Tech Mahindra Porter's Five Forces Analysis

Don't Miss the Bigger Picture

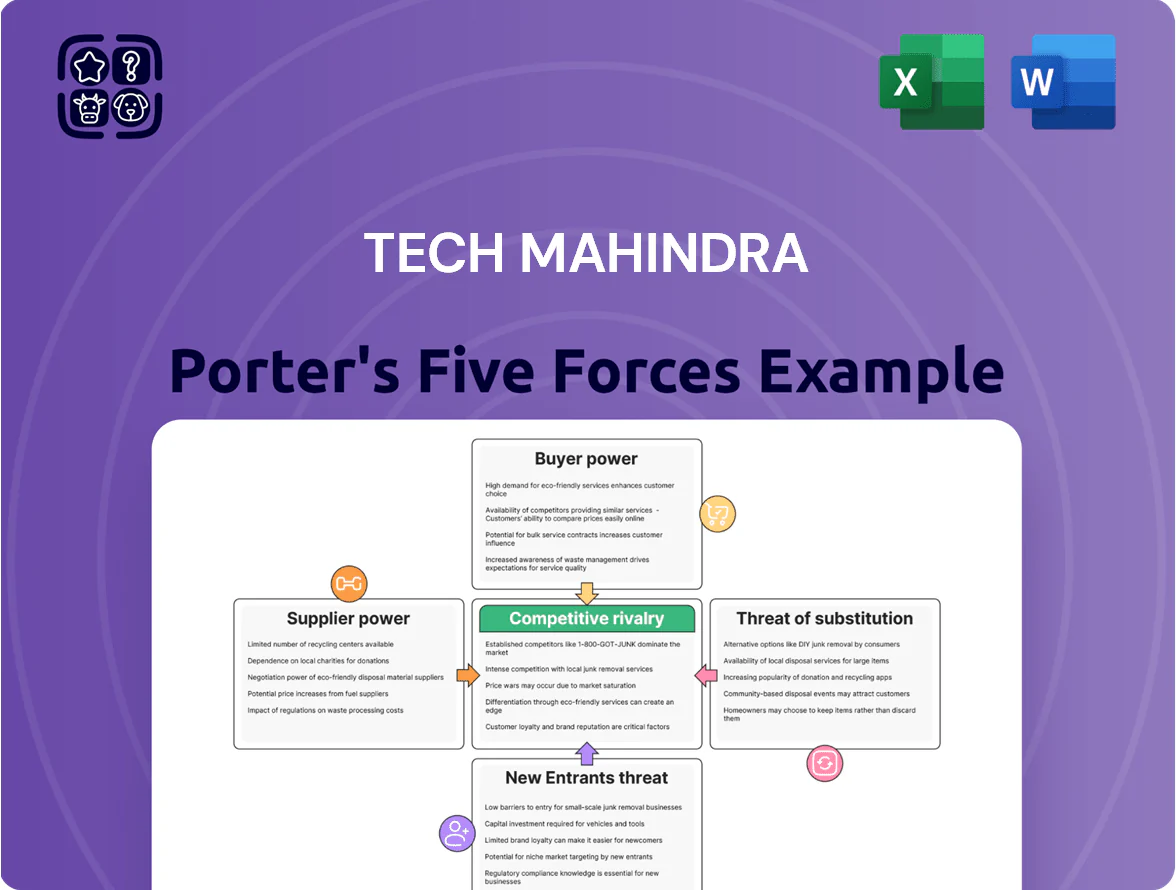

Tech Mahindra faces intense competitive rivalry, moderate buyer power due to large enterprise clients, supplier influence from niche tech vendors, a manageable threat of new entrants given scale requirements, and rising substitution risks from automation and cloud-native providers; this snapshot highlights key pressures but omits force-by-force ratings and strategic implications.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tech Mahindra’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Technical Talent

The primary suppliers for Tech Mahindra are specialized engineers in GenAI, 5G, and cybersecurity; by late 2025 the global shortage of senior-tier engineers (estimated 1.2M short in AI/ML roles per LinkedIn 2025 skills report) gives them strong bargaining power.

This drives wage inflation—Tech Mahindra reported 18% annual increase in employee costs in FY2024‑25—and forces heavy investment in retention, with upskilling budgets rising ~25% and hiring premiums up to 30% for niche skills.

Dependence on Hyperscale Cloud Providers

Tech Mahindra depends on AWS, Microsoft Azure, and Google Cloud for core cloud infrastructure, with hyperscalers accounting for an estimated 30–40% of its cloud-related spend in FY2024; this concentration gives suppliers strong bargaining power.

Hyperscalers set pricing, SLAs, and partner tiers that directly affect Tech Mahindra’s margins—AWS and Azure price increases in 2023–24 raised costs for many service providers by ~5–8%, pressuring operating margins.

Any adverse change in partnership tier or volume discounts can swing Tech Mahindra’s gross margins by several percentage points, so the company must negotiate favorable terms or diversify cloud stacks to protect profitability.

Rising Costs of Third-Party Software Licenses

Tech Mahindra relies on third-party enterprise software—SAP, Oracle, Microsoft—making vendors key suppliers; global SaaS spend rose 18% in 2024 to $237B, pushing vendor leverage.

With many vendors using subscription pricing and typical annual escalations of 5–8%, Tech Mahindra must absorb costs or raise client rates, squeezing margins; FY2024 gross margin was 23.6%.

Few dominant niche vendors create concentrated supplier power, limiting Tech Mahindra’s bargaining options and increasing price vulnerability.

Influence of Hardware and Semiconductor Manufacturers

For Tech Mahindra’s network services and 5G rollouts, hardware and semiconductor availability directly affect timelines and margins; global chip shortages raised telecom equipment lead times by ~30% in 2021–23 and still push component premiums of 5–15% in 2024.

Supply-chain volatility—e.g., 2023 saw semiconductor capital expenditure up 22% year-over-year—can force project delays and higher procurement costs, since a few global manufacturers (Qualcomm, Broadcom, Cisco suppliers) hold concentrated supply.

The concentrated supplier base gives moderate-to-high leverage: delayed deliveries often shift timeline risk to Tech Mahindra, increasing working capital needs and potential margin compression on large 5G contracts.

- Lead-time increases ~30% (2021–23)

- Component premiums 5–15% (2024)

- Chip capex +22% YoY (2023)

- Supplier concentration: few global OEMs

Impact of Global Labor Market Volatility

Volatility in the global labor market threatens Tech Mahindra’s delivery model because entry-level engineering graduates from India and delivery hubs supply ~60–70% of its onshore/offshore project staffing; a 2024 NASSCOM report showed a 12% drop in campus hiring yield versus 2019, raising cost-per-hire and ramp times.

Shifts in education quality, tighter migration visas (eg, US H-1B policy changes in 2023) or new hubs like Vietnam can raise wage bills and attrition, so Tech Mahindra must invest in reskilling, local hiring and higher campus engagement to keep large-scale project margins.

- 60–70% dependence on entry-level hires

- NASSCOM: 12% lower campus yield vs 2019 (2024)

- H-1B policy shifts increased offshore staffing by ~8% (2023)

- Mitigation: reskilling, local hiring, campus tie-ups

Supplier power (GenAI/5G/hyperscalers) squeezes margins via wage, cloud & component inflation

Suppliers (senior GenAI/5G engineers, hyperscalers, SAP/Oracle, semiconductors) exert moderate‑to‑high bargaining power, driving wage inflation (Tech Mahindra employee costs +18% FY2024‑25), cloud/vendor price pressure (hyperscaler spend 30–40%; cloud price rises 5–8% 2023–24) and component premiums (5–15% 2024), threatening margins (gross margin 23.6% FY2024).

| Metric | Value |

|---|---|

| Employee cost growth | +18% FY2024‑25 |

| Hyperscaler spend | 30–40% cloud spend |

| Cloud price impact | +5–8% (2023–24) |

| Component premiums | 5–15% (2024) |

| Gross margin | 23.6% FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Tech Mahindra, uncovering competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and strategic implications for pricing and profitability.

Compact Porter's Five Forces snapshot for Tech Mahindra—clarifies competitive pressures at a glance to speed strategic decisions.

Customers Bargaining Power

High Concentration in the Telecom Sector

Low Switching Costs for Standardized IT Services

In traditional IT maintenance and BPS (business process services), switching costs are low, so clients easily move among Tier‑1 and Tier‑2 vendors; globally, 2024 outsourcing churn rates hit ~18% annually, raising price pressure. Tech Mahindra faces dozens of rivals—Tata Consultancy Services, Cognizant, Wipro—forcing margin-sensitive bids: its FY2024 EBIT margin of 7.4% shows limited room to absorb price cuts. So Tech Mahindra must prove ongoing value and innovate to retain clients.

Demand for Outcome-Based Pricing Models

Proliferation of Multi-Vendor Strategies

Large enterprises increasingly use multi-vendor IT strategies to avoid vendor lock-in; Gartner reported in 2024 that 62% of CIOs had formal multi-sourcing policies, raising customer bargaining power versus single suppliers.

This lets buyers cherry-pick services and negotiate harder on pricing, SLAs, and renewals; Tech Mahindra frequently faces competition from other incumbents inside existing accounts, pressuring margins.

- 62% of CIOs had multi-sourcing policies (Gartner 2024)

- Higher churn risk at renewal, lower margin per deal

- Must win on value, not just incumbency

Increased Financial Literacy and Procurement Sophistication

Modern procurement teams use analytics to benchmark IT service costs against global peers, cutting information asymmetry and pressuring Tech Mahindra’s margins on routine outsourcing. Clients now negotiate SLAs using real-time market rates—Gartner estimated in 2024 that 62% of enterprise buyers used benchmarking platforms for IT sourcing. This shifts pricing power to buyers, forcing Tech Mahindra to compete on efficiency, outcome-based pricing, and value-added services.

- 62% of buyers use benchmarking (Gartner 2024)

- Routine task margins squeezed ~150–300 bps in 2023–24

- More SLAs tied to real-time KPIs and market indices

High telecom concentration, rising multi‑sourcing squeeze Tech Mahindra margins

| Metric | Value |

|---|---|

| Telecom revenue share FY2024 | 27% |

| EBIT margin FY2024 | 7.4% |

| CIOs with multi‑sourcing (Gartner 2024) | 62% |

| Outsourcing churn 2024 | ~18% |

| Deals outcome‑based by 2025 | 46% |

| Routine margin squeeze 2023–24 | 150–300 bps |

Full Version Awaits

Tech Mahindra Porter's Five Forces Analysis

This preview shows the exact Tech Mahindra Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, and once payment is completed you'll get instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Tech Mahindra faces intense competitive rivalry, moderate buyer power due to large enterprise clients, supplier influence from niche tech vendors, a manageable threat of new entrants given scale requirements, and rising substitution risks from automation and cloud-native providers; this snapshot highlights key pressures but omits force-by-force ratings and strategic implications.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tech Mahindra’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Specialized Technical Talent

The primary suppliers for Tech Mahindra are specialized engineers in GenAI, 5G, and cybersecurity; by late 2025 the global shortage of senior-tier engineers (estimated 1.2M short in AI/ML roles per LinkedIn 2025 skills report) gives them strong bargaining power.

This drives wage inflation—Tech Mahindra reported 18% annual increase in employee costs in FY2024‑25—and forces heavy investment in retention, with upskilling budgets rising ~25% and hiring premiums up to 30% for niche skills.

Dependence on Hyperscale Cloud Providers

Tech Mahindra depends on AWS, Microsoft Azure, and Google Cloud for core cloud infrastructure, with hyperscalers accounting for an estimated 30–40% of its cloud-related spend in FY2024; this concentration gives suppliers strong bargaining power.

Hyperscalers set pricing, SLAs, and partner tiers that directly affect Tech Mahindra’s margins—AWS and Azure price increases in 2023–24 raised costs for many service providers by ~5–8%, pressuring operating margins.

Any adverse change in partnership tier or volume discounts can swing Tech Mahindra’s gross margins by several percentage points, so the company must negotiate favorable terms or diversify cloud stacks to protect profitability.

Rising Costs of Third-Party Software Licenses

Tech Mahindra relies on third-party enterprise software—SAP, Oracle, Microsoft—making vendors key suppliers; global SaaS spend rose 18% in 2024 to $237B, pushing vendor leverage.

With many vendors using subscription pricing and typical annual escalations of 5–8%, Tech Mahindra must absorb costs or raise client rates, squeezing margins; FY2024 gross margin was 23.6%.

Few dominant niche vendors create concentrated supplier power, limiting Tech Mahindra’s bargaining options and increasing price vulnerability.

Influence of Hardware and Semiconductor Manufacturers

For Tech Mahindra’s network services and 5G rollouts, hardware and semiconductor availability directly affect timelines and margins; global chip shortages raised telecom equipment lead times by ~30% in 2021–23 and still push component premiums of 5–15% in 2024.

Supply-chain volatility—e.g., 2023 saw semiconductor capital expenditure up 22% year-over-year—can force project delays and higher procurement costs, since a few global manufacturers (Qualcomm, Broadcom, Cisco suppliers) hold concentrated supply.

The concentrated supplier base gives moderate-to-high leverage: delayed deliveries often shift timeline risk to Tech Mahindra, increasing working capital needs and potential margin compression on large 5G contracts.

- Lead-time increases ~30% (2021–23)

- Component premiums 5–15% (2024)

- Chip capex +22% YoY (2023)

- Supplier concentration: few global OEMs

Impact of Global Labor Market Volatility

Volatility in the global labor market threatens Tech Mahindra’s delivery model because entry-level engineering graduates from India and delivery hubs supply ~60–70% of its onshore/offshore project staffing; a 2024 NASSCOM report showed a 12% drop in campus hiring yield versus 2019, raising cost-per-hire and ramp times.

Shifts in education quality, tighter migration visas (eg, US H-1B policy changes in 2023) or new hubs like Vietnam can raise wage bills and attrition, so Tech Mahindra must invest in reskilling, local hiring and higher campus engagement to keep large-scale project margins.

- 60–70% dependence on entry-level hires

- NASSCOM: 12% lower campus yield vs 2019 (2024)

- H-1B policy shifts increased offshore staffing by ~8% (2023)

- Mitigation: reskilling, local hiring, campus tie-ups

Supplier power (GenAI/5G/hyperscalers) squeezes margins via wage, cloud & component inflation

Suppliers (senior GenAI/5G engineers, hyperscalers, SAP/Oracle, semiconductors) exert moderate‑to‑high bargaining power, driving wage inflation (Tech Mahindra employee costs +18% FY2024‑25), cloud/vendor price pressure (hyperscaler spend 30–40%; cloud price rises 5–8% 2023–24) and component premiums (5–15% 2024), threatening margins (gross margin 23.6% FY2024).

| Metric | Value |

|---|---|

| Employee cost growth | +18% FY2024‑25 |

| Hyperscaler spend | 30–40% cloud spend |

| Cloud price impact | +5–8% (2023–24) |

| Component premiums | 5–15% (2024) |

| Gross margin | 23.6% FY2024 |

What is included in the product

Tailored Porter's Five Forces analysis for Tech Mahindra, uncovering competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and strategic implications for pricing and profitability.

Compact Porter's Five Forces snapshot for Tech Mahindra—clarifies competitive pressures at a glance to speed strategic decisions.

Customers Bargaining Power

High Concentration in the Telecom Sector

Low Switching Costs for Standardized IT Services

In traditional IT maintenance and BPS (business process services), switching costs are low, so clients easily move among Tier‑1 and Tier‑2 vendors; globally, 2024 outsourcing churn rates hit ~18% annually, raising price pressure. Tech Mahindra faces dozens of rivals—Tata Consultancy Services, Cognizant, Wipro—forcing margin-sensitive bids: its FY2024 EBIT margin of 7.4% shows limited room to absorb price cuts. So Tech Mahindra must prove ongoing value and innovate to retain clients.

Demand for Outcome-Based Pricing Models

Proliferation of Multi-Vendor Strategies

Large enterprises increasingly use multi-vendor IT strategies to avoid vendor lock-in; Gartner reported in 2024 that 62% of CIOs had formal multi-sourcing policies, raising customer bargaining power versus single suppliers.

This lets buyers cherry-pick services and negotiate harder on pricing, SLAs, and renewals; Tech Mahindra frequently faces competition from other incumbents inside existing accounts, pressuring margins.

- 62% of CIOs had multi-sourcing policies (Gartner 2024)

- Higher churn risk at renewal, lower margin per deal

- Must win on value, not just incumbency

Increased Financial Literacy and Procurement Sophistication

Modern procurement teams use analytics to benchmark IT service costs against global peers, cutting information asymmetry and pressuring Tech Mahindra’s margins on routine outsourcing. Clients now negotiate SLAs using real-time market rates—Gartner estimated in 2024 that 62% of enterprise buyers used benchmarking platforms for IT sourcing. This shifts pricing power to buyers, forcing Tech Mahindra to compete on efficiency, outcome-based pricing, and value-added services.

- 62% of buyers use benchmarking (Gartner 2024)

- Routine task margins squeezed ~150–300 bps in 2023–24

- More SLAs tied to real-time KPIs and market indices

High telecom concentration, rising multi‑sourcing squeeze Tech Mahindra margins

| Metric | Value |

|---|---|

| Telecom revenue share FY2024 | 27% |

| EBIT margin FY2024 | 7.4% |

| CIOs with multi‑sourcing (Gartner 2024) | 62% |

| Outsourcing churn 2024 | ~18% |

| Deals outcome‑based by 2025 | 46% |

| Routine margin squeeze 2023–24 | 150–300 bps |

Full Version Awaits

Tech Mahindra Porter's Five Forces Analysis

This preview shows the exact Tech Mahindra Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable, and once payment is completed you'll get instant access to this identical file.