Techstep Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

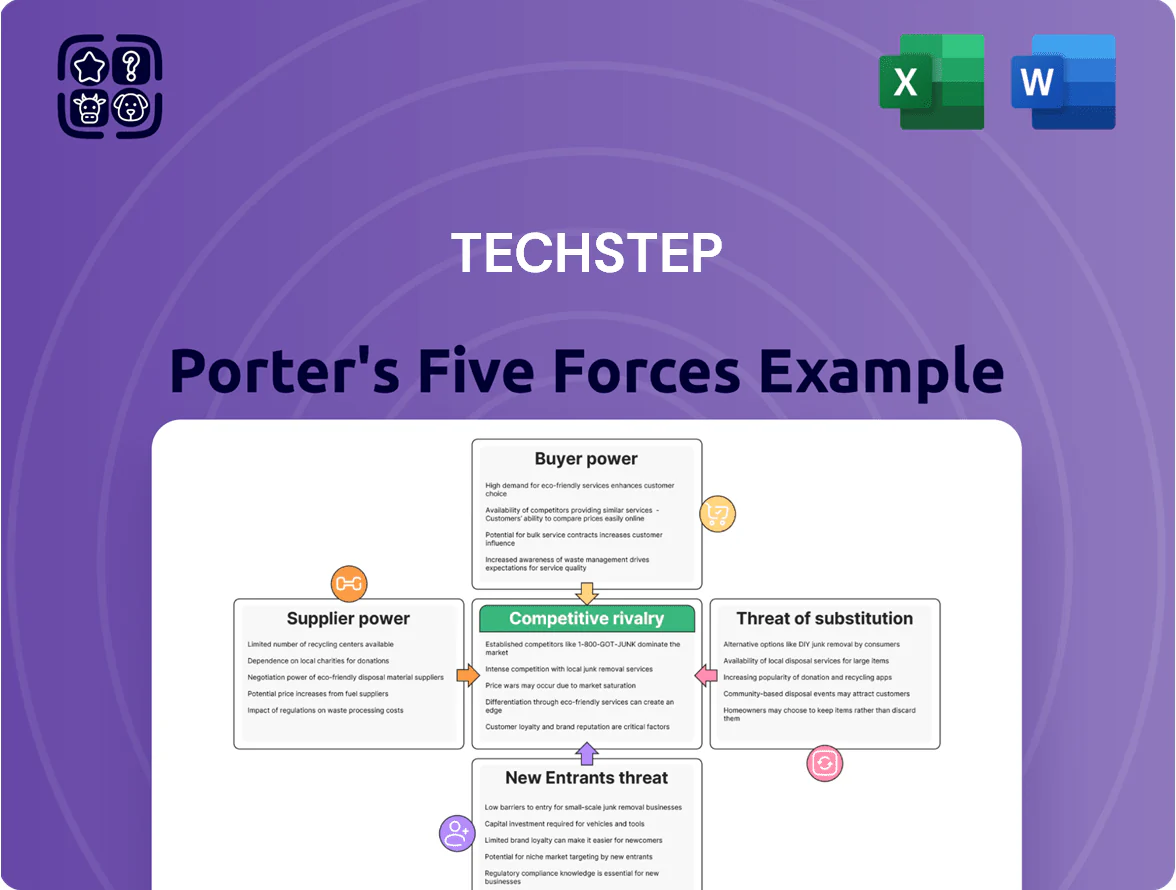

Techstep faces moderate supplier leverage, evolving buyer expectations, and targeted competitive threats from niche UCaaS players; this snapshot highlights key pressure points but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis to access force ratings, visuals, and actionable strategies that clarify Techstep’s competitive intensity and inform smarter investment or strategic decisions.

Suppliers Bargaining Power

Hardware Manufacturer Dominance

The bargaining power of suppliers is high because Techstep depends on a few global hardware giants like Apple and Samsung, which held about 58% of global smartphone shipments in 2024 (IDC). These manufacturers set device pricing, release timing, and inventory; shortages in 2023–24 pushed enterprise device costs up ~9% YoY. Techstep must keep strategic vendor agreements and priority allocations to supply clients with the latest devices.

Software and Operating System Control

Major software providers like Microsoft, Google and leading MDM vendors control key OS and API access, giving them strong pricing power over Techstep’s platform ecosystem.

Techstep embeds these third-party solutions; a 10–20% license or API-fee increase (similar to Microsoft’s Azure price moves in 2024) would hit gross margins directly.

High technical coupling and integration costs make supplier switches slow and costly, risking service disruption and customer churn.

Logistics and Distribution Partnerships

Techstep relies on third-party logistics and distribution partners for hardware movement and storage, but specialized handling for high-value electronics shrinks viable providers to a few regional specialists; global express carriers handle ~70% of urgent tech shipments while niche handlers cover the rest.

In 2025, logistics cost increases of 8–12% hit hardware margins; a 2024 DHL report showed tech-sector freight surcharges rose 9% year-over-year, so provider price hikes or disruptions can raise Techstep's operating costs materially.

Financing and Credit Providers

Techstep’s hardware-as-a-service and lifecycle model relies on external capital; banks and leasing firms set interest rates and covenants that directly affect unit economics and margins.

As of 2025, rising corporate loan spreads (EU BBB+ avg +160bps vs 2021 +95bps) would raise financing costs and compress recurring-revenue IRR, limiting fleet expansion.

If credit tightens further by end-2025, growth funding may shrink and churn risk rises as device refresh cycles slow.

- Depends on leasing rates and credit terms

- 2025 EU BBB+ spreads ~+160bps (vs 95bps in 2021)

- Higher spreads cut recurring-revenue IRR

- Tighter credit limits fleet growth and upsell

Specialized Cybersecurity Vendors

Techstep relies on niche cybersecurity vendors for threat defense and encryption, and those firms hold high bargaining power because their IP is specialized and scarce amid a 23% CAGR in mobile security spending (2020–2025), driving premium pricing.

Techstep must weigh higher vendor costs—often 10–20% of solution BOM—against enterprise price sensitivity; passing costs risks churn among mid-market clients where ARPU is lower.

- Specialized IP raises supplier leverage

- Mobile security spend grew ~23% CAGR to 2025

- Security add-ons equal ~10–20% of BOM

- Price-sensitive enterprise segments risk churn

Supplier power and rising costs squeeze device margins and fleet growth

Suppliers hold high power: Apple/Samsung ~58% smartphone share (2024, IDC); device shortages raised enterprise costs ~9% YoY (2023–24). Major software/MDM vendors can lift fees 10–20%, cutting gross margins. Logistics and leasing cost rises (DHL freight +9% 2024; EU BBB+ spreads +160bps 2025) squeeze unit economics and limit fleet growth.

| Metric | Value |

|---|---|

| Smartphone share (2024) | 58% |

| Device cost rise (2023–24) | ~9% YoY |

| Software fee shock | 10–20% |

| DHL freight rise (2024) | +9% |

| EU BBB+ spreads (2025) | +160bps |

What is included in the product

Concise Porter's Five Forces analysis tailored to Techstep that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary and editable Word-ready format for investor decks and internal strategy use.

A concise Porter's Five Forces one-sheet for Techstep that highlights competitive pressures and strategic levers, ready to drop into decks for fast, boardroom-ready decisions.

Customers Bargaining Power

Public Sector Procurement Influence

Enterprise Client Volume Discounts

Large private enterprises can negotiate double-digit seat discounts with Techstep; procurement benchmarks show 10–25% off list when clients exceed 5,000 managed seats (Gartner 2024 proxy deals).

These buyers compare Techstep to global rivals and regional resellers, driving price compression—industry surveys in 2025 report average contract fee pressure of 8–12% for unified-communications-as-a-service.

Buying power concentrates: top 5 customers often account for 30–45% of revenue, so losing one major account could cut annual revenue by a mid-teens percentage point.

Low Switching Costs for Software Only

For customers using only Techstep’s software, switching costs are low versus full lifecycle services; cloud MDM churn averaged ~12% annually in 2024 industry surveys, and standardization trends through 2025 make migrations faster. By 2025, common API and SSO support cut migration downtime to days not weeks, so customers can move with minimal ops impact. That reality forces Techstep to keep innovating and to offer superior support to protect recurring SaaS revenue.

High Integration as a Retention Tool

Techstep locks customers by bundling device leasing, MDM, recycling and helpdesk; clients using the full lifecycle suite face switching costs often >25% of annual IT OPEX, per 2024 vendor surveys, lowering buyer price leverage.

Embedding Techstep into HR onboarding and IT workflows creates a sticky platform; retention rises—Techstep reported 88% net retention in 2024—so the firm can resist margin-eroding price cuts.

- Full-suite users: switching cost >25% annual IT OPEX

- Net retention 2024: 88%

- Lifecycle bundling reduces buyer price pressure

Demand for Transparency and Customization

Buyers now insist on clear data-security metrics, ESG reports, and device-usage analytics; 68% of B2B buyers (Gartner 2024) rate transparency as a top procurement factor.

Customers can require tailored dashboards and certifications (ISO 27001, SOC 2); losing those needs risks churn—enterprise switching costs fell 12% in 2023.

Techstep must fund in-house software dev (estimate: €4–6m over 18 months for analytics and compliance modules) to retain contracts and block migration to more flexible vendors.

- 68% of B2B buyers demand transparency

- ISO 27001/SOC 2 often required

- €4–6m capex for in-house dev (18 months)

- 12% drop in enterprise switching costs (2023)

High buyer power: public sector cuts margins, top clients concentrate risk, €4–6m capex

| Metric | Value |

|---|---|

| Public revenue 2024 | 45% |

| Top5 concentration | 30–45% |

| Gross margin hit (pub) | −3–5 ppt |

| Seat discounts (large) | 10–25% |

| Net retention 2024 | 88% |

| Software churn 2024 | ~12% |

| Buyer transparency | 68% |

| Capex for modules | €4–6m (18m) |

Same Document Delivered

Techstep Porter's Five Forces Analysis

This preview shows the exact Techstep Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for instant download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Techstep faces moderate supplier leverage, evolving buyer expectations, and targeted competitive threats from niche UCaaS players; this snapshot highlights key pressure points but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis to access force ratings, visuals, and actionable strategies that clarify Techstep’s competitive intensity and inform smarter investment or strategic decisions.

Suppliers Bargaining Power

Hardware Manufacturer Dominance

The bargaining power of suppliers is high because Techstep depends on a few global hardware giants like Apple and Samsung, which held about 58% of global smartphone shipments in 2024 (IDC). These manufacturers set device pricing, release timing, and inventory; shortages in 2023–24 pushed enterprise device costs up ~9% YoY. Techstep must keep strategic vendor agreements and priority allocations to supply clients with the latest devices.

Software and Operating System Control

Major software providers like Microsoft, Google and leading MDM vendors control key OS and API access, giving them strong pricing power over Techstep’s platform ecosystem.

Techstep embeds these third-party solutions; a 10–20% license or API-fee increase (similar to Microsoft’s Azure price moves in 2024) would hit gross margins directly.

High technical coupling and integration costs make supplier switches slow and costly, risking service disruption and customer churn.

Logistics and Distribution Partnerships

Techstep relies on third-party logistics and distribution partners for hardware movement and storage, but specialized handling for high-value electronics shrinks viable providers to a few regional specialists; global express carriers handle ~70% of urgent tech shipments while niche handlers cover the rest.

In 2025, logistics cost increases of 8–12% hit hardware margins; a 2024 DHL report showed tech-sector freight surcharges rose 9% year-over-year, so provider price hikes or disruptions can raise Techstep's operating costs materially.

Financing and Credit Providers

Techstep’s hardware-as-a-service and lifecycle model relies on external capital; banks and leasing firms set interest rates and covenants that directly affect unit economics and margins.

As of 2025, rising corporate loan spreads (EU BBB+ avg +160bps vs 2021 +95bps) would raise financing costs and compress recurring-revenue IRR, limiting fleet expansion.

If credit tightens further by end-2025, growth funding may shrink and churn risk rises as device refresh cycles slow.

- Depends on leasing rates and credit terms

- 2025 EU BBB+ spreads ~+160bps (vs 95bps in 2021)

- Higher spreads cut recurring-revenue IRR

- Tighter credit limits fleet growth and upsell

Specialized Cybersecurity Vendors

Techstep relies on niche cybersecurity vendors for threat defense and encryption, and those firms hold high bargaining power because their IP is specialized and scarce amid a 23% CAGR in mobile security spending (2020–2025), driving premium pricing.

Techstep must weigh higher vendor costs—often 10–20% of solution BOM—against enterprise price sensitivity; passing costs risks churn among mid-market clients where ARPU is lower.

- Specialized IP raises supplier leverage

- Mobile security spend grew ~23% CAGR to 2025

- Security add-ons equal ~10–20% of BOM

- Price-sensitive enterprise segments risk churn

Supplier power and rising costs squeeze device margins and fleet growth

Suppliers hold high power: Apple/Samsung ~58% smartphone share (2024, IDC); device shortages raised enterprise costs ~9% YoY (2023–24). Major software/MDM vendors can lift fees 10–20%, cutting gross margins. Logistics and leasing cost rises (DHL freight +9% 2024; EU BBB+ spreads +160bps 2025) squeeze unit economics and limit fleet growth.

| Metric | Value |

|---|---|

| Smartphone share (2024) | 58% |

| Device cost rise (2023–24) | ~9% YoY |

| Software fee shock | 10–20% |

| DHL freight rise (2024) | +9% |

| EU BBB+ spreads (2025) | +160bps |

What is included in the product

Concise Porter's Five Forces analysis tailored to Techstep that uncovers competition drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary and editable Word-ready format for investor decks and internal strategy use.

A concise Porter's Five Forces one-sheet for Techstep that highlights competitive pressures and strategic levers, ready to drop into decks for fast, boardroom-ready decisions.

Customers Bargaining Power

Public Sector Procurement Influence

Enterprise Client Volume Discounts

Large private enterprises can negotiate double-digit seat discounts with Techstep; procurement benchmarks show 10–25% off list when clients exceed 5,000 managed seats (Gartner 2024 proxy deals).

These buyers compare Techstep to global rivals and regional resellers, driving price compression—industry surveys in 2025 report average contract fee pressure of 8–12% for unified-communications-as-a-service.

Buying power concentrates: top 5 customers often account for 30–45% of revenue, so losing one major account could cut annual revenue by a mid-teens percentage point.

Low Switching Costs for Software Only

For customers using only Techstep’s software, switching costs are low versus full lifecycle services; cloud MDM churn averaged ~12% annually in 2024 industry surveys, and standardization trends through 2025 make migrations faster. By 2025, common API and SSO support cut migration downtime to days not weeks, so customers can move with minimal ops impact. That reality forces Techstep to keep innovating and to offer superior support to protect recurring SaaS revenue.

High Integration as a Retention Tool

Techstep locks customers by bundling device leasing, MDM, recycling and helpdesk; clients using the full lifecycle suite face switching costs often >25% of annual IT OPEX, per 2024 vendor surveys, lowering buyer price leverage.

Embedding Techstep into HR onboarding and IT workflows creates a sticky platform; retention rises—Techstep reported 88% net retention in 2024—so the firm can resist margin-eroding price cuts.

- Full-suite users: switching cost >25% annual IT OPEX

- Net retention 2024: 88%

- Lifecycle bundling reduces buyer price pressure

Demand for Transparency and Customization

Buyers now insist on clear data-security metrics, ESG reports, and device-usage analytics; 68% of B2B buyers (Gartner 2024) rate transparency as a top procurement factor.

Customers can require tailored dashboards and certifications (ISO 27001, SOC 2); losing those needs risks churn—enterprise switching costs fell 12% in 2023.

Techstep must fund in-house software dev (estimate: €4–6m over 18 months for analytics and compliance modules) to retain contracts and block migration to more flexible vendors.

- 68% of B2B buyers demand transparency

- ISO 27001/SOC 2 often required

- €4–6m capex for in-house dev (18 months)

- 12% drop in enterprise switching costs (2023)

High buyer power: public sector cuts margins, top clients concentrate risk, €4–6m capex

| Metric | Value |

|---|---|

| Public revenue 2024 | 45% |

| Top5 concentration | 30–45% |

| Gross margin hit (pub) | −3–5 ppt |

| Seat discounts (large) | 10–25% |

| Net retention 2024 | 88% |

| Software churn 2024 | ~12% |

| Buyer transparency | 68% |

| Capex for modules | €4–6m (18m) |

Same Document Delivered

Techstep Porter's Five Forces Analysis

This preview shows the exact Techstep Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for instant download and use the moment you buy.