Telephone & Data Systems Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

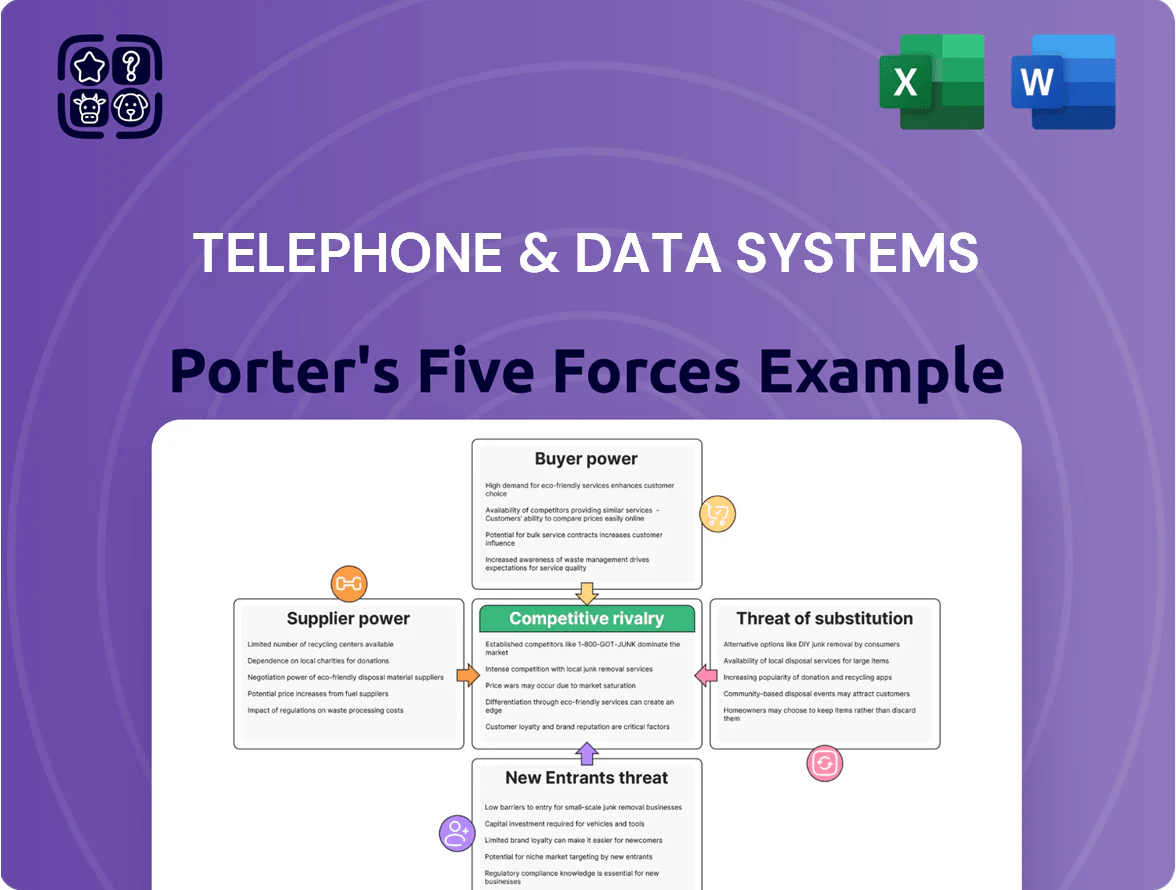

Telephone & Data Systems faces moderate buyer power, capital-intensive barriers to entry, and evolving substitute threats from OTT and wireless providers, while supplier leverage and regulatory pressure shape margins.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Telephone & Data Systems’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Network Equipment Providers

The 5G and fiber-optic hardware market is concentrated among Nokia, Ericsson, and Samsung, giving them pricing and support leverage over TDS (Telephone & Data Systems). TDS depends on these vendors for radios, basebands, and fiber gear as it upgrades networks, and vendor concentration raises capex risk: TDS forecasted ~\$900m–\$1.0bn network spend for 2024–25, much tied to vendor contracts. This leverage intensifies as TDS moves to FTTH by end-2025, limiting its bargaining power on lead times, firmware support, and upgrade pricing.

Dependency on Smartphone Manufacturers

UScellular’s subscriber growth hinges on access to Apple iPhone and Samsung Galaxy flagships; Apple held 53% of US smartphone OS market share in Q4 2024, making its allocations critical. These OEMs set release schedules and inventory, so TDS (market cap ~1.6B in 2025) can face constrained allocations versus Verizon and AT&T, which bought larger volumes. During 2020–24 supply shocks, smaller carriers saw shipment delays up to 30% versus majors, raising churn risk if flagship stock runs out.

Content Acquisition Costs for Video Services

TDS Telecom faces rising content acquisition costs as media giants push higher retransmission fees; AT&T/Warner Bros. Discovery and Comcast/NBCUniversal reported retrans fee growth of ~5–8% YoY in 2024, pressuring regional carriers.

With linear pay-TV subs down ~10–12% annually industry-wide (NCTA data 2023–24), content owners seek higher per-subscriber fees to offset losses, squeezing TDS margins.

TDS must absorb costs or raise prices; a $2–5 monthly fee hike could boost ARPU but risks 5–10% churn in competitive MVPD/streaming markets, per 2024 churn benchmarks.

Spectrum Acquisition and Regulatory Constraints

Federal government auctions and three large carriers (Verizon, AT&T, T-Mobile) control most mid‑band and mmWave spectrum after $120B+ auctions through 2023–2025, making licenses scarce for TDS; spectrum access now hinges on winning costly auctions or negotiating secondary deals with bigger rivals, often at premium prices.

That supply constraint raises capex risk—TDS spent roughly $200–400M annually on spectrum and network licenses in recent filings—and limits rapid 5G expansion without costly partnerships or spectrum leases.

- Primary gatekeepers: FCC auctions, Verizon/AT&T/T‑Mobile dominance

- Market fact: $120B+ major auctions 2023–2025

- Financial impact: TDS spectrum/network spend ~ $200–400M/yr

- Strategy: bid, lease, or buy via secondary markets

Labor and Specialized Technical Talent

The US fiber build surge drove demand for network engineers; BLS 2024 data shows 5% growth for telecom installers and technicians, tightening supply in key states where TDS operates.

TDS (Telephone & Data Systems Inc.) competes with AT&T and Lumen and with infra firms for scarce talent, raising wage costs—industry reports in 2024 note 8–12% year-over-year pay hikes for specialized technicians.

Continuous 5G/10G training needs increase OPEX and delay rollouts; a conservative estimate: 3–6% higher project labor costs and 1–3 month timeline extensions on fiber builds versus past averages.

- Labor supply tight; 5% job growth (BLS 2024)

- Wage pressure: +8–12% in 2024

- OPEX impact: +3–6% labor cost

- Project delays: +1–3 months

Suppliers wield outsized leverage over TDS—$1bn capex, $200–400m spectrum, iPhone 53%

Suppliers (Nokia, Ericsson, Samsung; Apple/Samsung for handsets; content owners; spectrum sellers; labor) hold strong bargaining power vs TDS—vendor concentration, $900m–$1.0bn 2024–25 network capex, $200–400m/yr spectrum spend, 53% iPhone OS share (Q4 2024), 5–12% wage inflation (2024) raise costs, limit lead-time, pricing, and expansion options.

| Item | Key number |

|---|---|

| Network capex | $900m–$1.0bn (2024–25) |

| Spectrum spend | $200–$400m/yr |

| Apple OS share | 53% (Q4 2024) |

| Wage inflation | 5–12% (2024) |

What is included in the product

Tailored exclusively for Telephone & Data Systems, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its market position and profitability.

A concise Porter's Five Forces snapshot for Telephone & Data Systems—quickly spot where competitive pressure eases and prioritize strategic moves to protect margins.

Customers Bargaining Power

Low Switching Costs in Wireless Services

High Price Sensitivity in Rural Markets

Demand for High-Speed Symmetrical Broadband

Consumer expectations now favor symmetrical gigabit-class broadband for remote work and 4K/8K streaming; surveys in 2024 show 62% of US households rate upload speed as critical. In TDS Telecom markets, fiber adoption rose 18% YoY in 2024, making fiber-grade service a baseline demand. That shift strengthens buyer leverage: customers push for upgrades from copper/DSL and will switch to the first reliable fiber entrant in their neighborhood.

Availability of Alternative Service Providers

Availability of Alternative Service Providers weakens TDS’s customer bargaining power: national cable giants (Comcast, Charter) and satellite providers (Viasat, HughesNet) plus fiber overbuilders expanded options, letting customers demand lower prices or promos; US fixed broadband competition rose—FCC reported 2024 that 94% of households had two+ providers, up from 88% in 2018.

- Multiple rivals: cable, fiber, satellite

- 94% US homes have 2+ providers (FCC 2024)

- Fiber footprint growth through 2025 erodes regional monopolies

Enterprise and Wholesale Negotiation Leverage

Large enterprise and government clients account for a meaningful share of TDS revenue and wield strong leverage: in 2024 approximately 30% of U.S. commercial telecom spend flowed through RFP-driven contracts, pressuring margins.

These buyers run formal bids for managed services, hosted VoIP, and data center space, forcing TDS to offer deep discounts and tailored SLAs to secure multi-year deals, which can cut EBITDA margins by 200–400 basis points on those accounts.

TDS margin squeeze: high buyer power, $44 ARPU, unlocked phones & fierce broadband choice

| Metric | Value |

|---|---|

| ARPU (2024) | $44.20 |

| Homes w/2+ providers (2024) | 94% |

| Unlocked handsets (2025) | 70% |

| Portability growth (2024–25) | +8% |

Full Version Awaits

Telephone & Data Systems Porter's Five Forces Analysis

This preview shows the exact Telephone & Data Systems Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy. You're looking at the actual, professionally written analysis file; once you complete your purchase, you’ll get instant access to this exact document. No mockups or samples—what you see is what you’ll be able to download after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Telephone & Data Systems faces moderate buyer power, capital-intensive barriers to entry, and evolving substitute threats from OTT and wireless providers, while supplier leverage and regulatory pressure shape margins.

This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Telephone & Data Systems’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Network Equipment Providers

The 5G and fiber-optic hardware market is concentrated among Nokia, Ericsson, and Samsung, giving them pricing and support leverage over TDS (Telephone & Data Systems). TDS depends on these vendors for radios, basebands, and fiber gear as it upgrades networks, and vendor concentration raises capex risk: TDS forecasted ~\$900m–\$1.0bn network spend for 2024–25, much tied to vendor contracts. This leverage intensifies as TDS moves to FTTH by end-2025, limiting its bargaining power on lead times, firmware support, and upgrade pricing.

Dependency on Smartphone Manufacturers

UScellular’s subscriber growth hinges on access to Apple iPhone and Samsung Galaxy flagships; Apple held 53% of US smartphone OS market share in Q4 2024, making its allocations critical. These OEMs set release schedules and inventory, so TDS (market cap ~1.6B in 2025) can face constrained allocations versus Verizon and AT&T, which bought larger volumes. During 2020–24 supply shocks, smaller carriers saw shipment delays up to 30% versus majors, raising churn risk if flagship stock runs out.

Content Acquisition Costs for Video Services

TDS Telecom faces rising content acquisition costs as media giants push higher retransmission fees; AT&T/Warner Bros. Discovery and Comcast/NBCUniversal reported retrans fee growth of ~5–8% YoY in 2024, pressuring regional carriers.

With linear pay-TV subs down ~10–12% annually industry-wide (NCTA data 2023–24), content owners seek higher per-subscriber fees to offset losses, squeezing TDS margins.

TDS must absorb costs or raise prices; a $2–5 monthly fee hike could boost ARPU but risks 5–10% churn in competitive MVPD/streaming markets, per 2024 churn benchmarks.

Spectrum Acquisition and Regulatory Constraints

Federal government auctions and three large carriers (Verizon, AT&T, T-Mobile) control most mid‑band and mmWave spectrum after $120B+ auctions through 2023–2025, making licenses scarce for TDS; spectrum access now hinges on winning costly auctions or negotiating secondary deals with bigger rivals, often at premium prices.

That supply constraint raises capex risk—TDS spent roughly $200–400M annually on spectrum and network licenses in recent filings—and limits rapid 5G expansion without costly partnerships or spectrum leases.

- Primary gatekeepers: FCC auctions, Verizon/AT&T/T‑Mobile dominance

- Market fact: $120B+ major auctions 2023–2025

- Financial impact: TDS spectrum/network spend ~ $200–400M/yr

- Strategy: bid, lease, or buy via secondary markets

Labor and Specialized Technical Talent

The US fiber build surge drove demand for network engineers; BLS 2024 data shows 5% growth for telecom installers and technicians, tightening supply in key states where TDS operates.

TDS (Telephone & Data Systems Inc.) competes with AT&T and Lumen and with infra firms for scarce talent, raising wage costs—industry reports in 2024 note 8–12% year-over-year pay hikes for specialized technicians.

Continuous 5G/10G training needs increase OPEX and delay rollouts; a conservative estimate: 3–6% higher project labor costs and 1–3 month timeline extensions on fiber builds versus past averages.

- Labor supply tight; 5% job growth (BLS 2024)

- Wage pressure: +8–12% in 2024

- OPEX impact: +3–6% labor cost

- Project delays: +1–3 months

Suppliers wield outsized leverage over TDS—$1bn capex, $200–400m spectrum, iPhone 53%

Suppliers (Nokia, Ericsson, Samsung; Apple/Samsung for handsets; content owners; spectrum sellers; labor) hold strong bargaining power vs TDS—vendor concentration, $900m–$1.0bn 2024–25 network capex, $200–400m/yr spectrum spend, 53% iPhone OS share (Q4 2024), 5–12% wage inflation (2024) raise costs, limit lead-time, pricing, and expansion options.

| Item | Key number |

|---|---|

| Network capex | $900m–$1.0bn (2024–25) |

| Spectrum spend | $200–$400m/yr |

| Apple OS share | 53% (Q4 2024) |

| Wage inflation | 5–12% (2024) |

What is included in the product

Tailored exclusively for Telephone & Data Systems, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its market position and profitability.

A concise Porter's Five Forces snapshot for Telephone & Data Systems—quickly spot where competitive pressure eases and prioritize strategic moves to protect margins.

Customers Bargaining Power

Low Switching Costs in Wireless Services

High Price Sensitivity in Rural Markets

Demand for High-Speed Symmetrical Broadband

Consumer expectations now favor symmetrical gigabit-class broadband for remote work and 4K/8K streaming; surveys in 2024 show 62% of US households rate upload speed as critical. In TDS Telecom markets, fiber adoption rose 18% YoY in 2024, making fiber-grade service a baseline demand. That shift strengthens buyer leverage: customers push for upgrades from copper/DSL and will switch to the first reliable fiber entrant in their neighborhood.

Availability of Alternative Service Providers

Availability of Alternative Service Providers weakens TDS’s customer bargaining power: national cable giants (Comcast, Charter) and satellite providers (Viasat, HughesNet) plus fiber overbuilders expanded options, letting customers demand lower prices or promos; US fixed broadband competition rose—FCC reported 2024 that 94% of households had two+ providers, up from 88% in 2018.

- Multiple rivals: cable, fiber, satellite

- 94% US homes have 2+ providers (FCC 2024)

- Fiber footprint growth through 2025 erodes regional monopolies

Enterprise and Wholesale Negotiation Leverage

Large enterprise and government clients account for a meaningful share of TDS revenue and wield strong leverage: in 2024 approximately 30% of U.S. commercial telecom spend flowed through RFP-driven contracts, pressuring margins.

These buyers run formal bids for managed services, hosted VoIP, and data center space, forcing TDS to offer deep discounts and tailored SLAs to secure multi-year deals, which can cut EBITDA margins by 200–400 basis points on those accounts.

TDS margin squeeze: high buyer power, $44 ARPU, unlocked phones & fierce broadband choice

| Metric | Value |

|---|---|

| ARPU (2024) | $44.20 |

| Homes w/2+ providers (2024) | 94% |

| Unlocked handsets (2025) | 70% |

| Portability growth (2024–25) | +8% |

Full Version Awaits

Telephone & Data Systems Porter's Five Forces Analysis

This preview shows the exact Telephone & Data Systems Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy. You're looking at the actual, professionally written analysis file; once you complete your purchase, you’ll get instant access to this exact document. No mockups or samples—what you see is what you’ll be able to download after payment.