephone & Data Systems BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just the fully formatted, analysis-ready document designed for strategic clarity and professional use.