Tenneco SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Tenneco’s recent pivot toward emissions control and ride-performance technologies highlights strong engineering capabilities and diversification, but legacy automotive cycles and supply-chain volatility pose material risks; regulatory tailwinds could accelerate aftermarket demand while margin pressure and integration challenges may constrain near-term returns. Purchase the full SWOT analysis to access a research-backed, editable report (Word + Excel) with detailed strategic recommendations, financial context, and investor-ready insights.

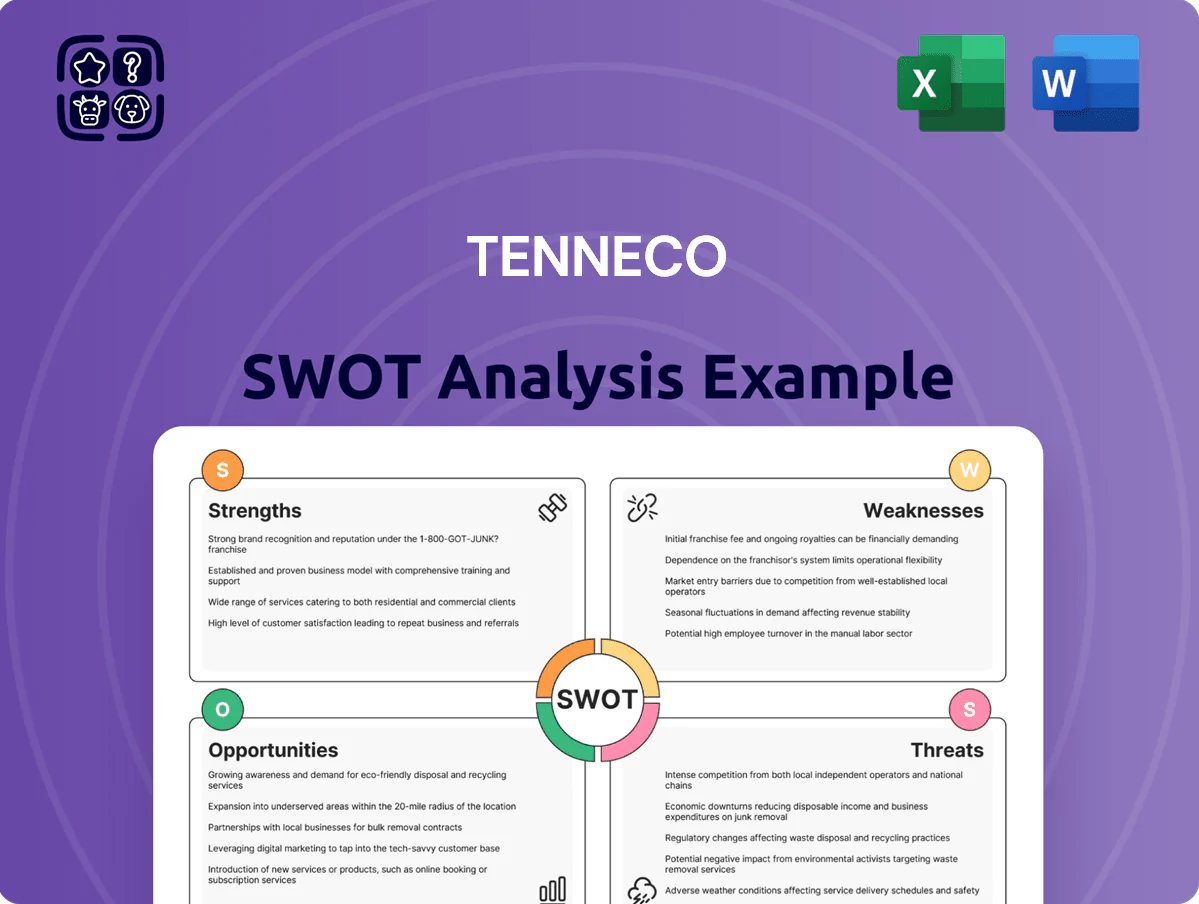

Strengths

Dominant Global Aftermarket Brand Portfolio

Tenneco’s Monroe, Moog, Walker, and Champion brands drive a dominant global aftermarket portfolio, covering ~25% share in key North American and European repair segments as of 2025 and anchoring recurring demand.

These well‑known brands generate higher gross margins—roughly 6–8 percentage points above OE parts—providing steady, high‑margin revenue that cushions Tenneco from new‑vehicle cyclicality.

By year‑end 2025 Tenneco maintained pricing power, passing through ~60–70% of input cost inflation and preserving aftermarket volumes despite global supply‑chain pressures.

Extensive Global Manufacturing Footprint

Tenneco operates over 230 manufacturing and distribution sites across North America, Europe and Asia, letting it supply major OEMs like Ford, Stellantis and Volkswagen locally and cut cross-border lead times by roughly 20–30%. This geographic spread lowers logistics spend and inventory days; in 2024 Tenneco reported global revenue of about $18.4 billion, underpinned by regional sales balance. The footprint is a strategic asset as automakers regionalize supply chains to reduce disruption and tariff risk.

Deep Engineering Expertise in Ride Performance

Tenneco leads in advanced suspension and NVH (noise, vibration, harshness) tech, supplying electronic suspension systems to premium OEMs; these products represented about 22% of its 2024 powertrain and ride revenues, driving margin resilience.

The company’s e‑suspension modules improve ride and handling, contributing to multi-year contracts with BMW, Mercedes, and Stellantis, and creating a steep technical barrier to entry.

That engineering depth supports recurring R&D partnerships and helped Tenneco secure $1.1 billion in ride-systems backlog at year-end 2024, anchoring long-term revenue visibility.

Diversified Revenue Across Multiple Segments

Tenneco operates four segments—Clean Air, Powertrain, Performance Solutions, and Motorparts—spreading revenue risk and softening exposure to any single market downturn.

Electrification pressures Powertrain and Clean Air long-term, but Motorparts and Performance Solutions (aftermarket, ride-control parts) remain resilient across ICE and EV fleets.

In 2024 Tenneco reported consolidated revenue of $14.8 billion, with aftermarket and performance contributing roughly 38% of sales, supporting cash flow stability.

- Four-segment mix reduces single-product cyclicality

- Motorparts + Performance ~38% of 2024 revenue

- Electrification risks offset by aftermarket demand

Strategic Private Equity Backing

Since Apollo Global Management took Tenneco private in 2022, disciplined capital allocation and operational-efficiency programs have driven cashflow improvement and margin recovery through 2025.

Private ownership has let management pursue multi-year strategic pivots—supply‑chain modernization and plant consolidations—without public quarterly pressure, supporting a focus on long-term value.

Apollo’s capital and deal expertise enabled more aggressive restructuring: ~US$1.1bn in capex and ~US$400m in restructuring spend approved 2023–2025, accelerating EBITDA recovery.

- Taken private 2022 by Apollo Global Management

- ~US$1.1bn capex 2023–2025

- ~US$400m restructuring spend 2023–2025

- Improved margins and cashflow through 2025

Tenneco: Strong 25% aftermarket share, $14.8B revenue & $1.1B e‑suspension backlog

Tenneco’s strong aftermarket brands (Monroe, Moog, Walker, Champion) supply ~25% share in key NA/EU repair segments (2025), driving 6–8ppt higher gross margins than OE and steady revenue; 230+ sites cut lead times 20–30% and supported $14.8bn revenue (2024); e‑suspension/ride backlog $1.1bn (2024); Apollo-backed capex ~$1.1bn and restructuring ~$400m (2023–25).

| Metric | Value |

|---|---|

| 2024 Revenue | $14.8bn |

| Aftermarket share | ~25% |

| Gross margin lift | 6–8ppt |

| Sites | 230+ |

| Ride backlog | $1.1bn |

| Capex (23–25) | $1.1bn |

| Restructuring (23–25) | $400m |

What is included in the product

Provides a concise SWOT analysis of Tenneco, outlining its operational strengths and weaknesses, identifying market opportunities and innovation drivers, and mapping external threats that could impact the company’s competitive position and strategic growth.

Delivers a concise Tenneco SWOT matrix for rapid strategic alignment, ideal for executives needing a quick snapshot of the company’s strengths, weaknesses, opportunities, and threats.

Weaknesses

Significant Debt and Interest Obligations

Tenneco’s 2018 private equity buyout left the firm with roughly $6.5 billion of debt; servicing that load consumed about $420 million in interest expense in 2024, and higher-for-longer rates push coverage ratios under stress. This leverage restricts R&D and capex—Tenneco spent $250 million on R&D in 2024, well below peers—limiting product development and electrification bets. Financial flexibility is constrained as management balances mandatory debt repayments with needed capital investments, raising refinancing and liquidity risk.

High Exposure to Internal Combustion Engines

Complex Organizational and Operational Structure

The integration of historical acquisitions has left Tenneco with a complex structure that slows decisions; management reported in 2024 that restructuring-related costs totaled about $120 million, highlighting agility constraints.

Redundant IT and administrative systems across regions drive inefficiencies and higher overhead; selling, general & administrative (SG&A) was $1.1 billion in 2024, up 6% year-over-year.

Streamlining is a multi-year program still short of full synergy—Tenneco projected $200–250 million of run-rate synergies by 2025 but acknowledged execution risks and uneven progress across business units.

Sensitivity to Raw Material Price Volatility

Tenneco depends on steel, aluminum and precious metals (for catalytic converters), so raw-material price spikes can quickly compress margins; nickel and palladium rose ~18% and 12% in 2024, raising component costs for OEM suppliers.

Hedging and pass-through pricing reduce risk but lag effects often cause temporary margin squeeze—Tenneco reported 2024 gross margin of ~12.8%, down 1.4 pts YoY due partly to commodity cost timing.

Geopolitical shocks or trade-policy shifts (tariffs, export controls) can sharply raise input costs and logistic fees, worsening short-term profitability.

- High commodity dependency: steel, Al, precious metals

- 2024: nickel +18%, palladium +12% (market moves)

- Hedging helps but lags; 2024 gross margin ~12.8%

- Trade shocks and tariffs amplify cost volatility

Historical Margin Compression in OEM Contracts

The OEM segment faces consistent downward pricing pressure from a few powerful global automakers, forcing Tenneco to deliver annual productivity gains; OEM operating margins fell to about 2.5% in FY2024, squeezing profitability.

Thin OEM margins force near-flawless execution—any production hiccup quickly erodes profits—so Tenneco depends on its aftermarket business, which generated roughly $1.6B and higher mid-single-digit margins in 2024, to subsidize OEM returns.

- FY2024 OEM margin ~2.5%

- Aftermarket revenue ≈ $1.6B in 2024

- Aftermarket mid-single-digit margins vs OEM low single-digits

Tenneco's $6.5B Debt Chokes R&D as EV Rise Threatens $10.1B ICE Revenue

Tenneco’s heavy 2018 buyout debt (~$6.5B) drove ~$420M interest in 2024, constraining R&D ($250M) and capex; pro forma ICE-linked revenue was ~$10.1B of $13.2B in 2024, risking decline as EVs hit ~14% sales in 2024. 2024 operating cash flow ≈$620M, gross margin ~12.8%, OEM margin ~2.5%, aftermarket $1.6B. Restructuring costs ~$120M; projected synergies $200–250M by 2025.

| Metric | 2024 |

|---|---|

| Debt | $6.5B |

| Interest | $420M |

| R&D | $250M |

| Revenue (pro forma) | $13.2B |

| ICE-linked | $10.1B |

| Op CF | $620M |

| Gross margin | 12.8% |

| OEM margin | 2.5% |

| Aftermarket | $1.6B |

Preview the Actual Deliverable

Tenneco SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Tenneco’s recent pivot toward emissions control and ride-performance technologies highlights strong engineering capabilities and diversification, but legacy automotive cycles and supply-chain volatility pose material risks; regulatory tailwinds could accelerate aftermarket demand while margin pressure and integration challenges may constrain near-term returns. Purchase the full SWOT analysis to access a research-backed, editable report (Word + Excel) with detailed strategic recommendations, financial context, and investor-ready insights.

Strengths

Dominant Global Aftermarket Brand Portfolio

Tenneco’s Monroe, Moog, Walker, and Champion brands drive a dominant global aftermarket portfolio, covering ~25% share in key North American and European repair segments as of 2025 and anchoring recurring demand.

These well‑known brands generate higher gross margins—roughly 6–8 percentage points above OE parts—providing steady, high‑margin revenue that cushions Tenneco from new‑vehicle cyclicality.

By year‑end 2025 Tenneco maintained pricing power, passing through ~60–70% of input cost inflation and preserving aftermarket volumes despite global supply‑chain pressures.

Extensive Global Manufacturing Footprint

Tenneco operates over 230 manufacturing and distribution sites across North America, Europe and Asia, letting it supply major OEMs like Ford, Stellantis and Volkswagen locally and cut cross-border lead times by roughly 20–30%. This geographic spread lowers logistics spend and inventory days; in 2024 Tenneco reported global revenue of about $18.4 billion, underpinned by regional sales balance. The footprint is a strategic asset as automakers regionalize supply chains to reduce disruption and tariff risk.

Deep Engineering Expertise in Ride Performance

Tenneco leads in advanced suspension and NVH (noise, vibration, harshness) tech, supplying electronic suspension systems to premium OEMs; these products represented about 22% of its 2024 powertrain and ride revenues, driving margin resilience.

The company’s e‑suspension modules improve ride and handling, contributing to multi-year contracts with BMW, Mercedes, and Stellantis, and creating a steep technical barrier to entry.

That engineering depth supports recurring R&D partnerships and helped Tenneco secure $1.1 billion in ride-systems backlog at year-end 2024, anchoring long-term revenue visibility.

Diversified Revenue Across Multiple Segments

Tenneco operates four segments—Clean Air, Powertrain, Performance Solutions, and Motorparts—spreading revenue risk and softening exposure to any single market downturn.

Electrification pressures Powertrain and Clean Air long-term, but Motorparts and Performance Solutions (aftermarket, ride-control parts) remain resilient across ICE and EV fleets.

In 2024 Tenneco reported consolidated revenue of $14.8 billion, with aftermarket and performance contributing roughly 38% of sales, supporting cash flow stability.

- Four-segment mix reduces single-product cyclicality

- Motorparts + Performance ~38% of 2024 revenue

- Electrification risks offset by aftermarket demand

Strategic Private Equity Backing

Since Apollo Global Management took Tenneco private in 2022, disciplined capital allocation and operational-efficiency programs have driven cashflow improvement and margin recovery through 2025.

Private ownership has let management pursue multi-year strategic pivots—supply‑chain modernization and plant consolidations—without public quarterly pressure, supporting a focus on long-term value.

Apollo’s capital and deal expertise enabled more aggressive restructuring: ~US$1.1bn in capex and ~US$400m in restructuring spend approved 2023–2025, accelerating EBITDA recovery.

- Taken private 2022 by Apollo Global Management

- ~US$1.1bn capex 2023–2025

- ~US$400m restructuring spend 2023–2025

- Improved margins and cashflow through 2025

Tenneco: Strong 25% aftermarket share, $14.8B revenue & $1.1B e‑suspension backlog

Tenneco’s strong aftermarket brands (Monroe, Moog, Walker, Champion) supply ~25% share in key NA/EU repair segments (2025), driving 6–8ppt higher gross margins than OE and steady revenue; 230+ sites cut lead times 20–30% and supported $14.8bn revenue (2024); e‑suspension/ride backlog $1.1bn (2024); Apollo-backed capex ~$1.1bn and restructuring ~$400m (2023–25).

| Metric | Value |

|---|---|

| 2024 Revenue | $14.8bn |

| Aftermarket share | ~25% |

| Gross margin lift | 6–8ppt |

| Sites | 230+ |

| Ride backlog | $1.1bn |

| Capex (23–25) | $1.1bn |

| Restructuring (23–25) | $400m |

What is included in the product

Provides a concise SWOT analysis of Tenneco, outlining its operational strengths and weaknesses, identifying market opportunities and innovation drivers, and mapping external threats that could impact the company’s competitive position and strategic growth.

Delivers a concise Tenneco SWOT matrix for rapid strategic alignment, ideal for executives needing a quick snapshot of the company’s strengths, weaknesses, opportunities, and threats.

Weaknesses

Significant Debt and Interest Obligations

Tenneco’s 2018 private equity buyout left the firm with roughly $6.5 billion of debt; servicing that load consumed about $420 million in interest expense in 2024, and higher-for-longer rates push coverage ratios under stress. This leverage restricts R&D and capex—Tenneco spent $250 million on R&D in 2024, well below peers—limiting product development and electrification bets. Financial flexibility is constrained as management balances mandatory debt repayments with needed capital investments, raising refinancing and liquidity risk.

High Exposure to Internal Combustion Engines

Complex Organizational and Operational Structure

The integration of historical acquisitions has left Tenneco with a complex structure that slows decisions; management reported in 2024 that restructuring-related costs totaled about $120 million, highlighting agility constraints.

Redundant IT and administrative systems across regions drive inefficiencies and higher overhead; selling, general & administrative (SG&A) was $1.1 billion in 2024, up 6% year-over-year.

Streamlining is a multi-year program still short of full synergy—Tenneco projected $200–250 million of run-rate synergies by 2025 but acknowledged execution risks and uneven progress across business units.

Sensitivity to Raw Material Price Volatility

Tenneco depends on steel, aluminum and precious metals (for catalytic converters), so raw-material price spikes can quickly compress margins; nickel and palladium rose ~18% and 12% in 2024, raising component costs for OEM suppliers.

Hedging and pass-through pricing reduce risk but lag effects often cause temporary margin squeeze—Tenneco reported 2024 gross margin of ~12.8%, down 1.4 pts YoY due partly to commodity cost timing.

Geopolitical shocks or trade-policy shifts (tariffs, export controls) can sharply raise input costs and logistic fees, worsening short-term profitability.

- High commodity dependency: steel, Al, precious metals

- 2024: nickel +18%, palladium +12% (market moves)

- Hedging helps but lags; 2024 gross margin ~12.8%

- Trade shocks and tariffs amplify cost volatility

Historical Margin Compression in OEM Contracts

The OEM segment faces consistent downward pricing pressure from a few powerful global automakers, forcing Tenneco to deliver annual productivity gains; OEM operating margins fell to about 2.5% in FY2024, squeezing profitability.

Thin OEM margins force near-flawless execution—any production hiccup quickly erodes profits—so Tenneco depends on its aftermarket business, which generated roughly $1.6B and higher mid-single-digit margins in 2024, to subsidize OEM returns.

- FY2024 OEM margin ~2.5%

- Aftermarket revenue ≈ $1.6B in 2024

- Aftermarket mid-single-digit margins vs OEM low single-digits

Tenneco's $6.5B Debt Chokes R&D as EV Rise Threatens $10.1B ICE Revenue

Tenneco’s heavy 2018 buyout debt (~$6.5B) drove ~$420M interest in 2024, constraining R&D ($250M) and capex; pro forma ICE-linked revenue was ~$10.1B of $13.2B in 2024, risking decline as EVs hit ~14% sales in 2024. 2024 operating cash flow ≈$620M, gross margin ~12.8%, OEM margin ~2.5%, aftermarket $1.6B. Restructuring costs ~$120M; projected synergies $200–250M by 2025.

| Metric | 2024 |

|---|---|

| Debt | $6.5B |

| Interest | $420M |

| R&D | $250M |

| Revenue (pro forma) | $13.2B |

| ICE-linked | $10.1B |

| Op CF | $620M |

| Gross margin | 12.8% |

| OEM margin | 2.5% |

| Aftermarket | $1.6B |

Preview the Actual Deliverable

Tenneco SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.