Telenet Group Holding Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

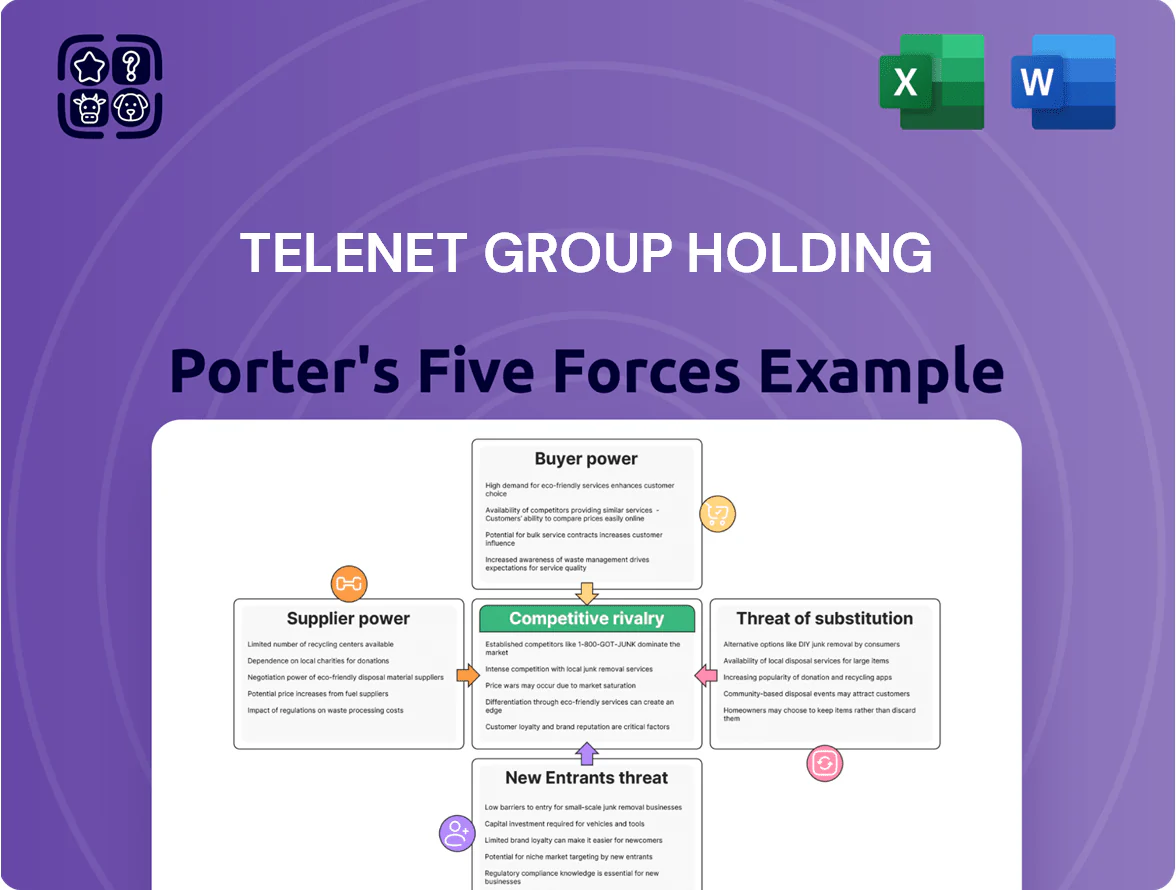

Telenet faces moderate rivalry underpinned by strong brand and integrated fixed-mobile offerings, while customer bargaining power is elevated by price-sensitive consumers and alternative providers; supplier influence is contained but technology vendors matter, and threats from substitutes and new entrants are tempered by high infrastructure costs and regulatory barriers. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Telenet Group Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Network Equipment Vendors

Telenet depends on a few global vendors—notably Nokia and Ericsson—for 5G and fiber builds, giving suppliers strong leverage over pricing, SLAs, and spare-part margins; vendor equipment accounted for an estimated 65–75% of capital deployment costs in 2024. Switching costs are high: interoperability, staff retraining, and new OSS/BSS integration can add 10–20% to project CAPEX and delay rollouts by 6–12 months, reinforcing supplier bargaining power.

Rising Costs of Premium Content Rights

As a TV operator, Telenet must buy rights for UEFA, Belgian Pro League and Hollywood libraries; these suppliers have high leverage because content is unique and non-substitutable.

Global streamers like Netflix and Amazon pushed rights prices up — UEFA domestic rights rose ~35% in 2023-24; Telenet’s content procurement costs grew, contributing to its 2024 TV segment margin pressure (TV EBITDA margin down ~2 pp to ~18%).

Dependence on Energy and Utility Providers

Telenet’s extensive data centers and national network need large electricity volumes—Belgium’s power use for telecoms rose ~6% in 2023—so Telenet is exposed to energy-market swings.

Belgian utilities remain concentrated despite regulation; industrial gas and power contracts give limited bargaining room, pressuring Telenet’s ability to secure lower rates.

Volatile prices hit margins and capex plans: in 2022–24 Belgian wholesale power jumped ~40%, forcing higher operating costs and shifting long‑term infrastructure timing.

Specialized Labor and IT Talent

The Belgian shortage of cybersecurity experts and network engineers boosts supplier bargaining power; estimates show a 20–30% gap in available specialists for telecoms in 2024, raising recruitment costs for Telenet.

Telenet needs continuous access to this talent to secure networks and drive its digital-transformation projects, forcing longer contracts and rapid hiring.

High cross-sector demand means Telenet must offer premium pay and favorable vendor terms—IT contractor rates rose ~12% in Belgium in 2024.

- 20–30% specialist shortfall (2024)

- IT contractor rates +12% (2024)

- Longer contracts, premium pay required

Mobile Handset Manufacturer Influence

Rising supplier power and shortages squeeze Telenet’s costs, capex and rollouts

Telenet faces high supplier power across network vendors (Nokia/Ericsson ~65–75% of capex 2024), content rights (UEFA rights +35% 2023–24) and device makers (Apple/Samsung ~60% global high‑end share 2024), plus energy and talent shortages (Belgian telecom power +40% 2022–24; 20–30% specialist shortfall 2024) that raise costs, working capital and rollout delays.

| Item | Key metric |

|---|---|

| Vendor capex share | 65–75% (2024) |

| UEFA rights change | +35% (2023–24) |

| Device market share | Apple/Samsung ~60% (2024) |

| Power price move | +40% (2022–24) |

| Specialist shortfall | 20–30% (2024) |

What is included in the product

Tailored exclusively for Telenet Group Holding, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier bargaining power, entry barriers, substitute threats, and disruptive forces affecting market share and profitability.

Concise Porter's Five Forces snapshot for Telenet—quickly identify competitive pressures and prioritize strategic moves to reduce churn and protect ARPU.

Customers Bargaining Power

High Price Sensitivity in Residential Markets

Belgian consumers now prioritize price-to-performance, with 62% citing cost as the top factor in 2024 ARCEP-style surveys, driving intense scrutiny of monthly internet and mobile fees; average household broadband ARPU fell 4% to €32.5 in FY2024. With market penetration near 95% in fixed broadband, customers switch for promos and cheaper bundles, so Telenet must tweak pricing and bundles frequently to avoid churn above the industry ~14% annual rate.

Impact of Digital Comparison Tools

The rise of online comparison platforms lets Belgian consumers compare Telenet Group Holding with Proximus and Orange in real time; price-comparison sites and apps increased search activity for telecom plans by about 28% in 2024, according to Statista EU telecom data. This transparency makes value-for-money obvious, constraining Telenet’s ability to sustain premium pricing as customers switch to offers with similar speeds or bundles.

Low Switching Costs for Mobile Users

Belgian law streamlined mobile number portability in 2015 and porting now takes under one business day on average, which lowered switching frictions and raised churn risk; Belgian mobile churn hit about 18% in 2024, so Telenet (market cap €3.6bn at end-2024) must boost retention spend—its 2024 churn-led marketing and loyalty costs rose ~12% to protect ARPU—by investing in CX and loyalty programs to counter quick customer migration.

Demand for Converged Service Bundles

Modern Belgian households favor quadruple-play bundles (fixed, mobile, internet, TV); in 2024 around 58% of EU broadband subscribers chose converged packages, raising customer stickiness for Telenet but increasing bargaining power for discounts.

Because a switch loses whole-household ARPU—Telenet reported group ARPU €56.4 in FY2024—competitors with better-priced bundles can capture full household revenue in one churn event, intensifying price pressure.

- 58% EU broadband users chose converged bundles in 2024

- Telenet FY2024 ARPU €56.4

- Quadruple-play increases retention but raises discount demands

- Competitor win = full household revenue lost at once

Wholesale and Enterprise Negotiation Leverage

Large enterprise and government clients secure high-volume contracts that boost their bargaining power at renewals; in 2024 Telenet reported B2B revenue around EUR 700m, so a single major account loss can dent annual performance notably.

These buyers run competitive tenders that pressure Telenet to cut margins for multi-year SLAs; public-sector procurement often forces price concessions exceeding 5–10% on initial offers.

- High-volume clients = strong leverage

- 2024 B2B revenue ~EUR 700m

- Competitive bids force 5–10%+ margin cuts

- Single large account loss materially affects revenue

Rising comparison searches and 58% bundle uptake squeeze Telenet ARPU and margins

Customers wield strong price leverage: FY2024 group ARPU €56.4, household broadband ARPU €32.5 (down 4%), fixed broadband penetration ~95%, annual churn ~14% (mobile ~18%), B2B revenue ~€700m; price-comparison search activity rose ~28% in 2024, and 58% of EU subscribers chose converged bundles—boosting switch-value and discount pressure on Telenet.

| Metric | 2024 |

|---|---|

| Group ARPU | €56.4 |

| Household broadband ARPU | €32.5 (-4%) |

| Fixed broadband penetration | ~95% |

| Annual churn (overall/mobile) | ~14% / 18% |

| B2B revenue | ~€700m |

| Comparison search rise | +28% |

| Converged bundle uptake | 58% |

Same Document Delivered

Telenet Group Holding Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Telenet Group Holding you'll receive—fully formatted, professionally written, and ready for immediate download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Telenet faces moderate rivalry underpinned by strong brand and integrated fixed-mobile offerings, while customer bargaining power is elevated by price-sensitive consumers and alternative providers; supplier influence is contained but technology vendors matter, and threats from substitutes and new entrants are tempered by high infrastructure costs and regulatory barriers. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Telenet Group Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Network Equipment Vendors

Telenet depends on a few global vendors—notably Nokia and Ericsson—for 5G and fiber builds, giving suppliers strong leverage over pricing, SLAs, and spare-part margins; vendor equipment accounted for an estimated 65–75% of capital deployment costs in 2024. Switching costs are high: interoperability, staff retraining, and new OSS/BSS integration can add 10–20% to project CAPEX and delay rollouts by 6–12 months, reinforcing supplier bargaining power.

Rising Costs of Premium Content Rights

As a TV operator, Telenet must buy rights for UEFA, Belgian Pro League and Hollywood libraries; these suppliers have high leverage because content is unique and non-substitutable.

Global streamers like Netflix and Amazon pushed rights prices up — UEFA domestic rights rose ~35% in 2023-24; Telenet’s content procurement costs grew, contributing to its 2024 TV segment margin pressure (TV EBITDA margin down ~2 pp to ~18%).

Dependence on Energy and Utility Providers

Telenet’s extensive data centers and national network need large electricity volumes—Belgium’s power use for telecoms rose ~6% in 2023—so Telenet is exposed to energy-market swings.

Belgian utilities remain concentrated despite regulation; industrial gas and power contracts give limited bargaining room, pressuring Telenet’s ability to secure lower rates.

Volatile prices hit margins and capex plans: in 2022–24 Belgian wholesale power jumped ~40%, forcing higher operating costs and shifting long‑term infrastructure timing.

Specialized Labor and IT Talent

The Belgian shortage of cybersecurity experts and network engineers boosts supplier bargaining power; estimates show a 20–30% gap in available specialists for telecoms in 2024, raising recruitment costs for Telenet.

Telenet needs continuous access to this talent to secure networks and drive its digital-transformation projects, forcing longer contracts and rapid hiring.

High cross-sector demand means Telenet must offer premium pay and favorable vendor terms—IT contractor rates rose ~12% in Belgium in 2024.

- 20–30% specialist shortfall (2024)

- IT contractor rates +12% (2024)

- Longer contracts, premium pay required

Mobile Handset Manufacturer Influence

Rising supplier power and shortages squeeze Telenet’s costs, capex and rollouts

Telenet faces high supplier power across network vendors (Nokia/Ericsson ~65–75% of capex 2024), content rights (UEFA rights +35% 2023–24) and device makers (Apple/Samsung ~60% global high‑end share 2024), plus energy and talent shortages (Belgian telecom power +40% 2022–24; 20–30% specialist shortfall 2024) that raise costs, working capital and rollout delays.

| Item | Key metric |

|---|---|

| Vendor capex share | 65–75% (2024) |

| UEFA rights change | +35% (2023–24) |

| Device market share | Apple/Samsung ~60% (2024) |

| Power price move | +40% (2022–24) |

| Specialist shortfall | 20–30% (2024) |

What is included in the product

Tailored exclusively for Telenet Group Holding, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier bargaining power, entry barriers, substitute threats, and disruptive forces affecting market share and profitability.

Concise Porter's Five Forces snapshot for Telenet—quickly identify competitive pressures and prioritize strategic moves to reduce churn and protect ARPU.

Customers Bargaining Power

High Price Sensitivity in Residential Markets

Belgian consumers now prioritize price-to-performance, with 62% citing cost as the top factor in 2024 ARCEP-style surveys, driving intense scrutiny of monthly internet and mobile fees; average household broadband ARPU fell 4% to €32.5 in FY2024. With market penetration near 95% in fixed broadband, customers switch for promos and cheaper bundles, so Telenet must tweak pricing and bundles frequently to avoid churn above the industry ~14% annual rate.

Impact of Digital Comparison Tools

The rise of online comparison platforms lets Belgian consumers compare Telenet Group Holding with Proximus and Orange in real time; price-comparison sites and apps increased search activity for telecom plans by about 28% in 2024, according to Statista EU telecom data. This transparency makes value-for-money obvious, constraining Telenet’s ability to sustain premium pricing as customers switch to offers with similar speeds or bundles.

Low Switching Costs for Mobile Users

Belgian law streamlined mobile number portability in 2015 and porting now takes under one business day on average, which lowered switching frictions and raised churn risk; Belgian mobile churn hit about 18% in 2024, so Telenet (market cap €3.6bn at end-2024) must boost retention spend—its 2024 churn-led marketing and loyalty costs rose ~12% to protect ARPU—by investing in CX and loyalty programs to counter quick customer migration.

Demand for Converged Service Bundles

Modern Belgian households favor quadruple-play bundles (fixed, mobile, internet, TV); in 2024 around 58% of EU broadband subscribers chose converged packages, raising customer stickiness for Telenet but increasing bargaining power for discounts.

Because a switch loses whole-household ARPU—Telenet reported group ARPU €56.4 in FY2024—competitors with better-priced bundles can capture full household revenue in one churn event, intensifying price pressure.

- 58% EU broadband users chose converged bundles in 2024

- Telenet FY2024 ARPU €56.4

- Quadruple-play increases retention but raises discount demands

- Competitor win = full household revenue lost at once

Wholesale and Enterprise Negotiation Leverage

Large enterprise and government clients secure high-volume contracts that boost their bargaining power at renewals; in 2024 Telenet reported B2B revenue around EUR 700m, so a single major account loss can dent annual performance notably.

These buyers run competitive tenders that pressure Telenet to cut margins for multi-year SLAs; public-sector procurement often forces price concessions exceeding 5–10% on initial offers.

- High-volume clients = strong leverage

- 2024 B2B revenue ~EUR 700m

- Competitive bids force 5–10%+ margin cuts

- Single large account loss materially affects revenue

Rising comparison searches and 58% bundle uptake squeeze Telenet ARPU and margins

Customers wield strong price leverage: FY2024 group ARPU €56.4, household broadband ARPU €32.5 (down 4%), fixed broadband penetration ~95%, annual churn ~14% (mobile ~18%), B2B revenue ~€700m; price-comparison search activity rose ~28% in 2024, and 58% of EU subscribers chose converged bundles—boosting switch-value and discount pressure on Telenet.

| Metric | 2024 |

|---|---|

| Group ARPU | €56.4 |

| Household broadband ARPU | €32.5 (-4%) |

| Fixed broadband penetration | ~95% |

| Annual churn (overall/mobile) | ~14% / 18% |

| B2B revenue | ~€700m |

| Comparison search rise | +28% |

| Converged bundle uptake | 58% |

Same Document Delivered

Telenet Group Holding Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Telenet Group Holding you'll receive—fully formatted, professionally written, and ready for immediate download after purchase.