Teradata Porter's Five Forces Analysis

From Overview to Strategy Blueprint

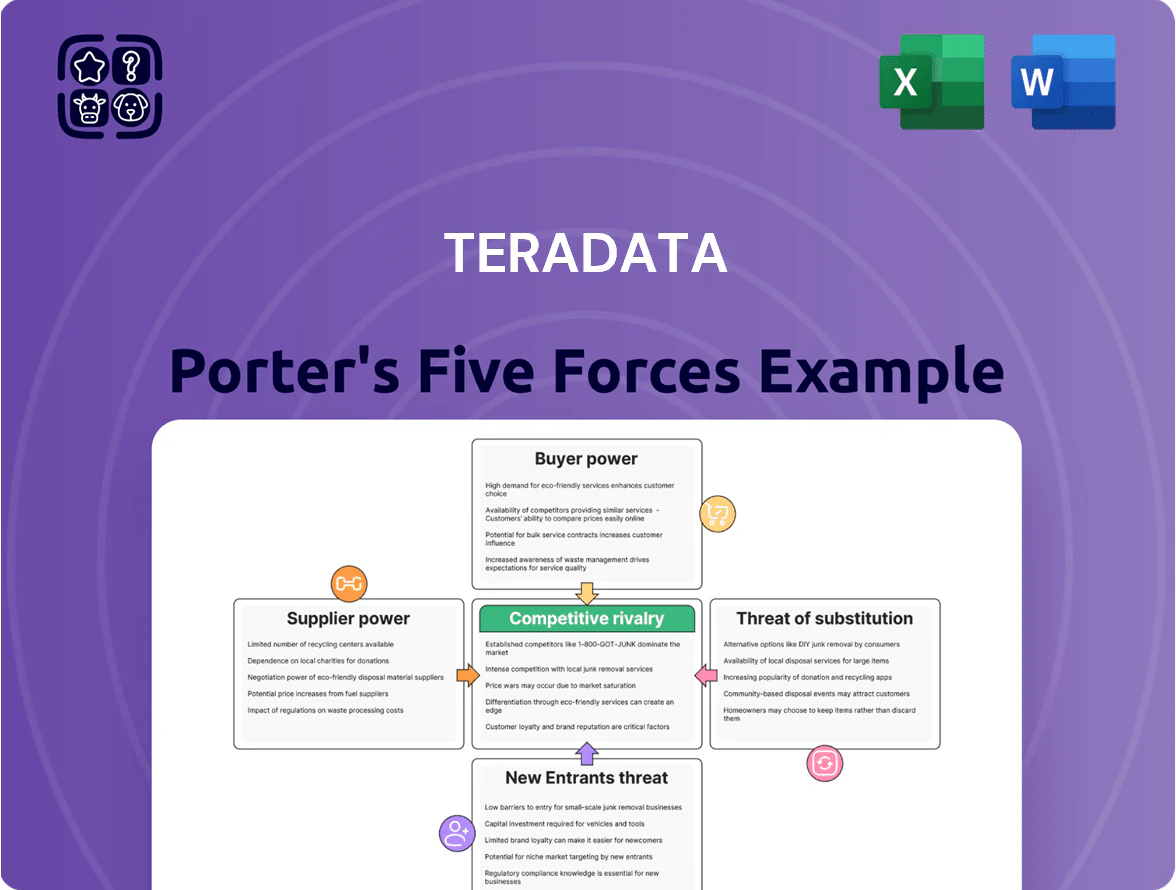

Teradata faces intense rivalry from cloud-native analytics firms and major cloud providers, with moderate supplier leverage and growing buyer power as enterprises demand flexible, consumption-based pricing.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Teradata’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Public Cloud Infrastructure Providers

Teradata depends on AWS, Microsoft Azure, and Google Cloud Platform to host Vantage, giving these three providers strong bargaining power over infrastructure pricing and SLAs.

By late 2025, the top three control roughly 65–70% of global cloud IaaS/PaaS, limiting Teradata’s ability to negotiate without risking feature or performance parity.

This reliance raises cost and strategic risk: a 10–20% cloud price hike or increased push of native analytics by providers could materially erode Teradata gross margins and customer retention.

Specialized Semiconductor and Hardware Manufacturers

Suppliers of advanced GPUs and CPUs like NVIDIA and Intel exert strong bargaining power because Teradata’s on-prem and hybrid appliances still rely on specialized silicon for HPC; NVIDIA held ~80% GPU market share for data-center AI in 2024 and price premiums persisted into 2025. Tight allocation and multi-quarter lead times for AI-optimized chips mean higher component costs and delivery risk. Teradata must lock multi-year contracts and diversify suppliers to protect performance and timelines.

Scarcity of Specialized Technical Talent

The supply of software engineers and data scientists expert in massive parallel processing and cloud architecture is tight in 2025; US STEM job openings hit 1.4M in 2024, and top talent commands 20–40% higher pay, boosting supplier power over Teradata.

Teradata competes with FAANG and well-funded startups for this scarce pool; maintaining proprietary kernel expertise is a critical bottleneck, so 2025 hiring and retention spend rose ~15% year-over-year to protect the innovation pipeline.

Third-Party Software and Integration Partners

Teradata relies on many third-party software components and proprietary connectors to stay interoperable; in 2025 about 18–25% of enterprise deployments cite third-party adapters as critical integration points.

Vendors of specialized software or connectors can raise fees or change standards, squeezing Teradata’s gross margins — vendor-driven licensing hikes of 5–12% yearly would cut platform margins materially.

Customer demand for plug-and-play in 2025 forces Teradata to preserve partnerships and compatibility, increasing supplier leverage and the risk that external IP capture reduces Teradata’s share of analytics value.

- 18–25% of deployments rely on third-party connectors

- Potential vendor price hikes 5–12% annually

- Dependency risks margin compression and value capture by vendors

Data Center and Co-location Providers

For hybrid and private cloud customers, Teradata depends on third-party data centers that control power, cooling, and network links—core to its on-premises value.

High-density power and low-latency networking needs shrink provider choice in some regions, raising switching costs and deployment delays.

By end-2025, a ~15–25% rise in commercial electricity prices in key markets increased facility leverage during renewals and SLAs.

- Dependency on third-party facilities

- Geographic limits due to power/network specs

- Rising energy costs (15–25% by 2025) boost supplier leverage

Supplier squeeze: cloud, NVIDIA, talent drive costs up 15–25% for Teradata

Suppliers (cloud hyperscalers, NVIDIA/Intel, talent, connectors, data centers) hold high bargaining power for Teradata in 2025—top-3 cloud 65–70% share, NVIDIA ~80% DC GPU share, STEM job openings 1.4M, hiring cost +15% YoY, third-party connector reliance 18–25%, potential vendor fee hikes 5–12%, energy costs +15–25%.

| Supplier | Key metric (2025) |

|---|---|

| Top-3 cloud | 65–70% market share |

| NVIDIA (DC GPU) | ~80% share |

| STEM openings | 1.4M (2024) |

| Hiring cost | +15% YoY |

| Connector reliance | 18–25% deployments |

| Vendor fee risk | +5–12% annually |

| Energy costs | +15–25% by 2025 |

What is included in the product

Tailored Porter's Five Forces analysis for Teradata that uncovers competitive drivers, customer and supplier power, entrant barriers, and substitutes, highlighting disruptive threats and strategic implications for pricing and profitability.

A concise Teradata Porter's Five Forces snapshot that highlights competitive threats and relief points—ideal for swift strategic decisions and boardroom use.

Customers Bargaining Power

Concentration of Large Enterprise Clients

Teradata serves large global corporations where roughly 20% of clients contribute about 70% of revenue, so a few accounts carry outsized weight.

Those high-value customers exert strong bargaining power, demanding custom features and discounts that compress margins.

By late 2025, enterprises increasingly used scale to extract better renewal terms, raising contract churn risk.

Losing a single Fortune 500 client can cut revenue and hurt market perception materially.

Availability of Cloud-Native Alternatives

The proliferation of cloud-native rivals like Snowflake (FY2024 revenue $3.4B) and Databricks (2024 ARR ~$3.0B) gives buyers more choice and lowers switching costs, raising customer bargaining power against Teradata.

By 2025 many enterprises run multi-cloud setups to avoid lock-in, so customers press for better pricing and features, forcing Teradata to prove superior ROI or risk churn.

Teradata must keep innovating—cloud native scaling and cost-per-query improvements—to stop migrations to these mature, scalable rivals.

Shift Toward Consumption-Based Pricing Models

High Complexity and Migration Costs

Customers have many choices, but migrating petabyte-scale, mission-critical Teradata warehouses incurs high technical debt and operational risk, which historically reduced buyer power.

By late 2025, automated migration tools and managed-services offerings cut estimated migration time by ~30–50% and lowered cost by ~20%, per industry vendor reports, so switching friction is falling.

Switching costs remain significant but are no longer an insurmountable moat for Teradata.

- High migration complexity, mission-critical data

- Technical debt and risk deter abrupt switches

- Late-2025 tools: ~30–50% faster, ~20% cheaper

- Switching costs high but weakening

Demand for Open Ecosystems and Interoperability

Enterprises now demand platforms that integrate with many third-party tools and open-source languages, cutting Teradata’s ability to lock customers into a proprietary stack.

By 2025 buyers prioritize flexibility and low friction; 68% of enterprises cite interoperability as a top procurement criterion, forcing Teradata to adopt industry standards and APIs.

This shift reduces Teradata’s bargaining power, as vendor choice and standards are set by buyer ecosystems rather than a single supplier.

- 68% of enterprises prioritize interoperability (2025)

- Open-source use up 12% YoY in analytics stacks (2024–25)

- Teradata must support common APIs, connectors, and SQL/Python/R

Top clients & cloud rivals amplify buyer power; consumption pricing fuels 15–20% volatility

Large accounts (~20% clients ≈70% revenue) wield strong price and feature leverage; cloud rivals (Snowflake $3.4B FY2024, Databricks ~ $3.0B ARR 2024) and multi-cloud setups raise buyer power; consumption pricing preferred by 62% of buyers (2025) increases bargaining and revenue volatility (~15–20%); migration tools cut time ~30–50% and cost ~20%, lowering switching friction.

| Metric | Value |

|---|---|

| Top-client revenue share | ~70% |

| Top-client percent of customers | ~20% |

| Snowflake revenue | $3.4B (FY2024) |

| Databricks ARR | ~$3.0B (2024) |

| Buyers preferring consumption | 62% (2025) |

| Revenue volatility from usage shift | ~15–20% |

| Migration time reduction | ~30–50% |

| Migration cost reduction | ~20% |

Preview the Actual Deliverable

Teradata Porter's Five Forces Analysis

This preview shows the exact Teradata Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

The document displayed here is the same professionally written file included in the full version and will be available for instant download once you complete your purchase.

You're looking at the final deliverable: a complete, ready-to-use analysis of Teradata’s competitive forces, suitable for decision-making, reporting, or further research.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Teradata faces intense rivalry from cloud-native analytics firms and major cloud providers, with moderate supplier leverage and growing buyer power as enterprises demand flexible, consumption-based pricing.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Teradata’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Public Cloud Infrastructure Providers

Teradata depends on AWS, Microsoft Azure, and Google Cloud Platform to host Vantage, giving these three providers strong bargaining power over infrastructure pricing and SLAs.

By late 2025, the top three control roughly 65–70% of global cloud IaaS/PaaS, limiting Teradata’s ability to negotiate without risking feature or performance parity.

This reliance raises cost and strategic risk: a 10–20% cloud price hike or increased push of native analytics by providers could materially erode Teradata gross margins and customer retention.

Specialized Semiconductor and Hardware Manufacturers

Suppliers of advanced GPUs and CPUs like NVIDIA and Intel exert strong bargaining power because Teradata’s on-prem and hybrid appliances still rely on specialized silicon for HPC; NVIDIA held ~80% GPU market share for data-center AI in 2024 and price premiums persisted into 2025. Tight allocation and multi-quarter lead times for AI-optimized chips mean higher component costs and delivery risk. Teradata must lock multi-year contracts and diversify suppliers to protect performance and timelines.

Scarcity of Specialized Technical Talent

The supply of software engineers and data scientists expert in massive parallel processing and cloud architecture is tight in 2025; US STEM job openings hit 1.4M in 2024, and top talent commands 20–40% higher pay, boosting supplier power over Teradata.

Teradata competes with FAANG and well-funded startups for this scarce pool; maintaining proprietary kernel expertise is a critical bottleneck, so 2025 hiring and retention spend rose ~15% year-over-year to protect the innovation pipeline.

Third-Party Software and Integration Partners

Teradata relies on many third-party software components and proprietary connectors to stay interoperable; in 2025 about 18–25% of enterprise deployments cite third-party adapters as critical integration points.

Vendors of specialized software or connectors can raise fees or change standards, squeezing Teradata’s gross margins — vendor-driven licensing hikes of 5–12% yearly would cut platform margins materially.

Customer demand for plug-and-play in 2025 forces Teradata to preserve partnerships and compatibility, increasing supplier leverage and the risk that external IP capture reduces Teradata’s share of analytics value.

- 18–25% of deployments rely on third-party connectors

- Potential vendor price hikes 5–12% annually

- Dependency risks margin compression and value capture by vendors

Data Center and Co-location Providers

For hybrid and private cloud customers, Teradata depends on third-party data centers that control power, cooling, and network links—core to its on-premises value.

High-density power and low-latency networking needs shrink provider choice in some regions, raising switching costs and deployment delays.

By end-2025, a ~15–25% rise in commercial electricity prices in key markets increased facility leverage during renewals and SLAs.

- Dependency on third-party facilities

- Geographic limits due to power/network specs

- Rising energy costs (15–25% by 2025) boost supplier leverage

Supplier squeeze: cloud, NVIDIA, talent drive costs up 15–25% for Teradata

Suppliers (cloud hyperscalers, NVIDIA/Intel, talent, connectors, data centers) hold high bargaining power for Teradata in 2025—top-3 cloud 65–70% share, NVIDIA ~80% DC GPU share, STEM job openings 1.4M, hiring cost +15% YoY, third-party connector reliance 18–25%, potential vendor fee hikes 5–12%, energy costs +15–25%.

| Supplier | Key metric (2025) |

|---|---|

| Top-3 cloud | 65–70% market share |

| NVIDIA (DC GPU) | ~80% share |

| STEM openings | 1.4M (2024) |

| Hiring cost | +15% YoY |

| Connector reliance | 18–25% deployments |

| Vendor fee risk | +5–12% annually |

| Energy costs | +15–25% by 2025 |

What is included in the product

Tailored Porter's Five Forces analysis for Teradata that uncovers competitive drivers, customer and supplier power, entrant barriers, and substitutes, highlighting disruptive threats and strategic implications for pricing and profitability.

A concise Teradata Porter's Five Forces snapshot that highlights competitive threats and relief points—ideal for swift strategic decisions and boardroom use.

Customers Bargaining Power

Concentration of Large Enterprise Clients

Teradata serves large global corporations where roughly 20% of clients contribute about 70% of revenue, so a few accounts carry outsized weight.

Those high-value customers exert strong bargaining power, demanding custom features and discounts that compress margins.

By late 2025, enterprises increasingly used scale to extract better renewal terms, raising contract churn risk.

Losing a single Fortune 500 client can cut revenue and hurt market perception materially.

Availability of Cloud-Native Alternatives

The proliferation of cloud-native rivals like Snowflake (FY2024 revenue $3.4B) and Databricks (2024 ARR ~$3.0B) gives buyers more choice and lowers switching costs, raising customer bargaining power against Teradata.

By 2025 many enterprises run multi-cloud setups to avoid lock-in, so customers press for better pricing and features, forcing Teradata to prove superior ROI or risk churn.

Teradata must keep innovating—cloud native scaling and cost-per-query improvements—to stop migrations to these mature, scalable rivals.

Shift Toward Consumption-Based Pricing Models

High Complexity and Migration Costs

Customers have many choices, but migrating petabyte-scale, mission-critical Teradata warehouses incurs high technical debt and operational risk, which historically reduced buyer power.

By late 2025, automated migration tools and managed-services offerings cut estimated migration time by ~30–50% and lowered cost by ~20%, per industry vendor reports, so switching friction is falling.

Switching costs remain significant but are no longer an insurmountable moat for Teradata.

- High migration complexity, mission-critical data

- Technical debt and risk deter abrupt switches

- Late-2025 tools: ~30–50% faster, ~20% cheaper

- Switching costs high but weakening

Demand for Open Ecosystems and Interoperability

Enterprises now demand platforms that integrate with many third-party tools and open-source languages, cutting Teradata’s ability to lock customers into a proprietary stack.

By 2025 buyers prioritize flexibility and low friction; 68% of enterprises cite interoperability as a top procurement criterion, forcing Teradata to adopt industry standards and APIs.

This shift reduces Teradata’s bargaining power, as vendor choice and standards are set by buyer ecosystems rather than a single supplier.

- 68% of enterprises prioritize interoperability (2025)

- Open-source use up 12% YoY in analytics stacks (2024–25)

- Teradata must support common APIs, connectors, and SQL/Python/R

Top clients & cloud rivals amplify buyer power; consumption pricing fuels 15–20% volatility

Large accounts (~20% clients ≈70% revenue) wield strong price and feature leverage; cloud rivals (Snowflake $3.4B FY2024, Databricks ~ $3.0B ARR 2024) and multi-cloud setups raise buyer power; consumption pricing preferred by 62% of buyers (2025) increases bargaining and revenue volatility (~15–20%); migration tools cut time ~30–50% and cost ~20%, lowering switching friction.

| Metric | Value |

|---|---|

| Top-client revenue share | ~70% |

| Top-client percent of customers | ~20% |

| Snowflake revenue | $3.4B (FY2024) |

| Databricks ARR | ~$3.0B (2024) |

| Buyers preferring consumption | 62% (2025) |

| Revenue volatility from usage shift | ~15–20% |

| Migration time reduction | ~30–50% |

| Migration cost reduction | ~20% |

Preview the Actual Deliverable

Teradata Porter's Five Forces Analysis

This preview shows the exact Teradata Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

The document displayed here is the same professionally written file included in the full version and will be available for instant download once you complete your purchase.

You're looking at the final deliverable: a complete, ready-to-use analysis of Teradata’s competitive forces, suitable for decision-making, reporting, or further research.