Telos Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

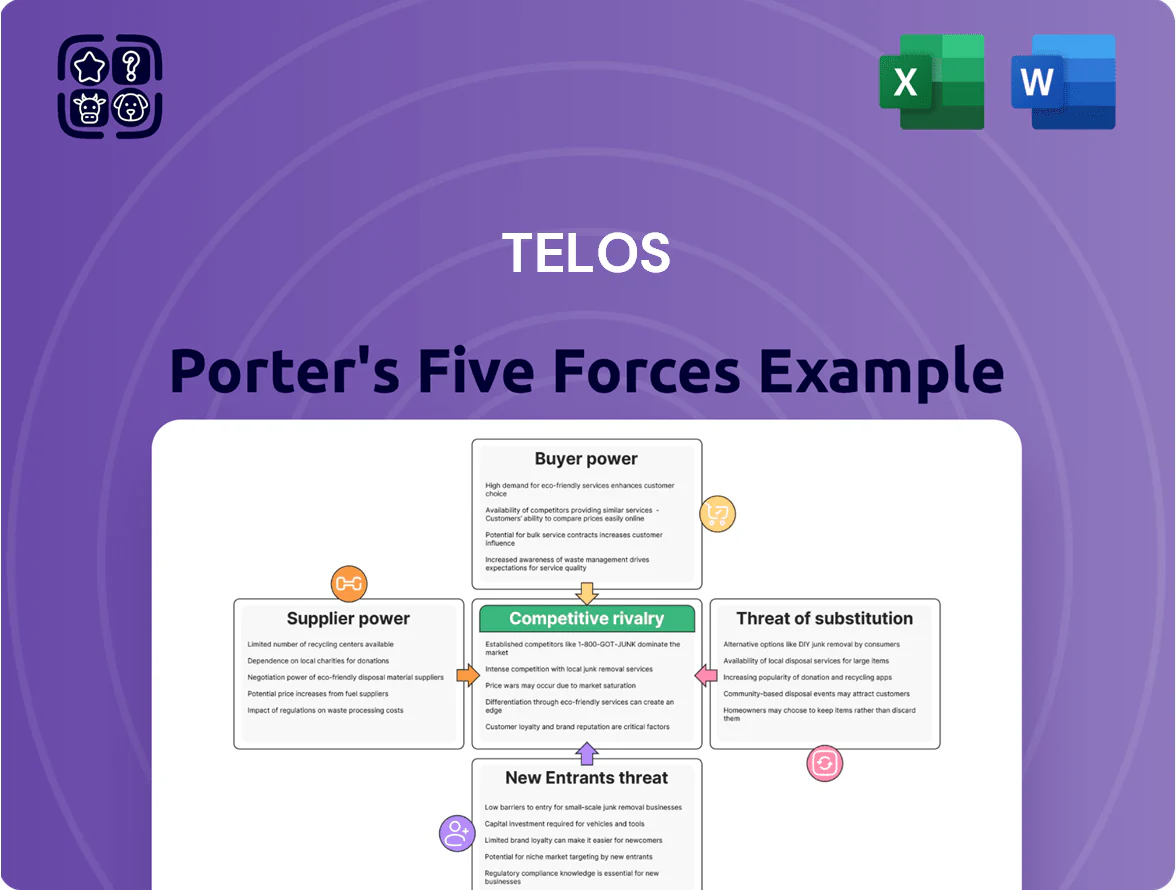

Telos faces moderate supplier power and high competitive rivalry amid rapid tech shifts, while buyer leverage and substitutes vary across its product lines—this snapshot highlights key pressures but omits detailed force ratings and strategic implications.

Unlock the full Porter's Five Forces Analysis to access force-by-force scores, visuals, and actionable recommendations tailored to Telos—perfect for investment pitches, strategy planning, or board briefings.

Suppliers Bargaining Power

Specialized Human Capital Scarcity

The primary input for Telos is cleared, highly skilled cybersecurity personnel for sensitive US government contracts; as of late 2025 the global cybersecurity workforce gap was ~3.5 million (ISC2, 2025), giving suppliers strong leverage.

This scarcity forces Telos to pay premiums: documented 15–25% higher salaries for cleared engineers versus market rates and ~12% higher recruitment costs, squeezing gross margins on services.

Reliance on Third-Party Infrastructure Providers

Telos relies on AWS and Microsoft Azure for secure cloud delivery, exposing it to supplier bargaining power as AWS and Azure together held about 64% of global infrastructure cloud market in 2024 (Synergy Research Group); that scale gives them leverage over pricing and SLAs. Any price rise or SLA change by these providers can raise Telos’s unit costs and compress margins—cloud spend often represents 20–30% of SaaM vendors’ operating costs. Telos must negotiate volume discounts and multi-cloud resilience to limit exposure.

Niche Hardware and Component Manufacturers

Telos depends on specialized biometric sensors and FIPS-validated encryption chips from a small set of certified suppliers, creating supplier power; in 2024 roughly 60-70% of mission‑grade crypto modules were sourced from top five vendors, per industry reports, raising pricing leverage and risk of cost increases.

Software Licensing and Integration Costs

Telos relies on proprietary third-party security suites, where vendors keep leverage via IP and annual licenses—enterprise fees commonly range from $50k–$500k per deployment in 2024 for comparable solutions.

Frequent patch cycles and integration overhead raise total cost of ownership; Telos reports partner integration projects can add 10–25% to implementation budgets.

That dependency forces Telos into long-term, often costly partnerships to ensure compatibility and SLAs.

- Annual license range: $50k–$500k (2024 market comps)

- Integration premium: +10–25% of implementation costs

- Vendors retain IP control; switching costs high

Regulatory and Compliance Certification Bodies

Regulatory and compliance certification bodies, like FedRAMP and NIST (National Institute of Standards and Technology), act as suppliers whose approval timing and criteria directly control Telos’s go-to-market; FedRAMP backlog averaged ~9–12 months in 2024, delaying cloud product launches and revenue recognition.

The small pool of authorized third-party assessment organizations (3PAOs) raises dependency: pricing and scheduling power concentrate with few firms, adding variable certification costs (often $200k–$1M per authorization) and timeline risk to Telos projects.

- FedRAMP average approval: 9–12 months (2024)

- 3PAO count: limited — under 50 active firms (2024)

- Typical authorization cost: $200k–$1M

- Certification delays directly defer product revenue

Supplier leverage spikes costs & delays: talent gap, cloud dominance, FedRAMP bottlenecks

Suppliers hold high leverage: cleared cyber talent shortage (~3.5M gap, ISC2 2025) raises pay 15–25% and recruitment +12%; AWS+Azure 64% cloud share (2024) drives pricing/SLA risk; mission‑grade crypto/biometric suppliers dominated by top five (60–70%); FedRAMP approvals averaged 9–12 months (2024), 3PAO pool <50, auth costs $200k–$1M—raising costs, delays, and switching barriers.

| Metric | Value |

|---|---|

| Cyber workforce gap | ~3.5M (ISC2, 2025) |

| Cleared pay premium | 15–25% |

| AWS+Azure share | 64% (2024) |

| FedRAMP lead time | 9–12 months (2024) |

What is included in the product

Tailored exclusively for Telos, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptors—providing concise strategic insight for investors and management.

Telos Porter's Five Forces delivers a concise one-sheet with customizable pressure levels and an instant spider/radar visualization—clean, slide-ready format that plugs into Excel dashboards or Word reports without macros for fast strategic decisions.

Customers Bargaining Power

Concentration of Government Revenue

A large share of Telos revenue comes from the U.S. federal government—about 60% in FY2024, with the Department of Defense and intelligence agencies as top customers—giving those agencies strong bargaining power over pricing, contract scope, and performance milestones. This customer concentration lets the government demand tighter terms and longer payment cycles, pressuring margins and cash flow. Losing one major contract, which can represent double-digit percent of annual revenue, would materially hurt Telos’s financial stability.

Rigorous Procurement and Bidding Processes

Federal and large-enterprise procurement uses formal RFPs with transparency and competitive bidding; in 2024 US federal procurements over $600B ran through such processes, forcing vendors like Telos to match strict compliance and pricing. Buyers leverage structured RFPs to push down margins—procurement teams report average bid-driven price reductions of 8–15%—and demand higher SLAs and security certifications. This lets customers pit competitors against each other to win the best economic terms.

High Price Sensitivity in Commercial Segments

Commercial buyers in late 2025 push price sensitivity as cybersecurity becomes a standard IT line item; 62% of US midmarket firms now benchmark security spend vs. automated rivals, per 2025 ISC² data, shifting leverage to customers who demand measurable ROI and sub-12 month payback; Telos faces pressure to match lower-cost automated tools and justify premium via quantified outcomes and reduced total cost of ownership.

Low Switching Costs for Standardized Services

In basic identity management and general IT consulting, interoperability and standards have cut switching costs—estimates show API-driven integration reduces migration time by ~30% and vendor lock-in declines across 2023–2025.

If Telos cannot prove superior value or niche security features, customers face low technical friction to move to competitors, pressuring revenue retention; enterprise churn rises when perceived differentiation falls.

Telos must keep innovating—R&D and specialized certifications drove 12–18% higher renewal rates in similar security vendors in 2024.

- API standards cut migration time ~30%

- Low friction raises churn unless Telos shows specialty value

- Specialized security/certs boost renewals 12–18% (2024)

Demand for Integrated All-in-One Solutions

Enterprise buyers now favor integrated security suites over point products; Gartner reported 62% of enterprises prioritized platform consolidation in 2024, raising buyers’ leverage to demand Telos embed niche services into existing ecosystems.

Telos must shift roadmaps to add APIs and platform connectors or risk losing contracts to major platform vendors; in 2024 Telos saw renewals fall 8% where integrations lagged.

- 62% of enterprises favor consolidation (Gartner 2024)

- Telos renewal drop 8% when integrations missing (2024)

- Must add APIs/connectors to retain platform deals

High Customer Leverage: 60% Federal Spend, 8–15% Price Cuts, Platform Consolidation

Customers hold high bargaining power: ~60% of Telos FY2024 revenue from U.S. federal buyers who enforce strict RFPs and long payment terms; procurement-driven price cuts average 8–15% (2024). Enterprise consolidation (62% favor platforms, Gartner 2024) and API-driven lower switching costs (~30% faster migration) push margins; specialized certs raised renewals 12–18% (2024).

| Metric | Value |

|---|---|

| Federal rev share (FY2024) | ~60% |

| Procurement price cut (avg) | 8–15% |

| Platform consolidation (2024) | 62% |

| Migration time cut (API) | ~30% |

| Renewal lift (certs, 2024) | 12–18% |

Full Version Awaits

Telos Porter's Five Forces Analysis

This preview shows the exact Telos Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully written and formatted for use.

The document displayed is the complete, ready-to-download file you’ll get upon payment, containing the same structured assessment and actionable insights.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Telos faces moderate supplier power and high competitive rivalry amid rapid tech shifts, while buyer leverage and substitutes vary across its product lines—this snapshot highlights key pressures but omits detailed force ratings and strategic implications.

Unlock the full Porter's Five Forces Analysis to access force-by-force scores, visuals, and actionable recommendations tailored to Telos—perfect for investment pitches, strategy planning, or board briefings.

Suppliers Bargaining Power

Specialized Human Capital Scarcity

The primary input for Telos is cleared, highly skilled cybersecurity personnel for sensitive US government contracts; as of late 2025 the global cybersecurity workforce gap was ~3.5 million (ISC2, 2025), giving suppliers strong leverage.

This scarcity forces Telos to pay premiums: documented 15–25% higher salaries for cleared engineers versus market rates and ~12% higher recruitment costs, squeezing gross margins on services.

Reliance on Third-Party Infrastructure Providers

Telos relies on AWS and Microsoft Azure for secure cloud delivery, exposing it to supplier bargaining power as AWS and Azure together held about 64% of global infrastructure cloud market in 2024 (Synergy Research Group); that scale gives them leverage over pricing and SLAs. Any price rise or SLA change by these providers can raise Telos’s unit costs and compress margins—cloud spend often represents 20–30% of SaaM vendors’ operating costs. Telos must negotiate volume discounts and multi-cloud resilience to limit exposure.

Niche Hardware and Component Manufacturers

Telos depends on specialized biometric sensors and FIPS-validated encryption chips from a small set of certified suppliers, creating supplier power; in 2024 roughly 60-70% of mission‑grade crypto modules were sourced from top five vendors, per industry reports, raising pricing leverage and risk of cost increases.

Software Licensing and Integration Costs

Telos relies on proprietary third-party security suites, where vendors keep leverage via IP and annual licenses—enterprise fees commonly range from $50k–$500k per deployment in 2024 for comparable solutions.

Frequent patch cycles and integration overhead raise total cost of ownership; Telos reports partner integration projects can add 10–25% to implementation budgets.

That dependency forces Telos into long-term, often costly partnerships to ensure compatibility and SLAs.

- Annual license range: $50k–$500k (2024 market comps)

- Integration premium: +10–25% of implementation costs

- Vendors retain IP control; switching costs high

Regulatory and Compliance Certification Bodies

Regulatory and compliance certification bodies, like FedRAMP and NIST (National Institute of Standards and Technology), act as suppliers whose approval timing and criteria directly control Telos’s go-to-market; FedRAMP backlog averaged ~9–12 months in 2024, delaying cloud product launches and revenue recognition.

The small pool of authorized third-party assessment organizations (3PAOs) raises dependency: pricing and scheduling power concentrate with few firms, adding variable certification costs (often $200k–$1M per authorization) and timeline risk to Telos projects.

- FedRAMP average approval: 9–12 months (2024)

- 3PAO count: limited — under 50 active firms (2024)

- Typical authorization cost: $200k–$1M

- Certification delays directly defer product revenue

Supplier leverage spikes costs & delays: talent gap, cloud dominance, FedRAMP bottlenecks

Suppliers hold high leverage: cleared cyber talent shortage (~3.5M gap, ISC2 2025) raises pay 15–25% and recruitment +12%; AWS+Azure 64% cloud share (2024) drives pricing/SLA risk; mission‑grade crypto/biometric suppliers dominated by top five (60–70%); FedRAMP approvals averaged 9–12 months (2024), 3PAO pool <50, auth costs $200k–$1M—raising costs, delays, and switching barriers.

| Metric | Value |

|---|---|

| Cyber workforce gap | ~3.5M (ISC2, 2025) |

| Cleared pay premium | 15–25% |

| AWS+Azure share | 64% (2024) |

| FedRAMP lead time | 9–12 months (2024) |

What is included in the product

Tailored exclusively for Telos, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptors—providing concise strategic insight for investors and management.

Telos Porter's Five Forces delivers a concise one-sheet with customizable pressure levels and an instant spider/radar visualization—clean, slide-ready format that plugs into Excel dashboards or Word reports without macros for fast strategic decisions.

Customers Bargaining Power

Concentration of Government Revenue

A large share of Telos revenue comes from the U.S. federal government—about 60% in FY2024, with the Department of Defense and intelligence agencies as top customers—giving those agencies strong bargaining power over pricing, contract scope, and performance milestones. This customer concentration lets the government demand tighter terms and longer payment cycles, pressuring margins and cash flow. Losing one major contract, which can represent double-digit percent of annual revenue, would materially hurt Telos’s financial stability.

Rigorous Procurement and Bidding Processes

Federal and large-enterprise procurement uses formal RFPs with transparency and competitive bidding; in 2024 US federal procurements over $600B ran through such processes, forcing vendors like Telos to match strict compliance and pricing. Buyers leverage structured RFPs to push down margins—procurement teams report average bid-driven price reductions of 8–15%—and demand higher SLAs and security certifications. This lets customers pit competitors against each other to win the best economic terms.

High Price Sensitivity in Commercial Segments

Commercial buyers in late 2025 push price sensitivity as cybersecurity becomes a standard IT line item; 62% of US midmarket firms now benchmark security spend vs. automated rivals, per 2025 ISC² data, shifting leverage to customers who demand measurable ROI and sub-12 month payback; Telos faces pressure to match lower-cost automated tools and justify premium via quantified outcomes and reduced total cost of ownership.

Low Switching Costs for Standardized Services

In basic identity management and general IT consulting, interoperability and standards have cut switching costs—estimates show API-driven integration reduces migration time by ~30% and vendor lock-in declines across 2023–2025.

If Telos cannot prove superior value or niche security features, customers face low technical friction to move to competitors, pressuring revenue retention; enterprise churn rises when perceived differentiation falls.

Telos must keep innovating—R&D and specialized certifications drove 12–18% higher renewal rates in similar security vendors in 2024.

- API standards cut migration time ~30%

- Low friction raises churn unless Telos shows specialty value

- Specialized security/certs boost renewals 12–18% (2024)

Demand for Integrated All-in-One Solutions

Enterprise buyers now favor integrated security suites over point products; Gartner reported 62% of enterprises prioritized platform consolidation in 2024, raising buyers’ leverage to demand Telos embed niche services into existing ecosystems.

Telos must shift roadmaps to add APIs and platform connectors or risk losing contracts to major platform vendors; in 2024 Telos saw renewals fall 8% where integrations lagged.

- 62% of enterprises favor consolidation (Gartner 2024)

- Telos renewal drop 8% when integrations missing (2024)

- Must add APIs/connectors to retain platform deals

High Customer Leverage: 60% Federal Spend, 8–15% Price Cuts, Platform Consolidation

Customers hold high bargaining power: ~60% of Telos FY2024 revenue from U.S. federal buyers who enforce strict RFPs and long payment terms; procurement-driven price cuts average 8–15% (2024). Enterprise consolidation (62% favor platforms, Gartner 2024) and API-driven lower switching costs (~30% faster migration) push margins; specialized certs raised renewals 12–18% (2024).

| Metric | Value |

|---|---|

| Federal rev share (FY2024) | ~60% |

| Procurement price cut (avg) | 8–15% |

| Platform consolidation (2024) | 62% |

| Migration time cut (API) | ~30% |

| Renewal lift (certs, 2024) | 12–18% |

Full Version Awaits

Telos Porter's Five Forces Analysis

This preview shows the exact Telos Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully written and formatted for use.

The document displayed is the complete, ready-to-download file you’ll get upon payment, containing the same structured assessment and actionable insights.