technotrans Porter's Five Forces Analysis

From Overview to Strategy Blueprint

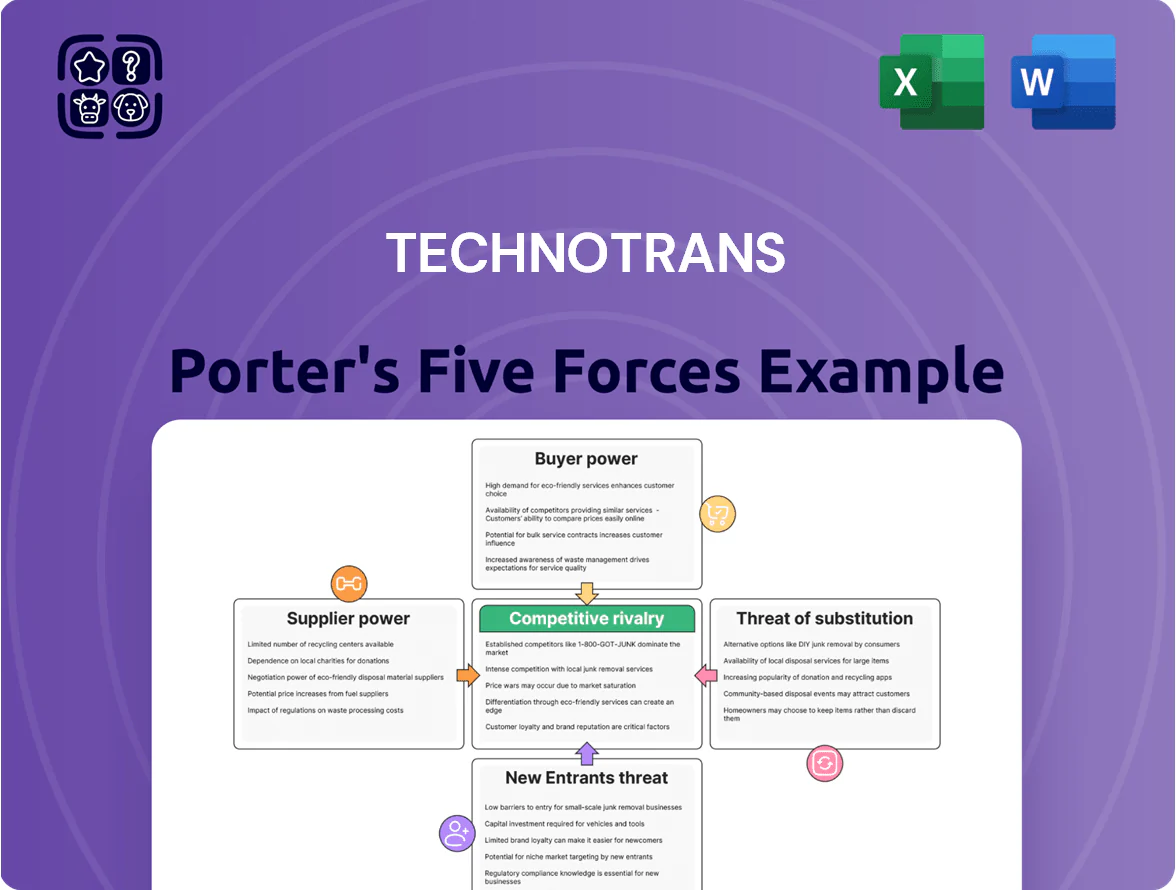

Technotrans faces moderate supplier power and niche customer segments, while capital intensity and regulatory standards limit new entrants but heighten competitive rivalry; substitutes pose a variable threat depending on application. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore technotrans’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Electronic Component Dependencies

Technotrans depends on specialized microelectronics and controllers to manage precise thermal systems, and by late 2025 high-performance semiconductors still drive production timing and costs; global chip shortages kept lead times at 20–28 weeks for certain controllers and added ~3–5% to BOM costs in 2024–25. Because a few manufacturers supply these parts, suppliers hold meaningful pricing and delivery leverage, raising input risk for margins and new-product timelines.

Raw Material Price Volatility

Technotrans relies on aluminum, copper and engineered plastics; in 2024 these raw materials drove 18–24% of COGS, and LME copper rose 28% from 2022–2024, pushing gross-margin pressure. The company hedges via forward contracts and supplier agreements, but pricing power remains with large metal miners and smelters who set spot and contract rates tied to global demand cycles. In 2025 Q1 procurement costs stayed ~12% above 2021 baseline, squeezing margins.

Niche Component Manufacturers

Technotrans relies on niche pumps and compressors made by a handful of specialized engineering firms; this supplier concentration gave those firms pricing power and contributed to supplier spend of ~12% of COGS in 2024 for similar mid-cap industrials.

Energy Costs and Utility Providers

Technotrans, a manufacturing-heavy firm, is exposed to energy pricing in Germany and Europe where industrial electricity costs averaged about 0.18 EUR/kWh in 2024, up ~8% vs 2022 due to grid fees and renewables integration.

Europe’s green-energy shift adds volatility: passthrough of carbon and balancing costs raises industrial bills and capex for on-site decarbonization, increasing supplier leverage.

Gas and grid operators keep bargaining power via regulated tariffs and limited high-capacity alternatives, so Technotrans faces concentrated supplier risk and little short-term hedging room.

- Industrial electricity ~0.18 EUR/kWh (2024)

- Energy cost rise ~8% vs 2022

- Carbon/balancing fees increase volatility

- Few immediate high-capacity alternatives

Logistics and Distribution Partners

Global supply chain integrity for technotrans hinges on a few Tier 1 shipping firms that move heavy thermal-management equipment; industry consolidation leaves roughly 5–7 global carriers able to manage oversize, high-value shipments, upping their leverage.

Those carriers imposed peak-season surcharges and detention fees that lifted logistics costs by 12–18% in 2023–2024 for heavy industrial cargo, squeezing technotrans gross margins on finished units.

Contractual tighter lead-times and strict insurance/packaging clauses force higher working capital and raise landed cost volatility, letting suppliers negotiate tougher payment and liability terms.

- 5–7 Tier 1 carriers for heavy industrial freight

- 12–18% logistics cost increase in 2023–24

- Surcharges, detention, insurance add margin pressure

- Tighter terms raise working capital and landed-cost volatility

Suppliers Squeeze technotrans: Chips, Metals, Power & Logistics Drive Rising Input Risk

Suppliers hold meaningful leverage over technotrans due to concentrated semiconductor, niche pump, metal and carrier markets; chip lead times 20–28 weeks and +3–5% BOM cost (2024–25) raised input risk, metals were 18–24% of COGS with LME copper +28% (2022–24), industrial power ~0.18 EUR/kWh (2024) +8% vs 2022, and logistics costs +12–18% (2023–24).

| Item | Metric |

|---|---|

| Chip lead times | 20–28 weeks (2024–25) |

| Chip cost impact | +3–5% BOM (2024–25) |

| Metals share of COGS | 18–24% (2024) |

| LME copper | +28% (2022–24) |

| Electricity | 0.18 EUR/kWh (2024) |

| Electricity change | +8% vs 2022 |

| Logistics cost rise | +12–18% (2023–24) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to technotrans, detailing each Porter force with industry data, supplier/buyer power, substitutes, entrant barriers, disruptive threats, and strategic implications for pricing and profitability—fully editable for reports and presentations.

A concise technotrans Porter's Five Forces one-sheet that highlights supplier and buyer leverage, competitive rivalry, threat of substitutes and entrants—ideal for rapid strategic decisions.

Customers Bargaining Power

Concentration in the E-mobility Sector

The shift to battery cooling made large OEMs and battery makers Technotrans’s main clients; in 2025 roughly 60% of its EV-related revenue tied to five global groups, concentrating buying power.

These high-volume customers command bargaining leverage via order scale and in-house engineering, pushing for lower unit costs and tech transfer options.

They typically require multi‑year contracts with fixed price caps or annual reduction targets often in the 3–7% range, pressuring margins.

Customization Requirements and System Integration

Many laser and healthcare clients demand bespoke thermal-management modules integrated into their machines, creating technical lock-in but enabling buyers to specify performance and safety metrics; in 2024 bespoke orders accounted for about 42% of Technotrans AGs industrial segment revenue (≈€95m of €225m total), boosting customer leverage.

Price Sensitivity in Legacy Printing Markets

In legacy printing markets, high maturity and intense cost pressure make customers highly price-sensitive; a 2024 IDC report showed print industry capex fell ~6% annually, pushing buyers to prioritize purchase price and energy efficiency over features.

Low Switching Costs for Standardized Units

For standardized cooling and filtration units, switching costs are low; buyers can swap suppliers with minimal integration work, pressuring Technotrans on pricing.

If competitors introduce 10–20% more energy-efficient or 15% cheaper modular units, industrial distributors often reallocate inventory within months, limiting Technotrans’s pricing power without tech or service differentiation.

- Low integration needs, quick supplier swaps

- Energy-efficiency gains (10–20%) drive shifts

- Price cuts (~15%) prompt distributor reallocation

- Only clear tech/service upgrades justify higher prices

Sustainability and ESG Mandates

Corporate buyers now tie 45–60% of supplier selection to ESG targets; in EU industrial procurement, 52% require verified energy-efficiency data as of 2024, pushing customers to demand low-carbon thermal systems.

These mandates give customers bargaining power: they request lifecycle emissions reports and energy-use proofs, pressuring technotrans to redesign products and certify performance to keep European market share.

- 52% of EU buyers require verified efficiency (2024)

- 45–60% of selections influenced by ESG

- Technotrans must certify lifecycle CO2 and energy use

OEMs dominate EV cooling: volume-driven price cuts, bespoke orders lock tech

Major OEMs/battery firms drive ~60% of EV cooling revenue (2025) and extract price concessions via volume and engineering; multi‑year contracts force 3–7% annual price cuts, squeezing margins. Bespoke industrial orders (42% of segment revenue, ≈€95m in 2024) create technical lock‑in but let buyers set specs. Standard units face low switching costs; 10–20% efficiency or ~15% price gaps cause rapid reallocation. EU procurement: 52% require verified efficiency (2024).

| Metric | Value |

|---|---|

| EV revenue share from 5 groups (2025) | ≈60% |

| Bespoke orders (industrial, 2024) | 42% ≈€95m |

| Contractual annual price cuts | 3–7% |

| Efficiency gap prompting switches | 10–20% |

| EU buyers requiring verified efficiency (2024) | 52% |

Preview the Actual Deliverable

technotrans Porter's Five Forces Analysis

This preview shows the exact technotrans Porter’s Five Forces analysis you’ll receive instantly after purchase—no placeholders or samples. The document is the complete, professionally formatted file, ready for download and immediate use. It contains the full forces assessment, implications for strategy, and concise recommendations tailored to technotrans. What you see here is precisely what you’ll get upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Technotrans faces moderate supplier power and niche customer segments, while capital intensity and regulatory standards limit new entrants but heighten competitive rivalry; substitutes pose a variable threat depending on application. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore technotrans’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Electronic Component Dependencies

Technotrans depends on specialized microelectronics and controllers to manage precise thermal systems, and by late 2025 high-performance semiconductors still drive production timing and costs; global chip shortages kept lead times at 20–28 weeks for certain controllers and added ~3–5% to BOM costs in 2024–25. Because a few manufacturers supply these parts, suppliers hold meaningful pricing and delivery leverage, raising input risk for margins and new-product timelines.

Raw Material Price Volatility

Technotrans relies on aluminum, copper and engineered plastics; in 2024 these raw materials drove 18–24% of COGS, and LME copper rose 28% from 2022–2024, pushing gross-margin pressure. The company hedges via forward contracts and supplier agreements, but pricing power remains with large metal miners and smelters who set spot and contract rates tied to global demand cycles. In 2025 Q1 procurement costs stayed ~12% above 2021 baseline, squeezing margins.

Niche Component Manufacturers

Technotrans relies on niche pumps and compressors made by a handful of specialized engineering firms; this supplier concentration gave those firms pricing power and contributed to supplier spend of ~12% of COGS in 2024 for similar mid-cap industrials.

Energy Costs and Utility Providers

Technotrans, a manufacturing-heavy firm, is exposed to energy pricing in Germany and Europe where industrial electricity costs averaged about 0.18 EUR/kWh in 2024, up ~8% vs 2022 due to grid fees and renewables integration.

Europe’s green-energy shift adds volatility: passthrough of carbon and balancing costs raises industrial bills and capex for on-site decarbonization, increasing supplier leverage.

Gas and grid operators keep bargaining power via regulated tariffs and limited high-capacity alternatives, so Technotrans faces concentrated supplier risk and little short-term hedging room.

- Industrial electricity ~0.18 EUR/kWh (2024)

- Energy cost rise ~8% vs 2022

- Carbon/balancing fees increase volatility

- Few immediate high-capacity alternatives

Logistics and Distribution Partners

Global supply chain integrity for technotrans hinges on a few Tier 1 shipping firms that move heavy thermal-management equipment; industry consolidation leaves roughly 5–7 global carriers able to manage oversize, high-value shipments, upping their leverage.

Those carriers imposed peak-season surcharges and detention fees that lifted logistics costs by 12–18% in 2023–2024 for heavy industrial cargo, squeezing technotrans gross margins on finished units.

Contractual tighter lead-times and strict insurance/packaging clauses force higher working capital and raise landed cost volatility, letting suppliers negotiate tougher payment and liability terms.

- 5–7 Tier 1 carriers for heavy industrial freight

- 12–18% logistics cost increase in 2023–24

- Surcharges, detention, insurance add margin pressure

- Tighter terms raise working capital and landed-cost volatility

Suppliers Squeeze technotrans: Chips, Metals, Power & Logistics Drive Rising Input Risk

Suppliers hold meaningful leverage over technotrans due to concentrated semiconductor, niche pump, metal and carrier markets; chip lead times 20–28 weeks and +3–5% BOM cost (2024–25) raised input risk, metals were 18–24% of COGS with LME copper +28% (2022–24), industrial power ~0.18 EUR/kWh (2024) +8% vs 2022, and logistics costs +12–18% (2023–24).

| Item | Metric |

|---|---|

| Chip lead times | 20–28 weeks (2024–25) |

| Chip cost impact | +3–5% BOM (2024–25) |

| Metals share of COGS | 18–24% (2024) |

| LME copper | +28% (2022–24) |

| Electricity | 0.18 EUR/kWh (2024) |

| Electricity change | +8% vs 2022 |

| Logistics cost rise | +12–18% (2023–24) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to technotrans, detailing each Porter force with industry data, supplier/buyer power, substitutes, entrant barriers, disruptive threats, and strategic implications for pricing and profitability—fully editable for reports and presentations.

A concise technotrans Porter's Five Forces one-sheet that highlights supplier and buyer leverage, competitive rivalry, threat of substitutes and entrants—ideal for rapid strategic decisions.

Customers Bargaining Power

Concentration in the E-mobility Sector

The shift to battery cooling made large OEMs and battery makers Technotrans’s main clients; in 2025 roughly 60% of its EV-related revenue tied to five global groups, concentrating buying power.

These high-volume customers command bargaining leverage via order scale and in-house engineering, pushing for lower unit costs and tech transfer options.

They typically require multi‑year contracts with fixed price caps or annual reduction targets often in the 3–7% range, pressuring margins.

Customization Requirements and System Integration

Many laser and healthcare clients demand bespoke thermal-management modules integrated into their machines, creating technical lock-in but enabling buyers to specify performance and safety metrics; in 2024 bespoke orders accounted for about 42% of Technotrans AGs industrial segment revenue (≈€95m of €225m total), boosting customer leverage.

Price Sensitivity in Legacy Printing Markets

In legacy printing markets, high maturity and intense cost pressure make customers highly price-sensitive; a 2024 IDC report showed print industry capex fell ~6% annually, pushing buyers to prioritize purchase price and energy efficiency over features.

Low Switching Costs for Standardized Units

For standardized cooling and filtration units, switching costs are low; buyers can swap suppliers with minimal integration work, pressuring Technotrans on pricing.

If competitors introduce 10–20% more energy-efficient or 15% cheaper modular units, industrial distributors often reallocate inventory within months, limiting Technotrans’s pricing power without tech or service differentiation.

- Low integration needs, quick supplier swaps

- Energy-efficiency gains (10–20%) drive shifts

- Price cuts (~15%) prompt distributor reallocation

- Only clear tech/service upgrades justify higher prices

Sustainability and ESG Mandates

Corporate buyers now tie 45–60% of supplier selection to ESG targets; in EU industrial procurement, 52% require verified energy-efficiency data as of 2024, pushing customers to demand low-carbon thermal systems.

These mandates give customers bargaining power: they request lifecycle emissions reports and energy-use proofs, pressuring technotrans to redesign products and certify performance to keep European market share.

- 52% of EU buyers require verified efficiency (2024)

- 45–60% of selections influenced by ESG

- Technotrans must certify lifecycle CO2 and energy use

OEMs dominate EV cooling: volume-driven price cuts, bespoke orders lock tech

Major OEMs/battery firms drive ~60% of EV cooling revenue (2025) and extract price concessions via volume and engineering; multi‑year contracts force 3–7% annual price cuts, squeezing margins. Bespoke industrial orders (42% of segment revenue, ≈€95m in 2024) create technical lock‑in but let buyers set specs. Standard units face low switching costs; 10–20% efficiency or ~15% price gaps cause rapid reallocation. EU procurement: 52% require verified efficiency (2024).

| Metric | Value |

|---|---|

| EV revenue share from 5 groups (2025) | ≈60% |

| Bespoke orders (industrial, 2024) | 42% ≈€95m |

| Contractual annual price cuts | 3–7% |

| Efficiency gap prompting switches | 10–20% |

| EU buyers requiring verified efficiency (2024) | 52% |

Preview the Actual Deliverable

technotrans Porter's Five Forces Analysis

This preview shows the exact technotrans Porter’s Five Forces analysis you’ll receive instantly after purchase—no placeholders or samples. The document is the complete, professionally formatted file, ready for download and immediate use. It contains the full forces assessment, implications for strategy, and concise recommendations tailored to technotrans. What you see here is precisely what you’ll get upon payment.