Teleperformance PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

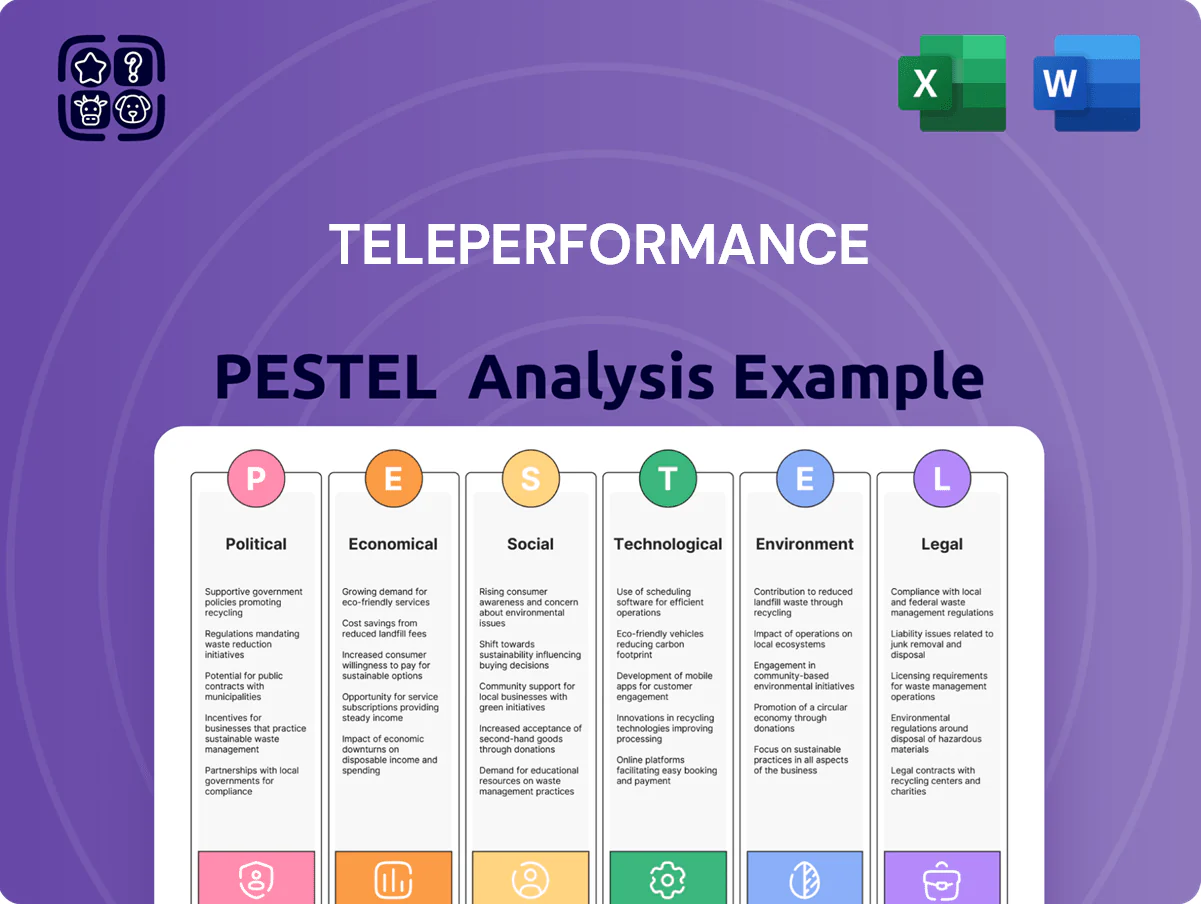

Unlock strategic clarity with our PESTLE Analysis of Teleperformance—concise, up-to-date insights into political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists. Purchase the full report to access the complete breakdown, editable files, and actionable recommendations you can apply immediately.

Political factors

Geopolitical stability in offshore delivery hubs

Teleperformance’s heavy footprint in the Philippines, India and Colombia—which accounted for roughly 55% of its 2024 FTE base—makes it highly sensitive to local political climates affecting operational continuity and employee safety.

As of late 2025 the firm must manage varying stability: Philippines localized protests, India state-level elections, and Colombia post-conflict unrest, any of which can disrupt sites and client SLAs.

Monitoring regional conflicts and government transitions is essential to mitigate sudden policy shifts, visa/worksite restrictions, or curfews that could raise contingency costs and reduce utilization rates.

Trade policies and international relations

Teleperformance’s global delivery model is sensitive to trade agreements and France’s diplomatic ties with service countries; in 2024 the group operated in 90+ countries, which helps mitigate bilateral risks.

Rising US protectionism could raise outsourcing costs—US offshore spend policies put pressure on margins where labor arbitrage shrinks; Teleperformance reported 2024 revenue of €8.8bn, highlighting reliance on scale.

Management cites geographic diversification—44% of 2024 revenue from EMEA, 33% Americas, 23% APAC—to hedge against shifts in tariffs, data transfer rules, and localization mandates.

Government incentives for digital transformation

Many governments now offer subsidies and tax credits for digital infrastructure and tech employment—EU Recovery and Resilience Facility committed over €723bn (2021–2026) and India’s production-linked incentive schemes target $26bn by 2026—measures Teleperformance uses to lower capex for its cloud contact centers and AI automation investments. Aligning expansions with national digital agendas helps Teleperformance deepen local partnerships and accelerate rollouts of digital citizen coordination services, improving ROI and reducing deployment time.

Nearshoring and friend-shoring trends

Political pressure in Western economies to shorten supply chains has boosted nearshoring to Mexico and Eastern Europe; Teleperformance reported a 12% increase in headcount in these regions in 2024 to meet client demand for proximity and political alignment.

The company has invested over $150m since 2022 in facilities and digital infrastructure in Mexico and Romania, reducing exposure to distant-region volatility and supporting service continuity during 2023–2025 geopolitical shocks.

Nearshoring and friend-shoring strengthen Teleperformance resilience by lowering cross-border risk and aligning with client compliance preferences, contributing to a more geographically diversified revenue mix now comprising roughly 28% from nearshore markets.

- 12% regional headcount growth in nearshore locations (2024)

- $150m+ investments in Mexico/Romania since 2022

- ~28% revenue from nearshore markets

- Improved continuity vs distant-region political volatility

Labor union influence and government regulation

The political landscape for collective bargaining varies across Teleperformance’s 100+ operating countries; rising pro-labor policies in markets like France and Brazil have driven wage inflation of 4–7% and added compliance costs up to 1–2% of local operating expense in 2024.

Teleperformance engages policymakers and unions proactively, investing in labor relations programs and compliance, helping contain margin pressure while preserving service levels and a 2024 adjusted EBITDA margin near 13%.

- Operates in 100+ countries with varied union regimes

- Wage inflation 4–7% in labor-positive jurisdictions (2024)

- Compliance adds ~1–2% to local OPEX in some markets

- Proactive stakeholder engagement supports 2024 adjusted EBITDA ~13%

Teleperformance: 55% FTE in PH/IN/CO raises political risk; 28% nearshore, €8.8bn rev

Teleperformance’s 55% FTE concentration in Philippines/India/Colombia (2024) raises political disruption risk; 90+ country footprint and 28% nearshore revenue mitigate bilateral shocks. Wage inflation 4–7% and compliance +1–2% OPEX pressure margins; 2024 revenue €8.8bn, adjusted EBITDA ~13%. $150m+ capex in Mexico/Romania since 2022 supports continuity.

| Metric | 2024/2022–24 |

|---|---|

| Revenue | €8.8bn |

| Adj. EBITDA | ~13% |

| FTE concentration | 55% |

| Nearshore rev. | ~28% |

| Wage inflation | 4–7% |

| Capex MX/RO | $150m+ |

What is included in the product

Explores how macro-environmental factors uniquely affect Teleperformance across Political, Economic, Social, Technological, Environmental, and Legal dimensions with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Teleperformance that eases meeting prep, supports risk discussions and market positioning, and can be dropped into presentations or shared across teams with room for region- or business-line–specific notes.

Economic factors

Global inflation and wage cost management

Persistent inflation through 2025 pushed global wage growth in BPOs toward 6–8% annually; Teleperformance reported 2024 labor cost inflation near 7%, forcing higher wage offers in key markets to curb attrition.

Management must balance competitive pay with margins—2024 adjusted EBITDA margin was about 10.5%, so sustained wage rises risk margin compression without offsetting measures.

The firm uses dynamic pricing models to pass roughly 40–60% of labor cost increases to clients and pursues automation and productivity gains to absorb remaining pressures.

Currency exchange rate volatility

As a Euro-reporting multinational, Teleperformance faces material FX risk: in 2024 roughly 40% of revenue was USD-linked and 15% GBP-linked, so a 5% USD appreciation could shave several hundred basis points off reported organic growth. Significant swings in emerging market currencies (e.g., Brazilian real, Philippine peso) also affect consolidated EBITA. The group uses forward hedges and reported €1.2bn of hedging instruments at end-2024, plus natural hedges by matching local revenues and costs where feasible.

Client outsourcing budget cycles

The global economy influences client outsourcing budgets across retail, tech and finance; IMF projected 2025 global GDP growth at 3.0% (as of Oct 2024), affecting spend capacity for Teleperformance’s client mix.

In downturns some clients cut volumes—BCG found 2023 cost-cutting led 28% of firms to reduce external services—while others increase outsourcing to save costs.

Teleperformance markets itself as a strategic, cost-efficient partner; Q3 2024 recurring revenue resilience showed limited churn, helping stabilize cash flows.

Economic growth in emerging markets

Strong GDP growth in emerging markets—4.5% in Asia and 2.1% in Latin America in 2024 IMF estimates—expands Teleperformance’s addressable client base and supports higher-margin CX services as middle classes grow.

Lower labor costs and a large skilled workforce (India and Philippines BPO talent pools >1.2 million combined) enable cost-efficient scaling and diversification beyond Western markets, reducing revenue concentration risk.

- 2024 IMF growth: Asia 4.5%, Latin America 2.1%

- India + Philippines BPO workforce >1.2M

- Diversifies revenue vs Western markets

- Rising middle class drives demand for advanced CX

Interest rates and capital allocation

The higher global interest rates in late 2025 raise Teleperformance’s cost of debt, tightening capital allocation for expansion and M&A versus 2021–2023 when rates were lower.

Management is emphasizing a strong balance sheet and free cash flow—Teleperformance reported €1.1bn FCF in 2024—favoring organic growth and dividends over leveraged deals.

- Higher borrowing costs reduce appetite for large acquisitions

- €1.1bn FCF in 2024 underpins dividends and capex

- Conservative leverage targets to preserve liquidity

Teleperformance weathers 7% labor inflation, €1.1bn FCF, hedges soften margin hit

Inflation drove 2024 labor cost increases ~7%, pressuring 2024 adj. EBITDA margin ~10.5%; Teleperformance passed 40–60% of wage rises to clients, used €1.2bn hedges and reported €1.1bn FCF. 2024 revenue mix: ~40% USD, 15% GBP; IMF 2024 GDP: Asia 4.5%, LatAm 2.1%; India+Philippines BPO workforce >1.2M; rising rates in 2025 raise borrowing costs, limiting large M&A.

| Metric | 2024 |

|---|---|

| Labor inflation | ~7% |

| Adj. EBITDA margin | ~10.5% |

| FCF | €1.1bn |

| Hedging instruments | €1.2bn |

| Revenue FX mix | USD 40%, GBP 15% |

Preview the Actual Deliverable

Teleperformance PESTLE Analysis

The preview shown here is the exact Teleperformance PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Teleperformance—concise, up-to-date insights into political, economic, social, technological, legal, and environmental forces shaping its future; ideal for investors and strategists. Purchase the full report to access the complete breakdown, editable files, and actionable recommendations you can apply immediately.

Political factors

Geopolitical stability in offshore delivery hubs

Teleperformance’s heavy footprint in the Philippines, India and Colombia—which accounted for roughly 55% of its 2024 FTE base—makes it highly sensitive to local political climates affecting operational continuity and employee safety.

As of late 2025 the firm must manage varying stability: Philippines localized protests, India state-level elections, and Colombia post-conflict unrest, any of which can disrupt sites and client SLAs.

Monitoring regional conflicts and government transitions is essential to mitigate sudden policy shifts, visa/worksite restrictions, or curfews that could raise contingency costs and reduce utilization rates.

Trade policies and international relations

Teleperformance’s global delivery model is sensitive to trade agreements and France’s diplomatic ties with service countries; in 2024 the group operated in 90+ countries, which helps mitigate bilateral risks.

Rising US protectionism could raise outsourcing costs—US offshore spend policies put pressure on margins where labor arbitrage shrinks; Teleperformance reported 2024 revenue of €8.8bn, highlighting reliance on scale.

Management cites geographic diversification—44% of 2024 revenue from EMEA, 33% Americas, 23% APAC—to hedge against shifts in tariffs, data transfer rules, and localization mandates.

Government incentives for digital transformation

Many governments now offer subsidies and tax credits for digital infrastructure and tech employment—EU Recovery and Resilience Facility committed over €723bn (2021–2026) and India’s production-linked incentive schemes target $26bn by 2026—measures Teleperformance uses to lower capex for its cloud contact centers and AI automation investments. Aligning expansions with national digital agendas helps Teleperformance deepen local partnerships and accelerate rollouts of digital citizen coordination services, improving ROI and reducing deployment time.

Nearshoring and friend-shoring trends

Political pressure in Western economies to shorten supply chains has boosted nearshoring to Mexico and Eastern Europe; Teleperformance reported a 12% increase in headcount in these regions in 2024 to meet client demand for proximity and political alignment.

The company has invested over $150m since 2022 in facilities and digital infrastructure in Mexico and Romania, reducing exposure to distant-region volatility and supporting service continuity during 2023–2025 geopolitical shocks.

Nearshoring and friend-shoring strengthen Teleperformance resilience by lowering cross-border risk and aligning with client compliance preferences, contributing to a more geographically diversified revenue mix now comprising roughly 28% from nearshore markets.

- 12% regional headcount growth in nearshore locations (2024)

- $150m+ investments in Mexico/Romania since 2022

- ~28% revenue from nearshore markets

- Improved continuity vs distant-region political volatility

Labor union influence and government regulation

The political landscape for collective bargaining varies across Teleperformance’s 100+ operating countries; rising pro-labor policies in markets like France and Brazil have driven wage inflation of 4–7% and added compliance costs up to 1–2% of local operating expense in 2024.

Teleperformance engages policymakers and unions proactively, investing in labor relations programs and compliance, helping contain margin pressure while preserving service levels and a 2024 adjusted EBITDA margin near 13%.

- Operates in 100+ countries with varied union regimes

- Wage inflation 4–7% in labor-positive jurisdictions (2024)

- Compliance adds ~1–2% to local OPEX in some markets

- Proactive stakeholder engagement supports 2024 adjusted EBITDA ~13%

Teleperformance: 55% FTE in PH/IN/CO raises political risk; 28% nearshore, €8.8bn rev

Teleperformance’s 55% FTE concentration in Philippines/India/Colombia (2024) raises political disruption risk; 90+ country footprint and 28% nearshore revenue mitigate bilateral shocks. Wage inflation 4–7% and compliance +1–2% OPEX pressure margins; 2024 revenue €8.8bn, adjusted EBITDA ~13%. $150m+ capex in Mexico/Romania since 2022 supports continuity.

| Metric | 2024/2022–24 |

|---|---|

| Revenue | €8.8bn |

| Adj. EBITDA | ~13% |

| FTE concentration | 55% |

| Nearshore rev. | ~28% |

| Wage inflation | 4–7% |

| Capex MX/RO | $150m+ |

What is included in the product

Explores how macro-environmental factors uniquely affect Teleperformance across Political, Economic, Social, Technological, Environmental, and Legal dimensions with data-backed trends and region-specific examples to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary for Teleperformance that eases meeting prep, supports risk discussions and market positioning, and can be dropped into presentations or shared across teams with room for region- or business-line–specific notes.

Economic factors

Global inflation and wage cost management

Persistent inflation through 2025 pushed global wage growth in BPOs toward 6–8% annually; Teleperformance reported 2024 labor cost inflation near 7%, forcing higher wage offers in key markets to curb attrition.

Management must balance competitive pay with margins—2024 adjusted EBITDA margin was about 10.5%, so sustained wage rises risk margin compression without offsetting measures.

The firm uses dynamic pricing models to pass roughly 40–60% of labor cost increases to clients and pursues automation and productivity gains to absorb remaining pressures.

Currency exchange rate volatility

As a Euro-reporting multinational, Teleperformance faces material FX risk: in 2024 roughly 40% of revenue was USD-linked and 15% GBP-linked, so a 5% USD appreciation could shave several hundred basis points off reported organic growth. Significant swings in emerging market currencies (e.g., Brazilian real, Philippine peso) also affect consolidated EBITA. The group uses forward hedges and reported €1.2bn of hedging instruments at end-2024, plus natural hedges by matching local revenues and costs where feasible.

Client outsourcing budget cycles

The global economy influences client outsourcing budgets across retail, tech and finance; IMF projected 2025 global GDP growth at 3.0% (as of Oct 2024), affecting spend capacity for Teleperformance’s client mix.

In downturns some clients cut volumes—BCG found 2023 cost-cutting led 28% of firms to reduce external services—while others increase outsourcing to save costs.

Teleperformance markets itself as a strategic, cost-efficient partner; Q3 2024 recurring revenue resilience showed limited churn, helping stabilize cash flows.

Economic growth in emerging markets

Strong GDP growth in emerging markets—4.5% in Asia and 2.1% in Latin America in 2024 IMF estimates—expands Teleperformance’s addressable client base and supports higher-margin CX services as middle classes grow.

Lower labor costs and a large skilled workforce (India and Philippines BPO talent pools >1.2 million combined) enable cost-efficient scaling and diversification beyond Western markets, reducing revenue concentration risk.

- 2024 IMF growth: Asia 4.5%, Latin America 2.1%

- India + Philippines BPO workforce >1.2M

- Diversifies revenue vs Western markets

- Rising middle class drives demand for advanced CX

Interest rates and capital allocation

The higher global interest rates in late 2025 raise Teleperformance’s cost of debt, tightening capital allocation for expansion and M&A versus 2021–2023 when rates were lower.

Management is emphasizing a strong balance sheet and free cash flow—Teleperformance reported €1.1bn FCF in 2024—favoring organic growth and dividends over leveraged deals.

- Higher borrowing costs reduce appetite for large acquisitions

- €1.1bn FCF in 2024 underpins dividends and capex

- Conservative leverage targets to preserve liquidity

Teleperformance weathers 7% labor inflation, €1.1bn FCF, hedges soften margin hit

Inflation drove 2024 labor cost increases ~7%, pressuring 2024 adj. EBITDA margin ~10.5%; Teleperformance passed 40–60% of wage rises to clients, used €1.2bn hedges and reported €1.1bn FCF. 2024 revenue mix: ~40% USD, 15% GBP; IMF 2024 GDP: Asia 4.5%, LatAm 2.1%; India+Philippines BPO workforce >1.2M; rising rates in 2025 raise borrowing costs, limiting large M&A.

| Metric | 2024 |

|---|---|

| Labor inflation | ~7% |

| Adj. EBITDA margin | ~10.5% |

| FCF | €1.1bn |

| Hedging instruments | €1.2bn |

| Revenue FX mix | USD 40%, GBP 15% |

Preview the Actual Deliverable

Teleperformance PESTLE Analysis

The preview shown here is the exact Teleperformance PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.