Telia PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

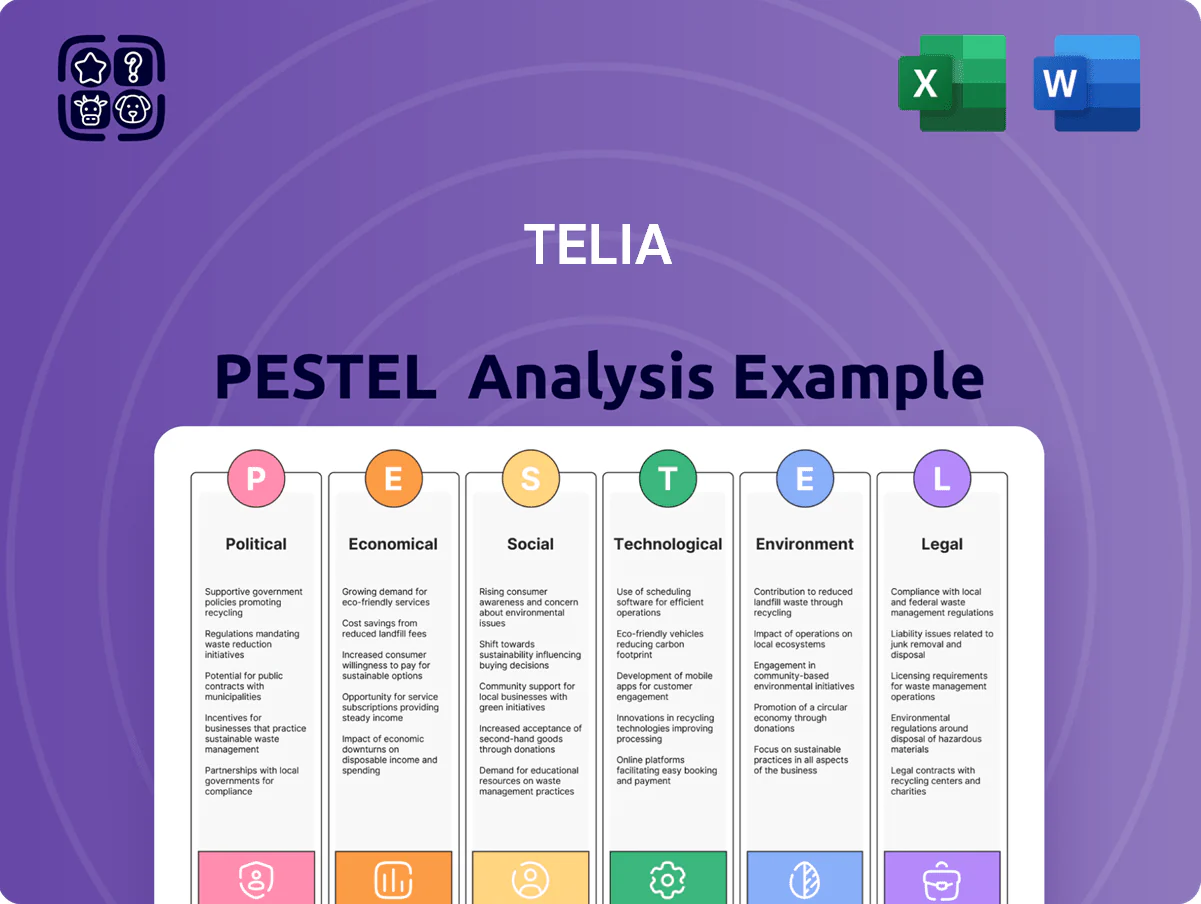

Our PESTLE Analysis for Telia maps the political, economic, social, technological, legal and environmental forces shaping its market position—revealing regulatory risks, digital transformation opportunities, and sustainability pressures. Ideal for investors and strategists, this concise briefing highlights impact and urgency. Purchase the full report to access the detailed evidence, scenarios, and actionable recommendations ready for immediate use.

Political factors

Geopolitical tensions in the Baltic region

Ongoing instability in Eastern Europe has pushed Telia to prioritize national security over expansion, redirecting an estimated 15–20% of 2024 regional CAPEX toward resilience and secure supply chains in the Baltics.

As a critical infrastructure provider in Estonia, Latvia and Lithuania, Telia faces intensified government scrutiny—compliance audits rose 40% in 2023—forcing stricter vendor vetting and stockpiling of critical network components.

This geopolitical climate requires close cooperation with defense agencies, influencing strategic investment: Telia scaled back planned border-region rollouts by ~25% in 2024 and reallocated resources to hardened sites and redundancy.

Nordic regulatory harmonization efforts

Political movements in the Nordic Council push for an integrated digital market across Sweden, Norway, Denmark and Finland, aiming to boost cross-border digital GDP—Nordic digital economy grew ~4.5% in 2024 to €420bn. Telia must balance differing national interests while lobbying for harmonized rules to enable seamless 5G roaming and pan-Nordic digital services. These shifts affect Telia’s regional structure and capital allocation, with 2025 capex guidance of SEK 14–16bn likely reprioritized toward cross-border infrastructure and spectrum coordination.

Government ownership and influence

The Swedish state holds 37.3% of Telia Company (2025 year-end), creating direct political oversight that shapes corporate governance and strategic choices. Political shifts in the Riksdag can alter expectations on dividends—Telia paid SEK 5.50 per share in 2024—and on social responsibility or potential divestments. This ownership forces Telia to balance commercial profitability with public-interest objectives and Sweden’s national digitalization targets, including the 98% broadband coverage goal by 2025.

Cybersecurity and national defense mandates

Governments in Telia's Nordic-Baltic core markets now mandate telcos as frontline defenders against state-grade cyber threats, driving Telia to expand sovereign cloud and advanced monitoring investments—Telia reported SEK 2.1bn cybersecurity capex in 2024 tied to these mandates.

These political requirements raise operating costs but reinforce Telia's role as a trusted domestic partner, supporting EBITDA resilience through secured public-sector contracts (public revenue share ~12% in 2024).

- Mandates: increased sovereign-cloud and monitoring obligations

- Cost impact: SEK 2.1bn cybersecurity capex in 2024

- Strategic benefit: ~12% revenue from public contracts, boosting domestic trust

EU digital sovereignty initiatives

The EU digital sovereignty drive shapes Telia’s procurement: Brussels targets 75% of critical infrastructure sourced within EU/EEA for strategic projects by 2027, pushing Telia to favor European vendors for core network and cloud contracts to meet compliance and funding criteria.

Political pressure to cut dependence on non-EU suppliers alters partnership choices—Telia reweights supplier mix after EU risk assessments and may incur ~2–5% higher capex for EU-aligned equipment, impacting network rollout economics.

Telia must align its roadmap with EU aims—investing in secure, interoperable European cloud and RAN solutions to support EU targets for resilient connectivity and to access public procurement and 2024–2027 EU digital infrastructure funds.

- EU target: 75% critical infrastructure EU/EEA sourcing by 2027

- Estimated 2–5% higher capex for EU-aligned vendors

- Alignment needed to access 2024–2027 EU digital funds

Telia shifts 15–20% 2024 CAPEX to security; SEK2.1bn cyber spend, EU rules raise costs

Political risks drive Telia to reallocate ~15–20% 2024 regional CAPEX to security, face 40% more compliance audits (2023), and incur SEK 2.1bn cybersecurity capex (2024); Swedish state 37.3% ownership shapes dividend and strategy; EU 75% sourcing target by 2027 may raise capex 2–5% for EU vendors.

| Metric | Value |

|---|---|

| 2024 security CAPEX reallocation | 15–20% |

| Compliance audits ↑ (2023) | 40% |

| Cybersecurity capex (2024) | SEK 2.1bn |

| Swedish state ownership (2025) | 37.3% |

| EU sourcing target (2027) | 75% |

| Estimated capex premium | 2–5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Telia across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

A concise Telia PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to support planning discussions on regulatory, technological, and market risks.

Economic factors

Inflationary pressure on operational costs

Persistent inflation across the Nordics and Baltics pushed Telia's energy, labor and hardware costs higher—Sweden's CPI averaged 6.8% in 2023 and Estonia 5.6%—increasing OPEX and capex for network upgrades.

Telia implemented selective price increases in 2023–24, but the lag between cost hikes and revenue realization squeezed 2024 adjusted EBIT margin to about 21.5%, per company reports.

Rising interest rates raised average cost of debt; Telia's net finance costs rose to roughly SEK 3.2 billion in 2024, making active debt management vital to protect the balance sheet.

Currency volatility in non-Euro markets

Fluctuations in the Swedish krona (SEK) and Norwegian krone (NOK) versus the euro and USD materially affect Telia’s reported EBIT and procurement; SEK fell ~6% and NOK ~4% vs EUR in 2024, magnifying EUR/USD-priced equipment costs and raising capex needs by an estimated SEK 1.2–1.8 billion annually.

With ~65% of network hardware priced in USD/EUR, a 5% local-currency weakening can increase procurement spend by roughly 3–4% of capex, squeezing free cash flow in 2024–25.

Telia uses FX hedges and natural offsets across Nordic operations, but persistent SEK/NOK depreciation since 2023 has reduced hedge effectiveness, leaving long-term currency trends to significantly shape investment capacity and reported earnings.

Consumer spending power contraction

Economic slowdowns in Telia’s core Nordic and Baltic markets drove retail price sensitivity in 2024–2025, with consumer discretionary spending down ~2–3% YoY and premium-package churn rising ~1.5–2 ppt; Telia faces pressure to trade margin for retention. Balancing premium positioning with value bundles is essential as handset sales fell ~12% in 2024, shifting strategy toward service-based recurring revenue, which grew ~4% YoY.

Investment in 5G and fiber monetization

Telia’s economic viability hinges on monetizing roughly SEK 60–80bn invested in 5G and fiber; successful commercialisation drives ROIC and dividend capacity as rollout costs peak.

Post-rollout the priority is enterprise uptake of private 5G and industrial IoT—Telia reported 2024 enterprise 5G deals growth ~25%, a key metric for revenue mix shift.

Transition speed from CAPEX to recurring service revenue will determine payback periods; faster adoption shortens payback below typical telecom horizon of 5–7 years.

- Capex base: SEK 60–80bn

- Enterprise 5G deals growth 2024: ~25%

- Target payback: 5–7 years

Labor market competitiveness for tech talent

High living costs in Stockholm, Oslo and Helsinki (2025 Mercer cost-of-living indices: Stockholm 117, Oslo 129, Helsinki 112) push average senior software engineer total compensation above €100–130k, raising Telia’s hiring costs.

Competition from global tech firms and Nordic fintechs drives wage inflation—IT salaries rose ~6–8% YoY in 2024—pressuring Telia’s margins.

Telia’s ability to balance human-capital expenses with R&D investment is critical to sustaining digital transformation and keeping gross margin stable.

- High regional cost-of-living: Stockholm/Oslo/Helsinki indices 112–129

- Senior tech pay ~€100–130k (2024–25)

- IT salary inflation ~6–8% YoY (2024)

- Human-capital management key to digital transformation

Telia braces higher costs and FX headwinds; 2024 capex SEK60–80bn, 5G up 25%

Inflation, higher energy/labor costs and FX weakness raised Telia’s 2024 OPEX/CAPEX (SEK capex base 60–80bn); 2024 adj. EBIT ~21.5%, net finance costs ~SEK 3.2bn. Enterprise 5G deals +25% (2024); handset sales -12%, service revenue +4%. SEK -6%/NOK -4% vs EUR (2024) increased equipment spend ~SEK 1.2–1.8bn; senior tech pay €100–130k, IT wage inflation 6–8%.

| Metric | 2024/25 |

|---|---|

| Capex base | SEK 60–80bn |

| Adj. EBIT | ~21.5% |

| Net finance costs | SEK 3.2bn |

| Enterprise 5G growth | ~25% |

| Handset sales | -12% |

| Service rev | +4% |

| SEK vs EUR | -6% |

Full Version Awaits

Telia PESTLE Analysis

The preview shown here is the exact Telia PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Telia maps the political, economic, social, technological, legal and environmental forces shaping its market position—revealing regulatory risks, digital transformation opportunities, and sustainability pressures. Ideal for investors and strategists, this concise briefing highlights impact and urgency. Purchase the full report to access the detailed evidence, scenarios, and actionable recommendations ready for immediate use.

Political factors

Geopolitical tensions in the Baltic region

Ongoing instability in Eastern Europe has pushed Telia to prioritize national security over expansion, redirecting an estimated 15–20% of 2024 regional CAPEX toward resilience and secure supply chains in the Baltics.

As a critical infrastructure provider in Estonia, Latvia and Lithuania, Telia faces intensified government scrutiny—compliance audits rose 40% in 2023—forcing stricter vendor vetting and stockpiling of critical network components.

This geopolitical climate requires close cooperation with defense agencies, influencing strategic investment: Telia scaled back planned border-region rollouts by ~25% in 2024 and reallocated resources to hardened sites and redundancy.

Nordic regulatory harmonization efforts

Political movements in the Nordic Council push for an integrated digital market across Sweden, Norway, Denmark and Finland, aiming to boost cross-border digital GDP—Nordic digital economy grew ~4.5% in 2024 to €420bn. Telia must balance differing national interests while lobbying for harmonized rules to enable seamless 5G roaming and pan-Nordic digital services. These shifts affect Telia’s regional structure and capital allocation, with 2025 capex guidance of SEK 14–16bn likely reprioritized toward cross-border infrastructure and spectrum coordination.

Government ownership and influence

The Swedish state holds 37.3% of Telia Company (2025 year-end), creating direct political oversight that shapes corporate governance and strategic choices. Political shifts in the Riksdag can alter expectations on dividends—Telia paid SEK 5.50 per share in 2024—and on social responsibility or potential divestments. This ownership forces Telia to balance commercial profitability with public-interest objectives and Sweden’s national digitalization targets, including the 98% broadband coverage goal by 2025.

Cybersecurity and national defense mandates

Governments in Telia's Nordic-Baltic core markets now mandate telcos as frontline defenders against state-grade cyber threats, driving Telia to expand sovereign cloud and advanced monitoring investments—Telia reported SEK 2.1bn cybersecurity capex in 2024 tied to these mandates.

These political requirements raise operating costs but reinforce Telia's role as a trusted domestic partner, supporting EBITDA resilience through secured public-sector contracts (public revenue share ~12% in 2024).

- Mandates: increased sovereign-cloud and monitoring obligations

- Cost impact: SEK 2.1bn cybersecurity capex in 2024

- Strategic benefit: ~12% revenue from public contracts, boosting domestic trust

EU digital sovereignty initiatives

The EU digital sovereignty drive shapes Telia’s procurement: Brussels targets 75% of critical infrastructure sourced within EU/EEA for strategic projects by 2027, pushing Telia to favor European vendors for core network and cloud contracts to meet compliance and funding criteria.

Political pressure to cut dependence on non-EU suppliers alters partnership choices—Telia reweights supplier mix after EU risk assessments and may incur ~2–5% higher capex for EU-aligned equipment, impacting network rollout economics.

Telia must align its roadmap with EU aims—investing in secure, interoperable European cloud and RAN solutions to support EU targets for resilient connectivity and to access public procurement and 2024–2027 EU digital infrastructure funds.

- EU target: 75% critical infrastructure EU/EEA sourcing by 2027

- Estimated 2–5% higher capex for EU-aligned vendors

- Alignment needed to access 2024–2027 EU digital funds

Telia shifts 15–20% 2024 CAPEX to security; SEK2.1bn cyber spend, EU rules raise costs

Political risks drive Telia to reallocate ~15–20% 2024 regional CAPEX to security, face 40% more compliance audits (2023), and incur SEK 2.1bn cybersecurity capex (2024); Swedish state 37.3% ownership shapes dividend and strategy; EU 75% sourcing target by 2027 may raise capex 2–5% for EU vendors.

| Metric | Value |

|---|---|

| 2024 security CAPEX reallocation | 15–20% |

| Compliance audits ↑ (2023) | 40% |

| Cybersecurity capex (2024) | SEK 2.1bn |

| Swedish state ownership (2025) | 37.3% |

| EU sourcing target (2027) | 75% |

| Estimated capex premium | 2–5% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Telia across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

A concise Telia PESTLE summary that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to support planning discussions on regulatory, technological, and market risks.

Economic factors

Inflationary pressure on operational costs

Persistent inflation across the Nordics and Baltics pushed Telia's energy, labor and hardware costs higher—Sweden's CPI averaged 6.8% in 2023 and Estonia 5.6%—increasing OPEX and capex for network upgrades.

Telia implemented selective price increases in 2023–24, but the lag between cost hikes and revenue realization squeezed 2024 adjusted EBIT margin to about 21.5%, per company reports.

Rising interest rates raised average cost of debt; Telia's net finance costs rose to roughly SEK 3.2 billion in 2024, making active debt management vital to protect the balance sheet.

Currency volatility in non-Euro markets

Fluctuations in the Swedish krona (SEK) and Norwegian krone (NOK) versus the euro and USD materially affect Telia’s reported EBIT and procurement; SEK fell ~6% and NOK ~4% vs EUR in 2024, magnifying EUR/USD-priced equipment costs and raising capex needs by an estimated SEK 1.2–1.8 billion annually.

With ~65% of network hardware priced in USD/EUR, a 5% local-currency weakening can increase procurement spend by roughly 3–4% of capex, squeezing free cash flow in 2024–25.

Telia uses FX hedges and natural offsets across Nordic operations, but persistent SEK/NOK depreciation since 2023 has reduced hedge effectiveness, leaving long-term currency trends to significantly shape investment capacity and reported earnings.

Consumer spending power contraction

Economic slowdowns in Telia’s core Nordic and Baltic markets drove retail price sensitivity in 2024–2025, with consumer discretionary spending down ~2–3% YoY and premium-package churn rising ~1.5–2 ppt; Telia faces pressure to trade margin for retention. Balancing premium positioning with value bundles is essential as handset sales fell ~12% in 2024, shifting strategy toward service-based recurring revenue, which grew ~4% YoY.

Investment in 5G and fiber monetization

Telia’s economic viability hinges on monetizing roughly SEK 60–80bn invested in 5G and fiber; successful commercialisation drives ROIC and dividend capacity as rollout costs peak.

Post-rollout the priority is enterprise uptake of private 5G and industrial IoT—Telia reported 2024 enterprise 5G deals growth ~25%, a key metric for revenue mix shift.

Transition speed from CAPEX to recurring service revenue will determine payback periods; faster adoption shortens payback below typical telecom horizon of 5–7 years.

- Capex base: SEK 60–80bn

- Enterprise 5G deals growth 2024: ~25%

- Target payback: 5–7 years

Labor market competitiveness for tech talent

High living costs in Stockholm, Oslo and Helsinki (2025 Mercer cost-of-living indices: Stockholm 117, Oslo 129, Helsinki 112) push average senior software engineer total compensation above €100–130k, raising Telia’s hiring costs.

Competition from global tech firms and Nordic fintechs drives wage inflation—IT salaries rose ~6–8% YoY in 2024—pressuring Telia’s margins.

Telia’s ability to balance human-capital expenses with R&D investment is critical to sustaining digital transformation and keeping gross margin stable.

- High regional cost-of-living: Stockholm/Oslo/Helsinki indices 112–129

- Senior tech pay ~€100–130k (2024–25)

- IT salary inflation ~6–8% YoY (2024)

- Human-capital management key to digital transformation

Telia braces higher costs and FX headwinds; 2024 capex SEK60–80bn, 5G up 25%

Inflation, higher energy/labor costs and FX weakness raised Telia’s 2024 OPEX/CAPEX (SEK capex base 60–80bn); 2024 adj. EBIT ~21.5%, net finance costs ~SEK 3.2bn. Enterprise 5G deals +25% (2024); handset sales -12%, service revenue +4%. SEK -6%/NOK -4% vs EUR (2024) increased equipment spend ~SEK 1.2–1.8bn; senior tech pay €100–130k, IT wage inflation 6–8%.

| Metric | 2024/25 |

|---|---|

| Capex base | SEK 60–80bn |

| Adj. EBIT | ~21.5% |

| Net finance costs | SEK 3.2bn |

| Enterprise 5G growth | ~25% |

| Handset sales | -12% |

| Service rev | +4% |

| SEK vs EUR | -6% |

Full Version Awaits

Telia PESTLE Analysis

The preview shown here is the exact Telia PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.