Teleperformance Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

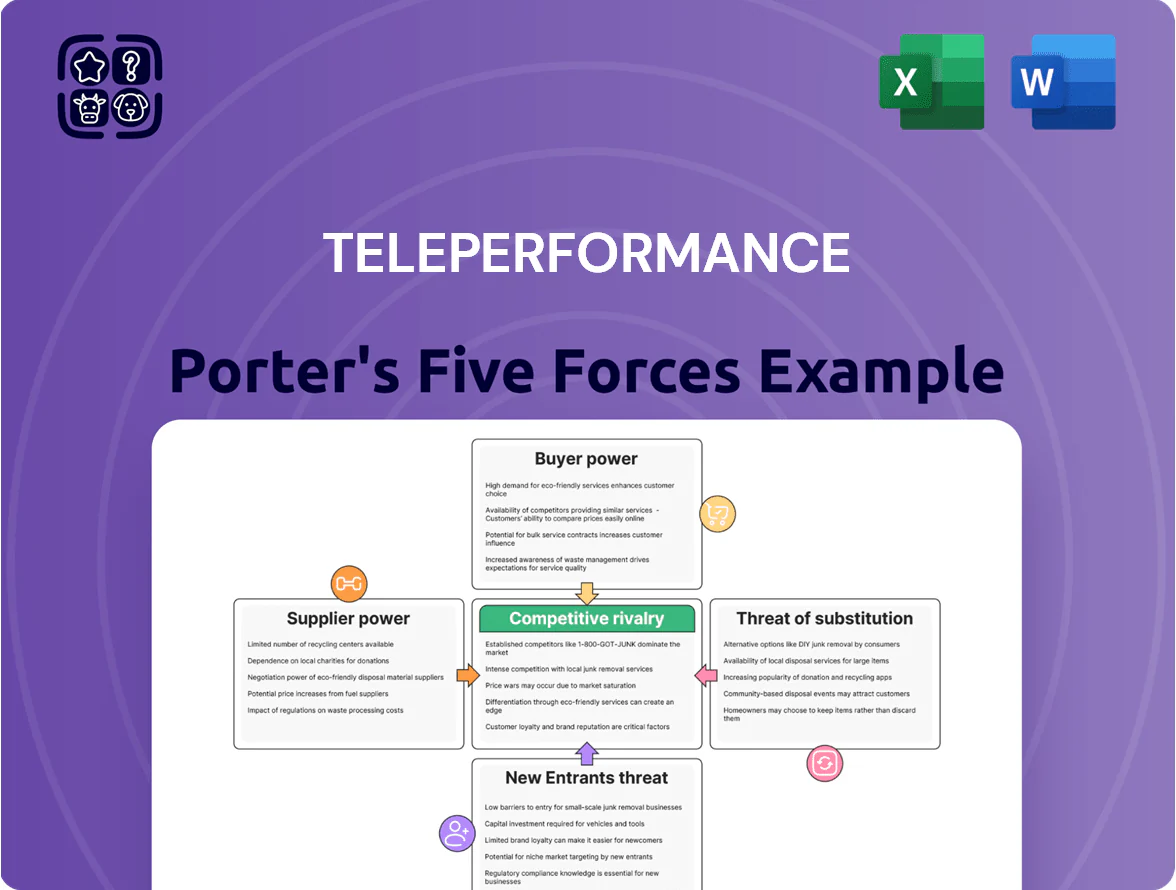

Teleperformance faces moderate supplier power but high buyer expectations and intense rivalry from global and regional BPO players, while technological change and automation heighten substitute threats and lower entry barriers in niche segments.

Suppliers Bargaining Power

Dominance of Enterprise Technology Providers

Teleperformance depends on enterprise software for CRM, cloud, and cybersecurity, with Microsoft and AWS powering large parts of its global stack; Microsoft reported Azure revenue growth to $110bn FY2024 and AWS $90bn FY2024, underlining their scale and leverage. Any price rise or outage at these providers can squeeze Teleperformance’s operating margin (14.5% adjusted EBITA in FY2024) and harm service continuity across 90+ countries. High switching costs and few equivalent, enterprise-grade alternatives keep supplier bargaining power high.

Labor Market Dynamics and Specialized Talent

Teleperformance’s primary input is its 420,000-strong global workforce (2024), so labor acts as a key supplier and cost driver.

In niches like multilingual support and healthcare tech, demand for scarce skills raises employee bargaining power as openings exceed qualified supply; churn in some markets hit 40% in 2023.

Wage inflation—average annual pay rises of 6–8% in key markets (2022–24)—and continuous AI upskilling needs strengthen workers’ leverage.

The firm must trade higher pay and training costs against margin pressure to keep staff for high-value contracts.

Geographic and Real Estate Dependencies

Physical hubs remain essential for Teleperformance’s security-sensitive work despite TP Cloud Campus adoption; in 2024 about 35% of seats were in-site in Philippines, India, and Colombia. Real estate and facility managers in those BPO hubs hold moderate leverage on rents and uptime, but Teleperformance’s ability to shift labor across 80+ countries and expand remote capacity reduces supplier power. This geographic flexibility helped negotiate lower lease renewals in 2023–24, cutting occupancy cost growth to under 2% YoY.

Specialized AI and Automation Vendors

Vendors of proprietary large language models (LLMs) and automation tools have rising leverage as buyers demand AI-augmented services; by 2025, global enterprise AI spending hit about $120B, increasing supplier importance for Teleperformance.

If an AI platform becomes the de facto standard, that vendor can push higher licensing and pricing, raising Teleperformance’s operating costs and margin pressure.

Teleperformance reduces this risk by investing in in-house AI and acquiring capabilities—its 2024 tech capex rose ~15% YoY—to lower long-term dependency on external AI suppliers.

- 2025 enterprise AI spend ~$120B

- Supplier power rises if LLMs standardize

- Pricing/licensing risk hits margins

- Teleperformance 2024 tech capex +15% YoY

Telecommunications and Connectivity Providers

Stable high-speed internet and global telecom infrastructure are non-negotiable for Teleperformance’s omnichannel services; in 2024, 92% of its voice and digital delivery depended on resilient connectivity across 90+ countries.

In some developing markets Teleperformance operates, a few dominant telecoms raise supplier bargaining power—outages or price hikes can breach SLAs and hit revenues (example: 2023 outage in Market X cost an estimated $4.2m in remediation).

Teleperformance mitigates this by contracting multiple carriers and building redundancies; typical country setups use 2–4 independent providers and dedicated failover links to limit single-supplier leverage.

- Connectivity is critical: 92% of delivery tied to telecoms (2024)

- Supplier concentration in some markets raises bargaining power

- Outage risk can cause SLA breaches and millions in costs

- Mitigation: 2–4 carriers per country, redundant failovers

Suppliers Tighten Margins: Hyperscalers, Labor & Telecoms Shape 2025 Cost Risks

Suppliers hold moderate-to-high power: hyperscalers (Microsoft/AWS) and LLM vendors can squeeze margins; labor (420,000 FTEs, 2024) and telecoms in some markets add leverage via wage inflation (6–8% pa 2022–24) and outage risk. Teleperformance raised tech capex ~15% YoY in 2024 and uses 2–4 carriers per country to reduce dependence.

| Item | 2024/2025 |

|---|---|

| FTEs | 420,000 |

| Adj EBITA | 14.5% |

| Hyperscaler revs | Azure $110bn / AWS $90bn |

| AI spend | $120B (2025 est) |

| Tech capex growth | +15% YoY |

What is included in the product

Tailored exclusively for Teleperformance, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats shaping its market position and profitability.

A concise Porter's Five Forces snapshot for Teleperformance—fast clarity on competitive pressures to guide outsourcing strategy and investment decisions.

Customers Bargaining Power

Concentration of Large Enterprise Clients

Teleperformance serves dozens of Fortune 500 firms; in 2024 roughly 60% of revenue came from large enterprise accounts, creating concentration risk—loss of a major client could cut EBITDA materially (single-client revenue swings >1–3% can move margins).

These clients demand bespoke service bundles and strict KPIs (SLAs, CSAT) and use scale to push prices down at renewal, compressing Teleperformance’s pricing power and forcing higher compliance costs.

Low Switching Costs for Standardized Services

In basic customer care and routine tech support, services are largely commoditized, making switching to rivals like Concentrix or Foundever easy at contract end; industry churn averages about 17% annually for low-complexity BPO accounts (2024 data).

That low switching cost forces Teleperformance to prove superior value and efficiency continuously, or risk margin erosion.

Teleperformance counters by deeply integrating into client workflows—custom APIs, shared KPIs, and co-managed teams—raising practical switching costs and protecting revenue; integrated accounts represented roughly 42% of TP’s 2024 revenues.

Demand for Transformational Outcomes

Modern clients now demand transformational outcomes, not just labor cost savings, pushing BPOs to deliver digital CX gains; 2024 IDC data shows 62% of enterprises expect vendors to provide AI-driven customer journeys.

This elevates buyer power: customers insist on integrated AI, analytics, and measurable CSAT/NPS improvements in contracts, or they switch—Teleperformance reported 2024 revenue growth of 8.4% but must match tech expectations.

If Teleperformance misses measurable end-user gains, large buyers can move to rivals with stronger tech stacks; Teleperformance needs continuous reinvestment—it spent €228m on capex and tech in 2023—to stay competitive.

Transparency and Third-Party Benchmarking

The BPO market’s transparency — boosted by consultants and benchmarks — lets buyers compare pricing and KPIs; 2024 surveys show 62% of enterprise buyers use third-party benchmarks when renewing contracts.

Clients leverage this data to demand lower rates or higher SLAs, pushing Teleperformance to prove premium pricing with consistent NPS, AHT and CSAT metrics.

Failure to match market benchmarks risks churn; Teleperformance reported 6.8% organic growth in 2024, so transparency-linked retention is material.

- 62% of buyers use benchmarks (2024)

- Key metrics: NPS, AHT, CSAT

- 2024 organic growth: 6.8%

Vertical-Specific Regulatory Pressures

Clients in finance, healthcare, and telecom shift compliance onto Teleperformance, demanding adherence to GDPR, HIPAA, PCI-DSS and local rules; in 2024 these sectors accounted for ~48% of Teleperformance revenue (€6.8bn of €14.2bn, pro forma), amplifying client leverage.

Customers can require ISO 27001, SOC 2, and bespoke controls; breaches risk fines (GDPR up to €20m or 4% global turnover) and immediate contract termination, so clients dictate security capex and protocols.

This gives buyers strong bargaining power over Teleperformance’s operations, forcing continuous investment in certifications, audited controls, and region-specific data-residency solutions.

- ~48% revenue from regulated sectors (2024 est.)

- GDPR fines up to €20m or 4% turnover

- Requires ISO 27001, SOC 2, HIPAA, PCI-DSS

- Noncompliance → contract termination, heavy penalties

Buyers Hold the Cards: High Client Concentration, Benchmarks, and Rising Tech Defense

Buyers have high leverage: ~60% revenue from large clients (2024), 17% churn in low-complexity accounts, 42% integrated accounts raise switching costs, 62% use benchmarks, 48% revenue from regulated sectors forcing compliance spend; Teleperformance’s 2024 organic growth 6.8% and €228m tech spend (2023) show reinvestment to counter buyer pressure.

| Metric | Value |

|---|---|

| Large-client rev | ~60% |

| Churn (low complexity) | 17% |

| Integrated accounts | 42% |

| Use benchmarks | 62% |

| Regulated-sector rev | ~48% (€6.8bn) |

| Organic growth (2024) | 6.8% |

| Tech/capex (2023) | €228m |

Same Document Delivered

Teleperformance Porter's Five Forces Analysis

This preview shows the exact Teleperformance Porter’s Five Forces analysis you’ll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Teleperformance faces moderate supplier power but high buyer expectations and intense rivalry from global and regional BPO players, while technological change and automation heighten substitute threats and lower entry barriers in niche segments.

Suppliers Bargaining Power

Dominance of Enterprise Technology Providers

Teleperformance depends on enterprise software for CRM, cloud, and cybersecurity, with Microsoft and AWS powering large parts of its global stack; Microsoft reported Azure revenue growth to $110bn FY2024 and AWS $90bn FY2024, underlining their scale and leverage. Any price rise or outage at these providers can squeeze Teleperformance’s operating margin (14.5% adjusted EBITA in FY2024) and harm service continuity across 90+ countries. High switching costs and few equivalent, enterprise-grade alternatives keep supplier bargaining power high.

Labor Market Dynamics and Specialized Talent

Teleperformance’s primary input is its 420,000-strong global workforce (2024), so labor acts as a key supplier and cost driver.

In niches like multilingual support and healthcare tech, demand for scarce skills raises employee bargaining power as openings exceed qualified supply; churn in some markets hit 40% in 2023.

Wage inflation—average annual pay rises of 6–8% in key markets (2022–24)—and continuous AI upskilling needs strengthen workers’ leverage.

The firm must trade higher pay and training costs against margin pressure to keep staff for high-value contracts.

Geographic and Real Estate Dependencies

Physical hubs remain essential for Teleperformance’s security-sensitive work despite TP Cloud Campus adoption; in 2024 about 35% of seats were in-site in Philippines, India, and Colombia. Real estate and facility managers in those BPO hubs hold moderate leverage on rents and uptime, but Teleperformance’s ability to shift labor across 80+ countries and expand remote capacity reduces supplier power. This geographic flexibility helped negotiate lower lease renewals in 2023–24, cutting occupancy cost growth to under 2% YoY.

Specialized AI and Automation Vendors

Vendors of proprietary large language models (LLMs) and automation tools have rising leverage as buyers demand AI-augmented services; by 2025, global enterprise AI spending hit about $120B, increasing supplier importance for Teleperformance.

If an AI platform becomes the de facto standard, that vendor can push higher licensing and pricing, raising Teleperformance’s operating costs and margin pressure.

Teleperformance reduces this risk by investing in in-house AI and acquiring capabilities—its 2024 tech capex rose ~15% YoY—to lower long-term dependency on external AI suppliers.

- 2025 enterprise AI spend ~$120B

- Supplier power rises if LLMs standardize

- Pricing/licensing risk hits margins

- Teleperformance 2024 tech capex +15% YoY

Telecommunications and Connectivity Providers

Stable high-speed internet and global telecom infrastructure are non-negotiable for Teleperformance’s omnichannel services; in 2024, 92% of its voice and digital delivery depended on resilient connectivity across 90+ countries.

In some developing markets Teleperformance operates, a few dominant telecoms raise supplier bargaining power—outages or price hikes can breach SLAs and hit revenues (example: 2023 outage in Market X cost an estimated $4.2m in remediation).

Teleperformance mitigates this by contracting multiple carriers and building redundancies; typical country setups use 2–4 independent providers and dedicated failover links to limit single-supplier leverage.

- Connectivity is critical: 92% of delivery tied to telecoms (2024)

- Supplier concentration in some markets raises bargaining power

- Outage risk can cause SLA breaches and millions in costs

- Mitigation: 2–4 carriers per country, redundant failovers

Suppliers Tighten Margins: Hyperscalers, Labor & Telecoms Shape 2025 Cost Risks

Suppliers hold moderate-to-high power: hyperscalers (Microsoft/AWS) and LLM vendors can squeeze margins; labor (420,000 FTEs, 2024) and telecoms in some markets add leverage via wage inflation (6–8% pa 2022–24) and outage risk. Teleperformance raised tech capex ~15% YoY in 2024 and uses 2–4 carriers per country to reduce dependence.

| Item | 2024/2025 |

|---|---|

| FTEs | 420,000 |

| Adj EBITA | 14.5% |

| Hyperscaler revs | Azure $110bn / AWS $90bn |

| AI spend | $120B (2025 est) |

| Tech capex growth | +15% YoY |

What is included in the product

Tailored exclusively for Teleperformance, this Porter's Five Forces overview uncovers key competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats shaping its market position and profitability.

A concise Porter's Five Forces snapshot for Teleperformance—fast clarity on competitive pressures to guide outsourcing strategy and investment decisions.

Customers Bargaining Power

Concentration of Large Enterprise Clients

Teleperformance serves dozens of Fortune 500 firms; in 2024 roughly 60% of revenue came from large enterprise accounts, creating concentration risk—loss of a major client could cut EBITDA materially (single-client revenue swings >1–3% can move margins).

These clients demand bespoke service bundles and strict KPIs (SLAs, CSAT) and use scale to push prices down at renewal, compressing Teleperformance’s pricing power and forcing higher compliance costs.

Low Switching Costs for Standardized Services

In basic customer care and routine tech support, services are largely commoditized, making switching to rivals like Concentrix or Foundever easy at contract end; industry churn averages about 17% annually for low-complexity BPO accounts (2024 data).

That low switching cost forces Teleperformance to prove superior value and efficiency continuously, or risk margin erosion.

Teleperformance counters by deeply integrating into client workflows—custom APIs, shared KPIs, and co-managed teams—raising practical switching costs and protecting revenue; integrated accounts represented roughly 42% of TP’s 2024 revenues.

Demand for Transformational Outcomes

Modern clients now demand transformational outcomes, not just labor cost savings, pushing BPOs to deliver digital CX gains; 2024 IDC data shows 62% of enterprises expect vendors to provide AI-driven customer journeys.

This elevates buyer power: customers insist on integrated AI, analytics, and measurable CSAT/NPS improvements in contracts, or they switch—Teleperformance reported 2024 revenue growth of 8.4% but must match tech expectations.

If Teleperformance misses measurable end-user gains, large buyers can move to rivals with stronger tech stacks; Teleperformance needs continuous reinvestment—it spent €228m on capex and tech in 2023—to stay competitive.

Transparency and Third-Party Benchmarking

The BPO market’s transparency — boosted by consultants and benchmarks — lets buyers compare pricing and KPIs; 2024 surveys show 62% of enterprise buyers use third-party benchmarks when renewing contracts.

Clients leverage this data to demand lower rates or higher SLAs, pushing Teleperformance to prove premium pricing with consistent NPS, AHT and CSAT metrics.

Failure to match market benchmarks risks churn; Teleperformance reported 6.8% organic growth in 2024, so transparency-linked retention is material.

- 62% of buyers use benchmarks (2024)

- Key metrics: NPS, AHT, CSAT

- 2024 organic growth: 6.8%

Vertical-Specific Regulatory Pressures

Clients in finance, healthcare, and telecom shift compliance onto Teleperformance, demanding adherence to GDPR, HIPAA, PCI-DSS and local rules; in 2024 these sectors accounted for ~48% of Teleperformance revenue (€6.8bn of €14.2bn, pro forma), amplifying client leverage.

Customers can require ISO 27001, SOC 2, and bespoke controls; breaches risk fines (GDPR up to €20m or 4% global turnover) and immediate contract termination, so clients dictate security capex and protocols.

This gives buyers strong bargaining power over Teleperformance’s operations, forcing continuous investment in certifications, audited controls, and region-specific data-residency solutions.

- ~48% revenue from regulated sectors (2024 est.)

- GDPR fines up to €20m or 4% turnover

- Requires ISO 27001, SOC 2, HIPAA, PCI-DSS

- Noncompliance → contract termination, heavy penalties

Buyers Hold the Cards: High Client Concentration, Benchmarks, and Rising Tech Defense

Buyers have high leverage: ~60% revenue from large clients (2024), 17% churn in low-complexity accounts, 42% integrated accounts raise switching costs, 62% use benchmarks, 48% revenue from regulated sectors forcing compliance spend; Teleperformance’s 2024 organic growth 6.8% and €228m tech spend (2023) show reinvestment to counter buyer pressure.

| Metric | Value |

|---|---|

| Large-client rev | ~60% |

| Churn (low complexity) | 17% |

| Integrated accounts | 42% |

| Use benchmarks | 62% |

| Regulated-sector rev | ~48% (€6.8bn) |

| Organic growth (2024) | 6.8% |

| Tech/capex (2023) | €228m |

Same Document Delivered

Teleperformance Porter's Five Forces Analysis

This preview shows the exact Teleperformance Porter’s Five Forces analysis you’ll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.