TE Connectivity PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, supply‑chain dynamics, and rapid tech innovation are reshaping TE Connectivity’s prospects in our concise PESTLE snapshot—then unlock the full, actionable analysis to inform investment and strategy decisions. Purchase the complete report for detailed risks, opportunities, and ready‑to‑use insights.

Political factors

Geopolitical Trade Tensions

Trade disputes between the U.S. and China directly strain TE Connectivity’s supply chain and manufacturing footprint, with tariffs and export controls contributing to a ~2–4% margin pressure on comparable electronics peers in 2023–2024 and potential incremental costs for TE’s $14.8B 2024 revenue base. Significant operations in both markets expose the firm to duties and licensing risks on high-tech components, raising unit costs and capex relocation expenses. Management must navigate shifting trade alliances and regional protectionism to retain access to key customers and mitigate supply disruptions.

Government Subsidies for Electrification

Political initiatives such as the U.S. Inflation Reduction Act—allocating roughly $369 billion for clean energy through 2031—and the EU Green Deal mobilizing €1 trillion over the decade, drive EV infrastructure demand, boosting orders for TE Connectivity’s connectors and sensors.

These subsidies and tax credits for manufacturers and consumers accelerate adoption of TE’s automotive and energy products; TE reported 2024 sales of $18.6B, with EV-related content growth outpacing core by mid-single digits.

Rising government spending on grid modernization and renewables—estimated $1.6T global annual investment needed by 2030—expands addressable markets for TE’s power-distribution and renewable-integration solutions.

National Security and Data Sovereignty

Rising political scrutiny of data networks and comms infrastructure—25% of G20 countries updated telecom security rules in 2024—slows 5G and fiber rollouts and raises compliance costs for suppliers like TE Connectivity.

Since 2023 over 40 governments tightened rules on hardware origin to curb espionage, affecting supply chains and procurement for critical infrastructure.

TE must certify components to meet evolving standards (e.g., equipment-origin bans, secure-supply mandates) to retain access to government-linked contracts representing a significant portion of global infrastructure spend.

Regional Stability in Manufacturing Hubs

Political instability in manufacturing hubs can cause labor stoppages and supply-chain delays for TE Connectivity, which reported 2025 revenue of $15.7 billion and relies on ~30 global manufacturing sites; disruptions in a single region could shave several percentage points off monthly output.

Geographic diversification across Americas, EMEA and APAC mitigates localized risk, yet sudden governance shifts—seen in 2024 trade restrictions affecting electronics components—still threaten lead times and costs.

Continuous monitoring of emerging-market political climates is critical to preserve resilience in a global delivery model and limit exposure to bottlenecks that could inflate COGS and compress margins.

- ~30 global plants; $15.7B 2025 revenue

- Diversification reduces but does not eliminate localized risk

- 2024 trade restrictions highlighted vulnerability in component sourcing

- Ongoing political monitoring essential to protect margins

Corporate Tax Policy Changes

Changes in international tax laws, including the OECD/G20 Pillar Two global minimum tax set at 15% (effective for many jurisdictions from 2023–2024), can compress TE Connectivity’s effective tax rate and impact cash flow timing.

Headquartered in Switzerland with 2024 revenue of $16.3B, TE is exposed to shifts in corporate tax rates and repatriation rules that affect cross-border earnings and deferred tax assets.

Financial strategists must model altered after-tax returns and adjust capital allocation; for example, a 1 percentage-point tax rise could reduce net income by roughly $30–50M annually based on 2024 margins.

- OECD Pillar Two 15% global minimum tax (effective 2023–2024)

- 2024 revenue $16.3B; sensitivity to 1ppt tax = ~$30–50M NI impact

- Exposure due to Swiss HQ and extensive global operations

- Repatriation rule changes affect cash repatriation and capital planning

Geopolitics, taxes and green subsidies squeeze margins but fuel EV-driven growth

Political risks include U.S.–China trade tensions imposing ~2–4% margin pressure on electronics peers (2023–24), OECD Pillar Two 15% tax (effective 2023–24) impacting TE’s after-tax returns (~$30–50M per 1ppt tax lift on 2024 margins), government clean-energy subsidies (IRA $369B) boosting EV demand, and tightened hardware-origin rules in 40+ countries raising compliance and sourcing costs.

| Metric | Value |

|---|---|

| 2024 revenue | $16.3B |

| 2025 revenue | $15.7B |

| Global plants | ~30 |

| EV content growth | mid-single digits |

What is included in the product

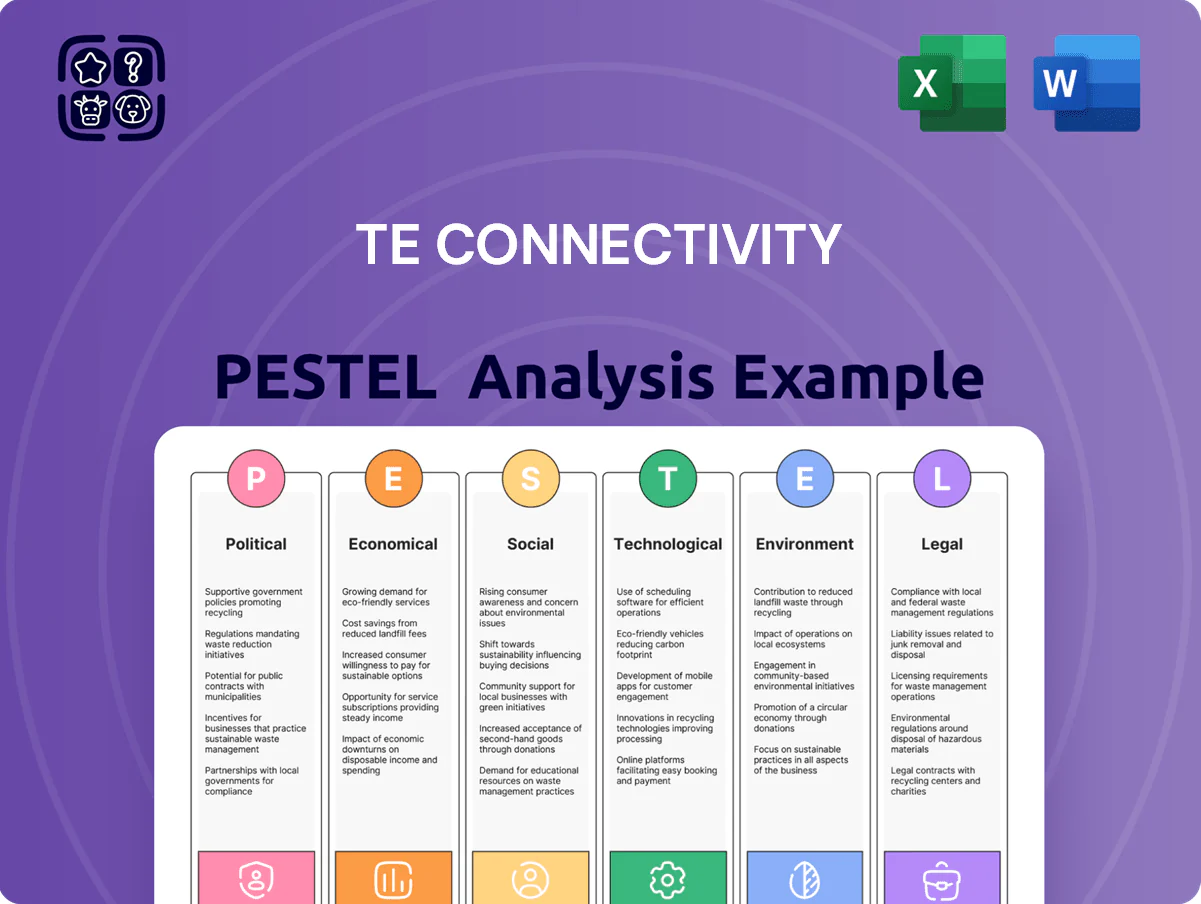

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact TE Connectivity, presenting data-backed trends and region- and industry-relevant examples to identify strategic risks and opportunities.

Condenses TE Connectivity's PESTLE insights into a compact, shareable brief that eases risk discussion and strategic alignment across teams during meetings or presentations.

Economic factors

Global Industrial Production Trends

The demand for TE Connectivity’s sensors and connectors tracks global industrial production, with world manufacturing output falling 1.8% in 2023 but rebounding 2.1% year-over-year in 2024, influencing order volumes for cohorts like automotive and aerospace.

Economic slowdowns in auto and aerospace—where TE derives an estimated 30% of revenue exposure—can reduce orders; global light-vehicle production declined 2% in 2023, pressuring component demand.

Conversely, industrial expansion boosts volume: global capex rose about 4.5% in 2024 as firms upgraded machinery and infrastructure, supporting TE’s sales growth and margin recovery.

Fluctuations in Raw Material Costs

TE Connectivity depends on copper, gold and plastics; copper rose ~35% from 2020‑2023 while Brent‑linked resin costs spiked ~20% in 2021‑22, pressuring margins if pass‑through fails.

Volatility in these commodities can compress gross margin—TE reported 2024 gross margin 29.8%—making pricing power critical.

TE mitigates risk via hedging and multi‑year supplier contracts; in 2023 ~40% of key purchases were under long‑term agreements per filings.

Currency Exchange Rate Volatility

As a U.S. dollar–reported company with ~70% revenue from outside the U.S., TE Connectivity faces material FX risk; 2025 sensitivity estimates showed a 1% USD strengthening could reduce reported revenue by roughly $50–70 million. Movements in the euro, renminbi and yen directly affect local pricing and margins, especially in Europe and APAC. Management reported using derivatives and natural hedges—net FX contracts and local sourcing—to limit translation and transaction exposure, reducing quarterly EBIT volatility in 2024–2025.

Interest Rate Environment

The prevailing interest rate environment affects TE Connectivity’s borrowing costs and its customers’ capital spending; with the US Fed funds rate at ~5.25–5.50% in 2024–2025, higher rates raise debt service and can constrain OEM and infrastructure capex, reducing demand for connectors and sensors.

Lower rates historically spur capital-heavy investments in automotive electrification and industrial automation, sectors that drive TE’s sales—TE reported net sales of $17.6B in FY2024, sensitive to capex cycles.

- Higher rates (Fed 5.25–5.50% 2024–25) → higher cost of debt, weaker customer capex

- Slower infrastructure/auto purchases → lower demand for TE components

- Low-rate periods → increased capital projects, benefiting TE’s high-end connectivity

Labor Market Dynamics and Inflation

- Wage inflation ~6–8% (2024) increases COGS

- FY2024 capex $1.2B toward automation

- Skilled labor vacancy ~4.5% constrains scaling

TE weathers cycles: 2024 margins hold amid commodity, wage and FX pressures

Economic cycles drive TE volumes—manufacturing fell 1.8% in 2023 then +2.1% in 2024; auto output -2% (2023). Commodity inflation (copper +35% 2020–23) and wage inflation ~6–8% (2024) pressure margins; TE GM 29.8% (2024), net sales $17.6B, capex $1.2B. FX risk: ~70% revenue ex‑US; 1% USD strength ≈ $50–70M revenue impact; Fed 5.25–5.50% raises funding costs.

| Metric | Value |

|---|---|

| Net sales FY2024 | $17.6B |

| Gross margin 2024 | 29.8% |

| Capex FY2024 | $1.2B |

| Copper change 2020–23 | +35% |

| Wage inflation 2024 | 6–8% |

| USD revenue exposure | ~70% ex‑US |

| FX sensitivity (1% USD) | $50–70M rev |

Same Document Delivered

TE Connectivity PESTLE Analysis

The preview shown here is the exact TE Connectivity PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders or teasers—this is the real, finished file you’ll own upon checkout. What you see is what you’ll be working with.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, supply‑chain dynamics, and rapid tech innovation are reshaping TE Connectivity’s prospects in our concise PESTLE snapshot—then unlock the full, actionable analysis to inform investment and strategy decisions. Purchase the complete report for detailed risks, opportunities, and ready‑to‑use insights.

Political factors

Geopolitical Trade Tensions

Trade disputes between the U.S. and China directly strain TE Connectivity’s supply chain and manufacturing footprint, with tariffs and export controls contributing to a ~2–4% margin pressure on comparable electronics peers in 2023–2024 and potential incremental costs for TE’s $14.8B 2024 revenue base. Significant operations in both markets expose the firm to duties and licensing risks on high-tech components, raising unit costs and capex relocation expenses. Management must navigate shifting trade alliances and regional protectionism to retain access to key customers and mitigate supply disruptions.

Government Subsidies for Electrification

Political initiatives such as the U.S. Inflation Reduction Act—allocating roughly $369 billion for clean energy through 2031—and the EU Green Deal mobilizing €1 trillion over the decade, drive EV infrastructure demand, boosting orders for TE Connectivity’s connectors and sensors.

These subsidies and tax credits for manufacturers and consumers accelerate adoption of TE’s automotive and energy products; TE reported 2024 sales of $18.6B, with EV-related content growth outpacing core by mid-single digits.

Rising government spending on grid modernization and renewables—estimated $1.6T global annual investment needed by 2030—expands addressable markets for TE’s power-distribution and renewable-integration solutions.

National Security and Data Sovereignty

Rising political scrutiny of data networks and comms infrastructure—25% of G20 countries updated telecom security rules in 2024—slows 5G and fiber rollouts and raises compliance costs for suppliers like TE Connectivity.

Since 2023 over 40 governments tightened rules on hardware origin to curb espionage, affecting supply chains and procurement for critical infrastructure.

TE must certify components to meet evolving standards (e.g., equipment-origin bans, secure-supply mandates) to retain access to government-linked contracts representing a significant portion of global infrastructure spend.

Regional Stability in Manufacturing Hubs

Political instability in manufacturing hubs can cause labor stoppages and supply-chain delays for TE Connectivity, which reported 2025 revenue of $15.7 billion and relies on ~30 global manufacturing sites; disruptions in a single region could shave several percentage points off monthly output.

Geographic diversification across Americas, EMEA and APAC mitigates localized risk, yet sudden governance shifts—seen in 2024 trade restrictions affecting electronics components—still threaten lead times and costs.

Continuous monitoring of emerging-market political climates is critical to preserve resilience in a global delivery model and limit exposure to bottlenecks that could inflate COGS and compress margins.

- ~30 global plants; $15.7B 2025 revenue

- Diversification reduces but does not eliminate localized risk

- 2024 trade restrictions highlighted vulnerability in component sourcing

- Ongoing political monitoring essential to protect margins

Corporate Tax Policy Changes

Changes in international tax laws, including the OECD/G20 Pillar Two global minimum tax set at 15% (effective for many jurisdictions from 2023–2024), can compress TE Connectivity’s effective tax rate and impact cash flow timing.

Headquartered in Switzerland with 2024 revenue of $16.3B, TE is exposed to shifts in corporate tax rates and repatriation rules that affect cross-border earnings and deferred tax assets.

Financial strategists must model altered after-tax returns and adjust capital allocation; for example, a 1 percentage-point tax rise could reduce net income by roughly $30–50M annually based on 2024 margins.

- OECD Pillar Two 15% global minimum tax (effective 2023–2024)

- 2024 revenue $16.3B; sensitivity to 1ppt tax = ~$30–50M NI impact

- Exposure due to Swiss HQ and extensive global operations

- Repatriation rule changes affect cash repatriation and capital planning

Geopolitics, taxes and green subsidies squeeze margins but fuel EV-driven growth

Political risks include U.S.–China trade tensions imposing ~2–4% margin pressure on electronics peers (2023–24), OECD Pillar Two 15% tax (effective 2023–24) impacting TE’s after-tax returns (~$30–50M per 1ppt tax lift on 2024 margins), government clean-energy subsidies (IRA $369B) boosting EV demand, and tightened hardware-origin rules in 40+ countries raising compliance and sourcing costs.

| Metric | Value |

|---|---|

| 2024 revenue | $16.3B |

| 2025 revenue | $15.7B |

| Global plants | ~30 |

| EV content growth | mid-single digits |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact TE Connectivity, presenting data-backed trends and region- and industry-relevant examples to identify strategic risks and opportunities.

Condenses TE Connectivity's PESTLE insights into a compact, shareable brief that eases risk discussion and strategic alignment across teams during meetings or presentations.

Economic factors

Global Industrial Production Trends

The demand for TE Connectivity’s sensors and connectors tracks global industrial production, with world manufacturing output falling 1.8% in 2023 but rebounding 2.1% year-over-year in 2024, influencing order volumes for cohorts like automotive and aerospace.

Economic slowdowns in auto and aerospace—where TE derives an estimated 30% of revenue exposure—can reduce orders; global light-vehicle production declined 2% in 2023, pressuring component demand.

Conversely, industrial expansion boosts volume: global capex rose about 4.5% in 2024 as firms upgraded machinery and infrastructure, supporting TE’s sales growth and margin recovery.

Fluctuations in Raw Material Costs

TE Connectivity depends on copper, gold and plastics; copper rose ~35% from 2020‑2023 while Brent‑linked resin costs spiked ~20% in 2021‑22, pressuring margins if pass‑through fails.

Volatility in these commodities can compress gross margin—TE reported 2024 gross margin 29.8%—making pricing power critical.

TE mitigates risk via hedging and multi‑year supplier contracts; in 2023 ~40% of key purchases were under long‑term agreements per filings.

Currency Exchange Rate Volatility

As a U.S. dollar–reported company with ~70% revenue from outside the U.S., TE Connectivity faces material FX risk; 2025 sensitivity estimates showed a 1% USD strengthening could reduce reported revenue by roughly $50–70 million. Movements in the euro, renminbi and yen directly affect local pricing and margins, especially in Europe and APAC. Management reported using derivatives and natural hedges—net FX contracts and local sourcing—to limit translation and transaction exposure, reducing quarterly EBIT volatility in 2024–2025.

Interest Rate Environment

The prevailing interest rate environment affects TE Connectivity’s borrowing costs and its customers’ capital spending; with the US Fed funds rate at ~5.25–5.50% in 2024–2025, higher rates raise debt service and can constrain OEM and infrastructure capex, reducing demand for connectors and sensors.

Lower rates historically spur capital-heavy investments in automotive electrification and industrial automation, sectors that drive TE’s sales—TE reported net sales of $17.6B in FY2024, sensitive to capex cycles.

- Higher rates (Fed 5.25–5.50% 2024–25) → higher cost of debt, weaker customer capex

- Slower infrastructure/auto purchases → lower demand for TE components

- Low-rate periods → increased capital projects, benefiting TE’s high-end connectivity

Labor Market Dynamics and Inflation

- Wage inflation ~6–8% (2024) increases COGS

- FY2024 capex $1.2B toward automation

- Skilled labor vacancy ~4.5% constrains scaling

TE weathers cycles: 2024 margins hold amid commodity, wage and FX pressures

Economic cycles drive TE volumes—manufacturing fell 1.8% in 2023 then +2.1% in 2024; auto output -2% (2023). Commodity inflation (copper +35% 2020–23) and wage inflation ~6–8% (2024) pressure margins; TE GM 29.8% (2024), net sales $17.6B, capex $1.2B. FX risk: ~70% revenue ex‑US; 1% USD strength ≈ $50–70M revenue impact; Fed 5.25–5.50% raises funding costs.

| Metric | Value |

|---|---|

| Net sales FY2024 | $17.6B |

| Gross margin 2024 | 29.8% |

| Capex FY2024 | $1.2B |

| Copper change 2020–23 | +35% |

| Wage inflation 2024 | 6–8% |

| USD revenue exposure | ~70% ex‑US |

| FX sensitivity (1% USD) | $50–70M rev |

Same Document Delivered

TE Connectivity PESTLE Analysis

The preview shown here is the exact TE Connectivity PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders or teasers—this is the real, finished file you’ll own upon checkout. What you see is what you’ll be working with.