TGS Porter's Five Forces Analysis

Don't Miss the Bigger Picture

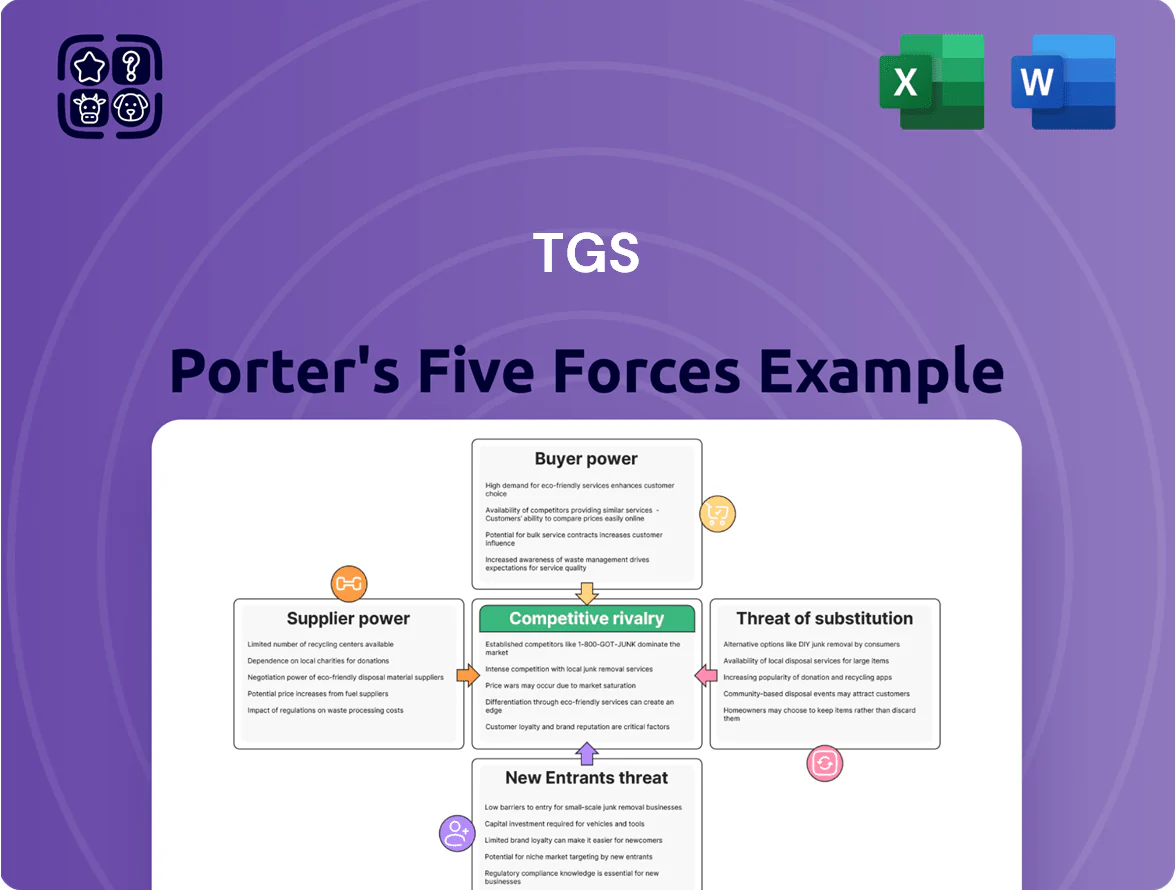

TGS faces a mix of powerful suppliers, evolving buyer demands, moderate substitution risk, and competitive rivalry that shapes its strategic choices—this snapshot highlights key pressure points and growth levers for the company.

Suppliers Bargaining Power

Concentration of High-End Vessel Owners

The market for specialized seismic vessels is concentrated among a few global owners (CGG, Polarcus, Magseis Fairfield, and others), giving them pricing power when demand spikes; spot charter rates surged ~40% in 2022–23, peaking near $60–80k/day for 3D vessels.

After merging with PGS in 2023, TGS added owned capacity but still charters third-party vessels for niche jobs; in 2024 about 25–35% of its vessel days were third-party, so charter-rate swings hit project EBITDA directly.

Dominance of Specialized Technology and Cloud Providers

TGS depends on high-performance computing and cloud services from a few giants to process petabyte‑scale seismic datasets; in 2024 hyperscalers controlled ~70% of global cloud IaaS market, concentrating supplier power.

Proprietary software stacks and data egress fees create high switching costs—moving 1 PB can cost >$100k and take weeks—so suppliers can push price and feature terms.

By late 2025, with AI/ML central to seismic interpretation, advanced compute remains a key cost driver, often 15–25% of project FCF in recent sector benchmarks.

Scarcity of Specialized Geophysical Equipment

Manufacture of seismic streamers, sensors, and ocean-bottom nodes is concentrated among a few engineered suppliers, giving them strong leverage over TGS; in 2024 about 70–80% of ocean-bottom node capacity came from three firms. Supply-chain disruptions can delay multi-client surveys by months and raise capex—TGS capex tied to equipment procurement was roughly $85–95m annually in 2023–2024—leaving few alternative sources if a primary maker stalls.

Highly Skilled Geoscientific Labor Market

The pool of experienced geophysicists and data scientists for advanced subsurface interpretation is small and in high demand, driving supplier power against TGS.

Competition from oil & gas and renewables raised industry median data scientist pay ~18% from 2019–2024; TGS needs top-market pay and cloud/ML tool investment to avoid losing talent and data-quality edge.

- Small talent pool

- Cross-sector competition

- Wage pressure ≈+18% (2019–2024)

- Must pay competitively and invest in tools

Regulatory and National Data Access Authorities

Governments and national oil companies act as sovereign suppliers, controlling access to offshore blocks and often taking 30–70% of upstream project revenue through licensing, royalties, and state participation (2024–25 averages in Africa and Latin America).

They impose strict data-sharing terms and local content rules that raise upfront costs; new 2025 environmental and maritime rules could add 5–12% to compliance costs and delay surveys by 3–9 months.

- State take: 30–70% revenue

- Local content: hiring/CapEx premium +10–25%

- 2025 regs: +5–12% compliance cost

- Survey delays: 3–9 months

Concentrated suppliers, rising costs & state take squeeze TGS project margins

Supplier power is high: vessel owners and streamer/node makers are concentrated (top 3 hold ~70–80% capacity), hyperscalers control ~70% IaaS, and talent pool is tight (data‑scientist pay +18% 2019–24), so charter/cloud/equipment costs and wages materially squeeze TGS project EBITDA. Governments add state take (30–70%) and local content (+10–25%), raising compliance and delay risk.

| Metric | Value |

|---|---|

| Top-3 equipment share | 70–80% |

| Hyperscaler IaaS share (2024) | ~70% |

| Data-scientist pay change (2019–24) | +18% |

| State take (regions) | 30–70% |

| Local content premium | +10–25% |

What is included in the product

Concise Porter's Five Forces for TGS: evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends and market barriers shaping TGS’s pricing power and profitability—editable for reports or investor materials.

Concise Porter's Five Forces snapshot tailored for TGS—quickly spot competitive pressures and tactical levers to relieve margin squeeze or protect pricing power.

Customers Bargaining Power

Consolidation of Global Energy Supermajors

The customer base for seismic data is concentrating as global supermajors merge; since 2015, the top 10 oil & gas firms’ share of upstream CAPEX rose to ~42% in 2024, boosting their bargaining leverage. This consolidation lets buyers demand volume discounts and tighter licensing—TGS reported 2024 revenue of $678m, so a single major client shifting procurement could swing annual revenue by several percent. Fewer independents mean contract terms and renewals now drive material pricing pressure.

Budget Sensitivity to Energy Price Volatility

TGS customers’ capex tracks oil/gas prices; a 40% Brent drop in 2020 showed exploration budgets fall first, and by late 2025 E&P firms report >15% tighter capex and require payback horizons under 24 months, forcing TGS to offer flexible pricing, staged deliveries, and deferred payments to win contracts.

Adoption of Multi-Client Subscription Models

Customers increasingly prefer multi-client subscription libraries, shifting spend from proprietary surveys to shared-cost models; industry reports show multi-client revenue comprised about 42% of global marine seismic sales in 2024, boosting TGS recurring revenue but compressing per-project margins.

This collective buying lets clients push TGS on uniform data formats and tiered pricing; in recent tender rounds, buyers negotiated average price reductions of 12–18% for bundled legacy data sets.

Because TGS maintains a vast library—over 2.5 million km of 2D/3D seismic and public-domain compilations—clients often delay purchases, waiting 9–15 months for older surveys to be discounted, pressuring new acquisition financing and product launch timing.

Demand for Integrated Energy Transition Data

As oil majors shift to broad energy providers, demand for integrated data spanning offshore wind, carbon capture and hydrocarbons rose; BP, Equinor and Shell increased renewables capex to about $45B in 2024, pushing cross-domain data needs.

Customers now pit providers on breadth and depth, so TGS must expand wind and CCS datasets or lose contracts to niche renewable data firms growing ~12% CAGR; failure risks revenue erosion in existing seismic services.

- TGS must add wind/CCS layers

- Customers favor cross-functional vendors

- Renewables data market growing ~12% CAGR

Internal Data Processing Capabilities of Clients

Top oil majors’ buying power squeezes TGS margins as renewables shift data demand

Customers’ bargaining power is high: top 10 oil majors held ~42% of upstream CAPEX in 2024, pushing discounts and tight licensing; TGS’s 2024 revenue $678m means single large client moves can shift annual revenue by several percent. Multi-client sales ~42% of marine seismic in 2024 compress margins; renewables capex (BP/Equinor/Shell) hit ~$45B in 2024, forcing cross-domain data demands and price pressure.

| Metric | 2024 value |

|---|---|

| Top-10 upstream CAPEX share | ~42% |

| TGS 2024 revenue | $678m |

| Multi-client marine share | ~42% |

| Renewables capex (BP/Equinor/Shell) | $45B |

What You See Is What You Get

TGS Porter's Five Forces Analysis

This preview shows the exact TGS Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the final, fully formatted file you'll be able to download and use the moment you buy.

You're viewing the actual deliverable: a complete, professionally written analysis ready for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

TGS faces a mix of powerful suppliers, evolving buyer demands, moderate substitution risk, and competitive rivalry that shapes its strategic choices—this snapshot highlights key pressure points and growth levers for the company.

Suppliers Bargaining Power

Concentration of High-End Vessel Owners

The market for specialized seismic vessels is concentrated among a few global owners (CGG, Polarcus, Magseis Fairfield, and others), giving them pricing power when demand spikes; spot charter rates surged ~40% in 2022–23, peaking near $60–80k/day for 3D vessels.

After merging with PGS in 2023, TGS added owned capacity but still charters third-party vessels for niche jobs; in 2024 about 25–35% of its vessel days were third-party, so charter-rate swings hit project EBITDA directly.

Dominance of Specialized Technology and Cloud Providers

TGS depends on high-performance computing and cloud services from a few giants to process petabyte‑scale seismic datasets; in 2024 hyperscalers controlled ~70% of global cloud IaaS market, concentrating supplier power.

Proprietary software stacks and data egress fees create high switching costs—moving 1 PB can cost >$100k and take weeks—so suppliers can push price and feature terms.

By late 2025, with AI/ML central to seismic interpretation, advanced compute remains a key cost driver, often 15–25% of project FCF in recent sector benchmarks.

Scarcity of Specialized Geophysical Equipment

Manufacture of seismic streamers, sensors, and ocean-bottom nodes is concentrated among a few engineered suppliers, giving them strong leverage over TGS; in 2024 about 70–80% of ocean-bottom node capacity came from three firms. Supply-chain disruptions can delay multi-client surveys by months and raise capex—TGS capex tied to equipment procurement was roughly $85–95m annually in 2023–2024—leaving few alternative sources if a primary maker stalls.

Highly Skilled Geoscientific Labor Market

The pool of experienced geophysicists and data scientists for advanced subsurface interpretation is small and in high demand, driving supplier power against TGS.

Competition from oil & gas and renewables raised industry median data scientist pay ~18% from 2019–2024; TGS needs top-market pay and cloud/ML tool investment to avoid losing talent and data-quality edge.

- Small talent pool

- Cross-sector competition

- Wage pressure ≈+18% (2019–2024)

- Must pay competitively and invest in tools

Regulatory and National Data Access Authorities

Governments and national oil companies act as sovereign suppliers, controlling access to offshore blocks and often taking 30–70% of upstream project revenue through licensing, royalties, and state participation (2024–25 averages in Africa and Latin America).

They impose strict data-sharing terms and local content rules that raise upfront costs; new 2025 environmental and maritime rules could add 5–12% to compliance costs and delay surveys by 3–9 months.

- State take: 30–70% revenue

- Local content: hiring/CapEx premium +10–25%

- 2025 regs: +5–12% compliance cost

- Survey delays: 3–9 months

Concentrated suppliers, rising costs & state take squeeze TGS project margins

Supplier power is high: vessel owners and streamer/node makers are concentrated (top 3 hold ~70–80% capacity), hyperscalers control ~70% IaaS, and talent pool is tight (data‑scientist pay +18% 2019–24), so charter/cloud/equipment costs and wages materially squeeze TGS project EBITDA. Governments add state take (30–70%) and local content (+10–25%), raising compliance and delay risk.

| Metric | Value |

|---|---|

| Top-3 equipment share | 70–80% |

| Hyperscaler IaaS share (2024) | ~70% |

| Data-scientist pay change (2019–24) | +18% |

| State take (regions) | 30–70% |

| Local content premium | +10–25% |

What is included in the product

Concise Porter's Five Forces for TGS: evaluates competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive trends and market barriers shaping TGS’s pricing power and profitability—editable for reports or investor materials.

Concise Porter's Five Forces snapshot tailored for TGS—quickly spot competitive pressures and tactical levers to relieve margin squeeze or protect pricing power.

Customers Bargaining Power

Consolidation of Global Energy Supermajors

The customer base for seismic data is concentrating as global supermajors merge; since 2015, the top 10 oil & gas firms’ share of upstream CAPEX rose to ~42% in 2024, boosting their bargaining leverage. This consolidation lets buyers demand volume discounts and tighter licensing—TGS reported 2024 revenue of $678m, so a single major client shifting procurement could swing annual revenue by several percent. Fewer independents mean contract terms and renewals now drive material pricing pressure.

Budget Sensitivity to Energy Price Volatility

TGS customers’ capex tracks oil/gas prices; a 40% Brent drop in 2020 showed exploration budgets fall first, and by late 2025 E&P firms report >15% tighter capex and require payback horizons under 24 months, forcing TGS to offer flexible pricing, staged deliveries, and deferred payments to win contracts.

Adoption of Multi-Client Subscription Models

Customers increasingly prefer multi-client subscription libraries, shifting spend from proprietary surveys to shared-cost models; industry reports show multi-client revenue comprised about 42% of global marine seismic sales in 2024, boosting TGS recurring revenue but compressing per-project margins.

This collective buying lets clients push TGS on uniform data formats and tiered pricing; in recent tender rounds, buyers negotiated average price reductions of 12–18% for bundled legacy data sets.

Because TGS maintains a vast library—over 2.5 million km of 2D/3D seismic and public-domain compilations—clients often delay purchases, waiting 9–15 months for older surveys to be discounted, pressuring new acquisition financing and product launch timing.

Demand for Integrated Energy Transition Data

As oil majors shift to broad energy providers, demand for integrated data spanning offshore wind, carbon capture and hydrocarbons rose; BP, Equinor and Shell increased renewables capex to about $45B in 2024, pushing cross-domain data needs.

Customers now pit providers on breadth and depth, so TGS must expand wind and CCS datasets or lose contracts to niche renewable data firms growing ~12% CAGR; failure risks revenue erosion in existing seismic services.

- TGS must add wind/CCS layers

- Customers favor cross-functional vendors

- Renewables data market growing ~12% CAGR

Internal Data Processing Capabilities of Clients

Top oil majors’ buying power squeezes TGS margins as renewables shift data demand

Customers’ bargaining power is high: top 10 oil majors held ~42% of upstream CAPEX in 2024, pushing discounts and tight licensing; TGS’s 2024 revenue $678m means single large client moves can shift annual revenue by several percent. Multi-client sales ~42% of marine seismic in 2024 compress margins; renewables capex (BP/Equinor/Shell) hit ~$45B in 2024, forcing cross-domain data demands and price pressure.

| Metric | 2024 value |

|---|---|

| Top-10 upstream CAPEX share | ~42% |

| TGS 2024 revenue | $678m |

| Multi-client marine share | ~42% |

| Renewables capex (BP/Equinor/Shell) | $45B |

What You See Is What You Get

TGS Porter's Five Forces Analysis

This preview shows the exact TGS Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the final, fully formatted file you'll be able to download and use the moment you buy.

You're viewing the actual deliverable: a complete, professionally written analysis ready for immediate application.