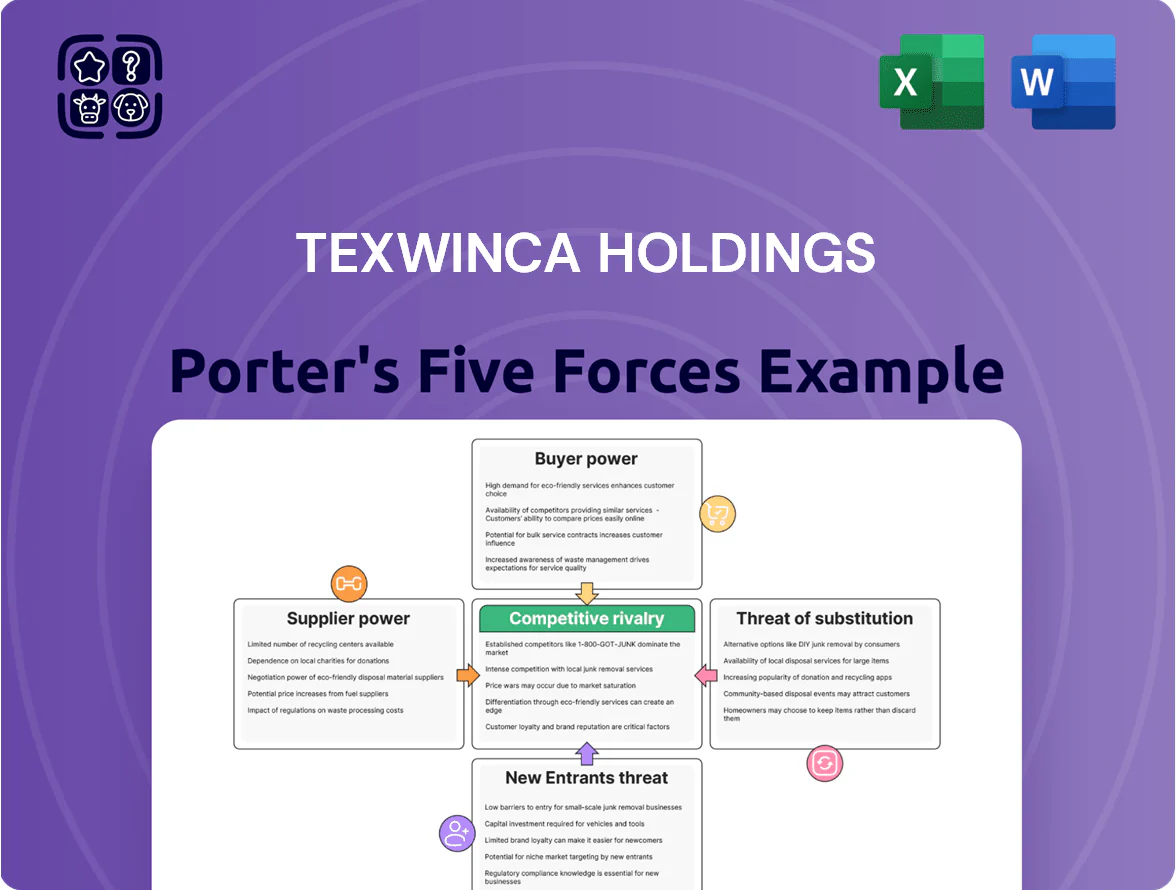

Texwinca Holdings Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Texwinca Holdings faces moderate supplier power and high buyer sensitivity amid intense retail competition and low switching costs, while new entrants pose a manageable threat thanks to scale economies; substitutes and rivalry pad down margins. This snapshot highlights key pressure points and strategic levers for value capture. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategies tailored to Texwinca Holdings.

Suppliers Bargaining Power

Raw material price volatility

Raw cotton and yarns, Texwinca’s main inputs, face global commodity swings; cotton futures rose ~18% in 2024-25 and spot prices hit $1.05/lb in Nov 2025, making input cost unpredictable.

Climate shocks in India and Brazil cut 2024 cotton output by ~6%, and geopolitical risks in Central Asia keep supply fragile, so Texwinca keeps 3–6 months’ strategic reserves and hedges ~30% of volumes.

Premium organic cotton suppliers command price premiums of 20–40% and growing ESG demand gives them bargaining leverage, pressuring margins unless Texwinca secures long-term contracts.

Concentration of specialized chemical providers

The dyeing and finishing stages demand specialized chemicals that meet strict EU REACH and US TSCA standards; only about 8–12 global suppliers are certified at the scale Texwinca needs, creating supplier concentration.

That concentration lets suppliers keep firm pricing—chemical input costs rose ~14% in 2023–24 for textile-grade dyes—and margins pressure Texwinca as tighter environmental rules raise compliance costs for producers.

Energy costs and utility dependence

Texwinca's textile plants are energy-heavy, so dependence on China and Southeast Asia grids and fuel suppliers makes utilities a key cost driver; in 2024 regional industrial electricity rates rose up to 12% in parts of Guangdong and 8% in Vietnam, directly squeezing margins.

With energy >15% of COGS in spinning and dyeing, short-term switching is impractical, so utility firms hold structural bargaining power that can lift unit costs and reduce operating margin by several percentage points.

Labor supply and wage inflation

The manufacturing sector faces rising minimum wages—India raised national floor wages ~8% in 2024 and key states hiked textile minimums 5–12%—while skilled garment operators declined ~7% in Surat and Tirupur since 2021, boosting labor suppliers’ bargaining power.

Texwinca must weigh higher pay against automation: a $1.5–2.5m line retrofit can cut direct labor by 30–40%, preserving margins amid wage inflation.

- Wage hikes 5–12% (2024 state moves)

- Skilled labor pool down ~7% in hubs

- Labor cost pressure raised supplier power

- Automation ROI: 18–36 months, 30–40% labor cut

Technological equipment manufacturers

The company depends on advanced knitting and dyeing machines from a handful of specialist global firms, giving suppliers leverage via proprietary tech and multi-year maintenance deals; switching costs can exceed 20–30% of capex and cause 6–12 months of downtime. Upgrades to hit 2025 sustainability targets (eg, water-use cuts of 40% and energy efficiency gains ~15%) lock Texwinca into recurrent capital spending and service contracts.

- Supplier concentration: few global OEMs

- Switching cost: 20–30% of capex, 6–12 months downtime

- Maintenance contracts: multi-year, recurring revenue for suppliers

- Sustainability upgrades: drive repeated capex (water -40%, energy +15% efficiency)

Supplier squeeze: cotton surge, energy & wage pressure—automation offsets margins

Suppliers hold moderate–high power: concentrated chemical and OEM markets, energy and labor cost swings, and premium cotton premiums (20–40%) and cotton futures (+18% in 2024–25) squeeze margins; Texwinca hedges ~30% volumes, keeps 3–6 months inventory, and automation ROI is 18–36 months to offset 5–12% wage rises.

| Factor | Key data |

|---|---|

| Cotton price move | +18% (2024–25); $1.05/lb Nov 2025 |

| Organic premium | +20–40% |

| Chemical suppliers | 8–12 global |

| Energy share COGS | >15%; rates +8–12% (2024) |

| Wage pressure | 5–12% hikes (2024) |

| Hedging & inventory | ~30% hedged; 3–6 months stock |

| Automation ROI | $1.5–2.5m; 18–36 months; −30–40% labor |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Texwinca Holdings, evaluating supplier and buyer power, threat of substitutes and entrants, and competitive rivalry to highlight pricing, profitability and strategic defenses.

Compact Porter's Five Forces snapshot for Texwinca Holdings—quickly identify competitive threats and bargaining pressures to inform strategic moves.

Customers Bargaining Power

Concentration of global apparel brands

A large share of Texwinca Holdings’ FY2024 fabric and garment revenue—about 60% per company disclosures—comes from a handful of global apparel brands, giving those buyers strong bargaining power. These clients enforce strict quality standards and tight lead times, lowering Texwinca’s pricing flexibility and margin control. Losing one major account could cut annual revenue by double-digit percentages, as single-brand orders have represented 10–25% of sales historically.

Low switching costs for brand owners

Consumer price sensitivity in retail

Through Baleno and other retail channels, Texwinca faces high mass-market price sensitivity; a 2025 Euromonitor survey showed 62% of Asia-Pacific shoppers prioritize price over brand, pressuring margins.

Easy access to price comparisons and low-cost alternatives—online fast-fashion grew 11% YoY in 2025—limits Texwinca’s ability to pass higher input costs to consumers.

Rising cotton and labor costs added ~6–8% to garment COGS in 2025, so passing this on risks double-digit sales volume declines in price-sensitive segments.

Demand for transparent and ethical sourcing

Modern buyers demand clear traceability of environmental and social impact in apparel, giving customers leverage to require certifications and third-party audits that can cost Texwinca $200k–$1M+ per factory upgrade (industry ranges 2024–25).

Major brands may terminate contracts immediately for violations; 2023–24 data show 12% of supplier exits in Bangladesh were for compliance lapses, and consumer boycotts can cut retail sales by 5–15% within a quarter.

Meeting these standards raises operating costs but protects revenue and brand access; failing to invest risks lost contracts and reputational damage.

- Customers demand audits/certs; upgrade costs $200k–$1M+ per site

- 12% supplier exits (2023–24) tied to compliance

- Boycotts can reduce sales 5–15% in a quarter

- Non-compliance risks immediate contract termination

E-commerce and direct-to-consumer competition

The rise of digital platforms gives consumers far more choice beyond brick-and-mortar, forcing Texwinca Holdings’ retail arm to compete on digital experience and delivery speed as well as product quality; global e-commerce sales hit US$5.7 trillion in 2023 and grew ~10% in 2024, raising online brand-switching.

Easy discovery of alternatives—search, marketplaces, social commerce—boosts customer bargaining power; Texwinca faces price and service pressure as >60% of apparel shoppers in 2024 tried new online brands.

- Global e-commerce: US$5.7T (2023), +~10% in 2024

- >60% of apparel buyers tried new online brands (2024)

- Key levers: UX, delivery speed, returns policy

Buyer leverage squeezes suppliers: high account risk, costly audits, price-driven APAC demand

Buyers hold high leverage: ~60% FY2024 revenue from few global brands, single-account risk 10–25% of sales, and brands keep 3+ suppliers (68% per McKinsey 2024), forcing price, lead-time, and compliance pressure; audits cost $200k–$1M+/factory (2024–25), non-compliance drove 12% supplier exits (2023–24), and 62% APAC shoppers prioritize price (2025).

| Metric | Value |

|---|---|

| Revenue from top buyers | ~60% (FY2024) |

| Single-account share | 10–25% |

| Brands with 3+ suppliers | 68% (McKinsey 2024) |

| Audit/upgrade cost | $200k–$1M+ (2024–25) |

| Supplier exits due to compliance | 12% (2023–24) |

| APAC price-sensitive shoppers | 62% (Euromonitor 2025) |

Preview the Actual Deliverable

Texwinca Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Texwinca Holdings you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Texwinca Holdings faces moderate supplier power and high buyer sensitivity amid intense retail competition and low switching costs, while new entrants pose a manageable threat thanks to scale economies; substitutes and rivalry pad down margins. This snapshot highlights key pressure points and strategic levers for value capture. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategies tailored to Texwinca Holdings.

Suppliers Bargaining Power

Raw material price volatility

Raw cotton and yarns, Texwinca’s main inputs, face global commodity swings; cotton futures rose ~18% in 2024-25 and spot prices hit $1.05/lb in Nov 2025, making input cost unpredictable.

Climate shocks in India and Brazil cut 2024 cotton output by ~6%, and geopolitical risks in Central Asia keep supply fragile, so Texwinca keeps 3–6 months’ strategic reserves and hedges ~30% of volumes.

Premium organic cotton suppliers command price premiums of 20–40% and growing ESG demand gives them bargaining leverage, pressuring margins unless Texwinca secures long-term contracts.

Concentration of specialized chemical providers

The dyeing and finishing stages demand specialized chemicals that meet strict EU REACH and US TSCA standards; only about 8–12 global suppliers are certified at the scale Texwinca needs, creating supplier concentration.

That concentration lets suppliers keep firm pricing—chemical input costs rose ~14% in 2023–24 for textile-grade dyes—and margins pressure Texwinca as tighter environmental rules raise compliance costs for producers.

Energy costs and utility dependence

Texwinca's textile plants are energy-heavy, so dependence on China and Southeast Asia grids and fuel suppliers makes utilities a key cost driver; in 2024 regional industrial electricity rates rose up to 12% in parts of Guangdong and 8% in Vietnam, directly squeezing margins.

With energy >15% of COGS in spinning and dyeing, short-term switching is impractical, so utility firms hold structural bargaining power that can lift unit costs and reduce operating margin by several percentage points.

Labor supply and wage inflation

The manufacturing sector faces rising minimum wages—India raised national floor wages ~8% in 2024 and key states hiked textile minimums 5–12%—while skilled garment operators declined ~7% in Surat and Tirupur since 2021, boosting labor suppliers’ bargaining power.

Texwinca must weigh higher pay against automation: a $1.5–2.5m line retrofit can cut direct labor by 30–40%, preserving margins amid wage inflation.

- Wage hikes 5–12% (2024 state moves)

- Skilled labor pool down ~7% in hubs

- Labor cost pressure raised supplier power

- Automation ROI: 18–36 months, 30–40% labor cut

Technological equipment manufacturers

The company depends on advanced knitting and dyeing machines from a handful of specialist global firms, giving suppliers leverage via proprietary tech and multi-year maintenance deals; switching costs can exceed 20–30% of capex and cause 6–12 months of downtime. Upgrades to hit 2025 sustainability targets (eg, water-use cuts of 40% and energy efficiency gains ~15%) lock Texwinca into recurrent capital spending and service contracts.

- Supplier concentration: few global OEMs

- Switching cost: 20–30% of capex, 6–12 months downtime

- Maintenance contracts: multi-year, recurring revenue for suppliers

- Sustainability upgrades: drive repeated capex (water -40%, energy +15% efficiency)

Supplier squeeze: cotton surge, energy & wage pressure—automation offsets margins

Suppliers hold moderate–high power: concentrated chemical and OEM markets, energy and labor cost swings, and premium cotton premiums (20–40%) and cotton futures (+18% in 2024–25) squeeze margins; Texwinca hedges ~30% volumes, keeps 3–6 months inventory, and automation ROI is 18–36 months to offset 5–12% wage rises.

| Factor | Key data |

|---|---|

| Cotton price move | +18% (2024–25); $1.05/lb Nov 2025 |

| Organic premium | +20–40% |

| Chemical suppliers | 8–12 global |

| Energy share COGS | >15%; rates +8–12% (2024) |

| Wage pressure | 5–12% hikes (2024) |

| Hedging & inventory | ~30% hedged; 3–6 months stock |

| Automation ROI | $1.5–2.5m; 18–36 months; −30–40% labor |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Texwinca Holdings, evaluating supplier and buyer power, threat of substitutes and entrants, and competitive rivalry to highlight pricing, profitability and strategic defenses.

Compact Porter's Five Forces snapshot for Texwinca Holdings—quickly identify competitive threats and bargaining pressures to inform strategic moves.

Customers Bargaining Power

Concentration of global apparel brands

A large share of Texwinca Holdings’ FY2024 fabric and garment revenue—about 60% per company disclosures—comes from a handful of global apparel brands, giving those buyers strong bargaining power. These clients enforce strict quality standards and tight lead times, lowering Texwinca’s pricing flexibility and margin control. Losing one major account could cut annual revenue by double-digit percentages, as single-brand orders have represented 10–25% of sales historically.

Low switching costs for brand owners

Consumer price sensitivity in retail

Through Baleno and other retail channels, Texwinca faces high mass-market price sensitivity; a 2025 Euromonitor survey showed 62% of Asia-Pacific shoppers prioritize price over brand, pressuring margins.

Easy access to price comparisons and low-cost alternatives—online fast-fashion grew 11% YoY in 2025—limits Texwinca’s ability to pass higher input costs to consumers.

Rising cotton and labor costs added ~6–8% to garment COGS in 2025, so passing this on risks double-digit sales volume declines in price-sensitive segments.

Demand for transparent and ethical sourcing

Modern buyers demand clear traceability of environmental and social impact in apparel, giving customers leverage to require certifications and third-party audits that can cost Texwinca $200k–$1M+ per factory upgrade (industry ranges 2024–25).

Major brands may terminate contracts immediately for violations; 2023–24 data show 12% of supplier exits in Bangladesh were for compliance lapses, and consumer boycotts can cut retail sales by 5–15% within a quarter.

Meeting these standards raises operating costs but protects revenue and brand access; failing to invest risks lost contracts and reputational damage.

- Customers demand audits/certs; upgrade costs $200k–$1M+ per site

- 12% supplier exits (2023–24) tied to compliance

- Boycotts can reduce sales 5–15% in a quarter

- Non-compliance risks immediate contract termination

E-commerce and direct-to-consumer competition

The rise of digital platforms gives consumers far more choice beyond brick-and-mortar, forcing Texwinca Holdings’ retail arm to compete on digital experience and delivery speed as well as product quality; global e-commerce sales hit US$5.7 trillion in 2023 and grew ~10% in 2024, raising online brand-switching.

Easy discovery of alternatives—search, marketplaces, social commerce—boosts customer bargaining power; Texwinca faces price and service pressure as >60% of apparel shoppers in 2024 tried new online brands.

- Global e-commerce: US$5.7T (2023), +~10% in 2024

- >60% of apparel buyers tried new online brands (2024)

- Key levers: UX, delivery speed, returns policy

Buyer leverage squeezes suppliers: high account risk, costly audits, price-driven APAC demand

Buyers hold high leverage: ~60% FY2024 revenue from few global brands, single-account risk 10–25% of sales, and brands keep 3+ suppliers (68% per McKinsey 2024), forcing price, lead-time, and compliance pressure; audits cost $200k–$1M+/factory (2024–25), non-compliance drove 12% supplier exits (2023–24), and 62% APAC shoppers prioritize price (2025).

| Metric | Value |

|---|---|

| Revenue from top buyers | ~60% (FY2024) |

| Single-account share | 10–25% |

| Brands with 3+ suppliers | 68% (McKinsey 2024) |

| Audit/upgrade cost | $200k–$1M+ (2024–25) |

| Supplier exits due to compliance | 12% (2023–24) |

| APAC price-sensitive shoppers | 62% (Euromonitor 2025) |

Preview the Actual Deliverable

Texwinca Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Texwinca Holdings you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to download.