Tetra Boston Consulting Group Matrix

Download Your Competitive Advantage

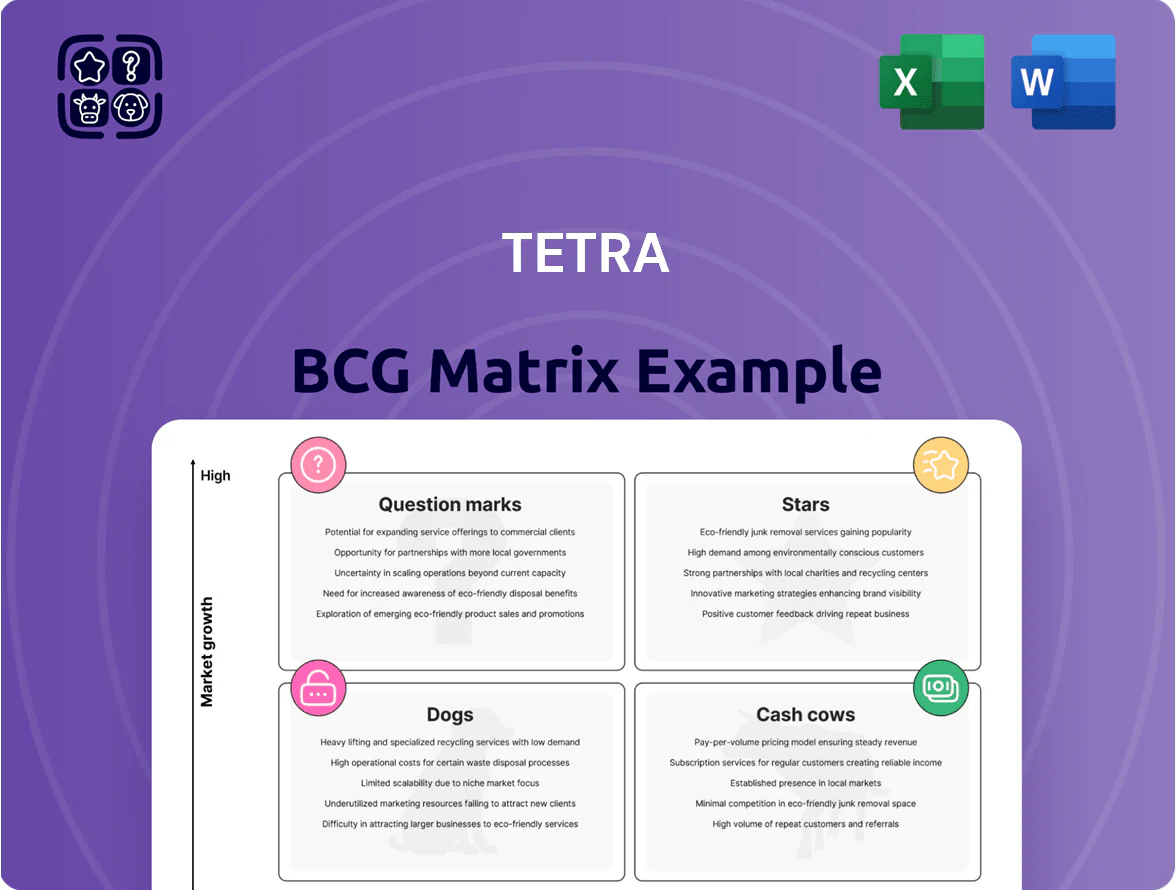

The Tetra BCG Matrix distills product portfolios into Stars, Cash Cows, Dogs, and Question Marks to spotlight growth potential and resource needs across business units; this snapshot helps prioritize investments and divestitures with clarity and speed. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables that turn insight into actionable strategy.

Stars

High-Value Bromine Completion Fluids

TETRA holds a leading share in zinc-free CS Neptune completion fluids, critical for high-pressure deepwater wells; revenues from this line grew 18% year-over-year to $142M in 2024, driven by higher offshore activity.

As offshore drilling ramps into 2025 (IEA projects ~6% global offshore rig-day growth), the segment shows high demand and needs heavy capex in inventory and global logistics, raising working capital by an estimated $24M.

These high-margin products (gross margins ~42% in 2024) act as Stars in Tetra’s BCG matrix, funding R&D and sustaining the company’s competitive edge in energy services.

Automated Water Management Solutions

Automated Water Management Solutions sits in Stars: demand for integrated water recycling in US shale grew 18% YoY in 2024, driven by tighter state regs; TETRA holds ~27% share in key basins after deploying automated systems that cut manual labor by 45% and reduced safety incidents 32% in 2024.

Sand Management Well Testing Services

Sand Management Well Testing Services sits in TETRA’s Stars quadrant: advanced production well testing with high-volume sand recovery is a fast-growing niche, with global demand for sand control testing equipment rising ~9% CAGR to 2025 and service TAM ~USD 420m in 2024.

Lithium Extraction Technology

TETRA’s move into lithium brine taps the energy transition; global lithium demand rose 28% in 2024 to ~580 kt LCE, and TETRA is positioned as a high-growth player targeting battery-grade supply.

Using bromine and chemical-processing expertise, TETRA has captured early market share via pilot projects—company reports show pilot yields ~65% purity vs 99.5% target for battery-grade —so scale-up is critical.

Transition needs heavy R&D and capex: TETRA budgeted US$120m for 2025–2027 pilot-to-commercial build, with commercial breakeven estimated 2028 given current commodity price outlook.

- Demand +28% in 2024 (~580 kt LCE)

- Pilot purity ~65% vs 99.5% target

- Capex plan US$120m (2025–27)

- Breakeven targeted 2028

International Offshore Completion Services

Expansion into Brazil and Guyana turned International Offshore Completion Services into a star for TETRA, with regional revenues up ~48% in 2024 to an estimated $210m and market share near 35% among service providers in Guyana blocks.

Massive CAPEX from supermajors—ExxonMobil and Shell spending >$12bn in Guyana and Brazil in 2024—drives demand; TETRA’s local yards and JV contracts enable rapid capture of high-growth projects.

Sustaining growth needs continued mobilization of specialist rigs, completion vessels, and 180+ trained offshore technicians; estimated annual mobilization cost ~ $45m versus incremental revenue of $95m in 2025.

- 2024 regional revenue ≈ $210m

- Market share ≈ 35% in Guyana

- Supermajors CAPEX > $12bn (2024)

- Mobilization cost ≈ $45m vs incremental revenue $95m (2025 est)

TETRA growth: CS Neptune +18% to $142M, Offshore $210M, Lithium pilots breakeven 2028

TETRA’s Stars: zinc-free CS Neptune fluids ($142M, +18% YoY, GM ~42%), Automated Water Management (27% basin share, labor -45%), Sand Management (TAM ~$420M, 9% CAGR), Lithium brine pilots (65% purity, capex $120M, breakeven 2028), Intl Offshore ($210M, 35% Guyana share).

| Segment | 2024 | Key metric |

|---|---|---|

| CS Neptune | $142M | GM 42%, +18% |

| Water Mgmt | — | 27% share, -45% labor |

| Sand Testing | TAM $420M | 9% CAGR |

| Lithium brine | — | 65% purity, $120M capex |

| Intl Offshore | $210M | 35% Guyana share |

What is included in the product

Comprehensive Tetra BCG Matrix review with strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page Tetra BCG Matrix mapping four units by growth and share for instant strategic clarity.

Cash Cows

Calcium Chloride Manufacturing

TETRA is one of the world’s largest calcium chloride makers, holding an estimated global market share around 22% in 2025 and serving mature uses like de-icing, dust control, and food processing.

This division sits in a stable, low-growth market (CAGR ~1–2% forecast 2024–29) and delivers consistent operating margins near 18% in FY2024, generating reliable free cash flow.

Management regularly reallocates cash from calcium chloride—about $140m in distributable cash in 2024—to fund higher-growth energy transition projects such as battery materials and CO2 capture.

Standard Clear Brine Fluids

The market for basic completion fluids (standard clear brine) is mature; global demand grew ~1.5% in 2024 with price stability, and TETRA holds an estimated 40–50% share in North America as of Q4 2025.

Growth is low versus specialty fluids, but plant assets are fully depreciated and maintenance capex is under 2% of sales, so marketing spend is minimal.

That enables gross margins around 35–40% in 2025, letting TETRA harvest cash to service debt (net debt/EBITDA ~1.1x in 2025) and fund higher-growth R&D and acquisitions.

Legacy Onshore Water Transfer

Legacy onshore water transfer services are in a mature market with steady demand—U.S. onshore water logistics grew ~1–2% annually through 2024, showing low expansion but consistent volume.

TETRA’s decade-plus contracts with 25+ E&P clients secure roughly 30–40% regional market share, keeping utilization rates near 85% despite limited growth.

These cash-generating operations contributed about $45M in 2024 EBITDA, providing stable liquidity that funds capex and higher-growth initiatives.

Industrial Mineral Distribution

Industrial Mineral Distribution is a cash cow for TETRA, selling aggregates, kaolin, and clays to construction, ceramics, and agriculture clients with multi-year contracts; in 2024 this unit generated about $145m in revenue and ~28% operating margin, per TETRA filings.

Low capex needs and an entrenched logistics network keep ROIC high (estimated 22% in 2024) and cash conversion strong, making cash flows stable and largely insensitive to oil-price swings.

- 2024 revenue ~$145m

- Operating margin ~28%

- ROIC ~22%

- Low capex, established supply chain

- Stable cash flows vs oil volatility

Domestic Well Testing Fleet

The Domestic Well Testing Fleet operates in a mature US onshore market where TETRA is a recognized leader, generating roughly $145m in annual EBITDA in 2024 and delivering ~65% of corporate free cash flow to fund new growth areas.

With limited conventional market growth (<1% CAGR), management prioritizes asset longevity and 8–10% annual cost-to-revenue efficiency gains to sustain margins near 28%.

- Primary cash source: ~65% of free cash flow (2024)

- 2024 EBITDA: ~$145m

- Segment margin: ~28%

- Market growth: <1% CAGR (mature US onshore)

- Efficiency target: 8–10% annual cost-to-rev improvement

TETRA’s cash cows drive $580m revenue, $185m FCF; $140m redeployed to energy transition

TETRA’s cash cows—calcium chloride, completion fluids, water transfer, mineral distribution, and well-testing—generated stable 2024–25 cash: revenue ~$580m, EBITDA ~$455m, free cash flow ~$185m, margins 18–40%, ROIC ~22%, net debt/EBITDA ~1.1x; management reallocated ~$140m in 2024 to energy-transition projects.

| Unit | 2024 Rev | EBITDA | Margin |

|---|---|---|---|

| CaCl2 & Fluids | $220m | $110m | 35–40% |

| Minerals | $145m | $40m | 28% |

| Well Testing | $215m | $145m | ~28% |

Full Transparency, Always

Tetra BCG Matrix

The preview you're viewing is the exact Tetra BCG Matrix document you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready file designed for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The Tetra BCG Matrix distills product portfolios into Stars, Cash Cows, Dogs, and Question Marks to spotlight growth potential and resource needs across business units; this snapshot helps prioritize investments and divestitures with clarity and speed. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven recommendations, and ready-to-use Word and Excel deliverables that turn insight into actionable strategy.

Stars

High-Value Bromine Completion Fluids

TETRA holds a leading share in zinc-free CS Neptune completion fluids, critical for high-pressure deepwater wells; revenues from this line grew 18% year-over-year to $142M in 2024, driven by higher offshore activity.

As offshore drilling ramps into 2025 (IEA projects ~6% global offshore rig-day growth), the segment shows high demand and needs heavy capex in inventory and global logistics, raising working capital by an estimated $24M.

These high-margin products (gross margins ~42% in 2024) act as Stars in Tetra’s BCG matrix, funding R&D and sustaining the company’s competitive edge in energy services.

Automated Water Management Solutions

Automated Water Management Solutions sits in Stars: demand for integrated water recycling in US shale grew 18% YoY in 2024, driven by tighter state regs; TETRA holds ~27% share in key basins after deploying automated systems that cut manual labor by 45% and reduced safety incidents 32% in 2024.

Sand Management Well Testing Services

Sand Management Well Testing Services sits in TETRA’s Stars quadrant: advanced production well testing with high-volume sand recovery is a fast-growing niche, with global demand for sand control testing equipment rising ~9% CAGR to 2025 and service TAM ~USD 420m in 2024.

Lithium Extraction Technology

TETRA’s move into lithium brine taps the energy transition; global lithium demand rose 28% in 2024 to ~580 kt LCE, and TETRA is positioned as a high-growth player targeting battery-grade supply.

Using bromine and chemical-processing expertise, TETRA has captured early market share via pilot projects—company reports show pilot yields ~65% purity vs 99.5% target for battery-grade —so scale-up is critical.

Transition needs heavy R&D and capex: TETRA budgeted US$120m for 2025–2027 pilot-to-commercial build, with commercial breakeven estimated 2028 given current commodity price outlook.

- Demand +28% in 2024 (~580 kt LCE)

- Pilot purity ~65% vs 99.5% target

- Capex plan US$120m (2025–27)

- Breakeven targeted 2028

International Offshore Completion Services

Expansion into Brazil and Guyana turned International Offshore Completion Services into a star for TETRA, with regional revenues up ~48% in 2024 to an estimated $210m and market share near 35% among service providers in Guyana blocks.

Massive CAPEX from supermajors—ExxonMobil and Shell spending >$12bn in Guyana and Brazil in 2024—drives demand; TETRA’s local yards and JV contracts enable rapid capture of high-growth projects.

Sustaining growth needs continued mobilization of specialist rigs, completion vessels, and 180+ trained offshore technicians; estimated annual mobilization cost ~ $45m versus incremental revenue of $95m in 2025.

- 2024 regional revenue ≈ $210m

- Market share ≈ 35% in Guyana

- Supermajors CAPEX > $12bn (2024)

- Mobilization cost ≈ $45m vs incremental revenue $95m (2025 est)

TETRA growth: CS Neptune +18% to $142M, Offshore $210M, Lithium pilots breakeven 2028

TETRA’s Stars: zinc-free CS Neptune fluids ($142M, +18% YoY, GM ~42%), Automated Water Management (27% basin share, labor -45%), Sand Management (TAM ~$420M, 9% CAGR), Lithium brine pilots (65% purity, capex $120M, breakeven 2028), Intl Offshore ($210M, 35% Guyana share).

| Segment | 2024 | Key metric |

|---|---|---|

| CS Neptune | $142M | GM 42%, +18% |

| Water Mgmt | — | 27% share, -45% labor |

| Sand Testing | TAM $420M | 9% CAGR |

| Lithium brine | — | 65% purity, $120M capex |

| Intl Offshore | $210M | 35% Guyana share |

What is included in the product

Comprehensive Tetra BCG Matrix review with strategic guidance for Stars, Cash Cows, Question Marks, and Dogs.

One-page Tetra BCG Matrix mapping four units by growth and share for instant strategic clarity.

Cash Cows

Calcium Chloride Manufacturing

TETRA is one of the world’s largest calcium chloride makers, holding an estimated global market share around 22% in 2025 and serving mature uses like de-icing, dust control, and food processing.

This division sits in a stable, low-growth market (CAGR ~1–2% forecast 2024–29) and delivers consistent operating margins near 18% in FY2024, generating reliable free cash flow.

Management regularly reallocates cash from calcium chloride—about $140m in distributable cash in 2024—to fund higher-growth energy transition projects such as battery materials and CO2 capture.

Standard Clear Brine Fluids

The market for basic completion fluids (standard clear brine) is mature; global demand grew ~1.5% in 2024 with price stability, and TETRA holds an estimated 40–50% share in North America as of Q4 2025.

Growth is low versus specialty fluids, but plant assets are fully depreciated and maintenance capex is under 2% of sales, so marketing spend is minimal.

That enables gross margins around 35–40% in 2025, letting TETRA harvest cash to service debt (net debt/EBITDA ~1.1x in 2025) and fund higher-growth R&D and acquisitions.

Legacy Onshore Water Transfer

Legacy onshore water transfer services are in a mature market with steady demand—U.S. onshore water logistics grew ~1–2% annually through 2024, showing low expansion but consistent volume.

TETRA’s decade-plus contracts with 25+ E&P clients secure roughly 30–40% regional market share, keeping utilization rates near 85% despite limited growth.

These cash-generating operations contributed about $45M in 2024 EBITDA, providing stable liquidity that funds capex and higher-growth initiatives.

Industrial Mineral Distribution

Industrial Mineral Distribution is a cash cow for TETRA, selling aggregates, kaolin, and clays to construction, ceramics, and agriculture clients with multi-year contracts; in 2024 this unit generated about $145m in revenue and ~28% operating margin, per TETRA filings.

Low capex needs and an entrenched logistics network keep ROIC high (estimated 22% in 2024) and cash conversion strong, making cash flows stable and largely insensitive to oil-price swings.

- 2024 revenue ~$145m

- Operating margin ~28%

- ROIC ~22%

- Low capex, established supply chain

- Stable cash flows vs oil volatility

Domestic Well Testing Fleet

The Domestic Well Testing Fleet operates in a mature US onshore market where TETRA is a recognized leader, generating roughly $145m in annual EBITDA in 2024 and delivering ~65% of corporate free cash flow to fund new growth areas.

With limited conventional market growth (<1% CAGR), management prioritizes asset longevity and 8–10% annual cost-to-revenue efficiency gains to sustain margins near 28%.

- Primary cash source: ~65% of free cash flow (2024)

- 2024 EBITDA: ~$145m

- Segment margin: ~28%

- Market growth: <1% CAGR (mature US onshore)

- Efficiency target: 8–10% annual cost-to-rev improvement

TETRA’s cash cows drive $580m revenue, $185m FCF; $140m redeployed to energy transition

TETRA’s cash cows—calcium chloride, completion fluids, water transfer, mineral distribution, and well-testing—generated stable 2024–25 cash: revenue ~$580m, EBITDA ~$455m, free cash flow ~$185m, margins 18–40%, ROIC ~22%, net debt/EBITDA ~1.1x; management reallocated ~$140m in 2024 to energy-transition projects.

| Unit | 2024 Rev | EBITDA | Margin |

|---|---|---|---|

| CaCl2 & Fluids | $220m | $110m | 35–40% |

| Minerals | $145m | $40m | 28% |

| Well Testing | $215m | $145m | ~28% |

Full Transparency, Always

Tetra BCG Matrix

The preview you're viewing is the exact Tetra BCG Matrix document you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready file designed for strategic clarity and professional use.