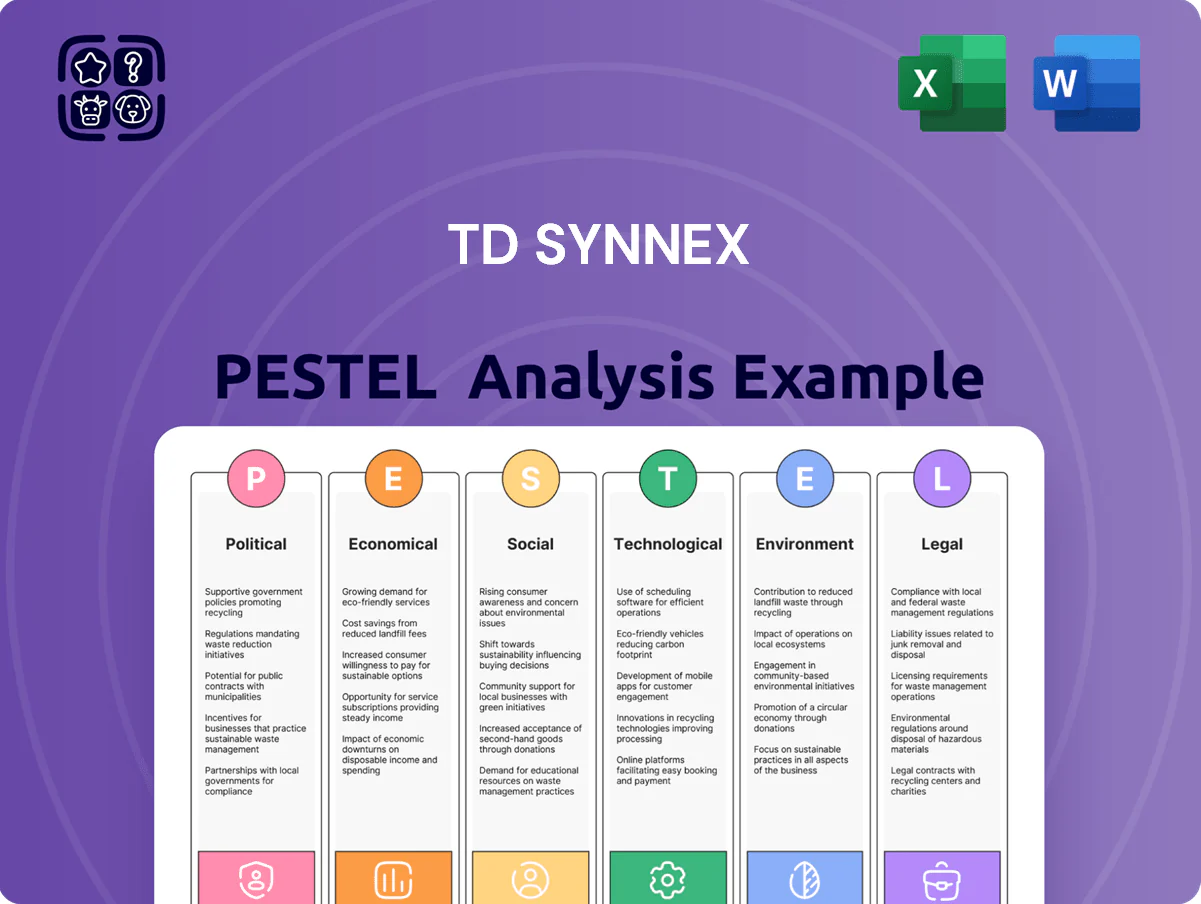

TD SYNNEX PESTLE Analysis

Your Competitive Advantage Starts with This Report

Get a sharp view of TD SYNNEX’s external landscape—our concise PESTLE highlights political, economic, social, technological, legal, and environmental forces shaping its strategy and risk profile; ideal for investors and strategists. Purchase the full PESTLE to unlock detailed, actionable insights, charts, and editable templates you can use immediately to inform decisions and spot opportunities.

Political factors

Geopolitical Trade Tensions

The US-China trade friction forces TD SYNNEX to keep supply chains agile; in 2024 the company reported supply-chain related cost pressures contributing to a 1.8% decline in gross margin, prompting shifts in sourcing and inventory strategies.

Tariffs and export controls on high-end semiconductors and networking gear—affecting vendors that supply ~35% of enterprise product revenue—drive continuous reassessment of vendor partnerships and logistics corridors.

Balancing compliance with US export rules and Chinese market access is critical to maintain product availability for TD SYNNEX’s $57.7bn FY2024 revenue stream while avoiding fines and shipment delays.

Government Digital Infrastructure Incentives

Many North American and European governments allocated over $120 billion in 2024–2025 for digital infrastructure upgrades; TD SYNNEX stands to gain as these programs boost demand for networking hardware and cloud services the company distributes.

Public funding increases procurement of switches, routers and cloud solutions—segments where TD SYNNEX reported $58.3 billion in FY2024 distribution revenue—heightening opportunity for margin-rich public-sector deals.

Strategic alignment with procurement cycles is essential: government IT contracts represented about 12–15% of enterprise IT spend in 2025, and timely bid positioning through 2026 will be key to capturing high-value, multi-year agreements.

Global Sanctions and Export Controls

Expansion of international sanctions and export controls forces TD SYNNEX to invest in advanced compliance systems to prevent unauthorized transfer of sensitive tech; global sanctions filings rose 24% in 2024, increasing due-diligence costs. Political instability in Eastern Europe and parts of Asia has produced rapidly changing restrictions, with over 30 new controls since 2022 affecting supply chains. Noncompliance risks include fines—recent tech-sector penalties exceeded $2.1 billion in 2023—and material reputational damage that could hit revenue and partner trust.

National Security and Trusted Vendor Lists

Western governments have increased trusted‑vendor lists, restricting some foreign vendors in critical infrastructure; US Executive Order and EU rules have expanded procurement security since 2023, affecting supply choices for distributors.

TD SYNNEX must align its vendor portfolio to meet regional security criteria—public sector sales comprised about 18% of global IT distribution revenue in 2024—shaping product prioritization and go‑to‑market efforts.

- Trusted‑vendor rules rising post‑2023

- Public sector ~18% of distributor revenue (2024)

- Portfolio curation required for regional compliance

- Influences brand prioritization for enterprise/public deals

Taxation Policy and Corporate Rates

- 2024 revenue $56.5B; effective tax rate sensitivity from global minimum tax proposals

- Digital services tax debates add volatility to cross-border pricing and compliance costs

- Active legislative monitoring required to preserve margins and investor trust

TD SYNNEX faces margin squeeze, vendor & geopolitical risks despite public‑sector tailwinds

US-China trade friction, tariffs and export controls raised supply‑chain costs, contributing to a 1.8% gross‑margin decline in 2024; FY2024 revenue ~$57.7B (distribution ~$58.3B in some reports) ties TD SYNNEX to vendor/geography risk. Government digital programs ($120B+ 2024–25) boost public‑sector demand (~18% of distributor revenue), while rising sanctions, trusted‑vendor rules and global minimum tax proposals increase compliance and tax planning costs.

| Metric | Value |

|---|---|

| FY2024 Revenue | $57.7B |

| Public‑sector share | ~18% |

| Gross margin impact (2024) | -1.8% |

| Digital infra funding (2024–25) | $120B+ |

What is included in the product

Explores how macro-environmental factors uniquely affect TD SYNNEX across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify strategic threats and opportunities.

A concise, visually segmented TD SYNNEX PESTLE summary that eases meeting prep and slide inclusion, letting teams quickly assess external risks and market positioning.

Economic factors

Interest Rate and Financing Costs

As a high-volume distributor, TD SYNNEX depends on credit facilities—inventory financing and vendor payables—so its interest expense rose as US Federal Reserve rates climbed to ~5.25–5.50% by late 2024, increasing borrowing costs and compressing margins.

Higher rates also tighten affordability for solution providers; TD SYNNEX reported net debt of about $6.8B in FY2024, making disciplined working capital management essential amid central bank policy shifts through 2025.

Currency Exchange Rate Volatility

Operating across 100+ countries, TD SYNNEX faces FX translation risk as international revenues are converted to USD; in FY2024 roughly 45% of revenue was non‑USD, so a 5% fall in the euro, yen or pound could swing reported revenue by hundreds of millions. Sharp moves in EUR/JPY/GBP have historically created +/-2–4% impacts on margins. Active hedging programs remain central to mitigate these non‑operational swings.

Shift from CAPEX to OPEX Models

The shift from CAPEX to OPEX—subscriptions and cloud—reduces large upfront hardware buys, altering revenue recognition for distributors; global SaaS spend reached about $214 billion in 2024, up ~16% YoY, driving distributor mix changes.

TD SYNNEX expanded cloud and SaaS offerings, reflected in higher recurring revenue (services and software contributed roughly 30% of 2024 revenue), aligning with customer OPEX preferences.

This yields more predictable long-term cash flow but forces TD SYNNEX to realign sales incentives and invest in recurring-revenue enablement, as subscription gross margins and churn metrics now drive performance.

Inflationary Pressure on Logistics

Persistent inflation in fuel, labor, and warehouse costs—U.S. diesel up ~18% in 2024 y/y and warehouse rents rising ~6–9% in major markets—squeezes TD SYNNEX’s thin IT-distribution margins, forcing either absorption or passthrough of higher unit costs.

TD SYNNEX must exploit scale and operational efficiency—company reported 2024 gross margin ~8%—to remain competitive while protecting profitability.

Ongoing investment in automation, robotics, and route optimization (reducing transport costs 5–15% in peers) is required to offset rising physical-goods movement expenses.

- Diesel +18% (2024 y/y)

- Warehouse rents +6–9%

- Gross margin ~8% (2024)

- Automation can cut transport costs 5–15%

Emerging Market Growth Potential

While mature markets offer stability, TD SYNNEX can tap emerging regions where IT spending is growing rapidly—IDC projected 2025 emerging market IT spend CAGR ~7.8% vs global ~4.5%, offering scale for solutions and services.

The company targets developing economies undergoing digital transformation and enterprise build-out; e.g., APAC emerging markets saw cloud spend rise ~22% in 2024, creating distribution and service demand.

Success requires nuanced understanding of local GDP per capita, currency volatility, and purchasing power—many target markets have PPP-adjusted growth of 3–6% annually but wide income dispersion.

- IDC: 2025 emerging IT spend CAGR ~7.8%

- APAC emerging cloud growth ~22% in 2024

- Target markets PPP growth 3–6% with high income dispersion

High debt, FX exposure and slim 8% gross margin force shift to SaaS and efficiencies

Higher rates raised borrowing costs (Fed funds ~5.25–5.50% late-2024), net debt ~ $6.8B (FY2024) and compressed margins; FX risk material with ~45% non‑USD revenue; shift to OPEX/SaaS (services/software ~30% of 2024 revenue) increases recurring cash flow but lowers upfront hardware sales; inflationary logistics/warehouse costs and ~8% gross margin force efficiency investments.

| Metric | Value |

|---|---|

| Net debt (FY2024) | $6.8B |

| Non‑USD revenue | ~45% |

| Services/software | ~30% rev |

| Gross margin | ~8% |

Preview Before You Purchase

TD SYNNEX PESTLE Analysis

The preview shown here is the exact TD SYNNEX PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content and structure visible in this sample match the downloadable file you’ll get immediately after checkout, with no placeholders or teasers. Don’t just imagine the report: what you see is the finished product you’ll own and can apply right away.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Get a sharp view of TD SYNNEX’s external landscape—our concise PESTLE highlights political, economic, social, technological, legal, and environmental forces shaping its strategy and risk profile; ideal for investors and strategists. Purchase the full PESTLE to unlock detailed, actionable insights, charts, and editable templates you can use immediately to inform decisions and spot opportunities.

Political factors

Geopolitical Trade Tensions

The US-China trade friction forces TD SYNNEX to keep supply chains agile; in 2024 the company reported supply-chain related cost pressures contributing to a 1.8% decline in gross margin, prompting shifts in sourcing and inventory strategies.

Tariffs and export controls on high-end semiconductors and networking gear—affecting vendors that supply ~35% of enterprise product revenue—drive continuous reassessment of vendor partnerships and logistics corridors.

Balancing compliance with US export rules and Chinese market access is critical to maintain product availability for TD SYNNEX’s $57.7bn FY2024 revenue stream while avoiding fines and shipment delays.

Government Digital Infrastructure Incentives

Many North American and European governments allocated over $120 billion in 2024–2025 for digital infrastructure upgrades; TD SYNNEX stands to gain as these programs boost demand for networking hardware and cloud services the company distributes.

Public funding increases procurement of switches, routers and cloud solutions—segments where TD SYNNEX reported $58.3 billion in FY2024 distribution revenue—heightening opportunity for margin-rich public-sector deals.

Strategic alignment with procurement cycles is essential: government IT contracts represented about 12–15% of enterprise IT spend in 2025, and timely bid positioning through 2026 will be key to capturing high-value, multi-year agreements.

Global Sanctions and Export Controls

Expansion of international sanctions and export controls forces TD SYNNEX to invest in advanced compliance systems to prevent unauthorized transfer of sensitive tech; global sanctions filings rose 24% in 2024, increasing due-diligence costs. Political instability in Eastern Europe and parts of Asia has produced rapidly changing restrictions, with over 30 new controls since 2022 affecting supply chains. Noncompliance risks include fines—recent tech-sector penalties exceeded $2.1 billion in 2023—and material reputational damage that could hit revenue and partner trust.

National Security and Trusted Vendor Lists

Western governments have increased trusted‑vendor lists, restricting some foreign vendors in critical infrastructure; US Executive Order and EU rules have expanded procurement security since 2023, affecting supply choices for distributors.

TD SYNNEX must align its vendor portfolio to meet regional security criteria—public sector sales comprised about 18% of global IT distribution revenue in 2024—shaping product prioritization and go‑to‑market efforts.

- Trusted‑vendor rules rising post‑2023

- Public sector ~18% of distributor revenue (2024)

- Portfolio curation required for regional compliance

- Influences brand prioritization for enterprise/public deals

Taxation Policy and Corporate Rates

- 2024 revenue $56.5B; effective tax rate sensitivity from global minimum tax proposals

- Digital services tax debates add volatility to cross-border pricing and compliance costs

- Active legislative monitoring required to preserve margins and investor trust

TD SYNNEX faces margin squeeze, vendor & geopolitical risks despite public‑sector tailwinds

US-China trade friction, tariffs and export controls raised supply‑chain costs, contributing to a 1.8% gross‑margin decline in 2024; FY2024 revenue ~$57.7B (distribution ~$58.3B in some reports) ties TD SYNNEX to vendor/geography risk. Government digital programs ($120B+ 2024–25) boost public‑sector demand (~18% of distributor revenue), while rising sanctions, trusted‑vendor rules and global minimum tax proposals increase compliance and tax planning costs.

| Metric | Value |

|---|---|

| FY2024 Revenue | $57.7B |

| Public‑sector share | ~18% |

| Gross margin impact (2024) | -1.8% |

| Digital infra funding (2024–25) | $120B+ |

What is included in the product

Explores how macro-environmental factors uniquely affect TD SYNNEX across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify strategic threats and opportunities.

A concise, visually segmented TD SYNNEX PESTLE summary that eases meeting prep and slide inclusion, letting teams quickly assess external risks and market positioning.

Economic factors

Interest Rate and Financing Costs

As a high-volume distributor, TD SYNNEX depends on credit facilities—inventory financing and vendor payables—so its interest expense rose as US Federal Reserve rates climbed to ~5.25–5.50% by late 2024, increasing borrowing costs and compressing margins.

Higher rates also tighten affordability for solution providers; TD SYNNEX reported net debt of about $6.8B in FY2024, making disciplined working capital management essential amid central bank policy shifts through 2025.

Currency Exchange Rate Volatility

Operating across 100+ countries, TD SYNNEX faces FX translation risk as international revenues are converted to USD; in FY2024 roughly 45% of revenue was non‑USD, so a 5% fall in the euro, yen or pound could swing reported revenue by hundreds of millions. Sharp moves in EUR/JPY/GBP have historically created +/-2–4% impacts on margins. Active hedging programs remain central to mitigate these non‑operational swings.

Shift from CAPEX to OPEX Models

The shift from CAPEX to OPEX—subscriptions and cloud—reduces large upfront hardware buys, altering revenue recognition for distributors; global SaaS spend reached about $214 billion in 2024, up ~16% YoY, driving distributor mix changes.

TD SYNNEX expanded cloud and SaaS offerings, reflected in higher recurring revenue (services and software contributed roughly 30% of 2024 revenue), aligning with customer OPEX preferences.

This yields more predictable long-term cash flow but forces TD SYNNEX to realign sales incentives and invest in recurring-revenue enablement, as subscription gross margins and churn metrics now drive performance.

Inflationary Pressure on Logistics

Persistent inflation in fuel, labor, and warehouse costs—U.S. diesel up ~18% in 2024 y/y and warehouse rents rising ~6–9% in major markets—squeezes TD SYNNEX’s thin IT-distribution margins, forcing either absorption or passthrough of higher unit costs.

TD SYNNEX must exploit scale and operational efficiency—company reported 2024 gross margin ~8%—to remain competitive while protecting profitability.

Ongoing investment in automation, robotics, and route optimization (reducing transport costs 5–15% in peers) is required to offset rising physical-goods movement expenses.

- Diesel +18% (2024 y/y)

- Warehouse rents +6–9%

- Gross margin ~8% (2024)

- Automation can cut transport costs 5–15%

Emerging Market Growth Potential

While mature markets offer stability, TD SYNNEX can tap emerging regions where IT spending is growing rapidly—IDC projected 2025 emerging market IT spend CAGR ~7.8% vs global ~4.5%, offering scale for solutions and services.

The company targets developing economies undergoing digital transformation and enterprise build-out; e.g., APAC emerging markets saw cloud spend rise ~22% in 2024, creating distribution and service demand.

Success requires nuanced understanding of local GDP per capita, currency volatility, and purchasing power—many target markets have PPP-adjusted growth of 3–6% annually but wide income dispersion.

- IDC: 2025 emerging IT spend CAGR ~7.8%

- APAC emerging cloud growth ~22% in 2024

- Target markets PPP growth 3–6% with high income dispersion

High debt, FX exposure and slim 8% gross margin force shift to SaaS and efficiencies

Higher rates raised borrowing costs (Fed funds ~5.25–5.50% late-2024), net debt ~ $6.8B (FY2024) and compressed margins; FX risk material with ~45% non‑USD revenue; shift to OPEX/SaaS (services/software ~30% of 2024 revenue) increases recurring cash flow but lowers upfront hardware sales; inflationary logistics/warehouse costs and ~8% gross margin force efficiency investments.

| Metric | Value |

|---|---|

| Net debt (FY2024) | $6.8B |

| Non‑USD revenue | ~45% |

| Services/software | ~30% rev |

| Gross margin | ~8% |

Preview Before You Purchase

TD SYNNEX PESTLE Analysis

The preview shown here is the exact TD SYNNEX PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content and structure visible in this sample match the downloadable file you’ll get immediately after checkout, with no placeholders or teasers. Don’t just imagine the report: what you see is the finished product you’ll own and can apply right away.