Deutsche Telekom Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Deutsche Telekom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Network Equipment Providers

Semiconductor and Hardware Dependencies

Deutsche Telekom depends on global chipmakers for CPE and handsets, and 2025 demand for AI-integrated hardware boosted silicon suppliers’ leverage—global AI chip revenue hit about $65 billion in 2024, raising vendor bargaining power. Supply shocks or export controls can delay device rollouts, hurting service contract delivery and shrinking retail hardware gross margins (hardware sales made ~€5.4 billion of revenue in 2024).

Energy Provider Influence

Operating 38+ data centers and ~100,000 mobile sites in Germany, Deutsche Telekom faces high energy demand, making utility and renewables suppliers powerful; in 2024 energy costs accounted for an estimated €1.1–1.3 billion of OpEx. With Germany/EU green mandates, DT relies on renewable producers and PPAs—about 40% of its power covered by long‑term contracts—so pricing shifts in wind/solar markets directly affect unit costs. Even with PPAs, 2022–24 wholesale price volatility (peaks >€300/MWh) shows exposure remains material to margins.

Content and Media Licensing Costs

For MagentaTV and IPTV, Deutsche Telekom negotiates with global media conglomerates and sports leagues whose exclusive rights drive fiber-to-the-home retention; these licensors wield strong leverage because unique live sports and premium shows are key churn reducers.

Rising licensing fees—estimated industry-wide increases of 8–12% in 2024 and reported pay-TV rights growth (UEFA/CPL deals) pushing single-event rights into hundreds of millions—compress service margins and force higher bundle costs or wholesale cuts in content scope.

- Exclusive rights = high supplier leverage

- 2024–25 licensing inflation ~8–12%

- Major sports deals cost hundreds of millions

- Margin pressure forces price hikes or content cuts

Specialized Labor and IT Talent

The move to software-defined networking and cloud-native ops raises Deutsche Telekom’s reliance on senior IT staff and niche consultants, increasing supplier power as headcount needs shift from hardware to software roles.

European shortages of cybersecurity and AI engineers persisted into late 2025, with vacancy rates for ICT specialists at 3.8% EU-wide and senior cloud/security salaries 20–35% above telecom averages, strengthening wage and contract leverage.

Specialized tech firms and talent now extract longer contracts, higher retention bonuses, and IP-sensitive terms, raising operating costs and strategic risk for Deutsche Telekom.

- ICT vacancy rate EU (2025 Q4): 3.8%

- Senior cloud/cyber pay premium: 20–35%

- Increased reliance: shift to SDN/cloud-native

Supplier squeeze: 5G, AI chips, energy and talent drive Deutsche Telekom margin risk

| Factor | Key metric |

|---|---|

| 5G vendors | Ericsson+Nokia ~60% (2024) |

| AI chips | $65bn revenue (2024) |

| Energy Opex | €1.1–1.3bn (2024) |

| Content inflation | 8–12% (2024) |

| ICT vacancy | 3.8% EU (2025 Q4) |

What is included in the product

Tailored for Deutsche Telekom, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its pricing power and strategic positioning.

One-sheet Porter's Five Forces for Deutsche Telekom—clear, deck-ready summary that quantifies competitive pressure across rivals, suppliers, buyers, new entrants, and substitutes to speed strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Consumer Segments

Individual retail customers in Germany and Europe use price-comparison platforms like Check24 and Verivox, driving high sensitivity to monthly fees; Germany’s average mobile ARPU fell to about €13.5 in 2024, pressuring premium pricing.

Deutsche Telekom’s premium positioning (Magenta) meets competition from discount MVNOs such as 1&1 Drillisch and Aldi Talk, which captured ~18% combined market share in Germany by 2024, forcing constant value justification.

This price sensitivity constrains Telekom’s ability to raise prices: a 5–7% annual price hike risks material churn given reported retail churn rates of ~1.2% monthly in 2024, so increases must be tied to clear service upgrades.

Low Switching Costs for Mobile Users

EU rules now require number portability within one working day, and as of 2025 about 40% of EU mobile plans support eSIM-only profiles, cutting SIM swap friction and letting users switch instantly.

This low switching cost raises customer bargaining power over Deutsche Telekom, driving churn when rivals offer aggressive promos—Germany saw a 6.2% mobile churn rate in 2024.

Operators respond with shorter-term discounts and bundled offers, compressing ARPU pressure; DT reported flat mobile service revenue growth of 0.5% in 2024, showing margin sensitivity.

Volume Leverage of Corporate Clients

Large enterprise and government clients routinely demand bespoke ICT and cloud contracts with volume discounts; top 100 corporate accounts accounted for about 18% of Deutsche Telekom Group revenue in 2024, so pricing pressure is material.

These B2B buyers run formal tenders and require strict SLAs, forcing DT to bid aggressively on price, service levels, and integration, compressing margins on large deals.

Loss of a single major account can cut regional revenue by several percentage points; in 2023 DT recorded a 2–5% revenue swing in affected regions after key contract changes.

Demand for Integrated Service Bundles

Customers now expect bundles combining mobile, fixed broadband and streaming; Deutsche Telekom reported 33.4 million fixed-network retail lines and 49.8 million mobile contracts in 2024, pushing DT to price bundles below standalone margins to protect uptake.

Subscribers threaten unbundling at renewal to extract discounts or perks, and DT’s MagentaEINS bundle mix lifted ARPU resilience—average revenue per user stayed near €22–€24 in 2024 despite promotional pressure.

- Bundling necessary to retain cross-sell: 33.4M fixed lines

- Price pressure: ARPU €22–€24 (2024)

- Negotiation leverage: churn risk rises at renewal

Informed Decision Making through Digital Transparency

- 90% Germany 5G population reach (2025)

- ~15% advertised vs. measured broadband gap

- 12% churn risk after 3h outages (2024)

Customers wield pricing power—low switching costs, MVNOs & big-client revenue risk

Customers hold strong bargaining power: low switching costs (one-day portability, rising eSIM adoption ~40% in 2025), price comparison sites, and MVNOs (1&1 Drillisch + Aldi ~18% share in 2024) pressure ARPU (€13.5 mobile, €22–24 bundled in 2024) and force promotional/ bundled pricing; top-100 corporate clients made ~18% of group revenue in 2024, creating material bid-driven margin risk.

| Metric | 2024–25 |

|---|---|

| Mobile ARPU | €13.5 (2024) |

| Bundled ARPU | €22–24 (2024) |

| MVNO share | ~18% (2024) |

| Top-100 clients rev | ~18% group (2024) |

| 5G reach | 90% population (2025) |

Full Version Awaits

Deutsche Telekom Porter's Five Forces Analysis

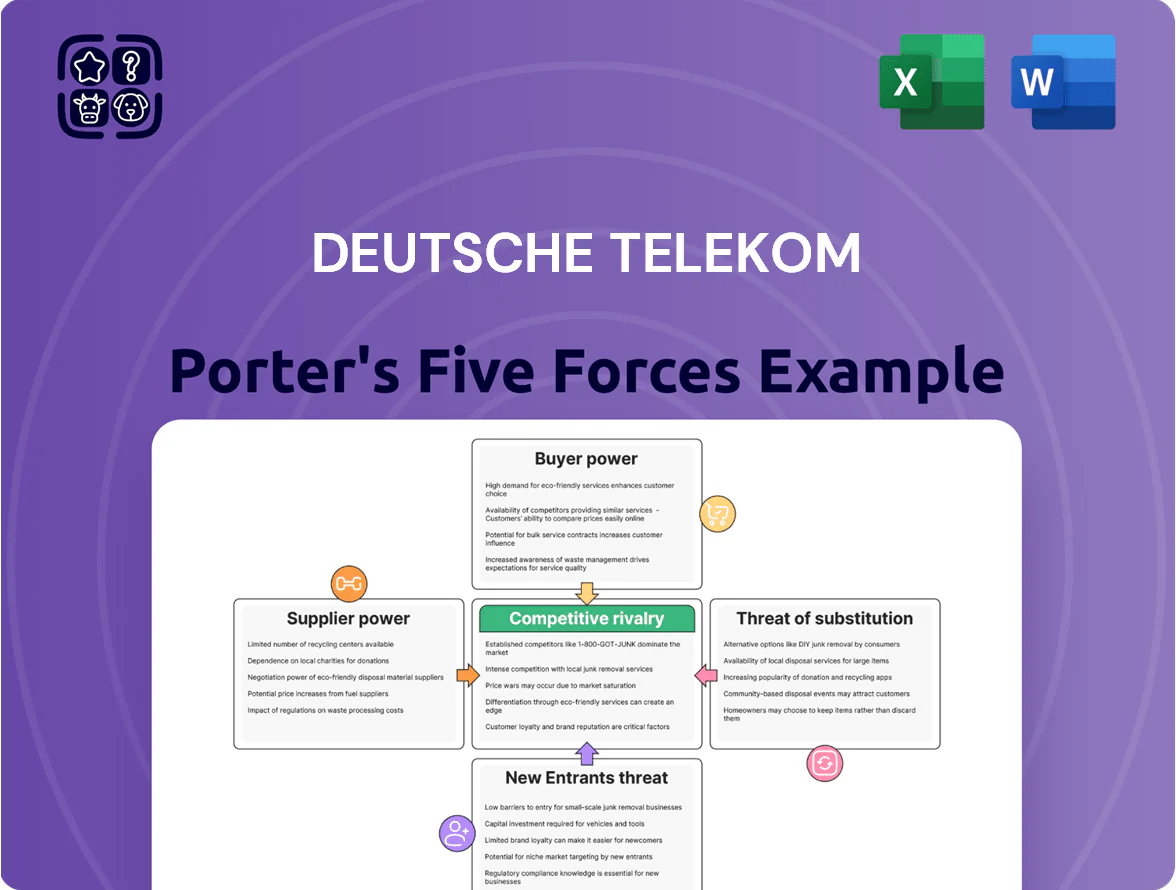

This preview shows the exact Deutsche Telekom Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, comprehensive, and ready to use; it covers competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with actionable insights.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Deutsche Telekom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Network Equipment Providers

Semiconductor and Hardware Dependencies

Deutsche Telekom depends on global chipmakers for CPE and handsets, and 2025 demand for AI-integrated hardware boosted silicon suppliers’ leverage—global AI chip revenue hit about $65 billion in 2024, raising vendor bargaining power. Supply shocks or export controls can delay device rollouts, hurting service contract delivery and shrinking retail hardware gross margins (hardware sales made ~€5.4 billion of revenue in 2024).

Energy Provider Influence

Operating 38+ data centers and ~100,000 mobile sites in Germany, Deutsche Telekom faces high energy demand, making utility and renewables suppliers powerful; in 2024 energy costs accounted for an estimated €1.1–1.3 billion of OpEx. With Germany/EU green mandates, DT relies on renewable producers and PPAs—about 40% of its power covered by long‑term contracts—so pricing shifts in wind/solar markets directly affect unit costs. Even with PPAs, 2022–24 wholesale price volatility (peaks >€300/MWh) shows exposure remains material to margins.

Content and Media Licensing Costs

For MagentaTV and IPTV, Deutsche Telekom negotiates with global media conglomerates and sports leagues whose exclusive rights drive fiber-to-the-home retention; these licensors wield strong leverage because unique live sports and premium shows are key churn reducers.

Rising licensing fees—estimated industry-wide increases of 8–12% in 2024 and reported pay-TV rights growth (UEFA/CPL deals) pushing single-event rights into hundreds of millions—compress service margins and force higher bundle costs or wholesale cuts in content scope.

- Exclusive rights = high supplier leverage

- 2024–25 licensing inflation ~8–12%

- Major sports deals cost hundreds of millions

- Margin pressure forces price hikes or content cuts

Specialized Labor and IT Talent

The move to software-defined networking and cloud-native ops raises Deutsche Telekom’s reliance on senior IT staff and niche consultants, increasing supplier power as headcount needs shift from hardware to software roles.

European shortages of cybersecurity and AI engineers persisted into late 2025, with vacancy rates for ICT specialists at 3.8% EU-wide and senior cloud/security salaries 20–35% above telecom averages, strengthening wage and contract leverage.

Specialized tech firms and talent now extract longer contracts, higher retention bonuses, and IP-sensitive terms, raising operating costs and strategic risk for Deutsche Telekom.

- ICT vacancy rate EU (2025 Q4): 3.8%

- Senior cloud/cyber pay premium: 20–35%

- Increased reliance: shift to SDN/cloud-native

Supplier squeeze: 5G, AI chips, energy and talent drive Deutsche Telekom margin risk

| Factor | Key metric |

|---|---|

| 5G vendors | Ericsson+Nokia ~60% (2024) |

| AI chips | $65bn revenue (2024) |

| Energy Opex | €1.1–1.3bn (2024) |

| Content inflation | 8–12% (2024) |

| ICT vacancy | 3.8% EU (2025 Q4) |

What is included in the product

Tailored for Deutsche Telekom, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats shaping its pricing power and strategic positioning.

One-sheet Porter's Five Forces for Deutsche Telekom—clear, deck-ready summary that quantifies competitive pressure across rivals, suppliers, buyers, new entrants, and substitutes to speed strategic decisions.

Customers Bargaining Power

High Price Sensitivity in Consumer Segments

Individual retail customers in Germany and Europe use price-comparison platforms like Check24 and Verivox, driving high sensitivity to monthly fees; Germany’s average mobile ARPU fell to about €13.5 in 2024, pressuring premium pricing.

Deutsche Telekom’s premium positioning (Magenta) meets competition from discount MVNOs such as 1&1 Drillisch and Aldi Talk, which captured ~18% combined market share in Germany by 2024, forcing constant value justification.

This price sensitivity constrains Telekom’s ability to raise prices: a 5–7% annual price hike risks material churn given reported retail churn rates of ~1.2% monthly in 2024, so increases must be tied to clear service upgrades.

Low Switching Costs for Mobile Users

EU rules now require number portability within one working day, and as of 2025 about 40% of EU mobile plans support eSIM-only profiles, cutting SIM swap friction and letting users switch instantly.

This low switching cost raises customer bargaining power over Deutsche Telekom, driving churn when rivals offer aggressive promos—Germany saw a 6.2% mobile churn rate in 2024.

Operators respond with shorter-term discounts and bundled offers, compressing ARPU pressure; DT reported flat mobile service revenue growth of 0.5% in 2024, showing margin sensitivity.

Volume Leverage of Corporate Clients

Large enterprise and government clients routinely demand bespoke ICT and cloud contracts with volume discounts; top 100 corporate accounts accounted for about 18% of Deutsche Telekom Group revenue in 2024, so pricing pressure is material.

These B2B buyers run formal tenders and require strict SLAs, forcing DT to bid aggressively on price, service levels, and integration, compressing margins on large deals.

Loss of a single major account can cut regional revenue by several percentage points; in 2023 DT recorded a 2–5% revenue swing in affected regions after key contract changes.

Demand for Integrated Service Bundles

Customers now expect bundles combining mobile, fixed broadband and streaming; Deutsche Telekom reported 33.4 million fixed-network retail lines and 49.8 million mobile contracts in 2024, pushing DT to price bundles below standalone margins to protect uptake.

Subscribers threaten unbundling at renewal to extract discounts or perks, and DT’s MagentaEINS bundle mix lifted ARPU resilience—average revenue per user stayed near €22–€24 in 2024 despite promotional pressure.

- Bundling necessary to retain cross-sell: 33.4M fixed lines

- Price pressure: ARPU €22–€24 (2024)

- Negotiation leverage: churn risk rises at renewal

Informed Decision Making through Digital Transparency

- 90% Germany 5G population reach (2025)

- ~15% advertised vs. measured broadband gap

- 12% churn risk after 3h outages (2024)

Customers wield pricing power—low switching costs, MVNOs & big-client revenue risk

Customers hold strong bargaining power: low switching costs (one-day portability, rising eSIM adoption ~40% in 2025), price comparison sites, and MVNOs (1&1 Drillisch + Aldi ~18% share in 2024) pressure ARPU (€13.5 mobile, €22–24 bundled in 2024) and force promotional/ bundled pricing; top-100 corporate clients made ~18% of group revenue in 2024, creating material bid-driven margin risk.

| Metric | 2024–25 |

|---|---|

| Mobile ARPU | €13.5 (2024) |

| Bundled ARPU | €22–24 (2024) |

| MVNO share | ~18% (2024) |

| Top-100 clients rev | ~18% group (2024) |

| 5G reach | 90% population (2025) |

Full Version Awaits

Deutsche Telekom Porter's Five Forces Analysis

This preview shows the exact Deutsche Telekom Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, comprehensive, and ready to use; it covers competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with actionable insights.