Tokyo Electric Power Company Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

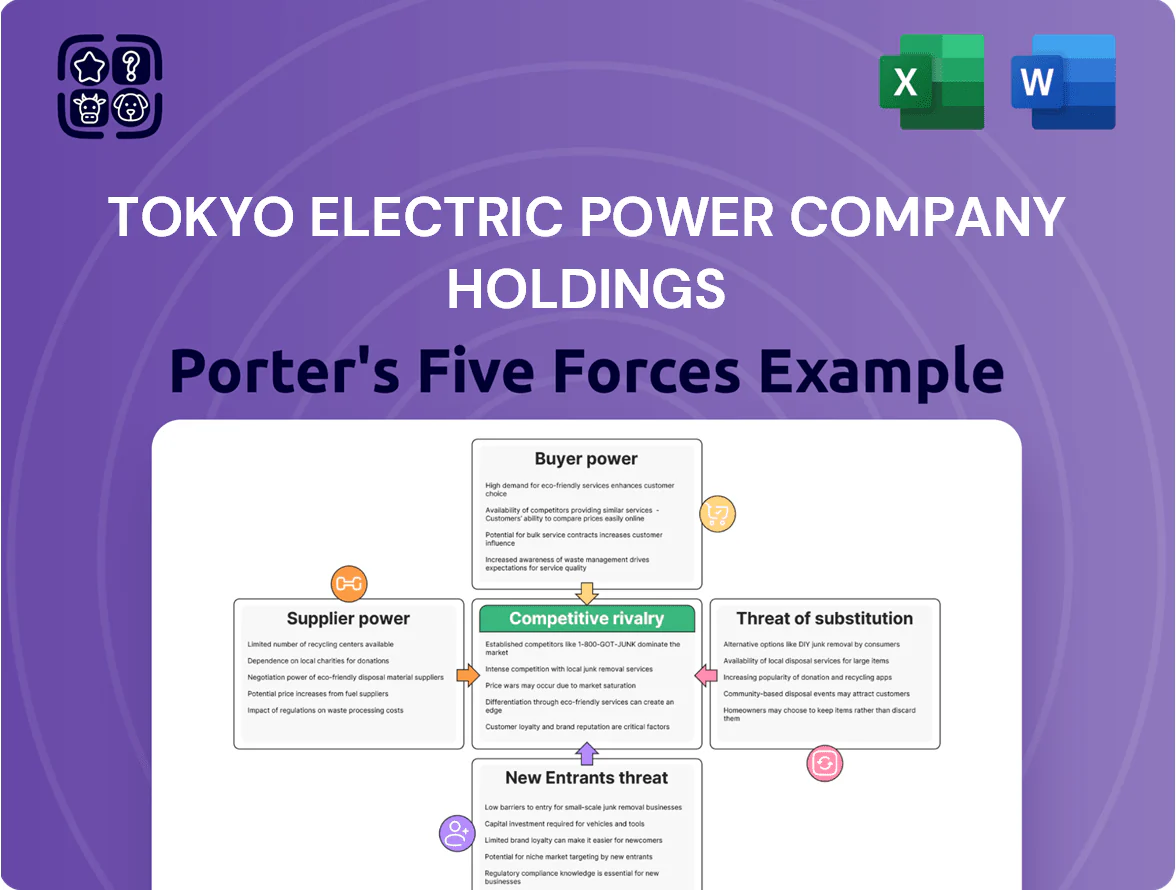

Tokyo Electric Power Company Holdings faces intense regulatory scrutiny, high capital intensity, and modest threat from new entrants, while supplier power and substitutes vary with fuel mix and renewables adoption.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore TEPCO’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Fuel Market Volatility

TEPCO depends on imported LNG and coal after nuclear shutdowns, importing about 40% of Japan’s LNG in FY2023 and burning ~30 million tonnes coal equivalent in 2024, making it a price taker in global markets.

Geopolitical shocks—Russia supply cuts in 2022 and 2023 LNG price spikes (peak JKM ~$60/MMBtu in 2022)—raise generation costs and force pass-through or margin compression.

Large integrated suppliers (Shell, ExxonMobil, JERA) set terms; TEPCO’s limited bargaining power and long-term contract exposure restrict price negotiation and hedging flexibility.

Specialized Decommissioning Services

The ongoing Fukushima Daiichi decommissioning needs advanced engineering and robotics available from only a handful of global firms (eg, Toshiba, Hitachi-GE, and international specialists), giving suppliers strong leverage; their expertise drives safety and regulatory compliance, forcing TEPCO to accept high contract premiums—TEPCO’s decommissioning budget rose to about ¥8.9 trillion (USD 64 billion) projected through 2051, so supplier concentration creates costly, limited alternatives.

Nuclear Fuel Procurement and Enrichment

Securing uranium and enrichment services relies on a handful of global suppliers—Cameco, Orano, and Kazatomprom control ~60% of production as of 2024—plus IAEA oversight, giving them strong leverage over TEPCO’s restart timing and costs; TEPCO plans to restart reactors to recover from ¥4.2 trillion liabilities (2024), so supplier terms materially affect economics. Japan lacks large-scale domestic enrichment, cementing vendor power on price and delivery.

Renewable Energy Infrastructure Providers

As TEPCO ramps offshore wind and solar for 2050 carbon neutrality, it faces a concentrated supplier market: the top 5 turbine makers (Siemens Gamesa, Vestas, GE Renewable Energy, Goldwind, Mingyang) held ~70% of global market share in 2024, creating firm pricing and long lead times.

High global demand caused turbine delivery backlogs averaging 18–30 months in 2023–24 and solar PV polysilicon shortages that lifted module prices ~25% in 2022–24, so TEPCO’s late aggressive entry forces direct competition with utilities for scarce components.

- Top-5 turbine vendors ≈70% share (2024)

- Turbine lead times 18–30 months (2023–24)

- Solar module prices up ~25% (2022–24)

- Late entry increases procurement cost and project delays

Grid Maintenance and Equipment Vendors

Grid maintenance for TEPCO’s Kanto network needs specialized transformers, switchgear, and heavy machinery; 2024 capital expenditures were ¥493 billion, much tied to such equipment.

The rise of smart-grid tech means new suppliers offer proprietary software and sensors, creating potential vendor lock-in and raising supplier bargaining power over time.

- ¥493bn 2024 capex tied to grid equipment

- Long-term ties with domestic giants (Mitsubishi, Hitachi)

- Proprietary smart-grid tech increases lock-in risk

Supplier Concentration Zooms Costs & Lead Times for TEPCO — Price Taker Risks Rising

Suppliers hold strong power: TEPCO is a price taker for LNG/coal (importer of ~40% of Japan’s LNG in FY2023) and faces concentrated vendors for decommissioning, uranium (~60% market control by Cameco/Orano/Kazatomprom in 2024), turbines (top‑5 ≈70% share) and grid gear, driving higher costs, long lead times and limited negotiation.

| Item | Metric |

|---|---|

| LNG share (FY2023) | ~40% |

| Uranium suppliers (2024) | ~60% |

| Top‑5 turbines (2024) | ≈70% market share |

| Turbine lead times (2023‑24) | 18–30 months |

| Decommissioning budget | ¥8.9tn (to 2051) |

What is included in the product

Tailored exclusively for Tokyo Electric Power Company Holdings, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, substitutes, and entry barriers shaping its market position, with strategic insight into disruptive threats and regulatory dynamics.

Compact Porter's Five Forces snapshot for Tokyo Electric Power Company Holdings—quickly assess regulatory, supplier, buyer, entrant, and rivalry pressures to guide strategic and investment decisions.

Customers Bargaining Power

Retail Market Liberalization

The full liberalization of Japan’s retail electricity market in April 2016 lets residential and small-business customers pick providers, boosting buyer power; as of 2024 about 40% of households had switched at least once, pressuring incumbents.

Consumers can churn for lower prices or bundled services, and with new entrants like regional New Power Producers and Suppliers offering rates 5–12% below TEPCO’s standard plans, switching costs are low.

TEPCO must prioritize retention—loyalty pricing, smart-meter services, and bundled energy solutions—since a 1% annual market-share loss could cut ~¥20–30 billion in revenue based on TEPCO HD’s 2024 consolidated operating revenue of ¥3.2 trillion.

Corporate Demand for Green Energy

Large industrial and commercial clients now demand renewable energy certificates to hit ESG and net-zero targets; globally corporate PPA volume hit a record 30.4 GW in 2023 and Japan saw ~1.2 GW corporate deals in 2024, giving buyers strong leverage.

These high-volume buyers can insist on tailored power purchase agreements or switch to greener providers; TEPCO must offer competitively priced green power or risk losing top corporate accounts that account for a disproportionate share of margin.

Low Switching Costs for Households

Advancements in smart meters and standardized switching now let Kanto households change electricity providers in under 10 minutes; Japan METI reported 45% of households had smart meters by 2023 and switching rates in liberalized regions hit 12% in 2024. Comparison sites and apps show real-time tariffs, so TEPCO (Tokyo Electric Power Company Holdings) must keep retail margins tight—its 2024 retail margin fell to ~3.2%—to stay competitive in a crowded market.

Price Sensitivity in an Inflationary Environment

Rising global fuel prices pushed Japan’s wholesale LNG and coal costs up ~40% in 2021–2023, making households more price-sensitive and resisting TEPCO tariff hikes tied to fuel pass-through.

Strong public/political pressure and the 2023 METI guidance limited full cost pass-through, so customers gain indirect bargaining power via government intervention that caps consumer bills.

- Wholesale fuel +40% (2021–2023)

- METI guidance 2023 limits pass-through

- Public pushback raises political risk to rate increases

Growth of Energy Self-Sufficiency

The falling cost of residential solar (module prices down ~60% since 2019) and home batteries (Li-ion pack costs ~120 USD/kWh in 2024) lets households and businesses cut grid purchases from TEPCO and sell surplus power, increasing customer bargaining power.

As prosumer adoption rises—Japan installed ~7.3 GW of distributed PV in 2023—customers can choose low-grid consumption or time-shift demand, forcing TEPCO to offer flexible rates and services to retain revenue.

- Residential PV + storage lowers grid dependency

- Japan distributed PV ~7.3 GW (2023)

- Battery cost ~120 USD/kWh (2024)

- Prosumers push flexible tariffs and services

Rising customer power: 40% switch, thin margins, PV & batteries squeeze utilities

Customers hold strong bargaining power: 40% households switched by 2024, retail margin fell to ~3.2% (TEPCO HD 2024 revenue ¥3.2T), smart meters ~45% (2023) enable 10‑min switching, distributed PV ~7.3 GW (2023) and battery costs ~120 USD/kWh (2024) cut grid demand, corporate PPAs ~1.2 GW (2024) raise buyer leverage, and METI 2023 guidance limits fuel pass-through.

| Metric | Value |

|---|---|

| Household switch rate | 40% (2024) |

| TEPCO revenue | ¥3.2T (2024) |

| Retail margin | ~3.2% (2024) |

| Smart meter share | 45% (2023) |

| Distributed PV | 7.3 GW (2023) |

| Battery cost | ~120 USD/kWh (2024) |

| Corporate PPAs Japan | ~1.2 GW (2024) |

Same Document Delivered

Tokyo Electric Power Company Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tokyo Electric Power Company Holdings you’ll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted analysis—ready for download and use the moment you buy.

No mockups: what you see is the deliverable and will be available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Tokyo Electric Power Company Holdings faces intense regulatory scrutiny, high capital intensity, and modest threat from new entrants, while supplier power and substitutes vary with fuel mix and renewables adoption.

This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore TEPCO’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Global Fuel Market Volatility

TEPCO depends on imported LNG and coal after nuclear shutdowns, importing about 40% of Japan’s LNG in FY2023 and burning ~30 million tonnes coal equivalent in 2024, making it a price taker in global markets.

Geopolitical shocks—Russia supply cuts in 2022 and 2023 LNG price spikes (peak JKM ~$60/MMBtu in 2022)—raise generation costs and force pass-through or margin compression.

Large integrated suppliers (Shell, ExxonMobil, JERA) set terms; TEPCO’s limited bargaining power and long-term contract exposure restrict price negotiation and hedging flexibility.

Specialized Decommissioning Services

The ongoing Fukushima Daiichi decommissioning needs advanced engineering and robotics available from only a handful of global firms (eg, Toshiba, Hitachi-GE, and international specialists), giving suppliers strong leverage; their expertise drives safety and regulatory compliance, forcing TEPCO to accept high contract premiums—TEPCO’s decommissioning budget rose to about ¥8.9 trillion (USD 64 billion) projected through 2051, so supplier concentration creates costly, limited alternatives.

Nuclear Fuel Procurement and Enrichment

Securing uranium and enrichment services relies on a handful of global suppliers—Cameco, Orano, and Kazatomprom control ~60% of production as of 2024—plus IAEA oversight, giving them strong leverage over TEPCO’s restart timing and costs; TEPCO plans to restart reactors to recover from ¥4.2 trillion liabilities (2024), so supplier terms materially affect economics. Japan lacks large-scale domestic enrichment, cementing vendor power on price and delivery.

Renewable Energy Infrastructure Providers

As TEPCO ramps offshore wind and solar for 2050 carbon neutrality, it faces a concentrated supplier market: the top 5 turbine makers (Siemens Gamesa, Vestas, GE Renewable Energy, Goldwind, Mingyang) held ~70% of global market share in 2024, creating firm pricing and long lead times.

High global demand caused turbine delivery backlogs averaging 18–30 months in 2023–24 and solar PV polysilicon shortages that lifted module prices ~25% in 2022–24, so TEPCO’s late aggressive entry forces direct competition with utilities for scarce components.

- Top-5 turbine vendors ≈70% share (2024)

- Turbine lead times 18–30 months (2023–24)

- Solar module prices up ~25% (2022–24)

- Late entry increases procurement cost and project delays

Grid Maintenance and Equipment Vendors

Grid maintenance for TEPCO’s Kanto network needs specialized transformers, switchgear, and heavy machinery; 2024 capital expenditures were ¥493 billion, much tied to such equipment.

The rise of smart-grid tech means new suppliers offer proprietary software and sensors, creating potential vendor lock-in and raising supplier bargaining power over time.

- ¥493bn 2024 capex tied to grid equipment

- Long-term ties with domestic giants (Mitsubishi, Hitachi)

- Proprietary smart-grid tech increases lock-in risk

Supplier Concentration Zooms Costs & Lead Times for TEPCO — Price Taker Risks Rising

Suppliers hold strong power: TEPCO is a price taker for LNG/coal (importer of ~40% of Japan’s LNG in FY2023) and faces concentrated vendors for decommissioning, uranium (~60% market control by Cameco/Orano/Kazatomprom in 2024), turbines (top‑5 ≈70% share) and grid gear, driving higher costs, long lead times and limited negotiation.

| Item | Metric |

|---|---|

| LNG share (FY2023) | ~40% |

| Uranium suppliers (2024) | ~60% |

| Top‑5 turbines (2024) | ≈70% market share |

| Turbine lead times (2023‑24) | 18–30 months |

| Decommissioning budget | ¥8.9tn (to 2051) |

What is included in the product

Tailored exclusively for Tokyo Electric Power Company Holdings, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, substitutes, and entry barriers shaping its market position, with strategic insight into disruptive threats and regulatory dynamics.

Compact Porter's Five Forces snapshot for Tokyo Electric Power Company Holdings—quickly assess regulatory, supplier, buyer, entrant, and rivalry pressures to guide strategic and investment decisions.

Customers Bargaining Power

Retail Market Liberalization

The full liberalization of Japan’s retail electricity market in April 2016 lets residential and small-business customers pick providers, boosting buyer power; as of 2024 about 40% of households had switched at least once, pressuring incumbents.

Consumers can churn for lower prices or bundled services, and with new entrants like regional New Power Producers and Suppliers offering rates 5–12% below TEPCO’s standard plans, switching costs are low.

TEPCO must prioritize retention—loyalty pricing, smart-meter services, and bundled energy solutions—since a 1% annual market-share loss could cut ~¥20–30 billion in revenue based on TEPCO HD’s 2024 consolidated operating revenue of ¥3.2 trillion.

Corporate Demand for Green Energy

Large industrial and commercial clients now demand renewable energy certificates to hit ESG and net-zero targets; globally corporate PPA volume hit a record 30.4 GW in 2023 and Japan saw ~1.2 GW corporate deals in 2024, giving buyers strong leverage.

These high-volume buyers can insist on tailored power purchase agreements or switch to greener providers; TEPCO must offer competitively priced green power or risk losing top corporate accounts that account for a disproportionate share of margin.

Low Switching Costs for Households

Advancements in smart meters and standardized switching now let Kanto households change electricity providers in under 10 minutes; Japan METI reported 45% of households had smart meters by 2023 and switching rates in liberalized regions hit 12% in 2024. Comparison sites and apps show real-time tariffs, so TEPCO (Tokyo Electric Power Company Holdings) must keep retail margins tight—its 2024 retail margin fell to ~3.2%—to stay competitive in a crowded market.

Price Sensitivity in an Inflationary Environment

Rising global fuel prices pushed Japan’s wholesale LNG and coal costs up ~40% in 2021–2023, making households more price-sensitive and resisting TEPCO tariff hikes tied to fuel pass-through.

Strong public/political pressure and the 2023 METI guidance limited full cost pass-through, so customers gain indirect bargaining power via government intervention that caps consumer bills.

- Wholesale fuel +40% (2021–2023)

- METI guidance 2023 limits pass-through

- Public pushback raises political risk to rate increases

Growth of Energy Self-Sufficiency

The falling cost of residential solar (module prices down ~60% since 2019) and home batteries (Li-ion pack costs ~120 USD/kWh in 2024) lets households and businesses cut grid purchases from TEPCO and sell surplus power, increasing customer bargaining power.

As prosumer adoption rises—Japan installed ~7.3 GW of distributed PV in 2023—customers can choose low-grid consumption or time-shift demand, forcing TEPCO to offer flexible rates and services to retain revenue.

- Residential PV + storage lowers grid dependency

- Japan distributed PV ~7.3 GW (2023)

- Battery cost ~120 USD/kWh (2024)

- Prosumers push flexible tariffs and services

Rising customer power: 40% switch, thin margins, PV & batteries squeeze utilities

Customers hold strong bargaining power: 40% households switched by 2024, retail margin fell to ~3.2% (TEPCO HD 2024 revenue ¥3.2T), smart meters ~45% (2023) enable 10‑min switching, distributed PV ~7.3 GW (2023) and battery costs ~120 USD/kWh (2024) cut grid demand, corporate PPAs ~1.2 GW (2024) raise buyer leverage, and METI 2023 guidance limits fuel pass-through.

| Metric | Value |

|---|---|

| Household switch rate | 40% (2024) |

| TEPCO revenue | ¥3.2T (2024) |

| Retail margin | ~3.2% (2024) |

| Smart meter share | 45% (2023) |

| Distributed PV | 7.3 GW (2023) |

| Battery cost | ~120 USD/kWh (2024) |

| Corporate PPAs Japan | ~1.2 GW (2024) |

Same Document Delivered

Tokyo Electric Power Company Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Tokyo Electric Power Company Holdings you’ll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted analysis—ready for download and use the moment you buy.

No mockups: what you see is the deliverable and will be available to you instantly after payment.