Tenneco Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

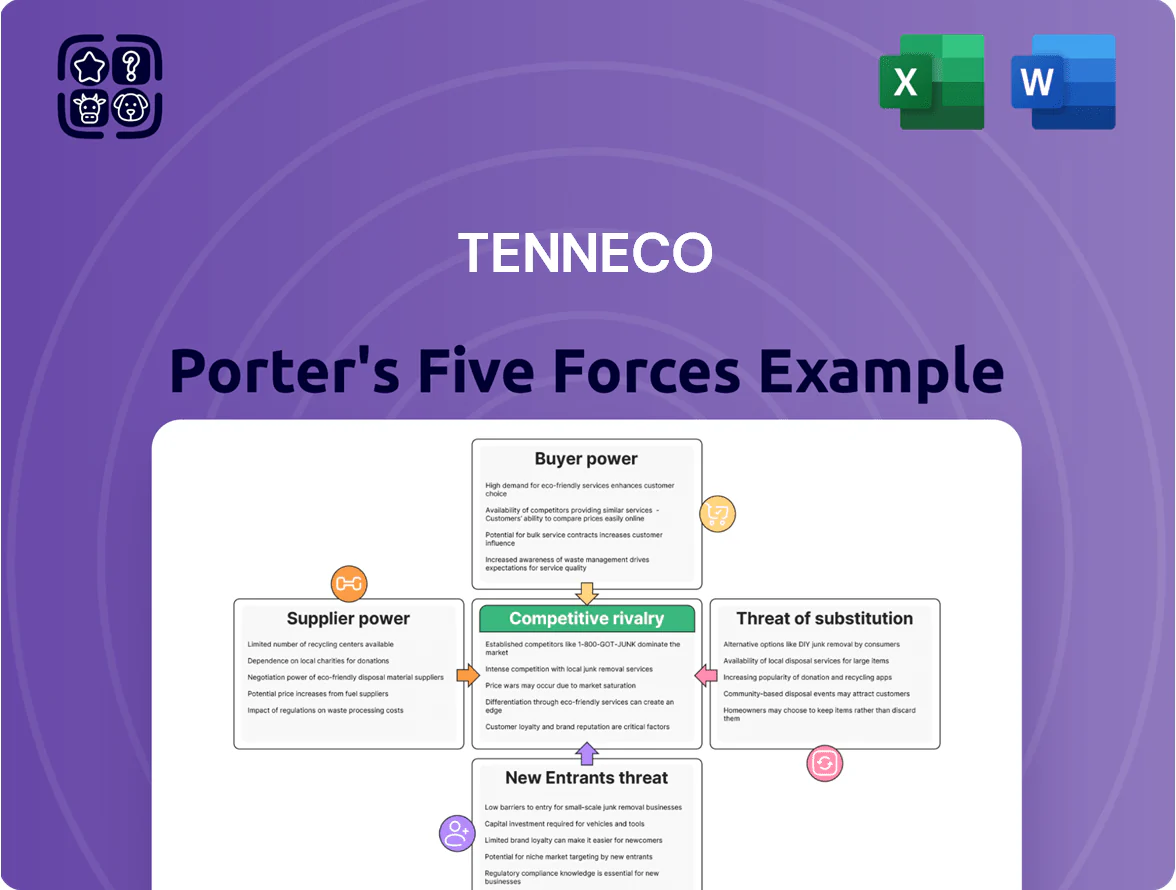

Tenneco faces intense competitive rivalry and evolving supplier dynamics as it adapts to electrification and aftermarket shifts, while buyer power and substitute threats vary across OE and aftermarket segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tenneco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Specialized Electronics Dependency

The growing use of electronic sensors in ride-control and braking systems gives specialized suppliers marked leverage over Tenneco; sensors now account for roughly 18% of ride-control module cost and 22% of braking-system value add in 2025 supplier audits. Many sensors are sole-sourced due to proprietary patents or tight specs, leaving Tenneco exposed to single-supplier risk. Supply-chain bottlenecks or a 10–25% sudden price spike in these parts could raise Tenneco’s COGS for affected lines by 2–4% and disrupt production. Operational contingency now requires multi-sourcing, longer inventory buffers, or pay-for-IP arrangements to reduce this supplier power.

Energy and Utility Costs

Manufacturing emission and ride-control systems is energy-intensive, so Tenneco is exposed to utility pricing: in 2024 global industrial electricity averages rose 8% year-over-year, pushing manufacturing margins down—Tenneco reported 2024 adjusted operating margin of 4.2%, partly due to higher energy and input costs.

Regional energy shocks, like Europe’s 2022–24 gas volatility, can spike costs quickly; a 20% rise in energy tariffs would add millions to Tenneco’s annual operating expense given its ~200 global plants.

Suppliers of energy-efficient equipment wield leverage as Tenneco decarbonizes: capital for retrofits and electrification can exceed $50k–$200k per production line, creating supplier-driven timing and price risk.

Tier Two Supplier Consolidation

Mergers among tier-two component makers have cut the supplier pool for basic parts by about 18% globally since 2019, reducing Tenneco’s ability to play vendors off each other for price or terms.

That consolidation raises switching costs and negotiation power for remaining suppliers, so Tenneco increasingly needs multi-year strategic partnerships to secure supply for key product lines and limit margin pressure.

- Supplier pool down ~18% since 2019

- Higher switching costs, tighter terms

- Multi-year contracts now common for core parts

- Partnerships reduce disruption risk, protect margins

Sustainability and ESG Compliance

Suppliers meeting strict ESG standards can charge 10–20% premiums as OEMs press Tenneco to green its supply chain; in 2024 over 60% of major auto OEMs had net-zero supplier requirements, raising sourcing costs for compliant parts.

Finding vendors that hit both cost targets and sustainability mandates is harder, boosting bargaining power for the compliant niche during contract talks and increasing Tenneco’s supplier risk.

- ESG-compliant suppliers demand 10–20% premium

- 60%+ OEMs had net-zero supplier rules in 2024

- Supply scarcity raises negotiation leverage

Supplier squeeze: commodity spikes, consolidation & ESG premiums pinch Tenneco’s thin margins

Suppliers hold moderate-to-high power: commodity price swings (steel +22% 2021–23; palladium ~$1,800/oz 2024) and sensor sole-sourcing raise input cost risk, while consolidation (supplier pool −18% since 2019) and ESG premiums (10–20%) tighten leverage, forcing multi-year contracts, hedging, and higher inventories to protect Tenneco’s thin margins (2024 adjusted operating margin 4.2%).

| Metric | Value |

|---|---|

| Steel change | +22% (2021–23) |

| Palladium | $1,800/oz (2024) |

| Supplier pool | −18% since 2019 |

| ESG premium | 10–20% |

| Adj. OP margin | 4.2% (2024) |

What is included in the product

Tailored exclusively for Tenneco, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, threats from substitutes and new entrants, and strategic barriers that shape the company’s pricing, margins, and competitive positioning.

A concise Porter's Five Forces snapshot tailored for Tenneco—highlighting supplier power, buyer leverage, competitive rivalry, threat of substitutes, and entrant risk to speed strategic decisions and investor pitches.

Customers Bargaining Power

High OEM Concentration

Major OEMs such as General Motors, Ford, and Volkswagen made up roughly 45–55% of Tenneco’s original-equipment revenue in 2024, giving these buyers outsized leverage to demand price cuts and extended payment terms.

Because a single OEM contract can represent multiple percentage points of sales, losing one would sharply reduce factory utilization and could cut quarterly revenue by double-digit percentages, pressuring margins and cash flow.

Aftermarket Distributor Leverage

Large U.S. retail chains and distributors now control about 55% of aftermarket sales, concentrating buying power against Tenneco brands like Monroe and Walker and forcing deeper trade discounts.

These buyers can switch to private labels or competitors quickly; in 2024 private-label share rose to ~12% in key categories, so pricing and promo support must be aggressive to avoid share loss.

Maintaining loyalty is getting pricier: Tenneco reported rising aftermarket SG&A per unit in 2024, indicating higher promo and rebate spending to protect shelf space.

Low Switching Costs for Standard Parts

For many standard braking and sealing parts, OEMs can switch suppliers with low friction and technical risk, so Tenneco faces strong price pressure—commodity OE brake pads and seals drove 2024 aftermarket ASP declines of ~3–5% in comparable segments. This forces competition on price and logistics; Tenneco reported 2024 gross margin of ~16% for ride-control and sealing lines versus 22% target, showing squeeze. Only continuous product innovation that creates technical stickiness—patented materials, system integration, or software-enabled diagnostics—can reduce this buyer power.

Electric Vehicle Platform Shifts

- EVs 16% of new sales 2024 (~14.4M)

- Tenneco 2024 net sales $13.6B

- One OEM loss could trim >10% revenue

- Must secure EV-specific thermal/ride contracts by 2027

Demand for Integrated Modular Systems

Customers shift to integrated modular systems, reducing purchases of standalone parts and pressuring Tenneco to deliver complex sub-assemblies that match OEM architectures.

This drives higher R&D spend—Tenneco increased R&D to about $95m in 2024—so buyers favor suppliers who cut OEM assembly time and internal costs.

- Buyers choose partners that simplify assembly

- Shift raises Tenneco R&D burden (~$95m in 2024)

- OEMs favor turnkey sub-assemblies, increasing customer bargaining power

Tenneco at Risk: OEM Leverage, EV Shift Threaten >10% Revenue and Tighten 16% Margins

Buyers hold strong leverage: top OEMs (45–55% of OE revenue) and large retailers (~55% aftermarket) force price cuts, longer terms, and demand integrated EV-ready systems; Tenneco’s 2024 metrics show $13.6B sales, R&D ~$95M, and EVs 16% of new car sales (~14.4M), so losing one OEM could cut >10% revenue and compress margins already at ~16% in key lines.

| Metric | 2024 |

|---|---|

| Tenneco net sales | $13.6B |

| R&D | $95M |

| OEM concentration | 45–55% |

| Aftermarket buyers | ~55% |

| EV share new sales | 16% (~14.4M) |

| Key line gross margin | ~16% |

Full Version Awaits

Tenneco Porter's Five Forces Analysis

This preview shows the exact Tenneco Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no mockups, fully formatted and ready for immediate download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Tenneco faces intense competitive rivalry and evolving supplier dynamics as it adapts to electrification and aftermarket shifts, while buyer power and substitute threats vary across OE and aftermarket segments.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Tenneco’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

Specialized Electronics Dependency

The growing use of electronic sensors in ride-control and braking systems gives specialized suppliers marked leverage over Tenneco; sensors now account for roughly 18% of ride-control module cost and 22% of braking-system value add in 2025 supplier audits. Many sensors are sole-sourced due to proprietary patents or tight specs, leaving Tenneco exposed to single-supplier risk. Supply-chain bottlenecks or a 10–25% sudden price spike in these parts could raise Tenneco’s COGS for affected lines by 2–4% and disrupt production. Operational contingency now requires multi-sourcing, longer inventory buffers, or pay-for-IP arrangements to reduce this supplier power.

Energy and Utility Costs

Manufacturing emission and ride-control systems is energy-intensive, so Tenneco is exposed to utility pricing: in 2024 global industrial electricity averages rose 8% year-over-year, pushing manufacturing margins down—Tenneco reported 2024 adjusted operating margin of 4.2%, partly due to higher energy and input costs.

Regional energy shocks, like Europe’s 2022–24 gas volatility, can spike costs quickly; a 20% rise in energy tariffs would add millions to Tenneco’s annual operating expense given its ~200 global plants.

Suppliers of energy-efficient equipment wield leverage as Tenneco decarbonizes: capital for retrofits and electrification can exceed $50k–$200k per production line, creating supplier-driven timing and price risk.

Tier Two Supplier Consolidation

Mergers among tier-two component makers have cut the supplier pool for basic parts by about 18% globally since 2019, reducing Tenneco’s ability to play vendors off each other for price or terms.

That consolidation raises switching costs and negotiation power for remaining suppliers, so Tenneco increasingly needs multi-year strategic partnerships to secure supply for key product lines and limit margin pressure.

- Supplier pool down ~18% since 2019

- Higher switching costs, tighter terms

- Multi-year contracts now common for core parts

- Partnerships reduce disruption risk, protect margins

Sustainability and ESG Compliance

Suppliers meeting strict ESG standards can charge 10–20% premiums as OEMs press Tenneco to green its supply chain; in 2024 over 60% of major auto OEMs had net-zero supplier requirements, raising sourcing costs for compliant parts.

Finding vendors that hit both cost targets and sustainability mandates is harder, boosting bargaining power for the compliant niche during contract talks and increasing Tenneco’s supplier risk.

- ESG-compliant suppliers demand 10–20% premium

- 60%+ OEMs had net-zero supplier rules in 2024

- Supply scarcity raises negotiation leverage

Supplier squeeze: commodity spikes, consolidation & ESG premiums pinch Tenneco’s thin margins

Suppliers hold moderate-to-high power: commodity price swings (steel +22% 2021–23; palladium ~$1,800/oz 2024) and sensor sole-sourcing raise input cost risk, while consolidation (supplier pool −18% since 2019) and ESG premiums (10–20%) tighten leverage, forcing multi-year contracts, hedging, and higher inventories to protect Tenneco’s thin margins (2024 adjusted operating margin 4.2%).

| Metric | Value |

|---|---|

| Steel change | +22% (2021–23) |

| Palladium | $1,800/oz (2024) |

| Supplier pool | −18% since 2019 |

| ESG premium | 10–20% |

| Adj. OP margin | 4.2% (2024) |

What is included in the product

Tailored exclusively for Tenneco, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, threats from substitutes and new entrants, and strategic barriers that shape the company’s pricing, margins, and competitive positioning.

A concise Porter's Five Forces snapshot tailored for Tenneco—highlighting supplier power, buyer leverage, competitive rivalry, threat of substitutes, and entrant risk to speed strategic decisions and investor pitches.

Customers Bargaining Power

High OEM Concentration

Major OEMs such as General Motors, Ford, and Volkswagen made up roughly 45–55% of Tenneco’s original-equipment revenue in 2024, giving these buyers outsized leverage to demand price cuts and extended payment terms.

Because a single OEM contract can represent multiple percentage points of sales, losing one would sharply reduce factory utilization and could cut quarterly revenue by double-digit percentages, pressuring margins and cash flow.

Aftermarket Distributor Leverage

Large U.S. retail chains and distributors now control about 55% of aftermarket sales, concentrating buying power against Tenneco brands like Monroe and Walker and forcing deeper trade discounts.

These buyers can switch to private labels or competitors quickly; in 2024 private-label share rose to ~12% in key categories, so pricing and promo support must be aggressive to avoid share loss.

Maintaining loyalty is getting pricier: Tenneco reported rising aftermarket SG&A per unit in 2024, indicating higher promo and rebate spending to protect shelf space.

Low Switching Costs for Standard Parts

For many standard braking and sealing parts, OEMs can switch suppliers with low friction and technical risk, so Tenneco faces strong price pressure—commodity OE brake pads and seals drove 2024 aftermarket ASP declines of ~3–5% in comparable segments. This forces competition on price and logistics; Tenneco reported 2024 gross margin of ~16% for ride-control and sealing lines versus 22% target, showing squeeze. Only continuous product innovation that creates technical stickiness—patented materials, system integration, or software-enabled diagnostics—can reduce this buyer power.

Electric Vehicle Platform Shifts

- EVs 16% of new sales 2024 (~14.4M)

- Tenneco 2024 net sales $13.6B

- One OEM loss could trim >10% revenue

- Must secure EV-specific thermal/ride contracts by 2027

Demand for Integrated Modular Systems

Customers shift to integrated modular systems, reducing purchases of standalone parts and pressuring Tenneco to deliver complex sub-assemblies that match OEM architectures.

This drives higher R&D spend—Tenneco increased R&D to about $95m in 2024—so buyers favor suppliers who cut OEM assembly time and internal costs.

- Buyers choose partners that simplify assembly

- Shift raises Tenneco R&D burden (~$95m in 2024)

- OEMs favor turnkey sub-assemblies, increasing customer bargaining power

Tenneco at Risk: OEM Leverage, EV Shift Threaten >10% Revenue and Tighten 16% Margins

Buyers hold strong leverage: top OEMs (45–55% of OE revenue) and large retailers (~55% aftermarket) force price cuts, longer terms, and demand integrated EV-ready systems; Tenneco’s 2024 metrics show $13.6B sales, R&D ~$95M, and EVs 16% of new car sales (~14.4M), so losing one OEM could cut >10% revenue and compress margins already at ~16% in key lines.

| Metric | 2024 |

|---|---|

| Tenneco net sales | $13.6B |

| R&D | $95M |

| OEM concentration | 45–55% |

| Aftermarket buyers | ~55% |

| EV share new sales | 16% (~14.4M) |

| Key line gross margin | ~16% |

Full Version Awaits

Tenneco Porter's Five Forces Analysis

This preview shows the exact Tenneco Porter’s Five Forces analysis you’ll receive after purchase—no placeholders, no mockups, fully formatted and ready for immediate download.