Tenaska Porter's Five Forces Analysis

From Overview to Strategy Blueprint

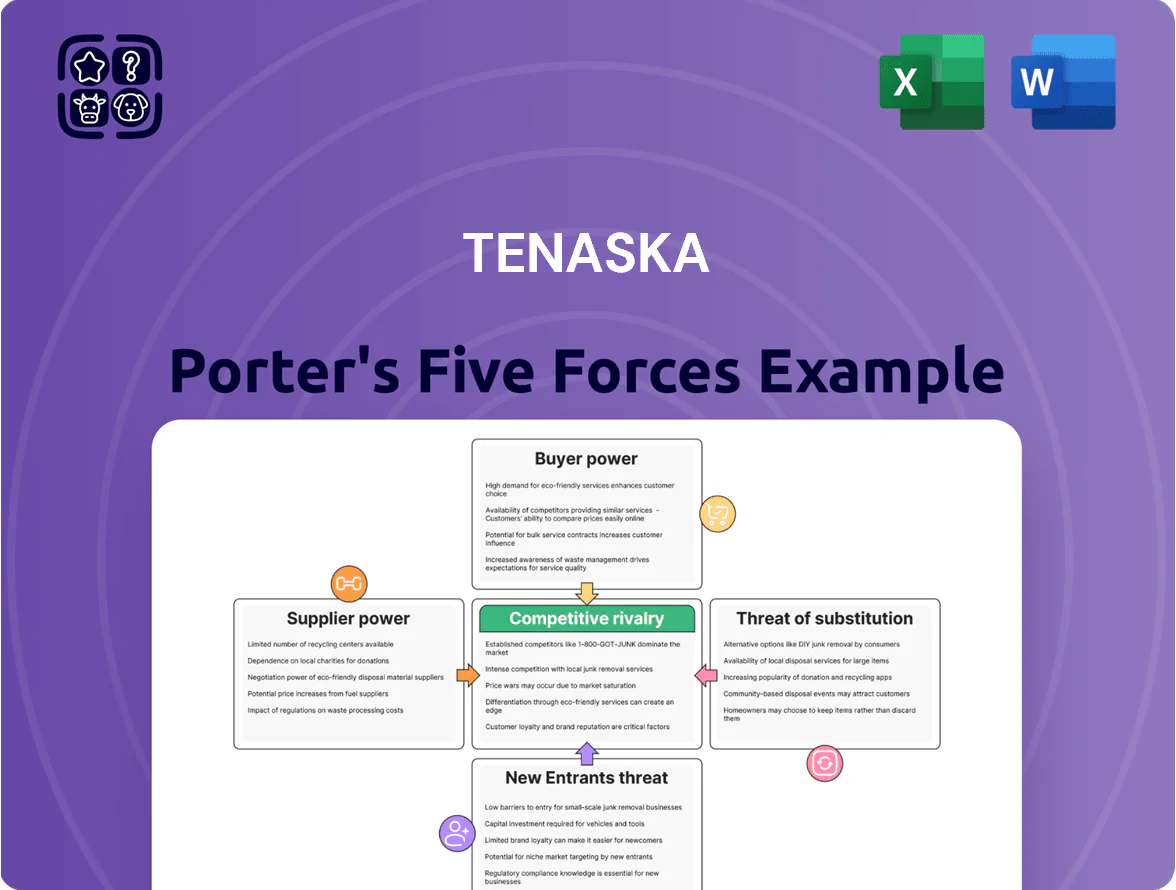

Tenaska faces moderate buyer power and supplier constraints, with new entrant threats tempered by capital intensity and regulatory barriers, while substitutes and rivalry hinge on evolving energy markets and project execution capacity. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tenaska’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural Gas Feedstock Volatility

Tenaska depends on natural gas for ~80% of its thermal generation and marketing book, so upstream price swings (Henry Hub rose 65% in 2022 and averaged $3.85/MMBtu in 2025 YTD) directly squeeze margins; major E&P players control ~60% of regional pipeline receipts, giving suppliers bargaining power in tight winter demand; pipeline outages and 5–10% production dips can force costly spot purchases and reduce merchant margins by tens of $/MWh.

EPC Contractor Specialization

The development of new power plants and carbon capture projects needs specialized EPC (engineering, procurement, construction) firms; globally, about 20–30 firms handle gigawatt-scale projects, concentrating pricing power.

Tenaska’s 2025 push into renewables and CCS raises demand for these niche skills, so suppliers can command higher margins—EPC bids often carry 8–15% premium versus generic builds.

Limited supplier pool constrains Tenaska’s negotiating leverage, increasing capex risk and schedule exposure for multimillion- to billion-dollar projects.

Renewable Technology OEM Dependency

As Tenaska shifts into solar and wind, dependency on a few OEMs for turbines and PV modules raises supplier power; global top 5 turbine makers held ~80% of market share in 2024 and module capacity additions concentrated in China (≈75% of polysilicon production), so supply shocks lift prices to developers. OEMs face rare‑earth and inverter chip shortages—prices for polysilicon rose ~35% in 2024—while bespoke grid‑grade specs make switching costly and delay projects by months.

Interconnection and Grid Operators

RTOs/ISOs function as quasi-suppliers, controlling transmission and wholesale market access; Tenaska must follow their tariffs and standards to sell power.

These operators often set non-negotiable fees—e.g., average U.S. transmission charges rose ~4% in 2024, tightening Tenaska’s margins—and their regional monopolies limit Tenaska’s bargaining leverage.

Compliance costs and congestion charges can represent several $/MWh, directly hitting project returns and leaving Tenaska little room to negotiate rates.

- RTO/ISO monopoly over grid infra

- Tariffs non-negotiable; 2024 transmission +4%

- Fees/congestion add several $/MWh

- Regulatory compliance limits pricing flexibility

Financial Capital and Debt Markets

Financial capital is a major supplier for Tenaska: large projects need billions—US utility-scale gas plants or renewables often cost $500M–$2B—so institutional lenders and private equity control access.

Cost of capital (US 10‑yr treasury + credit spread) drives project IRR; a 200 bps rise in rates can cut IRR by ~2–4 percentage points, making marginal projects unviable.

ESG lending shifts and lender covenant terms give creditors leverage to set financing structure, tenor, and covenants, directly affecting cash flow timing and returns.

- Typical project capex: $500M–$2B

- Rate sensitivity: 200 bps → IRR −2–4 pts

- ESG filters reduced fossil finance by ~20% in 2024

- Debt terms dictate tenor, covenants, and DSCR requirements

Supply shocks, rising costs and rate hikes squeeze Tenaska margins

Suppliers hold strong leverage: natural gas (~80% fuel exposure) and top 5 turbine/module OEMs (~80% share) concentrate pricing power, while ~20–30 global EPCs and institutional lenders (projects $500M–$2B) set terms; transmission RTO/ISO fees rose ~4% in 2024 and polysilicon +35% in 2024, so supply shocks, capex premiums (EPC +8–15%) and +200bps rates (IRR −2–4pt) compress Tenaska margins.

| Metric | Value (2024–25) |

|---|---|

| Fuel exposure | ~80% gas |

| OEM share | Top5 ≈80% |

| Polysilicon price change | +35% (2024) |

| EPC premium | 8–15% |

| Transmission fees | +4% (2024) |

| Project capex | $500M–$2B |

| Rate shock impact | +200bps → IRR −2–4pt |

What is included in the product

Tailored Tenaska Porter’s Five Forces analysis uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptors that influence its pricing, profitability, and market positioning.

Clear one-sheet Porter’s Five Forces for Tenaska—rapidly assess competitive pressures and make quick strategic choices.

Customers Bargaining Power

Wholesale Market Price Takers

Utility Offtake Agreements

Tenaska secures long-term stability through Power Purchase Agreements (PPAs) with large regulated utilities and cooperatives, but these buyers wield strong bargaining power since they provide the guaranteed cash flows lenders want for project financing; in 2024 utilities signed ~60% of US utility-scale PPAs by capacity, tightening leverage for sellers. Utilities press for lower levelized cost of energy (LCOE) and firming guarantees as merchant entrants and 2023–25 battery+solar builds raise competition. Typical PPA terms now span 10–25 years, giving buyers leverage to require strict performance and price step-downs tied to market indices.

Corporate Renewable Procurement

Large corporates now sign bilateral renewables deals: global corporate PPAs hit 32.7 GW in 2023, and US C&I procurement reached ~13 GW in 2024, so buyers wield real leverage. These buyers run detailed RFPs and pit developers for the lowest LCOE—recent US virtual PPA strikes fell below $20/MWh for wind and $30/MWh for solar in best markets. Tenaska must deliver bespoke contracts, tight pricing, and risk allocation to secure multi‑year, high‑volume deals.

Natural Gas Marketing Counterparties

Tenaska faces strong customer bargaining power: industrial end-users and local distribution companies (LDCs) can choose among many marketers, making them highly price- and reliability-sensitive and often contracting with multiple suppliers to force competitive bids.

Market transparency—daily Henry Hub futures and NYMEX spreads visible to all—lets buyers compare rates instantly, squeezing Tenaska’s trading margins; U.S. non-residential gas consumers saw average spot-price volatility of ~35% in 2024, raising churn and bid-driven margin pressure.

- Multiple suppliers available

- Buyers price- and reliability-sensitive

- Multi-supplier contracting common

- High market transparency (Henry Hub/NYMEX)

- ~35% spot-price volatility in 2024

Regulatory Influence on Rates

Regulatory bodies, notably state public utility commissions (PUCs), act for end consumers and can block or force renegotiation of Tenaska’s PPAs if rates exceed what regulators deem in the public interest, creating material contract risk.

In 2024-25, several US PUCs rejected or modified PPAs with avoided-cost disputes; a single PUC decision can alter projected asset-level cash flows by 5–15% over 10 years, raising adjustment risk to Tenaska’s long-term revenue forecasts.

What this hides: regulatory decisions vary by state and hinge on avoided-cost calculations, making conservatively stressed revenue scenarios prudent.

- PUC oversight = indirect customer power

- Rejected/renegotiated PPAs hit cash flows 5–15% over decade

- State-by-state variance increases portfolio revenue volatility

Tenaska squeezed: utility PPAs, volatile gas and transparent markets compress margins

| Metric | 2023–24 |

|---|---|

| Tenaska power revenue (est) | >$2.1B |

| US utility PPA share | ~60% |

| Corporate PPAs global | 32.7 GW (2023) |

| Gas spot vol | ~35% (2024) |

Full Version Awaits

Tenaska Porter's Five Forces Analysis

This preview shows the exact Tenaska Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, complete, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Tenaska faces moderate buyer power and supplier constraints, with new entrant threats tempered by capital intensity and regulatory barriers, while substitutes and rivalry hinge on evolving energy markets and project execution capacity. This snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tenaska’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural Gas Feedstock Volatility

Tenaska depends on natural gas for ~80% of its thermal generation and marketing book, so upstream price swings (Henry Hub rose 65% in 2022 and averaged $3.85/MMBtu in 2025 YTD) directly squeeze margins; major E&P players control ~60% of regional pipeline receipts, giving suppliers bargaining power in tight winter demand; pipeline outages and 5–10% production dips can force costly spot purchases and reduce merchant margins by tens of $/MWh.

EPC Contractor Specialization

The development of new power plants and carbon capture projects needs specialized EPC (engineering, procurement, construction) firms; globally, about 20–30 firms handle gigawatt-scale projects, concentrating pricing power.

Tenaska’s 2025 push into renewables and CCS raises demand for these niche skills, so suppliers can command higher margins—EPC bids often carry 8–15% premium versus generic builds.

Limited supplier pool constrains Tenaska’s negotiating leverage, increasing capex risk and schedule exposure for multimillion- to billion-dollar projects.

Renewable Technology OEM Dependency

As Tenaska shifts into solar and wind, dependency on a few OEMs for turbines and PV modules raises supplier power; global top 5 turbine makers held ~80% of market share in 2024 and module capacity additions concentrated in China (≈75% of polysilicon production), so supply shocks lift prices to developers. OEMs face rare‑earth and inverter chip shortages—prices for polysilicon rose ~35% in 2024—while bespoke grid‑grade specs make switching costly and delay projects by months.

Interconnection and Grid Operators

RTOs/ISOs function as quasi-suppliers, controlling transmission and wholesale market access; Tenaska must follow their tariffs and standards to sell power.

These operators often set non-negotiable fees—e.g., average U.S. transmission charges rose ~4% in 2024, tightening Tenaska’s margins—and their regional monopolies limit Tenaska’s bargaining leverage.

Compliance costs and congestion charges can represent several $/MWh, directly hitting project returns and leaving Tenaska little room to negotiate rates.

- RTO/ISO monopoly over grid infra

- Tariffs non-negotiable; 2024 transmission +4%

- Fees/congestion add several $/MWh

- Regulatory compliance limits pricing flexibility

Financial Capital and Debt Markets

Financial capital is a major supplier for Tenaska: large projects need billions—US utility-scale gas plants or renewables often cost $500M–$2B—so institutional lenders and private equity control access.

Cost of capital (US 10‑yr treasury + credit spread) drives project IRR; a 200 bps rise in rates can cut IRR by ~2–4 percentage points, making marginal projects unviable.

ESG lending shifts and lender covenant terms give creditors leverage to set financing structure, tenor, and covenants, directly affecting cash flow timing and returns.

- Typical project capex: $500M–$2B

- Rate sensitivity: 200 bps → IRR −2–4 pts

- ESG filters reduced fossil finance by ~20% in 2024

- Debt terms dictate tenor, covenants, and DSCR requirements

Supply shocks, rising costs and rate hikes squeeze Tenaska margins

Suppliers hold strong leverage: natural gas (~80% fuel exposure) and top 5 turbine/module OEMs (~80% share) concentrate pricing power, while ~20–30 global EPCs and institutional lenders (projects $500M–$2B) set terms; transmission RTO/ISO fees rose ~4% in 2024 and polysilicon +35% in 2024, so supply shocks, capex premiums (EPC +8–15%) and +200bps rates (IRR −2–4pt) compress Tenaska margins.

| Metric | Value (2024–25) |

|---|---|

| Fuel exposure | ~80% gas |

| OEM share | Top5 ≈80% |

| Polysilicon price change | +35% (2024) |

| EPC premium | 8–15% |

| Transmission fees | +4% (2024) |

| Project capex | $500M–$2B |

| Rate shock impact | +200bps → IRR −2–4pt |

What is included in the product

Tailored Tenaska Porter’s Five Forces analysis uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging disruptors that influence its pricing, profitability, and market positioning.

Clear one-sheet Porter’s Five Forces for Tenaska—rapidly assess competitive pressures and make quick strategic choices.

Customers Bargaining Power

Wholesale Market Price Takers

Utility Offtake Agreements

Tenaska secures long-term stability through Power Purchase Agreements (PPAs) with large regulated utilities and cooperatives, but these buyers wield strong bargaining power since they provide the guaranteed cash flows lenders want for project financing; in 2024 utilities signed ~60% of US utility-scale PPAs by capacity, tightening leverage for sellers. Utilities press for lower levelized cost of energy (LCOE) and firming guarantees as merchant entrants and 2023–25 battery+solar builds raise competition. Typical PPA terms now span 10–25 years, giving buyers leverage to require strict performance and price step-downs tied to market indices.

Corporate Renewable Procurement

Large corporates now sign bilateral renewables deals: global corporate PPAs hit 32.7 GW in 2023, and US C&I procurement reached ~13 GW in 2024, so buyers wield real leverage. These buyers run detailed RFPs and pit developers for the lowest LCOE—recent US virtual PPA strikes fell below $20/MWh for wind and $30/MWh for solar in best markets. Tenaska must deliver bespoke contracts, tight pricing, and risk allocation to secure multi‑year, high‑volume deals.

Natural Gas Marketing Counterparties

Tenaska faces strong customer bargaining power: industrial end-users and local distribution companies (LDCs) can choose among many marketers, making them highly price- and reliability-sensitive and often contracting with multiple suppliers to force competitive bids.

Market transparency—daily Henry Hub futures and NYMEX spreads visible to all—lets buyers compare rates instantly, squeezing Tenaska’s trading margins; U.S. non-residential gas consumers saw average spot-price volatility of ~35% in 2024, raising churn and bid-driven margin pressure.

- Multiple suppliers available

- Buyers price- and reliability-sensitive

- Multi-supplier contracting common

- High market transparency (Henry Hub/NYMEX)

- ~35% spot-price volatility in 2024

Regulatory Influence on Rates

Regulatory bodies, notably state public utility commissions (PUCs), act for end consumers and can block or force renegotiation of Tenaska’s PPAs if rates exceed what regulators deem in the public interest, creating material contract risk.

In 2024-25, several US PUCs rejected or modified PPAs with avoided-cost disputes; a single PUC decision can alter projected asset-level cash flows by 5–15% over 10 years, raising adjustment risk to Tenaska’s long-term revenue forecasts.

What this hides: regulatory decisions vary by state and hinge on avoided-cost calculations, making conservatively stressed revenue scenarios prudent.

- PUC oversight = indirect customer power

- Rejected/renegotiated PPAs hit cash flows 5–15% over decade

- State-by-state variance increases portfolio revenue volatility

Tenaska squeezed: utility PPAs, volatile gas and transparent markets compress margins

| Metric | 2023–24 |

|---|---|

| Tenaska power revenue (est) | >$2.1B |

| US utility PPA share | ~60% |

| Corporate PPAs global | 32.7 GW (2023) |

| Gas spot vol | ~35% (2024) |

Full Version Awaits

Tenaska Porter's Five Forces Analysis

This preview shows the exact Tenaska Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, complete, and ready for download with no placeholders or samples.