Heineken PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Heineken faces shifting regulatory, economic, and social pressures that reshape market access and consumer demand; our concise PESTLE highlights these forces and their strategic implications. Want the complete, actionable breakdown—ready for investor decks and strategy sessions? Purchase the full PESTLE analysis to get detailed insights, forecasts, and editable files for immediate use.

Political factors

Global trade barriers and tariffs

Heineken operates in over 190 countries, leaving it exposed to shifting trade policies and protectionist measures seen through 2025, including a 12% average increase in applied tariffs on beverages in certain emerging markets. Increased tariffs on imported barley or aluminum cans—inputs that account for roughly 15–20% of COGS in regional breweries—can materially raise unit costs and compress margins. Strategic use of regional trade agreements (EU, USMCA, ASEAN) and local sourcing helped reduce tariff impact by an estimated €120m in 2024, but ongoing policy volatility requires active supply-chain and pricing adjustments to keep the global Heineken brand competitively priced.

Geopolitical instability in emerging markets

Heineken's significant exposure—over 25% of 2024 revenue from Africa, the Middle East and Asia-Pacific—raises risks from civil unrest and government transitions that have in past decades caused temporary plant closures and supply shocks. Political volatility can trigger sudden operational shutdowns or asset seizures, jeopardizing multi-year infrastructure investments of hundreds of millions of euros. Heineken must regularly reassess its footprint to weigh high-growth CAGR opportunities (often 5–8%+) against such upheaval risks.

Changes in alcohol excise duties

Governments often raise excise duties to boost revenue or curb alcohol harm, directly lifting retail prices; UK duty increases in 2023 raised beer duty by 10% in real terms, while Vietnam hiked beer taxes 15% in 2024, suppressing volumes. Higher taxes in major markets have driven declines in off-trade beer sales—UK beer volume fell ~1.5% in 2023—prompting shifts to lower-cost brands. Heineken tracks fiscal moves to realign pricing, promotions and preserve its premium positioning and margin.

Stricter marketing and advertising regulations

Stricter global limits on alcohol advertising—e.g., EU proposals tightening digital ad rules and France’s 2024 Loi Evin enforcement—reduce Heineken’s reach on platforms with 20%+ youth audiences, forcing a pivot to experiential and sponsorship-led marketing.

Noncompliance risks fines (up to 5% of revenue in some jurisdictions) and reputational harm; Heineken (2024 net revenue €30.8bn) must navigate divergent regional codes, raising compliance costs and shifting spend toward subtle branding.

- Advertising reach constrained on digital and live sports

- Shift to experiential, influencer restrictions, and POS marketing

- Regulatory fines and compliance costs potentially material vs €30.8bn revenue

Governmental focus on local sourcing

- 32% of G20 countries with local-sourcing policies (2024)

- ~40% of Heineken barley sourced locally in key markets

- Potential tax/incentive savings: millions per country

Heineken margins pressured by tariffs, taxes and ad bans despite €120m sourcing gains

Political risks—tariffs up ~12% in some emerging markets (2024), excise hikes (UK beer duty +10% real 2023; Vietnam tax +15% 2024), 25%+ revenue exposure to AfMEAP, and advertising restrictions (EU/France 2024)—raise input, compliance and marketing costs; regional sourcing saved ~€120m in 2024 but volatility threatens margins of €30.8bn revenue Heineken.

| Metric | Value |

|---|---|

| Revenue (2024) | €30.8bn |

| Tariff rise (emerging) | ~12% |

| Revenue from AfMEAP | >25% |

| Saved via regional sourcing (2024) | €120m |

What is included in the product

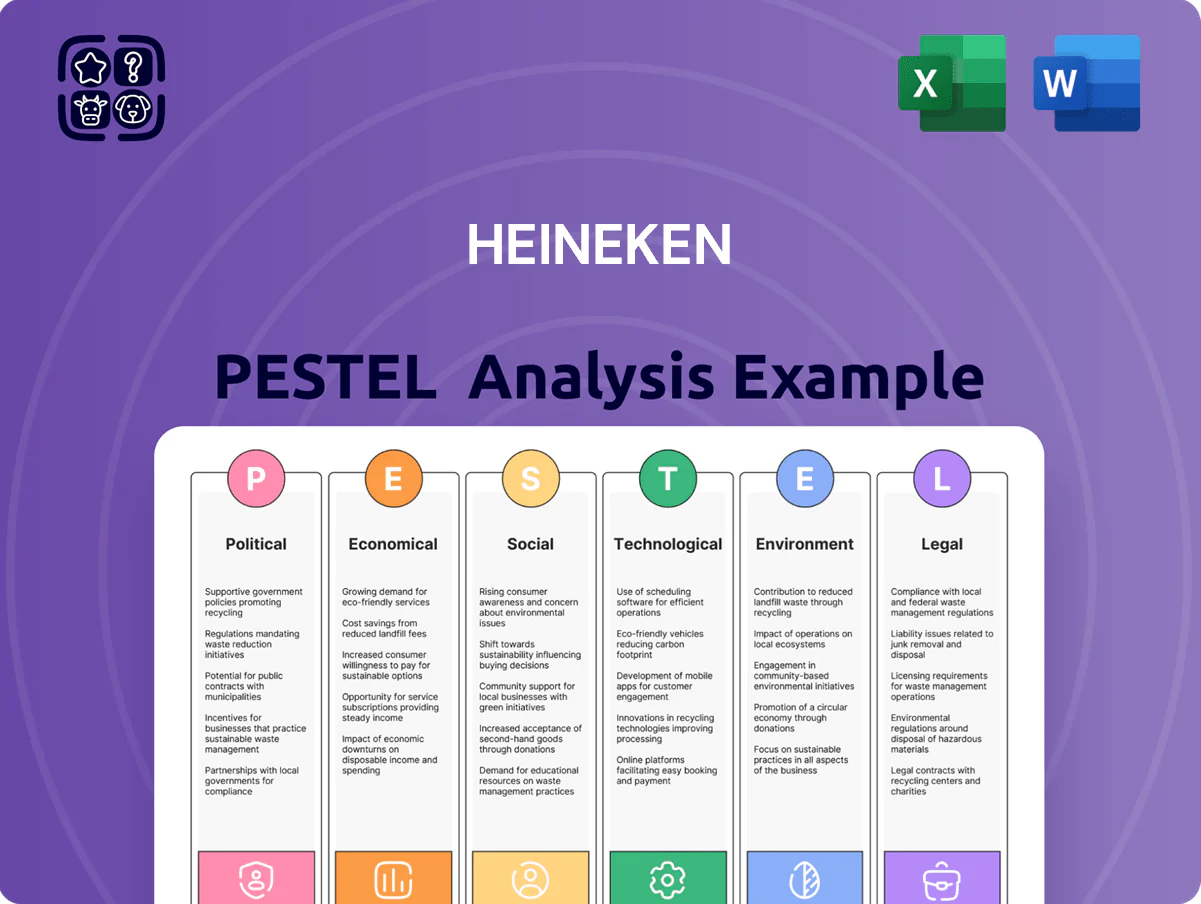

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Heineken, combining data-driven trends and regional insights to identify risks, opportunities, and strategic responses for executives, investors, and consultants.

A concise Heineken PESTLE summary that highlights key political, economic, social, technological, legal, and environmental factors for quick reference in meetings or presentations.

Economic factors

Global inflationary pressures on inputs

By end‑2025 persistent inflation in energy, logistics and raw materials—average input cost inflation ~7–9% y/y in 2024–25—continues to squeeze brewing margins, with malt up ~12% and container glass up ~8% in key markets.

Heineken deploys hedging and EverGreen efficiency programs, targeting €200–€300m in annual cost savings by 2025 to offset higher input costs.

Selective price increases in 2024–25 raised net selling prices ~3–5% but passing full costs risks volume loss in price‑sensitive markets where elasticity is high.

Currency exchange rate volatility

As a Euro-reporting multinational, Heineken faces transactional and translational risks from FX swings in markets like Nigeria and Brazil; between 2022–2024 the NGN fell ~35% and BRL ~18% vs EUR, reducing repatriated profits. Currency devaluations raise imported-capex costs—Heineken noted FX impacts of €150–€200m in recent annuals. The company uses hedging, FX forwards and local-currency debt to stabilize its balance sheet.

Shifts in consumer disposable income

Economic downturns in Heineken’s mature markets can cut discretionary spending on premium beer; global consumer spending fell amid 2023–24 inflation waves, with real disposable income in EU households down ~1.5% YoY in 2023, pressuring premium categories.

The premium segment shows resilience—Heineken’s 2024 premium portfolio delivered mid-single-digit volume growth—but prolonged cost-of-living stress risks trade-downs to value brands and less out-of-home consumption.

Heineken mitigates this with a broad portfolio across price points; in 2024 Heineken reported diversified net revenue per hectolitre and growth in value-brand volumes in key markets, preserving market share during income shifts.

Interest rate environment and debt servicing

The 2025 higher interest rate environment (ECB deposit rate ~4.0% in late 2024; Fed funds ~5.25–5.50%) raises Heineken’s weighted average cost of capital, increasing financing costs for capex across its ~170 breweries and global distribution network.

Elevated rates heighten debt-servicing expenses on Heineken’s €13.4bn net debt (2024), encouraging caution on large acquisitions and prioritizing cash flow generation.

The group targets strong investment-grade credit metrics (net debt/EBITDA ~2.5x in 2024) to secure favorable borrowing terms for strategic growth.

- Higher market rates → higher WACC and capex cost

- €13.4bn net debt (2024) → increased interest expense risk

- Net debt/EBITDA ~2.5x → focus on credit rating maintenance

Growth of the non-alcoholic market segment

- Heineken 0.0: multi-point revenue contributor;

- Lower excise taxes improve net margin;

- 20% CAGR (2019–2024) indicates strong upside;

Heineken margins squeezed by inflation, FX; €200–300m cuts, non‑alc 20% CAGR

Inflation (input costs +7–9% in 2024–25) and FX volatility (NGN -35%, BRL -18% vs EUR 2022–24) pressure margins; Heineken targets €200–€300m savings and uses hedging. Net debt €13.4bn (2024), net debt/EBITDA ~2.5x increases financing costs amid ECB rate ~4%/Fed ~5.25–5.5%. Non‑alcoholic segment grew ~20% CAGR (2019–24), ~€5–6bn value in core markets.

| Metric | Value |

|---|---|

| Input inflation | 7–9% (2024–25) |

| Net debt | €13.4bn (2024) |

| Net debt/EBITDA | ~2.5x (2024) |

| FX moves | NGN -35%, BRL -18% (2022–24) |

| EverGreen savings | €200–€300m target (by 2025) |

| 0.0 market | ~20% CAGR (2019–24); €5–6bn (2024) |

Preview Before You Purchase

Heineken PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Heineken PESTLE Analysis covers political, economic, social, technological, legal, and environmental factors with concise insights and actionable implications for strategy and investment. No placeholders or teasers—what you see is the final, downloadable file. Use it immediately for research, presentations, or decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Heineken faces shifting regulatory, economic, and social pressures that reshape market access and consumer demand; our concise PESTLE highlights these forces and their strategic implications. Want the complete, actionable breakdown—ready for investor decks and strategy sessions? Purchase the full PESTLE analysis to get detailed insights, forecasts, and editable files for immediate use.

Political factors

Global trade barriers and tariffs

Heineken operates in over 190 countries, leaving it exposed to shifting trade policies and protectionist measures seen through 2025, including a 12% average increase in applied tariffs on beverages in certain emerging markets. Increased tariffs on imported barley or aluminum cans—inputs that account for roughly 15–20% of COGS in regional breweries—can materially raise unit costs and compress margins. Strategic use of regional trade agreements (EU, USMCA, ASEAN) and local sourcing helped reduce tariff impact by an estimated €120m in 2024, but ongoing policy volatility requires active supply-chain and pricing adjustments to keep the global Heineken brand competitively priced.

Geopolitical instability in emerging markets

Heineken's significant exposure—over 25% of 2024 revenue from Africa, the Middle East and Asia-Pacific—raises risks from civil unrest and government transitions that have in past decades caused temporary plant closures and supply shocks. Political volatility can trigger sudden operational shutdowns or asset seizures, jeopardizing multi-year infrastructure investments of hundreds of millions of euros. Heineken must regularly reassess its footprint to weigh high-growth CAGR opportunities (often 5–8%+) against such upheaval risks.

Changes in alcohol excise duties

Governments often raise excise duties to boost revenue or curb alcohol harm, directly lifting retail prices; UK duty increases in 2023 raised beer duty by 10% in real terms, while Vietnam hiked beer taxes 15% in 2024, suppressing volumes. Higher taxes in major markets have driven declines in off-trade beer sales—UK beer volume fell ~1.5% in 2023—prompting shifts to lower-cost brands. Heineken tracks fiscal moves to realign pricing, promotions and preserve its premium positioning and margin.

Stricter marketing and advertising regulations

Stricter global limits on alcohol advertising—e.g., EU proposals tightening digital ad rules and France’s 2024 Loi Evin enforcement—reduce Heineken’s reach on platforms with 20%+ youth audiences, forcing a pivot to experiential and sponsorship-led marketing.

Noncompliance risks fines (up to 5% of revenue in some jurisdictions) and reputational harm; Heineken (2024 net revenue €30.8bn) must navigate divergent regional codes, raising compliance costs and shifting spend toward subtle branding.

- Advertising reach constrained on digital and live sports

- Shift to experiential, influencer restrictions, and POS marketing

- Regulatory fines and compliance costs potentially material vs €30.8bn revenue

Governmental focus on local sourcing

- 32% of G20 countries with local-sourcing policies (2024)

- ~40% of Heineken barley sourced locally in key markets

- Potential tax/incentive savings: millions per country

Heineken margins pressured by tariffs, taxes and ad bans despite €120m sourcing gains

Political risks—tariffs up ~12% in some emerging markets (2024), excise hikes (UK beer duty +10% real 2023; Vietnam tax +15% 2024), 25%+ revenue exposure to AfMEAP, and advertising restrictions (EU/France 2024)—raise input, compliance and marketing costs; regional sourcing saved ~€120m in 2024 but volatility threatens margins of €30.8bn revenue Heineken.

| Metric | Value |

|---|---|

| Revenue (2024) | €30.8bn |

| Tariff rise (emerging) | ~12% |

| Revenue from AfMEAP | >25% |

| Saved via regional sourcing (2024) | €120m |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact Heineken, combining data-driven trends and regional insights to identify risks, opportunities, and strategic responses for executives, investors, and consultants.

A concise Heineken PESTLE summary that highlights key political, economic, social, technological, legal, and environmental factors for quick reference in meetings or presentations.

Economic factors

Global inflationary pressures on inputs

By end‑2025 persistent inflation in energy, logistics and raw materials—average input cost inflation ~7–9% y/y in 2024–25—continues to squeeze brewing margins, with malt up ~12% and container glass up ~8% in key markets.

Heineken deploys hedging and EverGreen efficiency programs, targeting €200–€300m in annual cost savings by 2025 to offset higher input costs.

Selective price increases in 2024–25 raised net selling prices ~3–5% but passing full costs risks volume loss in price‑sensitive markets where elasticity is high.

Currency exchange rate volatility

As a Euro-reporting multinational, Heineken faces transactional and translational risks from FX swings in markets like Nigeria and Brazil; between 2022–2024 the NGN fell ~35% and BRL ~18% vs EUR, reducing repatriated profits. Currency devaluations raise imported-capex costs—Heineken noted FX impacts of €150–€200m in recent annuals. The company uses hedging, FX forwards and local-currency debt to stabilize its balance sheet.

Shifts in consumer disposable income

Economic downturns in Heineken’s mature markets can cut discretionary spending on premium beer; global consumer spending fell amid 2023–24 inflation waves, with real disposable income in EU households down ~1.5% YoY in 2023, pressuring premium categories.

The premium segment shows resilience—Heineken’s 2024 premium portfolio delivered mid-single-digit volume growth—but prolonged cost-of-living stress risks trade-downs to value brands and less out-of-home consumption.

Heineken mitigates this with a broad portfolio across price points; in 2024 Heineken reported diversified net revenue per hectolitre and growth in value-brand volumes in key markets, preserving market share during income shifts.

Interest rate environment and debt servicing

The 2025 higher interest rate environment (ECB deposit rate ~4.0% in late 2024; Fed funds ~5.25–5.50%) raises Heineken’s weighted average cost of capital, increasing financing costs for capex across its ~170 breweries and global distribution network.

Elevated rates heighten debt-servicing expenses on Heineken’s €13.4bn net debt (2024), encouraging caution on large acquisitions and prioritizing cash flow generation.

The group targets strong investment-grade credit metrics (net debt/EBITDA ~2.5x in 2024) to secure favorable borrowing terms for strategic growth.

- Higher market rates → higher WACC and capex cost

- €13.4bn net debt (2024) → increased interest expense risk

- Net debt/EBITDA ~2.5x → focus on credit rating maintenance

Growth of the non-alcoholic market segment

- Heineken 0.0: multi-point revenue contributor;

- Lower excise taxes improve net margin;

- 20% CAGR (2019–2024) indicates strong upside;

Heineken margins squeezed by inflation, FX; €200–300m cuts, non‑alc 20% CAGR

Inflation (input costs +7–9% in 2024–25) and FX volatility (NGN -35%, BRL -18% vs EUR 2022–24) pressure margins; Heineken targets €200–€300m savings and uses hedging. Net debt €13.4bn (2024), net debt/EBITDA ~2.5x increases financing costs amid ECB rate ~4%/Fed ~5.25–5.5%. Non‑alcoholic segment grew ~20% CAGR (2019–24), ~€5–6bn value in core markets.

| Metric | Value |

|---|---|

| Input inflation | 7–9% (2024–25) |

| Net debt | €13.4bn (2024) |

| Net debt/EBITDA | ~2.5x (2024) |

| FX moves | NGN -35%, BRL -18% (2022–24) |

| EverGreen savings | €200–€300m target (by 2025) |

| 0.0 market | ~20% CAGR (2019–24); €5–6bn (2024) |

Preview Before You Purchase

Heineken PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Heineken PESTLE Analysis covers political, economic, social, technological, legal, and environmental factors with concise insights and actionable implications for strategy and investment. No placeholders or teasers—what you see is the final, downloadable file. Use it immediately for research, presentations, or decision-making.