Tokyo Electric Power Company Holdings Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

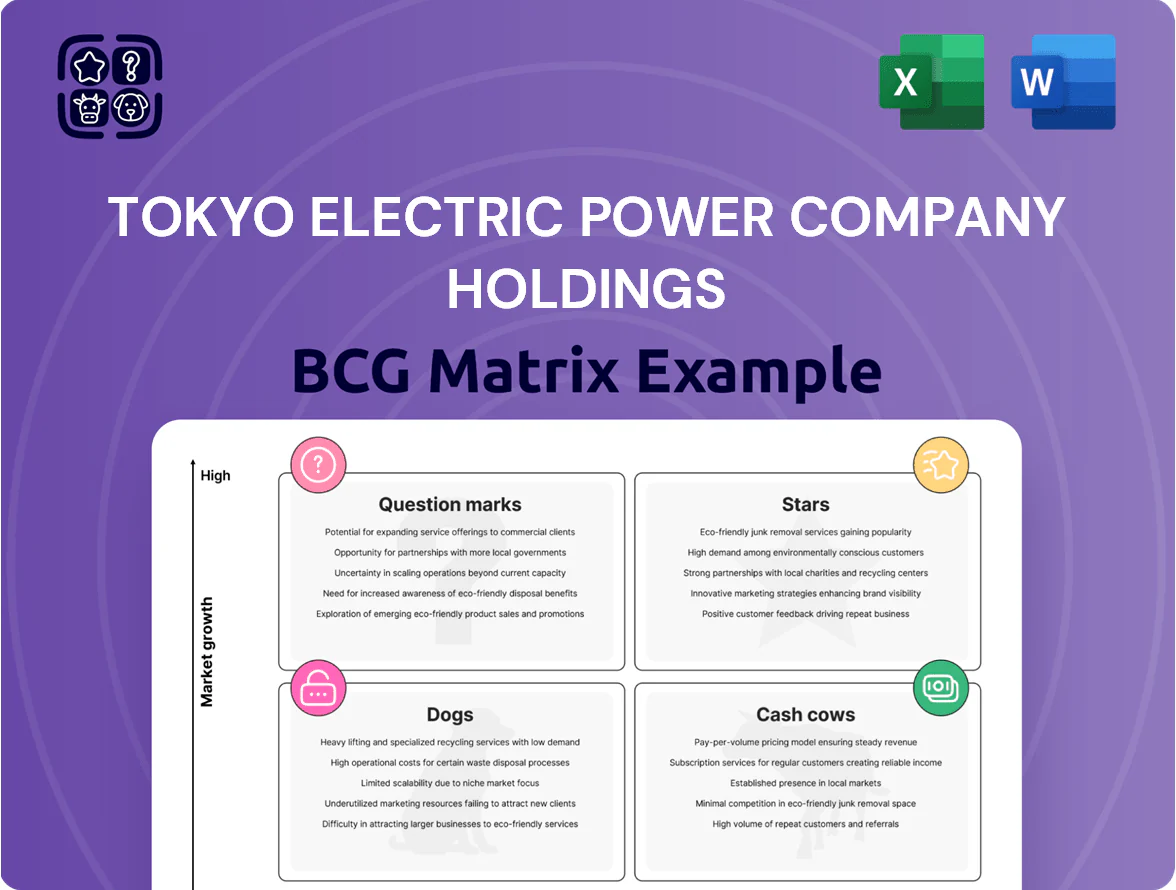

Tokyo Electric Power Company Holdings faces a mixed portfolio: legacy nuclear and thermal assets behave like Cash Cows with steady cash flow but rising regulatory and decommissioning costs, while renewables and grid modernization initiatives are emerging Question Marks that could become Stars with targeted investment and policy support. Strategic divestments and reallocation toward distributed generation and storage could unlock value and reduce risk exposure. This preview highlights key quadrant dynamics—purchase the full BCG Matrix for a complete breakdown, actionable recommendations, and ready-to-use Word and Excel deliverables.

Stars

Offshore Wind Development

TEPCO Renewable Power scaled offshore wind to 2.1 GW of capacity under development in 2025, aligning with Japan’s goal of 10 GW by 2030 and capturing Kanto subsidies covering up to 30% of capex.

Strong market growth (projected 20% CAGR 2025–30) and feed-in supports make this a Star in TEPCO’s BCG matrix despite ~¥400–600 billion per-GW upfront costs.

Electric Vehicle Charging Networks

TEPCO’s EV charging networks are a Star: it controls ~45% of high-speed chargers in Tokyo metro (2025 METI registry) and added 1,200 DC fast ports in 2024 alone, driving revenue growth above group average.

With Japan targeting 23–25 million EVs by 2030 (Japan EV strategy, 2023) rising domestic EV sales 28% YoY in 2024, this unit is a primary growth engine for TEPCO.

TEPCO is investing ¥120 billion through 2026 in smart charging and V2G (vehicle-to-grid) pilots to enable grid load balancing and ancillary service revenues; pilots showed peak shave potential of 150 MW.

International Energy Investment

Through strategic partnerships and direct investments, Tokyo Electric Power Company Holdings (TEPCO) has increased renewable capacity abroad to about 1.1 GW by Q3 2025, targeting Southeast Asia and Europe via joint ventures with local IPPs and a €300m equity fund commitment.

These ventures let TEPCO capture faster 6–8% market growth in developing economies while shifting revenue mix—international renewables rose to 9% of consolidated EBITDA in FY2024, up from 3% in FY2020.

Given global green energy investment projected at $1.7 trillion in 2025, TEPCO has made international renewables a top capital allocation priority, earmarking ¥60–80 billion for 2026–27 expansion.

Advanced Energy Storage Solutions

TEPCO’s Advanced Energy Storage is a Star: utility-scale battery demand rose 48% in Japan 2024, and TEPCO has committed ¥120 billion (~$800M) to lithium-ion and vanadium flow projects through 2026, positioning it as a market leader in grid stability and fast-response capacity.

This unit tackles supply-demand volatility, supports frequency control and peak shaving, and benefits from rising corporate PPA storage requirements; project-level IRRs target 8–12% with expected CAGR ~25% to 2028.

- 2024 Japan utility storage demand +48%

- TEPCO capex ¥120B (to 2026)

- Target IRR 8–12%

- Market CAGR ~25% (to 2028)

Smart Grid Modernization

Smart Grid Modernization sits as a Star for Tokyo Electric Power Company Holdings (TEPCO) in 2025: TEPCO Power Grid’s IoT sensors and AI grid-management rollouts drove 18% revenue growth in grid services in FY2024, and pilot smart-meter deployments reached 1.2 million units by Dec 2024.

Next-gen meters plus predictive-maintenance cut SAIDI (outage duration) by 22% in pilots and unlocked energy-as-a-service contracts worth ¥75 billion ($520M) pipeline through 2025, cementing tech leadership as decentralization rises.

- 18% grid-services revenue growth FY2024

- 1.2M smart meters deployed by Dec 2024

- 22% SAIDI reduction in pilots

- ¥75B energy-as-a-service pipeline (2025)

Power Play: Offshore Wind, EV Charging & Storage Drive 2025 Growth

Stars: Offshore wind (2.1 GW dev, ¥400–600B/GW capex), EV charging (~45% Tokyo high-speed share, +1,200 DC ports 2024), Advanced Storage (¥120B to 2026, target IRR 8–12%), Smart Grid (1.2M meters, 18% grid-services growth FY2024).

| Unit | 2025 Metric | Key finance |

|---|---|---|

| Offshore wind | 2.1 GW dev | ¥400–600B/GW |

| EV charging | 45% Tokyo share | 1,200 DC ports added 2024 |

| Storage | Committed ¥120B | IRR 8–12% |

| Smart Grid | 1.2M meters | 18% revenue growth FY2024 |

What is included in the product

Comprehensive BCG review of TEPCO’s units: Stars (renewables), Cash Cows (nuclear/thermal), Question Marks (grid tech), Dogs (legacy assets) with invest/hold/divest guidance.

One-page overview placing each TEPCO business unit in a quadrant for quick strategic clarity and executive decision-making.

Cash Cows

Power Transmission and Distribution

TEPCO Power Grid, a regulated monopoly serving Kanto, is TEPCO HD’s cash cow, delivering steady EBITDA margins near 35% and operating income around ¥600–700 billion annually (FY2024), funding decommissioning and R&D for renewables and hydrogen.

Core Retail Electricity Sales

Despite retail liberalization, TEPCO Energy Partner serves about 27 million customers in the Tokyo metro area, retaining ~40–45% market share and delivering stable annual retail revenue near ¥1.2 trillion (FY2024), making it a cash cow in a mature, low-growth market.

Thermal Power via JERA

JERA, the joint venture between Tokyo Electric Power Company Holdings (TEPCO) and Chubu Electric, supplies roughly 40% of TEPCO Group’s base-load power via efficient LNG and thermal plants and accounted for about ¥1.6 trillion in group revenue contribution in FY2024.

As a mature, high-market-share cash cow, JERA generated operating cash flow of ~¥420 billion in FY2024, buffering TEPCO during winter peaks and market price spikes.

Growth is constrained by Japan’s 2030–2050 decarbonization rules and stricter emissions limits, so JERA’s thermal assets mainly fund short-term capex and debt reduction for the group.

Power Line Maintenance Services

The Power Line Maintenance Services subsidiary delivers high-margin, low-competition work, contributing stable EBITDA—about ¥45–55 billion annually in 2024—thanks to long-term contracts covering 70%+ of grid assets and essential outage-response roles.

Predictable cash flows and capex-light operations make it a classic cash cow for Tokyo Electric Power Company Holdings, funding network upgrades and cross-subsidiary needs with minimal marketing spend.

- 2024 revenue ≈ ¥120–140B

- EBITDA margin ~37% (2024)

- 70%+ revenue from multiyear contracts

- Low churn; critical services in all cycles

Real Estate and Asset Leasing

TEPCO holds ~3,200 hectares of land and >1,000 utility sites leased to telcos and manufacturers, generating steady rental income; in FY2024 these leases contributed ~¥45 billion to non-core revenue, reflecting low volatility in a mature market with high entry barriers.

Income is passively managed to bolster liquidity—cash leases support working capital and debt service, lowering parent-company financing costs and providing predictable, low-risk returns versus core power generation.

- ~3,200 hectares land

- ~1,000 utility/site leases

- FY2024 income ≈ ¥45 billion

- Low volatility, high entry barriers

TEPCO cash cows: ¥4.0T revenue, ¥1.2T EBITDA, ¥480B OpCF funding transition

TEPCO’s cash cows—TEPCO Power Grid, TEPCO Energy Partner, JERA, maintenance services, and leases—delivered FY2024 combined EBITDA ~¥1.2T, operating cash flow ~¥480B, and revenue ~¥4.0T, funding capex, decommissioning, and renewables transition.

| Unit | FY2024 |

|---|---|

| Revenue | ¥4.0T |

| EBITDA | ¥1.2T |

| OpCF | ¥480B |

Preview = Final Product

Tokyo Electric Power Company Holdings BCG Matrix

The file you're previewing is the exact Tokyo Electric Power Company Holdings BCG Matrix report you will receive after purchase—no watermarks, no placeholder content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Tokyo Electric Power Company Holdings faces a mixed portfolio: legacy nuclear and thermal assets behave like Cash Cows with steady cash flow but rising regulatory and decommissioning costs, while renewables and grid modernization initiatives are emerging Question Marks that could become Stars with targeted investment and policy support. Strategic divestments and reallocation toward distributed generation and storage could unlock value and reduce risk exposure. This preview highlights key quadrant dynamics—purchase the full BCG Matrix for a complete breakdown, actionable recommendations, and ready-to-use Word and Excel deliverables.

Stars

Offshore Wind Development

TEPCO Renewable Power scaled offshore wind to 2.1 GW of capacity under development in 2025, aligning with Japan’s goal of 10 GW by 2030 and capturing Kanto subsidies covering up to 30% of capex.

Strong market growth (projected 20% CAGR 2025–30) and feed-in supports make this a Star in TEPCO’s BCG matrix despite ~¥400–600 billion per-GW upfront costs.

Electric Vehicle Charging Networks

TEPCO’s EV charging networks are a Star: it controls ~45% of high-speed chargers in Tokyo metro (2025 METI registry) and added 1,200 DC fast ports in 2024 alone, driving revenue growth above group average.

With Japan targeting 23–25 million EVs by 2030 (Japan EV strategy, 2023) rising domestic EV sales 28% YoY in 2024, this unit is a primary growth engine for TEPCO.

TEPCO is investing ¥120 billion through 2026 in smart charging and V2G (vehicle-to-grid) pilots to enable grid load balancing and ancillary service revenues; pilots showed peak shave potential of 150 MW.

International Energy Investment

Through strategic partnerships and direct investments, Tokyo Electric Power Company Holdings (TEPCO) has increased renewable capacity abroad to about 1.1 GW by Q3 2025, targeting Southeast Asia and Europe via joint ventures with local IPPs and a €300m equity fund commitment.

These ventures let TEPCO capture faster 6–8% market growth in developing economies while shifting revenue mix—international renewables rose to 9% of consolidated EBITDA in FY2024, up from 3% in FY2020.

Given global green energy investment projected at $1.7 trillion in 2025, TEPCO has made international renewables a top capital allocation priority, earmarking ¥60–80 billion for 2026–27 expansion.

Advanced Energy Storage Solutions

TEPCO’s Advanced Energy Storage is a Star: utility-scale battery demand rose 48% in Japan 2024, and TEPCO has committed ¥120 billion (~$800M) to lithium-ion and vanadium flow projects through 2026, positioning it as a market leader in grid stability and fast-response capacity.

This unit tackles supply-demand volatility, supports frequency control and peak shaving, and benefits from rising corporate PPA storage requirements; project-level IRRs target 8–12% with expected CAGR ~25% to 2028.

- 2024 Japan utility storage demand +48%

- TEPCO capex ¥120B (to 2026)

- Target IRR 8–12%

- Market CAGR ~25% (to 2028)

Smart Grid Modernization

Smart Grid Modernization sits as a Star for Tokyo Electric Power Company Holdings (TEPCO) in 2025: TEPCO Power Grid’s IoT sensors and AI grid-management rollouts drove 18% revenue growth in grid services in FY2024, and pilot smart-meter deployments reached 1.2 million units by Dec 2024.

Next-gen meters plus predictive-maintenance cut SAIDI (outage duration) by 22% in pilots and unlocked energy-as-a-service contracts worth ¥75 billion ($520M) pipeline through 2025, cementing tech leadership as decentralization rises.

- 18% grid-services revenue growth FY2024

- 1.2M smart meters deployed by Dec 2024

- 22% SAIDI reduction in pilots

- ¥75B energy-as-a-service pipeline (2025)

Power Play: Offshore Wind, EV Charging & Storage Drive 2025 Growth

Stars: Offshore wind (2.1 GW dev, ¥400–600B/GW capex), EV charging (~45% Tokyo high-speed share, +1,200 DC ports 2024), Advanced Storage (¥120B to 2026, target IRR 8–12%), Smart Grid (1.2M meters, 18% grid-services growth FY2024).

| Unit | 2025 Metric | Key finance |

|---|---|---|

| Offshore wind | 2.1 GW dev | ¥400–600B/GW |

| EV charging | 45% Tokyo share | 1,200 DC ports added 2024 |

| Storage | Committed ¥120B | IRR 8–12% |

| Smart Grid | 1.2M meters | 18% revenue growth FY2024 |

What is included in the product

Comprehensive BCG review of TEPCO’s units: Stars (renewables), Cash Cows (nuclear/thermal), Question Marks (grid tech), Dogs (legacy assets) with invest/hold/divest guidance.

One-page overview placing each TEPCO business unit in a quadrant for quick strategic clarity and executive decision-making.

Cash Cows

Power Transmission and Distribution

TEPCO Power Grid, a regulated monopoly serving Kanto, is TEPCO HD’s cash cow, delivering steady EBITDA margins near 35% and operating income around ¥600–700 billion annually (FY2024), funding decommissioning and R&D for renewables and hydrogen.

Core Retail Electricity Sales

Despite retail liberalization, TEPCO Energy Partner serves about 27 million customers in the Tokyo metro area, retaining ~40–45% market share and delivering stable annual retail revenue near ¥1.2 trillion (FY2024), making it a cash cow in a mature, low-growth market.

Thermal Power via JERA

JERA, the joint venture between Tokyo Electric Power Company Holdings (TEPCO) and Chubu Electric, supplies roughly 40% of TEPCO Group’s base-load power via efficient LNG and thermal plants and accounted for about ¥1.6 trillion in group revenue contribution in FY2024.

As a mature, high-market-share cash cow, JERA generated operating cash flow of ~¥420 billion in FY2024, buffering TEPCO during winter peaks and market price spikes.

Growth is constrained by Japan’s 2030–2050 decarbonization rules and stricter emissions limits, so JERA’s thermal assets mainly fund short-term capex and debt reduction for the group.

Power Line Maintenance Services

The Power Line Maintenance Services subsidiary delivers high-margin, low-competition work, contributing stable EBITDA—about ¥45–55 billion annually in 2024—thanks to long-term contracts covering 70%+ of grid assets and essential outage-response roles.

Predictable cash flows and capex-light operations make it a classic cash cow for Tokyo Electric Power Company Holdings, funding network upgrades and cross-subsidiary needs with minimal marketing spend.

- 2024 revenue ≈ ¥120–140B

- EBITDA margin ~37% (2024)

- 70%+ revenue from multiyear contracts

- Low churn; critical services in all cycles

Real Estate and Asset Leasing

TEPCO holds ~3,200 hectares of land and >1,000 utility sites leased to telcos and manufacturers, generating steady rental income; in FY2024 these leases contributed ~¥45 billion to non-core revenue, reflecting low volatility in a mature market with high entry barriers.

Income is passively managed to bolster liquidity—cash leases support working capital and debt service, lowering parent-company financing costs and providing predictable, low-risk returns versus core power generation.

- ~3,200 hectares land

- ~1,000 utility/site leases

- FY2024 income ≈ ¥45 billion

- Low volatility, high entry barriers

TEPCO cash cows: ¥4.0T revenue, ¥1.2T EBITDA, ¥480B OpCF funding transition

TEPCO’s cash cows—TEPCO Power Grid, TEPCO Energy Partner, JERA, maintenance services, and leases—delivered FY2024 combined EBITDA ~¥1.2T, operating cash flow ~¥480B, and revenue ~¥4.0T, funding capex, decommissioning, and renewables transition.

| Unit | FY2024 |

|---|---|

| Revenue | ¥4.0T |

| EBITDA | ¥1.2T |

| OpCF | ¥480B |

Preview = Final Product

Tokyo Electric Power Company Holdings BCG Matrix

The file you're previewing is the exact Tokyo Electric Power Company Holdings BCG Matrix report you will receive after purchase—no watermarks, no placeholder content, just the fully formatted, analysis-ready document crafted for strategic clarity and professional use.