Tokyo Electron PESTLE Analysis

Your Competitive Advantage Starts with This Report

Uncover how geopolitical shifts, supply-chain dynamics, and rapid semiconductor innovation are shaping Tokyo Electron’s strategic outlook; our concise PESTLE highlights risks and opportunities you need to know. Purchase the full analysis for a complete, actionable report—ready to download and use in investment theses, strategy decks, or boardroom briefings.

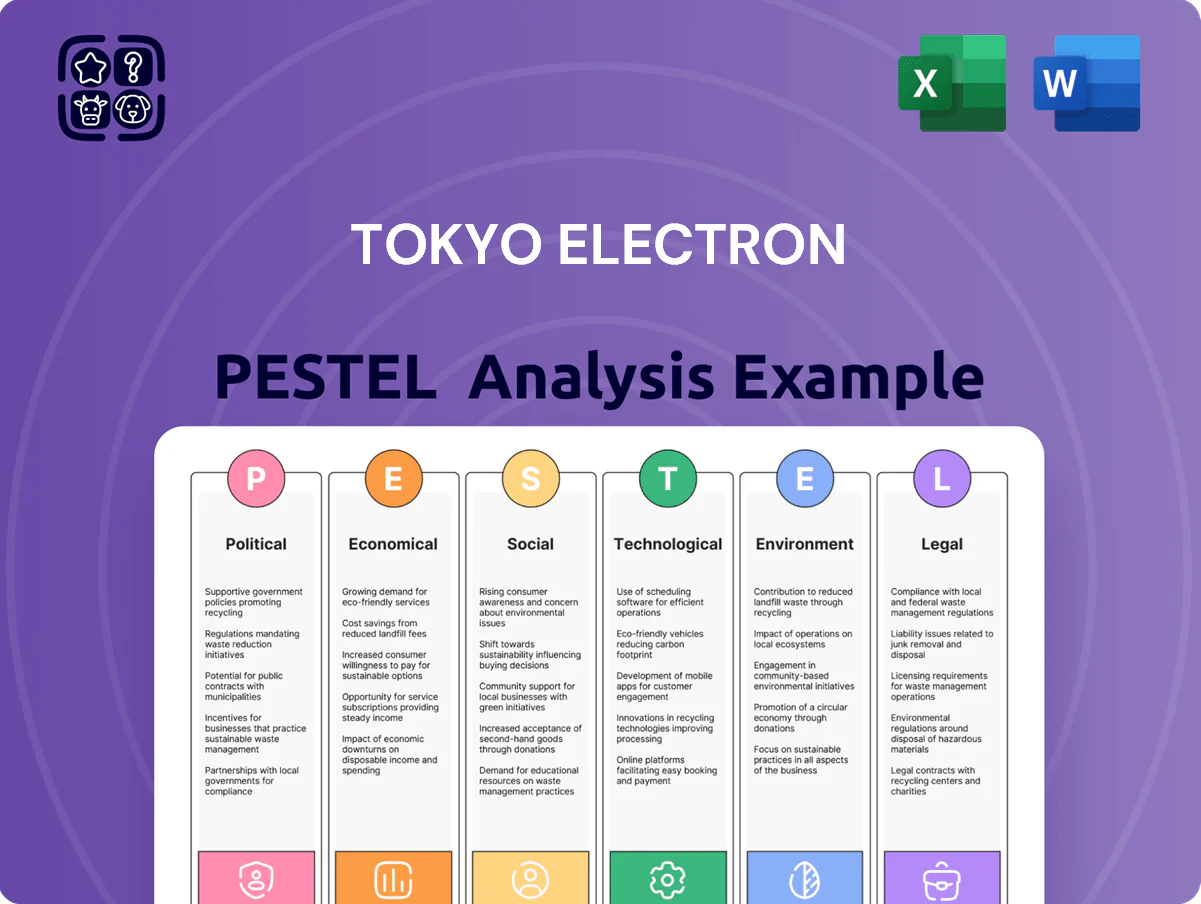

Political factors

Strategic export control policies

The Japanese government, aligning with the US and EU, tightened export controls in 2023–24 limiting high-end semiconductor equipment to China, which constrained Tokyo Electron’s 2024 China-related revenues—about 12% of group sales in FY2023—to face licensing hurdles.

These rules force Tokyo Electron into complex licensing workflows and compliance costs that pressured operating margins in 2024, with capital expenditure cycles delayed for some Chinese customers.

Management must monitor geopolitical shifts continuously to hedge risks that sudden policy changes could cut projected China sales growth and affect multi-year order books exceeding several billion dollars.

Government subsidies for domestic production

Japan is investing over ¥2.2 trillion (≈$15.5B) through initiatives like the Leading-edge Semiconductor Technology Center and Rapidus support to revive domestic fabs; Tokyo Electron, as a leading equipment supplier, stands to capture significant order flow for toolsets and services.

These state-backed investments underpin a more stable domestic revenue stream—Tokyo Electron recorded ¥1.2 trillion in Japan sales in FY2024—and accelerate joint R&D on next-generation nodes and packaging, strengthening long-term strategic collaboration.

Global trade tensions and decoupling

Ongoing US-China trade friction and export controls have pushed Tokyo Electron to diversify suppliers and markets; in FY2024 (ending Mar 2024) semiconductor-equipment revenue split showed rising sales to Taiwan and Korea as a hedge, with Japan/NA/EMEA localization increasing CAPEX exposure by an estimated mid-single-digit percentage of total capital spending.

National security and technology protection

Semiconductor equipment is now treated as a national security asset, prompting tighter export controls and limits on joint ventures; in 2024 global chip export restrictions expanded—US-led controls cover tools affecting nodes below 14nm, impacting Tokyo Electron’s addressable market and revenue mix (2023 sales ¥1.24 trillion).

Tokyo Electron must enforce strict compliance—access controls, encryption, and partner vetting—to safeguard etch/deposition IP and avoid sanctions or license denials that could disrupt supply to key customers.

Frequent government engagement is required: licensing, audits, and policy dialogue with Japan, US, and allied regulators to sustain operations and secure approvals for cross-border transfers.

- 2024 export controls broadened to advanced lithography/etch tools

- 2023 sales ¥1.24 trillion; compliance risk could affect future CAGR

- Needs: enhanced IT security, export licensing, government relations

Intergovernmental cooperation on supply chains

Agreements between Japan, the United States, and EU partners aim to build a resilient semiconductor ecosystem; G7 and US-led initiatives directed roughly $50–60 billion in public support to reshape supply chains through 2025, reducing regional disruption risks.

Tokyo Electron is central in these frameworks, contributing to standardization of advanced manufacturing processes and capturing part of a global equipment market forecasted at $90–100 billion in 2024–25.

Such cooperation stabilizes markets but forces Tokyo Electron to comply with multi-lateral export controls, subsidy rules, and cross-border IP standards, affecting capital allocation and customer engagements.

- Japan-US-EU pacts mobilized ~$50–60B public support (through 2025)

- Global semiconductor equipment market ≈ $90–100B (2024–25)

- Tokyo Electron positioned as standard-setter; faces multilateral regulatory compliance

Export Controls Trim China Sales; Japan’s ¥2.2T Push Fuels Equipment Market Shift

Geopolitical export controls (2023–24) cut China-facing sales and raised compliance costs; FY2023 China exposure ~12% of group sales. Japan’s ¥2.2T semiconductor push and ~$50–60B allied subsidies through 2025 boost domestic orders; Tokyo Electron FY2024 Japan sales ¥1.2T. Diversification increased Taiwan/Korea revenue share; global equipment market ≈$90–100B (2024–25).

| Metric | Value |

|---|---|

| China exposure | ~12% FY2023 |

| Japan investment | ¥2.2T (~$15.5B) |

| Japan sales | ¥1.2T FY2024 |

| Allied subsidies | $50–60B (thru 2025) |

| Market size | $90–100B (2024–25) |

What is included in the product

Explores how macro-environmental factors uniquely impact Tokyo Electron across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE snapshot of Tokyo Electron that highlights regulatory, technological, and supply-chain risks for quick alignment in meetings or inclusion in client reports.

Economic factors

Semiconductor industry capital expenditure cycles

Tokyo Electron revenue is highly sensitive to capex cycles at TSMC, Intel and Samsung; TSMC’s announced 2024–25 capex of ~$44–46bn and Intel’s $20–25bn guidance for advanced nodes drive demand for advanced wafer bonders and coater/developers.

Currency exchange rate fluctuations

As a Japan-based firm with ~70–80% of sales overseas, Tokyo Electron's reported profits are sensitive to JPY/USD and JPY/EUR moves; a 10% weaker yen raised FY2024 operating profit estimates across the sector by several hundred million dollars. A weaker yen boosts export competitiveness and inflates repatriated earnings, while a stronger yen compresses margins. TEL uses layered FX hedges—forwards, options and natural hedges—to stabilize guidance and limit volatility.

Rising research and development costs

Maintaining leadership in semiconductor equipment forces Tokyo Electron to ramp R&D spending—the company invested ¥104.6 billion in R&D in FY2024, up ~7% year-on-year—to track Moore’s Law and scale into 3D integration and advanced materials.

Developing specialized tools for EUV, heterogeneous integration and new substrates drives exponential cost growth in prototype and pilot production.

Tokyo Electron must balance these investments against operating margin targets—operating profit margin was 23.1% in FY2024—while preserving cash flow for shareholders.

AI-driven demand for high-performance computing

The generative AI boom and LLM deployment drove a 2024 global data center capex surge—IDC estimates hyperscaler spending rose ~18% YoY—boosting demand for HBM and advanced logic; Tokyo Electron benefits via lithography and packaging tools tied to HBM/AI-class chips used in GPUs/CPUs.

This structural shift yields steadier growth vs consumer electronics cyclicality: server/AI compute demand underpins multiyear equipment cycles, supporting TEL revenue resilience—company reported semiconductor equipment orders recovering to ¥1.2 trillion in FY2024.

Global inflation and supply chain costs

Persistently high costs for silicon, specialty gases and logistics raised Tokyo Electron's COGS; global semiconductor material prices rose ~8-12% in 2024 while ocean freight rates remained elevated versus pre-2020 levels.

To protect margins, Tokyo Electron is optimizing procurement, hedging key inputs and implemented selective price increases—helping sustain operating margin near 20% in FY2024.

Ongoing inflation management is critical to maintain investment-grade credit metrics and fund capex for 2025 fabs and R&D.

- Raw material and component costs up ~8–12% in 2024

- Selective customer price adjustments to defend margins

- Procurement optimization and hedging underway

- Maintains operating margin ~20% in FY2024

Tokyo Electron rides capex wave, FX tailwinds, and margin pressure from rising costs

Tokyo Electron faces capex-driven demand (TSMC $44–46bn, Intel $20–25bn for 2024–25) and FX exposure—~70–80% sales overseas; a 10% weaker JPY lifted sector FY2024 operating profit by several hundred million USD. R&D ¥104.6bn (FY2024) and rising material/logistics costs (+8–12% in 2024) pressure margins; TEL kept operating margin ~23.1% and orders ~¥1.2T (FY2024).

| Metric | Value |

|---|---|

| R&D FY2024 | ¥104.6bn |

| Operating margin FY2024 | 23.1% |

| Equipment orders FY2024 | ¥1.2T |

| Material cost change 2024 | +8–12% |

| TSMC capex 2024–25 | $44–46bn |

| Intel capex guidance | $20–25bn |

Full Version Awaits

Tokyo Electron PESTLE Analysis

The preview shown here is the exact Tokyo Electron PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Uncover how geopolitical shifts, supply-chain dynamics, and rapid semiconductor innovation are shaping Tokyo Electron’s strategic outlook; our concise PESTLE highlights risks and opportunities you need to know. Purchase the full analysis for a complete, actionable report—ready to download and use in investment theses, strategy decks, or boardroom briefings.

Political factors

Strategic export control policies

The Japanese government, aligning with the US and EU, tightened export controls in 2023–24 limiting high-end semiconductor equipment to China, which constrained Tokyo Electron’s 2024 China-related revenues—about 12% of group sales in FY2023—to face licensing hurdles.

These rules force Tokyo Electron into complex licensing workflows and compliance costs that pressured operating margins in 2024, with capital expenditure cycles delayed for some Chinese customers.

Management must monitor geopolitical shifts continuously to hedge risks that sudden policy changes could cut projected China sales growth and affect multi-year order books exceeding several billion dollars.

Government subsidies for domestic production

Japan is investing over ¥2.2 trillion (≈$15.5B) through initiatives like the Leading-edge Semiconductor Technology Center and Rapidus support to revive domestic fabs; Tokyo Electron, as a leading equipment supplier, stands to capture significant order flow for toolsets and services.

These state-backed investments underpin a more stable domestic revenue stream—Tokyo Electron recorded ¥1.2 trillion in Japan sales in FY2024—and accelerate joint R&D on next-generation nodes and packaging, strengthening long-term strategic collaboration.

Global trade tensions and decoupling

Ongoing US-China trade friction and export controls have pushed Tokyo Electron to diversify suppliers and markets; in FY2024 (ending Mar 2024) semiconductor-equipment revenue split showed rising sales to Taiwan and Korea as a hedge, with Japan/NA/EMEA localization increasing CAPEX exposure by an estimated mid-single-digit percentage of total capital spending.

National security and technology protection

Semiconductor equipment is now treated as a national security asset, prompting tighter export controls and limits on joint ventures; in 2024 global chip export restrictions expanded—US-led controls cover tools affecting nodes below 14nm, impacting Tokyo Electron’s addressable market and revenue mix (2023 sales ¥1.24 trillion).

Tokyo Electron must enforce strict compliance—access controls, encryption, and partner vetting—to safeguard etch/deposition IP and avoid sanctions or license denials that could disrupt supply to key customers.

Frequent government engagement is required: licensing, audits, and policy dialogue with Japan, US, and allied regulators to sustain operations and secure approvals for cross-border transfers.

- 2024 export controls broadened to advanced lithography/etch tools

- 2023 sales ¥1.24 trillion; compliance risk could affect future CAGR

- Needs: enhanced IT security, export licensing, government relations

Intergovernmental cooperation on supply chains

Agreements between Japan, the United States, and EU partners aim to build a resilient semiconductor ecosystem; G7 and US-led initiatives directed roughly $50–60 billion in public support to reshape supply chains through 2025, reducing regional disruption risks.

Tokyo Electron is central in these frameworks, contributing to standardization of advanced manufacturing processes and capturing part of a global equipment market forecasted at $90–100 billion in 2024–25.

Such cooperation stabilizes markets but forces Tokyo Electron to comply with multi-lateral export controls, subsidy rules, and cross-border IP standards, affecting capital allocation and customer engagements.

- Japan-US-EU pacts mobilized ~$50–60B public support (through 2025)

- Global semiconductor equipment market ≈ $90–100B (2024–25)

- Tokyo Electron positioned as standard-setter; faces multilateral regulatory compliance

Export Controls Trim China Sales; Japan’s ¥2.2T Push Fuels Equipment Market Shift

Geopolitical export controls (2023–24) cut China-facing sales and raised compliance costs; FY2023 China exposure ~12% of group sales. Japan’s ¥2.2T semiconductor push and ~$50–60B allied subsidies through 2025 boost domestic orders; Tokyo Electron FY2024 Japan sales ¥1.2T. Diversification increased Taiwan/Korea revenue share; global equipment market ≈$90–100B (2024–25).

| Metric | Value |

|---|---|

| China exposure | ~12% FY2023 |

| Japan investment | ¥2.2T (~$15.5B) |

| Japan sales | ¥1.2T FY2024 |

| Allied subsidies | $50–60B (thru 2025) |

| Market size | $90–100B (2024–25) |

What is included in the product

Explores how macro-environmental factors uniquely impact Tokyo Electron across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable PESTLE snapshot of Tokyo Electron that highlights regulatory, technological, and supply-chain risks for quick alignment in meetings or inclusion in client reports.

Economic factors

Semiconductor industry capital expenditure cycles

Tokyo Electron revenue is highly sensitive to capex cycles at TSMC, Intel and Samsung; TSMC’s announced 2024–25 capex of ~$44–46bn and Intel’s $20–25bn guidance for advanced nodes drive demand for advanced wafer bonders and coater/developers.

Currency exchange rate fluctuations

As a Japan-based firm with ~70–80% of sales overseas, Tokyo Electron's reported profits are sensitive to JPY/USD and JPY/EUR moves; a 10% weaker yen raised FY2024 operating profit estimates across the sector by several hundred million dollars. A weaker yen boosts export competitiveness and inflates repatriated earnings, while a stronger yen compresses margins. TEL uses layered FX hedges—forwards, options and natural hedges—to stabilize guidance and limit volatility.

Rising research and development costs

Maintaining leadership in semiconductor equipment forces Tokyo Electron to ramp R&D spending—the company invested ¥104.6 billion in R&D in FY2024, up ~7% year-on-year—to track Moore’s Law and scale into 3D integration and advanced materials.

Developing specialized tools for EUV, heterogeneous integration and new substrates drives exponential cost growth in prototype and pilot production.

Tokyo Electron must balance these investments against operating margin targets—operating profit margin was 23.1% in FY2024—while preserving cash flow for shareholders.

AI-driven demand for high-performance computing

The generative AI boom and LLM deployment drove a 2024 global data center capex surge—IDC estimates hyperscaler spending rose ~18% YoY—boosting demand for HBM and advanced logic; Tokyo Electron benefits via lithography and packaging tools tied to HBM/AI-class chips used in GPUs/CPUs.

This structural shift yields steadier growth vs consumer electronics cyclicality: server/AI compute demand underpins multiyear equipment cycles, supporting TEL revenue resilience—company reported semiconductor equipment orders recovering to ¥1.2 trillion in FY2024.

Global inflation and supply chain costs

Persistently high costs for silicon, specialty gases and logistics raised Tokyo Electron's COGS; global semiconductor material prices rose ~8-12% in 2024 while ocean freight rates remained elevated versus pre-2020 levels.

To protect margins, Tokyo Electron is optimizing procurement, hedging key inputs and implemented selective price increases—helping sustain operating margin near 20% in FY2024.

Ongoing inflation management is critical to maintain investment-grade credit metrics and fund capex for 2025 fabs and R&D.

- Raw material and component costs up ~8–12% in 2024

- Selective customer price adjustments to defend margins

- Procurement optimization and hedging underway

- Maintains operating margin ~20% in FY2024

Tokyo Electron rides capex wave, FX tailwinds, and margin pressure from rising costs

Tokyo Electron faces capex-driven demand (TSMC $44–46bn, Intel $20–25bn for 2024–25) and FX exposure—~70–80% sales overseas; a 10% weaker JPY lifted sector FY2024 operating profit by several hundred million USD. R&D ¥104.6bn (FY2024) and rising material/logistics costs (+8–12% in 2024) pressure margins; TEL kept operating margin ~23.1% and orders ~¥1.2T (FY2024).

| Metric | Value |

|---|---|

| R&D FY2024 | ¥104.6bn |

| Operating margin FY2024 | 23.1% |

| Equipment orders FY2024 | ¥1.2T |

| Material cost change 2024 | +8–12% |

| TSMC capex 2024–25 | $44–46bn |

| Intel capex guidance | $20–25bn |

Full Version Awaits

Tokyo Electron PESTLE Analysis

The preview shown here is the exact Tokyo Electron PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.