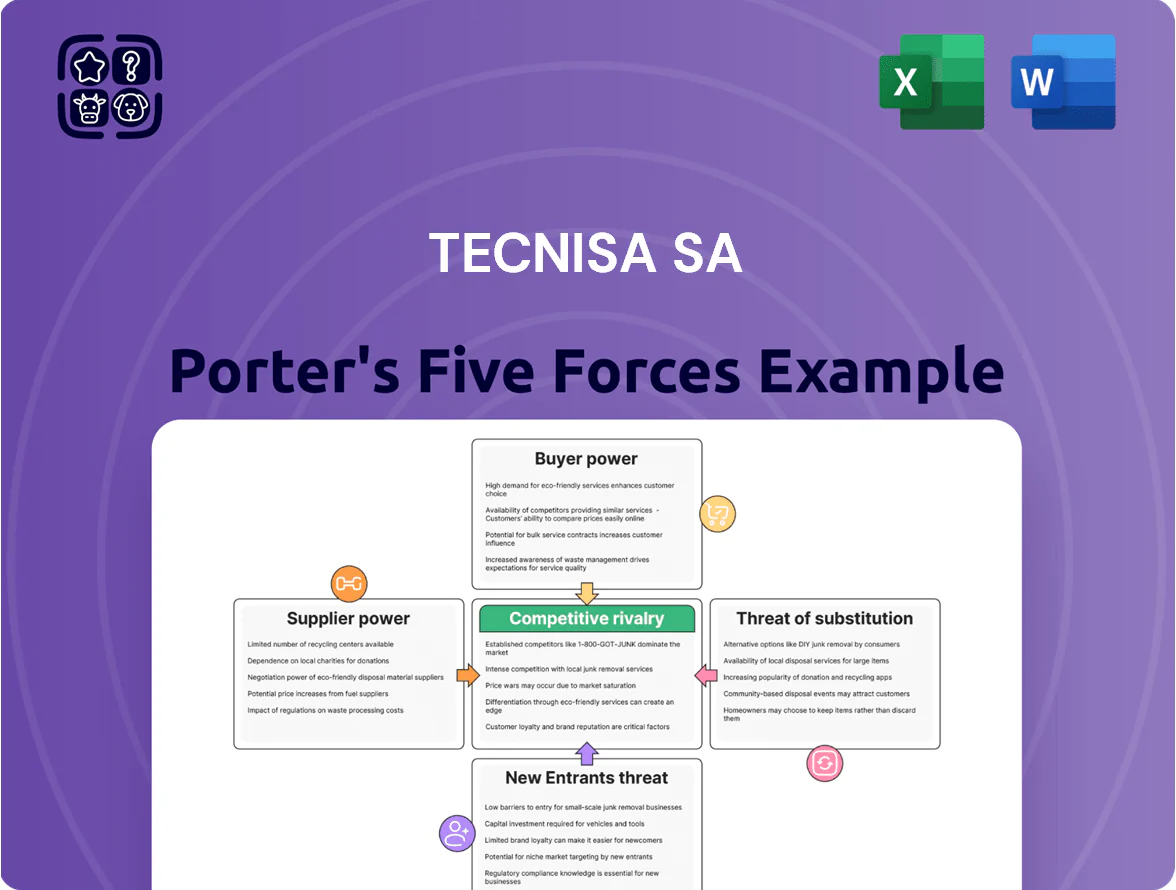

Tecnisa SA Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Tecnisa SA operates in a capital-intensive, cyclical real estate market where buyer bargaining power and substitute housing options weigh heavily, while supplier leverage and regulatory shifts add complexity; competitive rivalry is intense among national and regional developers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Tecnisa SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The Brazilian steel, cement and concrete markets are highly concentrated: in 2024 the top five suppliers controlled ~68% of cement capacity and ArcelorMittal Brasil and Gerdau led steel, giving suppliers pricing leverage over developers like Tecnisa.

During 2020–24 infrastructure booms, supplier-driven price spikes raised construction input costs by ~12–20% year-over-year at peaks, squeezing Tecnisa’s gross margins on projects.

Global commodity swings matter: iron ore and cement-linked freight shifts moved input-cost exposure for Tecnisa by roughly ±6–10% of project budgets in 2023–24.

Labor Market Constraints and Specialized Trades

The São Paulo metro area had a 2024 skilled construction labor shortage of about 8.3% versus demand, tightening supply for Tecnisa's high-end projects and raising reliance on niche subcontractors who gain bargaining power.

Specialized engineering and architectural trades can charge premiums of 10–18% above standard rates; Tecnisa's dependence on them increases supplier leverage and scheduling risk.

Union-negotiated wage rises averaged 7.5% in 2024, pushing construction labor costs up and squeezing Tecnisa's operating margin.

Land Availability in Prime Urban Areas

The supply of developable land in prime São Paulo districts is highly limited and held by few owners, giving suppliers strong leverage over Tecnisa SA; in 2024, land price per m² in Jardins and Vila Nova Conceição averaged BRL 18,000–28,000, squeezing margins.

Scarcity forces Tecnisa into costly purchases or land-swap deals—recent 2023–24 transactions show premium plots costing 25–40% above municipal valuations, raising upfront capital needs.

Maintaining a competitive land bank thus requires large cash reserves or credit lines; Tecnisa’s LTM cash and equivalents of BRL 420 million (Q3 2024) limits aggressive land buying without higher leverage.

Financial Institutions and Capital Providers

Tecnisa depends on banks and capital markets for project financing and working capital; in 2025 Brazil’s Selic averaged about 11.75%, so borrowing costs remain high and volatile, directly squeezing project IRRs and cash flow.

Banks and bond investors thus hold strong leverage: a 300 bps move in Selic or tighter reserve requirements can raise Tecinsa’s debt service by tens of millions annually and force project deferrals.

What this hides: fluctuating credit spreads and tighter macro rules (Basel IV-like moves) could further raise lenders’ pricing and approval hurdles.

- 2025 Selic avg 11.75%

- 300 bps rise → notable debt-service jump

- Capital markets access shapes project timing

- Regulatory shifts (bank rules) increase lender power

Technological and Sustainable Solution Providers

Tecnisa relies on niche suppliers for green materials and smart-home systems as demand for LEED/BREEAM-like certifications and IoT integration rises; in Brazil green-certified projects grew ~18% in 2024, raising procurement concentration risk.

These vendors command pricing power—specialized materials can add 5–12% to construction costs—and limited substitutes increase dependency, yet the tech is key to maintaining Tecnisa’s premium positioning and higher ASPs.

- 2024: green projects +18%

- Specialized inputs add 5–12% cost

- Single-source suppliers common

- Essential for premium ASPs and brand

Suppliers Squeeze Tecnisa: Input Shocks, High Rates & Tight Land/Labor Crippling Margins

Suppliers hold strong leverage over Tecnisa: top-5 cement/steel ~68% (2024), input-cost spikes +12–20% peak YoY (2020–24), iron-ore/cement swings ±6–10% project budgets (2023–24), skilled-labor shortage ~8.3% (São Paulo 2024), land prices BRL18,000–28,000/m² in prime districts (2024), LTM cash BRL420m (Q3 2024), 2025 Selic avg 11.75% raising financing cost.

| Metric | Value |

|---|---|

| Top-5 cement/steel | ~68% |

| Input-cost spikes | +12–20% YoY |

| Iron-ore/cement swing | ±6–10% |

| Labor shortage SP | 8.3% |

| Prime land price | BRL18k–28k/m² |

| LTM cash | BRL420m |

| Selic (2025 avg) | 11.75% |

What is included in the product

Tailored Porter's Five Forces analysis for Tecnisa SA that uncovers competitive drivers, buyer and supplier bargaining power, entry and substitution threats, and strategic levers shaping its pricing, profitability, and market defensibility.

Clear, one-sheet Porter's Five Forces for Tecnisa S.A.—condensed insights to speed strategic decisions and investor briefings.

Customers Bargaining Power

Availability of Financing for Homebuyers

The purchasing power of Tecnisa SA customers hinges on mortgage availability and rates in Brazil; as of Q4 2025 the Selic-linked average mortgage rate was about 12.5% (CBN data), which tightens affordability and raises bargaining leverage for buyers.

If rates climb, buyers push for discounts or exit markets, forcing Tecnisa to extend softer payment plans or promotions to preserve sales; in 2024 about 28% of new-home transactions used bank financing, highlighting sensitivity to credit terms.

Information Transparency and Digital Comparison

Modern buyers use platforms like VivaReal and Zillow-style apps to compare prices and specs across developers in real time; a 2024 Localiza/Ibope study found 62% of Brazilian homebuyers check three+ listings before contacting a seller.

This transparency cuts information asymmetry, letting customers push discounts tied to market benchmarks; in 2023 average discounting in São Paulo new launches reached 4.8%.

Tecnisa must justify premiums through brand equity and features—its 2024 gross margin of 12.5% vs. sector median 9.1% shows some pricing power, but ongoing product differentiation is essential.

Low Switching Costs During Pre-launch Phase

In Tecnisa SA’s pre-launch phase, low switching costs let buyers shift to rival projects with little financial loss, forcing Tecnisa to spend heavily on marketing and differentiated amenities to lock early commitments; in 2024 Tecnisa increased sales & marketing expense to 4.2% of revenue, up from 3.1% in 2022.

Economic Sensitivity of Target Segments

Tecnisa targets middle and upper-middle income buyers who cut back when Brazil’s GDP growth slows or inflation exceeds the central bank target; in 2024 Brazil inflation averaged about 4.3% and real GDP grew ~3.6%, which still left many buyers preferring smaller units or delayed purchases.

This cyclicality boosts buyer leverage, forcing Tecnisa to offer flexible financing, longer payment plans, or product downshifts to retain sales and maintain margins.

- 2024 Brazil inflation ~4.3%

- 2024 real GDP growth ~3.6%

- Buyers favor smaller units or delayed purchases

- Developers must add financing and flexible terms

Impact of Secondary Market Inventory

The availability of used and recently completed units in the same neighborhoods creates a practical price ceiling for Tecnisa’s new launches, as buyers compare new-unit premiums to secondary-market discounts; in 2024 resale listings in Greater São Paulo undercut new-launch asking prices by about 8–12% on average.

This comparison limits Tecnisa’s pricing power and means the firm must add clear differentiation—better finishes, amenities, or financing—to avoid markdowns; otherwise raising prices unilaterally risks slower absorption and longer inventory days.

- 2024 Greater São Paulo resale discount vs new: ~8–12%

- Secondary inventory increases buyer bargaining leverage

- Differentiation or financing needed to sustain premiums

High borrowing costs and savvy buyers squeeze margins—Tecnisa outperforms sector

Buyers hold moderate-high leverage: Q4 2025 average mortgage ~12.5% (CBN), 2024 bank-financed share 28%, 2024 gross margin Tecnisa 12.5% vs sector 9.1%, São Paulo resale undercut new by ~8–12%, 62% of buyers compare 3+ listings.

| Metric | Value |

|---|---|

| Avg mortgage rate (Q4 2025) | 12.5% |

| Bank-financed new sales (2024) | 28% |

| Tecnisa gross margin (2024) | 12.5% |

| Sector median margin (2024) | 9.1% |

| Resale vs new discount (SP, 2024) | 8–12% |

| Buyers checking 3+ listings (2024) | 62% |

What You See Is What You Get

Tecnisa SA Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tecnisa S.A. you’ll receive after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for immediate download and use once you complete payment. It contains a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to Tecnisa’s market position and strategy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Tecnisa SA operates in a capital-intensive, cyclical real estate market where buyer bargaining power and substitute housing options weigh heavily, while supplier leverage and regulatory shifts add complexity; competitive rivalry is intense among national and regional developers. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Tecnisa SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Raw Material Providers

The Brazilian steel, cement and concrete markets are highly concentrated: in 2024 the top five suppliers controlled ~68% of cement capacity and ArcelorMittal Brasil and Gerdau led steel, giving suppliers pricing leverage over developers like Tecnisa.

During 2020–24 infrastructure booms, supplier-driven price spikes raised construction input costs by ~12–20% year-over-year at peaks, squeezing Tecnisa’s gross margins on projects.

Global commodity swings matter: iron ore and cement-linked freight shifts moved input-cost exposure for Tecnisa by roughly ±6–10% of project budgets in 2023–24.

Labor Market Constraints and Specialized Trades

The São Paulo metro area had a 2024 skilled construction labor shortage of about 8.3% versus demand, tightening supply for Tecnisa's high-end projects and raising reliance on niche subcontractors who gain bargaining power.

Specialized engineering and architectural trades can charge premiums of 10–18% above standard rates; Tecnisa's dependence on them increases supplier leverage and scheduling risk.

Union-negotiated wage rises averaged 7.5% in 2024, pushing construction labor costs up and squeezing Tecnisa's operating margin.

Land Availability in Prime Urban Areas

The supply of developable land in prime São Paulo districts is highly limited and held by few owners, giving suppliers strong leverage over Tecnisa SA; in 2024, land price per m² in Jardins and Vila Nova Conceição averaged BRL 18,000–28,000, squeezing margins.

Scarcity forces Tecnisa into costly purchases or land-swap deals—recent 2023–24 transactions show premium plots costing 25–40% above municipal valuations, raising upfront capital needs.

Maintaining a competitive land bank thus requires large cash reserves or credit lines; Tecnisa’s LTM cash and equivalents of BRL 420 million (Q3 2024) limits aggressive land buying without higher leverage.

Financial Institutions and Capital Providers

Tecnisa depends on banks and capital markets for project financing and working capital; in 2025 Brazil’s Selic averaged about 11.75%, so borrowing costs remain high and volatile, directly squeezing project IRRs and cash flow.

Banks and bond investors thus hold strong leverage: a 300 bps move in Selic or tighter reserve requirements can raise Tecinsa’s debt service by tens of millions annually and force project deferrals.

What this hides: fluctuating credit spreads and tighter macro rules (Basel IV-like moves) could further raise lenders’ pricing and approval hurdles.

- 2025 Selic avg 11.75%

- 300 bps rise → notable debt-service jump

- Capital markets access shapes project timing

- Regulatory shifts (bank rules) increase lender power

Technological and Sustainable Solution Providers

Tecnisa relies on niche suppliers for green materials and smart-home systems as demand for LEED/BREEAM-like certifications and IoT integration rises; in Brazil green-certified projects grew ~18% in 2024, raising procurement concentration risk.

These vendors command pricing power—specialized materials can add 5–12% to construction costs—and limited substitutes increase dependency, yet the tech is key to maintaining Tecnisa’s premium positioning and higher ASPs.

- 2024: green projects +18%

- Specialized inputs add 5–12% cost

- Single-source suppliers common

- Essential for premium ASPs and brand

Suppliers Squeeze Tecnisa: Input Shocks, High Rates & Tight Land/Labor Crippling Margins

Suppliers hold strong leverage over Tecnisa: top-5 cement/steel ~68% (2024), input-cost spikes +12–20% peak YoY (2020–24), iron-ore/cement swings ±6–10% project budgets (2023–24), skilled-labor shortage ~8.3% (São Paulo 2024), land prices BRL18,000–28,000/m² in prime districts (2024), LTM cash BRL420m (Q3 2024), 2025 Selic avg 11.75% raising financing cost.

| Metric | Value |

|---|---|

| Top-5 cement/steel | ~68% |

| Input-cost spikes | +12–20% YoY |

| Iron-ore/cement swing | ±6–10% |

| Labor shortage SP | 8.3% |

| Prime land price | BRL18k–28k/m² |

| LTM cash | BRL420m |

| Selic (2025 avg) | 11.75% |

What is included in the product

Tailored Porter's Five Forces analysis for Tecnisa SA that uncovers competitive drivers, buyer and supplier bargaining power, entry and substitution threats, and strategic levers shaping its pricing, profitability, and market defensibility.

Clear, one-sheet Porter's Five Forces for Tecnisa S.A.—condensed insights to speed strategic decisions and investor briefings.

Customers Bargaining Power

Availability of Financing for Homebuyers

The purchasing power of Tecnisa SA customers hinges on mortgage availability and rates in Brazil; as of Q4 2025 the Selic-linked average mortgage rate was about 12.5% (CBN data), which tightens affordability and raises bargaining leverage for buyers.

If rates climb, buyers push for discounts or exit markets, forcing Tecnisa to extend softer payment plans or promotions to preserve sales; in 2024 about 28% of new-home transactions used bank financing, highlighting sensitivity to credit terms.

Information Transparency and Digital Comparison

Modern buyers use platforms like VivaReal and Zillow-style apps to compare prices and specs across developers in real time; a 2024 Localiza/Ibope study found 62% of Brazilian homebuyers check three+ listings before contacting a seller.

This transparency cuts information asymmetry, letting customers push discounts tied to market benchmarks; in 2023 average discounting in São Paulo new launches reached 4.8%.

Tecnisa must justify premiums through brand equity and features—its 2024 gross margin of 12.5% vs. sector median 9.1% shows some pricing power, but ongoing product differentiation is essential.

Low Switching Costs During Pre-launch Phase

In Tecnisa SA’s pre-launch phase, low switching costs let buyers shift to rival projects with little financial loss, forcing Tecnisa to spend heavily on marketing and differentiated amenities to lock early commitments; in 2024 Tecnisa increased sales & marketing expense to 4.2% of revenue, up from 3.1% in 2022.

Economic Sensitivity of Target Segments

Tecnisa targets middle and upper-middle income buyers who cut back when Brazil’s GDP growth slows or inflation exceeds the central bank target; in 2024 Brazil inflation averaged about 4.3% and real GDP grew ~3.6%, which still left many buyers preferring smaller units or delayed purchases.

This cyclicality boosts buyer leverage, forcing Tecnisa to offer flexible financing, longer payment plans, or product downshifts to retain sales and maintain margins.

- 2024 Brazil inflation ~4.3%

- 2024 real GDP growth ~3.6%

- Buyers favor smaller units or delayed purchases

- Developers must add financing and flexible terms

Impact of Secondary Market Inventory

The availability of used and recently completed units in the same neighborhoods creates a practical price ceiling for Tecnisa’s new launches, as buyers compare new-unit premiums to secondary-market discounts; in 2024 resale listings in Greater São Paulo undercut new-launch asking prices by about 8–12% on average.

This comparison limits Tecnisa’s pricing power and means the firm must add clear differentiation—better finishes, amenities, or financing—to avoid markdowns; otherwise raising prices unilaterally risks slower absorption and longer inventory days.

- 2024 Greater São Paulo resale discount vs new: ~8–12%

- Secondary inventory increases buyer bargaining leverage

- Differentiation or financing needed to sustain premiums

High borrowing costs and savvy buyers squeeze margins—Tecnisa outperforms sector

Buyers hold moderate-high leverage: Q4 2025 average mortgage ~12.5% (CBN), 2024 bank-financed share 28%, 2024 gross margin Tecnisa 12.5% vs sector 9.1%, São Paulo resale undercut new by ~8–12%, 62% of buyers compare 3+ listings.

| Metric | Value |

|---|---|

| Avg mortgage rate (Q4 2025) | 12.5% |

| Bank-financed new sales (2024) | 28% |

| Tecnisa gross margin (2024) | 12.5% |

| Sector median margin (2024) | 9.1% |

| Resale vs new discount (SP, 2024) | 8–12% |

| Buyers checking 3+ listings (2024) | 62% |

What You See Is What You Get

Tecnisa SA Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tecnisa S.A. you’ll receive after purchase—no placeholders, no mockups. The document is fully formatted, professionally written, and ready for immediate download and use once you complete payment. It contains a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to Tecnisa’s market position and strategy.