Tencent Holdings Boston Consulting Group Matrix

Unlock Strategic Clarity

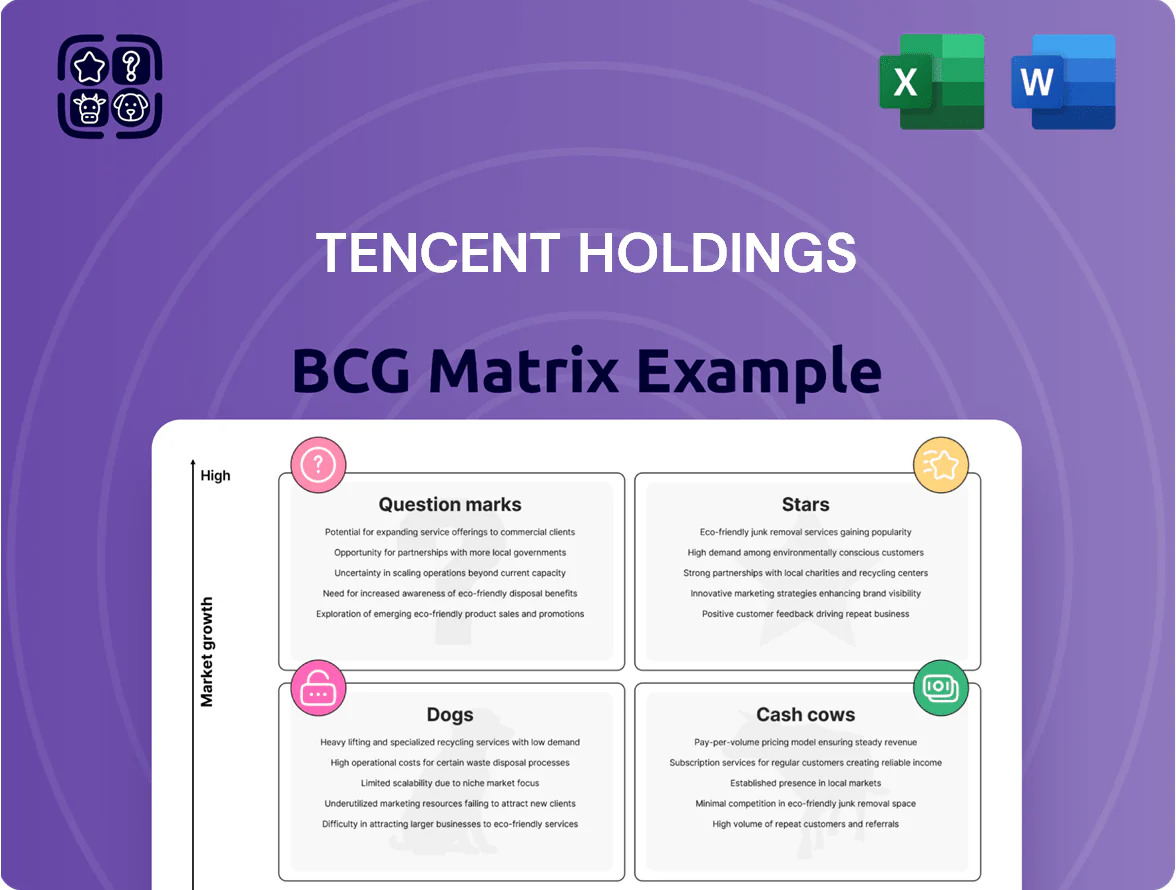

Tencent’s BCG Matrix preview highlights its dominant Stars in social and gaming, Cash Cows from mature platforms and ad services, plus Question Marks in cloud and international ventures that could reshape growth—while a few niche initiatives sit in the Dogs quadrant. This snapshot shows where Tencent generates cash, where it must invest, and which units may need divestment or reinvention. Purchase the full BCG Matrix for quadrant-level data, actionable strategic moves, and ready-to-use Word and Excel deliverables to guide investment and portfolio decisions.

Stars

WeChat Video Accounts

By end-2025 WeChat Video Accounts (Weixin Shipin) is a star in Tencent Holdings BCG Matrix: it held ~28% of Chinese short-video daily time spent and grew MAUs to 650M, challenging Douyin's dominance.

Revenue surged to an estimated RMB 45bn in 2025 from e-commerce commissions and ads, yet Tencent still spent ~RMB 12bn on creator incentives and RMB 8bn on live-streaming infra to sustain growth.

International Gaming Expansion

Level Infinite, Tencent’s global publishing label, holds a rising share in international mobile and console gaming, with overseas game revenues contributing roughly 25% of Tencent Games’ RMB 201.5bn 2024 revenue, up 6 percentage points from 2022.

Through acquisitions (eg. Sumo Group 2021) and internal studios, Level Infinite launched high-profile titles driving global MAU growth—international DAU rose ~18% YoY in 2024.

These expansions need heavy upfront spend: Tencent reported gaming S&M and localization costs rising to RMB 32bn in 2024, pressuring near-term margins.

As China’s market slows, Level Infinite is the division’s primary growth engine, targeting double-digit CAGR in overseas revenues through 2026.

Hunyuan Enterprise AI Solutions

Hunyuan Enterprise AI Solutions is a Star in Tencent Holdings’ BCG matrix: Hunyuan, Tencent’s large language model, anchors its B2B push across finance, gaming, healthcare, and government, driving cloud AI revenue that helped Tencent Cloud grow 42% YoY in 2024 to RMB 72.6 billion (about USD 10.5B).

Fintech Wealth Management Services

Fintech Wealth Management Services: Tencent’s move beyond payments into wealth and insurance distribution within WeChat shows strong growth—assets under management via its platforms rose ~28% YoY to an estimated RMB 1.1 trillion by end-2025, driven by wallet market share ~45% and millions of monthly active users buying funds and insurance.

Ongoing risks: regulatory oversight (licensing, product limits) and required tech spend on risk models and KYC keep this a high-investment, high-growth quadrant versus banks.

- ~RMB 1.1T AUM (2025 est)

- ~28% YoY AUM growth (2024–25)

- ~45% digital wallet market share

- Needs continual regulatory navigation + tech investment

Smart Retail and SaaS Ecosystem

Tencent Holdings’ Smart Retail and SaaS ecosystem—anchored by WeCom (WeChat Work) and Mini Programs—holds a leading share in China’s digital retail transformation, with Tencent Cloud revenue up 38% in FY2024 and Mini Program monthly active users exceeding 900 million as of Dec 2024.

These tools power merchant-customer flows as retail shifts online; over 60% of surveyed Chinese retailers used Mini Programs for sales in 2024, and transaction GMV via Mini Programs grew ~45% YoY.

Tencent must keep investing in cloud capacity and product updates—Tencent Cloud capex rose in 2024—to repel Alibaba and ByteDance and convert platform usage into SaaS recurring revenue and higher-margin services.

- WeCom + Mini Programs: ~900M MAU (Dec 2024)

- Tencent Cloud revenue: +38% FY2024

- Mini Program GMV growth: ~45% YoY (2024)

- ~60% retailers using Mini Programs (2024 survey)

Tencent’s Growth Engines: Video, Cloud, Games, Fintech & Mini Programs Power Surge

Stars: WeChat Video Accounts, Level Infinite, Hunyuan AI, Fintech wealth, and Mini Programs drive Tencent’s high-growth businesses—WeChat Video ~28% short-video time, 650M MAU (2025); Tencent Games overseas ~25% of RMB201.5bn (2024); Tencent Cloud RMB72.6bn (42% YoY, 2024); AUM ~RMB1.1T (2025 est); Mini Programs 900M MAU (Dec 2024).

| Asset | Key 2024–25 metrics |

|---|---|

| WeChat Video | 28% time share; 650M MAU (2025) |

| Games (Level Infinite) | 25% overseas revenue of RMB201.5bn (2024) |

| Hunyuan/Cloud | RMB72.6bn Cloud rev; +42% YoY (2024) |

| Fintech AUM | ~RMB1.1T; +28% YoY (2024–25) |

| Mini Programs | 900M MAU (Dec 2024); GMV +45% YoY |

What is included in the product

BCG Matrix for Tencent: strategic placement of Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance and trend context.

One-page Tencent BCG Matrix mapping business units into quadrants for rapid portfolio prioritization and investor briefings.

Cash Cows

Domestic Online Games

Honor of Kings and Peacekeeper Elite together held ~57% of China’s mobile game grossing in 2024, with Honor of Kings reporting RMB 30.4 billion (~USD 4.2B) revenue in 2024 and Peacekeeper Elite ~RMB 18.7 billion, producing steady operating cash flow and low marginal costs versus initial dev spend.

These franchises fund Tencent Holdings’ R&D and global bets: Tencent allocated RMB 26.8 billion to overseas investments and experimental projects in 2024, largely covered by domestic online games’ free cash flow.

WeChat Core Messaging and Social

WeChat core messaging and social functions sit in a mature market where Tencent Holdings holds a near-monopoly in China, with 1.31 billion monthly active users as of Q4 2025, requiring maintenance more than aggressive growth.

The service generates steady, low-cost user data and access that underpins Tencent’s ad, payments, cloud, and gaming units, contributing to stable cash flow and cross-sell reach across the ecosystem.

Operating margins on WeChat-related services stay high because incremental user costs are low; in 2025 WeChat-related advertising and social commerce helped sustain Tencent’s platform revenue resilience amid slower overall growth.

Tencent Music Entertainment

Tencent Music Entertainment (TME) leads China’s streaming market with ~66% music subscription market share and 85m+ paying users as of Q4 2025, making it a cash cow in Tencent Holdings’ BCG matrix.

Revenue mix has stabilized: subscriptions and ads drove RMB 27.3B in FY2024 revenue with gross margins near 40%, yielding steady free cash flow.

That predictable cash flow funds Tencent’s broader digital-content investments and lets the group avoid high-risk capital injections into TME.

Payment Processing Infrastructure

The WeChat Pay ecosystem now handles an estimated 70% of China’s mobile peer-to-peer and point-of-sale micro-transactions, processing roughly CNY 20 trillion in 2024 and generating stable service fees despite slower user growth.

Growth in new users has decelerated to low single digits, but daily transaction volume—over 1 billion transactions per day—delivers predictable fee income and low marginal marketing costs.

As a utility-like cash cow, this unit supplies steady operating cashflow that funds Tencent’s higher-growth bets across gaming, cloud, and AI investments.

- 2024 volume ~CNY 20 trillion

- ~1 billion daily transactions

- Market share ~70% of mobile micro-payments

- User growth low single digits (2024)

Social Media Advertising

Social Media Advertising via WeChat Moments and Tencent’s wider social ecosystem is a mature, high-margin cash cow, capturing roughly 30–35% of China’s performance-ad spend in 2024 and generating double-digit operating margins for the segment.

Unparalleled user targeting (WeChat 1.4bn MAU in 2024) drives high ROI, low capex needs, and steady free cash flow that funded ~20% of Tencent’s R&D spend in 2024 (R&D = RMB 86.9bn).

- Market share: ~30–35% of performance ads (2024)

- WeChat MAU: 1.4 billion (2024)

- R&D funded: ~20% from ad cash flow (2024)

- Characteristics: high margins, low capex, stable FCF

Tencent’s cash engines: Gaming, WeChat, Pay and TME drive massive revenue and engagement

Strong cash cows: Honor of Kings + Peacekeeper Elite (~RMB 49.1B revenue, ~57% China mobile grossing 2024), WeChat (1.31B MAU Q4 2025; high margins, low incremental costs), WeChat Pay (~CNY 20T volume 2024; ~1B daily tx), Tencent Music (TME 85M+ paying users, RMB 27.3B FY2024).

| Unit | Key 2024–25 |

|---|---|

| Games | RMB49.1B; 57% market |

| 1.31B MAU; high margins | |

| WeChat Pay | CNY20T; 1B/day |

| TME | 85M+ pay; RMB27.3B |

Preview = Final Product

Tencent Holdings BCG Matrix

The file you're previewing is the exact Tencent Holdings BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Tencent’s BCG Matrix preview highlights its dominant Stars in social and gaming, Cash Cows from mature platforms and ad services, plus Question Marks in cloud and international ventures that could reshape growth—while a few niche initiatives sit in the Dogs quadrant. This snapshot shows where Tencent generates cash, where it must invest, and which units may need divestment or reinvention. Purchase the full BCG Matrix for quadrant-level data, actionable strategic moves, and ready-to-use Word and Excel deliverables to guide investment and portfolio decisions.

Stars

WeChat Video Accounts

By end-2025 WeChat Video Accounts (Weixin Shipin) is a star in Tencent Holdings BCG Matrix: it held ~28% of Chinese short-video daily time spent and grew MAUs to 650M, challenging Douyin's dominance.

Revenue surged to an estimated RMB 45bn in 2025 from e-commerce commissions and ads, yet Tencent still spent ~RMB 12bn on creator incentives and RMB 8bn on live-streaming infra to sustain growth.

International Gaming Expansion

Level Infinite, Tencent’s global publishing label, holds a rising share in international mobile and console gaming, with overseas game revenues contributing roughly 25% of Tencent Games’ RMB 201.5bn 2024 revenue, up 6 percentage points from 2022.

Through acquisitions (eg. Sumo Group 2021) and internal studios, Level Infinite launched high-profile titles driving global MAU growth—international DAU rose ~18% YoY in 2024.

These expansions need heavy upfront spend: Tencent reported gaming S&M and localization costs rising to RMB 32bn in 2024, pressuring near-term margins.

As China’s market slows, Level Infinite is the division’s primary growth engine, targeting double-digit CAGR in overseas revenues through 2026.

Hunyuan Enterprise AI Solutions

Hunyuan Enterprise AI Solutions is a Star in Tencent Holdings’ BCG matrix: Hunyuan, Tencent’s large language model, anchors its B2B push across finance, gaming, healthcare, and government, driving cloud AI revenue that helped Tencent Cloud grow 42% YoY in 2024 to RMB 72.6 billion (about USD 10.5B).

Fintech Wealth Management Services

Fintech Wealth Management Services: Tencent’s move beyond payments into wealth and insurance distribution within WeChat shows strong growth—assets under management via its platforms rose ~28% YoY to an estimated RMB 1.1 trillion by end-2025, driven by wallet market share ~45% and millions of monthly active users buying funds and insurance.

Ongoing risks: regulatory oversight (licensing, product limits) and required tech spend on risk models and KYC keep this a high-investment, high-growth quadrant versus banks.

- ~RMB 1.1T AUM (2025 est)

- ~28% YoY AUM growth (2024–25)

- ~45% digital wallet market share

- Needs continual regulatory navigation + tech investment

Smart Retail and SaaS Ecosystem

Tencent Holdings’ Smart Retail and SaaS ecosystem—anchored by WeCom (WeChat Work) and Mini Programs—holds a leading share in China’s digital retail transformation, with Tencent Cloud revenue up 38% in FY2024 and Mini Program monthly active users exceeding 900 million as of Dec 2024.

These tools power merchant-customer flows as retail shifts online; over 60% of surveyed Chinese retailers used Mini Programs for sales in 2024, and transaction GMV via Mini Programs grew ~45% YoY.

Tencent must keep investing in cloud capacity and product updates—Tencent Cloud capex rose in 2024—to repel Alibaba and ByteDance and convert platform usage into SaaS recurring revenue and higher-margin services.

- WeCom + Mini Programs: ~900M MAU (Dec 2024)

- Tencent Cloud revenue: +38% FY2024

- Mini Program GMV growth: ~45% YoY (2024)

- ~60% retailers using Mini Programs (2024 survey)

Tencent’s Growth Engines: Video, Cloud, Games, Fintech & Mini Programs Power Surge

Stars: WeChat Video Accounts, Level Infinite, Hunyuan AI, Fintech wealth, and Mini Programs drive Tencent’s high-growth businesses—WeChat Video ~28% short-video time, 650M MAU (2025); Tencent Games overseas ~25% of RMB201.5bn (2024); Tencent Cloud RMB72.6bn (42% YoY, 2024); AUM ~RMB1.1T (2025 est); Mini Programs 900M MAU (Dec 2024).

| Asset | Key 2024–25 metrics |

|---|---|

| WeChat Video | 28% time share; 650M MAU (2025) |

| Games (Level Infinite) | 25% overseas revenue of RMB201.5bn (2024) |

| Hunyuan/Cloud | RMB72.6bn Cloud rev; +42% YoY (2024) |

| Fintech AUM | ~RMB1.1T; +28% YoY (2024–25) |

| Mini Programs | 900M MAU (Dec 2024); GMV +45% YoY |

What is included in the product

BCG Matrix for Tencent: strategic placement of Stars, Cash Cows, Question Marks, Dogs with investment, hold, divest guidance and trend context.

One-page Tencent BCG Matrix mapping business units into quadrants for rapid portfolio prioritization and investor briefings.

Cash Cows

Domestic Online Games

Honor of Kings and Peacekeeper Elite together held ~57% of China’s mobile game grossing in 2024, with Honor of Kings reporting RMB 30.4 billion (~USD 4.2B) revenue in 2024 and Peacekeeper Elite ~RMB 18.7 billion, producing steady operating cash flow and low marginal costs versus initial dev spend.

These franchises fund Tencent Holdings’ R&D and global bets: Tencent allocated RMB 26.8 billion to overseas investments and experimental projects in 2024, largely covered by domestic online games’ free cash flow.

WeChat Core Messaging and Social

WeChat core messaging and social functions sit in a mature market where Tencent Holdings holds a near-monopoly in China, with 1.31 billion monthly active users as of Q4 2025, requiring maintenance more than aggressive growth.

The service generates steady, low-cost user data and access that underpins Tencent’s ad, payments, cloud, and gaming units, contributing to stable cash flow and cross-sell reach across the ecosystem.

Operating margins on WeChat-related services stay high because incremental user costs are low; in 2025 WeChat-related advertising and social commerce helped sustain Tencent’s platform revenue resilience amid slower overall growth.

Tencent Music Entertainment

Tencent Music Entertainment (TME) leads China’s streaming market with ~66% music subscription market share and 85m+ paying users as of Q4 2025, making it a cash cow in Tencent Holdings’ BCG matrix.

Revenue mix has stabilized: subscriptions and ads drove RMB 27.3B in FY2024 revenue with gross margins near 40%, yielding steady free cash flow.

That predictable cash flow funds Tencent’s broader digital-content investments and lets the group avoid high-risk capital injections into TME.

Payment Processing Infrastructure

The WeChat Pay ecosystem now handles an estimated 70% of China’s mobile peer-to-peer and point-of-sale micro-transactions, processing roughly CNY 20 trillion in 2024 and generating stable service fees despite slower user growth.

Growth in new users has decelerated to low single digits, but daily transaction volume—over 1 billion transactions per day—delivers predictable fee income and low marginal marketing costs.

As a utility-like cash cow, this unit supplies steady operating cashflow that funds Tencent’s higher-growth bets across gaming, cloud, and AI investments.

- 2024 volume ~CNY 20 trillion

- ~1 billion daily transactions

- Market share ~70% of mobile micro-payments

- User growth low single digits (2024)

Social Media Advertising

Social Media Advertising via WeChat Moments and Tencent’s wider social ecosystem is a mature, high-margin cash cow, capturing roughly 30–35% of China’s performance-ad spend in 2024 and generating double-digit operating margins for the segment.

Unparalleled user targeting (WeChat 1.4bn MAU in 2024) drives high ROI, low capex needs, and steady free cash flow that funded ~20% of Tencent’s R&D spend in 2024 (R&D = RMB 86.9bn).

- Market share: ~30–35% of performance ads (2024)

- WeChat MAU: 1.4 billion (2024)

- R&D funded: ~20% from ad cash flow (2024)

- Characteristics: high margins, low capex, stable FCF

Tencent’s cash engines: Gaming, WeChat, Pay and TME drive massive revenue and engagement

Strong cash cows: Honor of Kings + Peacekeeper Elite (~RMB 49.1B revenue, ~57% China mobile grossing 2024), WeChat (1.31B MAU Q4 2025; high margins, low incremental costs), WeChat Pay (~CNY 20T volume 2024; ~1B daily tx), Tencent Music (TME 85M+ paying users, RMB 27.3B FY2024).

| Unit | Key 2024–25 |

|---|---|

| Games | RMB49.1B; 57% market |

| 1.31B MAU; high margins | |

| WeChat Pay | CNY20T; 1B/day |

| TME | 85M+ pay; RMB27.3B |

Preview = Final Product

Tencent Holdings BCG Matrix

The file you're previewing is the exact Tencent Holdings BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready report crafted for strategic clarity and professional use.