Lion Electric Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Lion Electric faces strong supplier and technology-driven pressures but benefits from rising EV demand and niche commercial vehicle focus; competitive intensity hinges on scale, battery supply, and regulatory tailwinds that could reshape profitability.

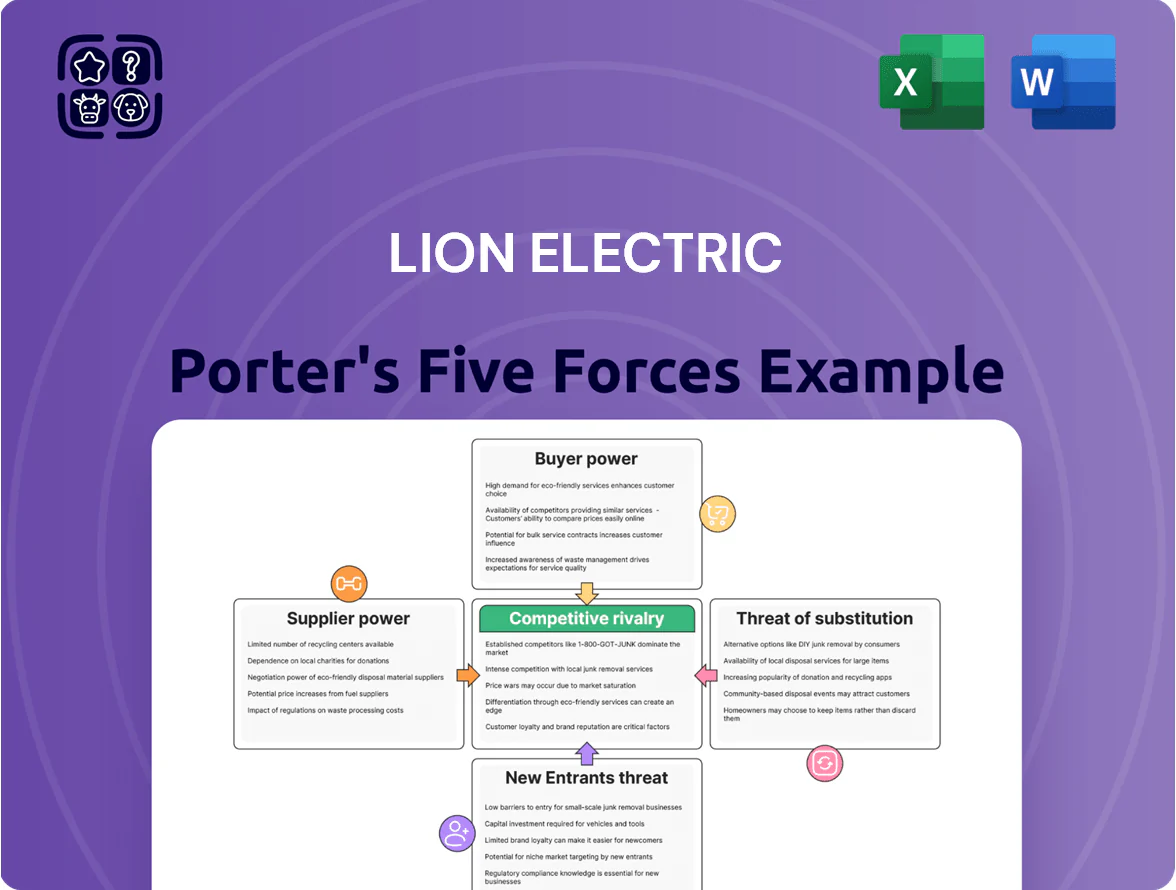

Suppliers Bargaining Power

Concentration of battery cell manufacturers

The battery-cell market is highly concentrated: CATL, LG Energy Solution, and Panasonic held about 60–70% of global EV cell capacity in 2024, giving them clear pricing power over Lion Electric, which outsources its most costly component.

Lion’s dependence raises margin risk—cells can be ~30–40% of an electric bus’s BOM—and late-2025 swings in lithium, nickel, or cobalt prices or supply shocks rapidly squeezed gross margins and delayed deliveries.

Scarcity of critical minerals and raw materials

The production of Lion Electric medium and heavy-duty EVs depends heavily on lithium, cobalt, and nickel; global battery-grade lithium demand rose 40% in 2023 to ~550 kt LCE (lithium carbonate equivalent), intensifying competition from passenger EVs and grid storage and creating a sellers’ market for miners. Lion faces limited leverage: long-term offtakes and premiums are common, and spot nickel jumped 90% in 2022–23, forcing higher input costs and constrained price negotiation power.

Specialized semiconductor and electronic components

Modern Lion Electric trucks and buses rely on specialized semiconductors for power electronics and ADAS sensors; by 2025 global auto-grade semiconductor lead times fell to ~12 weeks from peaks over 30 weeks, but Lion still buys from a narrow set of suppliers representing >60% of its critical IC spend.

This supplier concentration limits switching: redesign and re-certification can cost millions and add 6–18 months to program timelines, constraining Lion’s negotiating leverage and raising input-cost volatility risk.

Limited vertical integration of powertrain components

Lion Electric designs many systems internally but still buys high-voltage cables, thermal management modules, and electric motors from Tier 1 specialists, leaving suppliers with leverage due to proprietary tech and scale.

Switching these items in-house would likely cost hundreds of millions and delay launches; supplier R&D thus sets upgrade timing and creates a collaborative yet vulnerable dependency.

- Tier 1 control: proprietary IP and scale

- In-house switch cost: likely $100–300M capex

- Supplier-led R&D dictates upgrade cadence

Impact of regional manufacturing requirements

Regional content rules like the US Inflation Reduction Act (2022) force Lion Electric to source batteries and key EV components in North America, shrinking its vendor pool and cutting leverage to import cheaper Asian parts.

With Canada/US local sourcing targets, Lion faces higher input costs; e.g., NA battery pack premiums of ~10–20% vs Asia raise vehicle COGS and limit price negotiation.

Local suppliers can sustain higher margins because Lion must meet regional thresholds to qualify customers for subsidies, reducing Lion’s bargaining power.

- IRA (2022) and Canadian procurement rules restrict sourcing regions

- NA battery premium ~10–20% vs Asia

- Smaller vendor pool → less price competition

- Local suppliers retain pricing power due to subsidy rules

Concentrated EV supply chain drives price volatility, redesign risk, and a 10–20% NA battery premium

Supplier power is high: three cell makers (CATL, LG, Panasonic) held ~60–70% of EV cell capacity in 2024, making cells ~30–40% of bus BOM and exposing Lion to input-price swings.

Critical materials demand rose sharply—battery-grade lithium ~550 kt LCE in 2023 (+40%)—tightening supply and raising spot-price volatility; nickel jumped ~90% in 2022–23.

Specialized semis and Tier-1 parts concentrate >60% of critical spend, redesigns cost $100–300M and add 6–18 months, while IRA regional rules impose a NA battery premium ~10–20%, shrinking vendor choices.

| Metric | Value |

|---|---|

| Top cell makers share (2024) | 60–70% |

| Battery-grade lithium (2023) | ~550 kt LCE (+40% YoY) |

| Nickel spot move (2022–23) | ~+90% |

| Cells share of BOM | ~30–40% |

| In-house switch cost | $100–300M |

| NA battery premium vs Asia | ~10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for Lion Electric, uncovering key competitive drivers, supplier and buyer power, substitution threats, and entry barriers with strategic insights to inform investor decks and internal strategy.

A concise Porter's Five Forces snapshot for Lion Electric—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Dependence on government subsidies and grants

A large share of Lion Electric’s buyers—school districts and transit agencies—depend on federal/state grants; the EPA’s Clean School Bus Program allocated about $5 billion through 2023, and 2024–25 discretionary renewals remain uncertain. If incentives are cut or delayed by end-2025, customers could defer orders or demand deeper discounts, pressuring Lion’s margins. Here’s the quick math: a $300k electric bus needs ~$100k–$150k subsidy to match diesel cost; loss of that funding ties purchase decisions to policy, not need.

High volume procurement by fleet operators

Total Cost of Ownership sensitivity

Commercial buyers use strict Total Cost of Ownership (TCO) models—fleet operators report average 25–40% lower operating costs for EVs vs diesel over 8 years per 2024 CALSTART and ICCT data—so Lion must prove comparable savings.

Customers demand guaranteed fuel and maintenance savings; surveys show 62% of fleets require uptime/energy guarantees before switching, shifting risk to Lion.

That pressure forces Lion to supply granular performance data, warranties, and service SLAs, raising upfront R&D and warranty reserves—Lion disclosed CAD 23.5M in warranty provisions in FY2024.

Low switching costs for future fleet expansion

While initial charging investments (average depot EV charging capex ~$150–250k per site in 2024) create some lock-in, many fleet operators are trialing trucks from multiple OEMs at once, reducing allegiance.

By late 2025, with ~15–20 OEMs targeting medium/heavy electric trucks and growing production, customers can pivot easily if Lion misses deliveries or service SLA targets.

This low switching-cost environment raises pressure on Lion for timely deliveries, strong uptime (target >95%), and competitive pricing to retain orders.

- Charging capex ~$150–250k/site (2024)

- 15–20 OEMs entering e-truck market by late 2025

- Customer uptime target >95% raises service stakes

- Low brand lock-in increases price/service sensitivity

Infrastructure and service support requirements

Customers demand turnkey packages—vehicle plus charging and multi-year maintenance—letting buyers push for bundled pricing and strict service-level agreements that shrink Lion Electric’s margins; fleet operators in North America placed 2024 EV total cost-of-ownership (TCO) as a top criterion, with 62% citing charging/network support as decisive.

If Lion fails to deliver an integrated ecosystem, fleets can switch to rivals (e.g., BYD, Volvo) offering end-to-end fleet management, giving customers clear exit leverage and raising Lion’s customer acquisition costs.

- Bundled deals reduce margin

- 62% of fleets cite charging support (2024)

- Competitors offer turnkey fleet services

- Risk: higher churn and CAC

Fleet buyers wield leverage: subsidies, bulk demand & uptime force discounts on Lion

Buyers (school districts, fleets) hold high bargaining power due to subsidy dependence (Clean School Bus ~$5B through 2023), bulk volumes (large fleets ≈40% of projected demand by 2028), strict TCO/uptime demands (62% require charging support; target uptime >95%), and many OEM alternatives (15–20 e‑truck entrants by late 2025), forcing Lion into discounts, bundled deals, and higher warranty/service costs (CAD 23.5M FY2024).

| Metric | Value |

|---|---|

| Clean School Bus funding | $5B (through 2023) |

| Fleet share of e‑truck demand | ≈40% (by 2028) |

| Fleets requiring charging support | 62% (2024) |

| Uptime target | >95% |

| OEM entrants | 15–20 (by late 2025) |

| Lion warranty reserves | CAD 23.5M (FY2024) |

Preview the Actual Deliverable

Lion Electric Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Lion Electric you'll receive immediately after purchase—no placeholders, no samples. The file is fully formatted and ready for download and use the moment you buy. It is the complete, final deliverable covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Instant access to this precise document upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Lion Electric faces strong supplier and technology-driven pressures but benefits from rising EV demand and niche commercial vehicle focus; competitive intensity hinges on scale, battery supply, and regulatory tailwinds that could reshape profitability.

Suppliers Bargaining Power

Concentration of battery cell manufacturers

The battery-cell market is highly concentrated: CATL, LG Energy Solution, and Panasonic held about 60–70% of global EV cell capacity in 2024, giving them clear pricing power over Lion Electric, which outsources its most costly component.

Lion’s dependence raises margin risk—cells can be ~30–40% of an electric bus’s BOM—and late-2025 swings in lithium, nickel, or cobalt prices or supply shocks rapidly squeezed gross margins and delayed deliveries.

Scarcity of critical minerals and raw materials

The production of Lion Electric medium and heavy-duty EVs depends heavily on lithium, cobalt, and nickel; global battery-grade lithium demand rose 40% in 2023 to ~550 kt LCE (lithium carbonate equivalent), intensifying competition from passenger EVs and grid storage and creating a sellers’ market for miners. Lion faces limited leverage: long-term offtakes and premiums are common, and spot nickel jumped 90% in 2022–23, forcing higher input costs and constrained price negotiation power.

Specialized semiconductor and electronic components

Modern Lion Electric trucks and buses rely on specialized semiconductors for power electronics and ADAS sensors; by 2025 global auto-grade semiconductor lead times fell to ~12 weeks from peaks over 30 weeks, but Lion still buys from a narrow set of suppliers representing >60% of its critical IC spend.

This supplier concentration limits switching: redesign and re-certification can cost millions and add 6–18 months to program timelines, constraining Lion’s negotiating leverage and raising input-cost volatility risk.

Limited vertical integration of powertrain components

Lion Electric designs many systems internally but still buys high-voltage cables, thermal management modules, and electric motors from Tier 1 specialists, leaving suppliers with leverage due to proprietary tech and scale.

Switching these items in-house would likely cost hundreds of millions and delay launches; supplier R&D thus sets upgrade timing and creates a collaborative yet vulnerable dependency.

- Tier 1 control: proprietary IP and scale

- In-house switch cost: likely $100–300M capex

- Supplier-led R&D dictates upgrade cadence

Impact of regional manufacturing requirements

Regional content rules like the US Inflation Reduction Act (2022) force Lion Electric to source batteries and key EV components in North America, shrinking its vendor pool and cutting leverage to import cheaper Asian parts.

With Canada/US local sourcing targets, Lion faces higher input costs; e.g., NA battery pack premiums of ~10–20% vs Asia raise vehicle COGS and limit price negotiation.

Local suppliers can sustain higher margins because Lion must meet regional thresholds to qualify customers for subsidies, reducing Lion’s bargaining power.

- IRA (2022) and Canadian procurement rules restrict sourcing regions

- NA battery premium ~10–20% vs Asia

- Smaller vendor pool → less price competition

- Local suppliers retain pricing power due to subsidy rules

Concentrated EV supply chain drives price volatility, redesign risk, and a 10–20% NA battery premium

Supplier power is high: three cell makers (CATL, LG, Panasonic) held ~60–70% of EV cell capacity in 2024, making cells ~30–40% of bus BOM and exposing Lion to input-price swings.

Critical materials demand rose sharply—battery-grade lithium ~550 kt LCE in 2023 (+40%)—tightening supply and raising spot-price volatility; nickel jumped ~90% in 2022–23.

Specialized semis and Tier-1 parts concentrate >60% of critical spend, redesigns cost $100–300M and add 6–18 months, while IRA regional rules impose a NA battery premium ~10–20%, shrinking vendor choices.

| Metric | Value |

|---|---|

| Top cell makers share (2024) | 60–70% |

| Battery-grade lithium (2023) | ~550 kt LCE (+40% YoY) |

| Nickel spot move (2022–23) | ~+90% |

| Cells share of BOM | ~30–40% |

| In-house switch cost | $100–300M |

| NA battery premium vs Asia | ~10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for Lion Electric, uncovering key competitive drivers, supplier and buyer power, substitution threats, and entry barriers with strategic insights to inform investor decks and internal strategy.

A concise Porter's Five Forces snapshot for Lion Electric—quickly highlights supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decisions.

Customers Bargaining Power

Dependence on government subsidies and grants

A large share of Lion Electric’s buyers—school districts and transit agencies—depend on federal/state grants; the EPA’s Clean School Bus Program allocated about $5 billion through 2023, and 2024–25 discretionary renewals remain uncertain. If incentives are cut or delayed by end-2025, customers could defer orders or demand deeper discounts, pressuring Lion’s margins. Here’s the quick math: a $300k electric bus needs ~$100k–$150k subsidy to match diesel cost; loss of that funding ties purchase decisions to policy, not need.

High volume procurement by fleet operators

Total Cost of Ownership sensitivity

Commercial buyers use strict Total Cost of Ownership (TCO) models—fleet operators report average 25–40% lower operating costs for EVs vs diesel over 8 years per 2024 CALSTART and ICCT data—so Lion must prove comparable savings.

Customers demand guaranteed fuel and maintenance savings; surveys show 62% of fleets require uptime/energy guarantees before switching, shifting risk to Lion.

That pressure forces Lion to supply granular performance data, warranties, and service SLAs, raising upfront R&D and warranty reserves—Lion disclosed CAD 23.5M in warranty provisions in FY2024.

Low switching costs for future fleet expansion

While initial charging investments (average depot EV charging capex ~$150–250k per site in 2024) create some lock-in, many fleet operators are trialing trucks from multiple OEMs at once, reducing allegiance.

By late 2025, with ~15–20 OEMs targeting medium/heavy electric trucks and growing production, customers can pivot easily if Lion misses deliveries or service SLA targets.

This low switching-cost environment raises pressure on Lion for timely deliveries, strong uptime (target >95%), and competitive pricing to retain orders.

- Charging capex ~$150–250k/site (2024)

- 15–20 OEMs entering e-truck market by late 2025

- Customer uptime target >95% raises service stakes

- Low brand lock-in increases price/service sensitivity

Infrastructure and service support requirements

Customers demand turnkey packages—vehicle plus charging and multi-year maintenance—letting buyers push for bundled pricing and strict service-level agreements that shrink Lion Electric’s margins; fleet operators in North America placed 2024 EV total cost-of-ownership (TCO) as a top criterion, with 62% citing charging/network support as decisive.

If Lion fails to deliver an integrated ecosystem, fleets can switch to rivals (e.g., BYD, Volvo) offering end-to-end fleet management, giving customers clear exit leverage and raising Lion’s customer acquisition costs.

- Bundled deals reduce margin

- 62% of fleets cite charging support (2024)

- Competitors offer turnkey fleet services

- Risk: higher churn and CAC

Fleet buyers wield leverage: subsidies, bulk demand & uptime force discounts on Lion

Buyers (school districts, fleets) hold high bargaining power due to subsidy dependence (Clean School Bus ~$5B through 2023), bulk volumes (large fleets ≈40% of projected demand by 2028), strict TCO/uptime demands (62% require charging support; target uptime >95%), and many OEM alternatives (15–20 e‑truck entrants by late 2025), forcing Lion into discounts, bundled deals, and higher warranty/service costs (CAD 23.5M FY2024).

| Metric | Value |

|---|---|

| Clean School Bus funding | $5B (through 2023) |

| Fleet share of e‑truck demand | ≈40% (by 2028) |

| Fleets requiring charging support | 62% (2024) |

| Uptime target | >95% |

| OEM entrants | 15–20 (by late 2025) |

| Lion warranty reserves | CAD 23.5M (FY2024) |

Preview the Actual Deliverable

Lion Electric Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Lion Electric you'll receive immediately after purchase—no placeholders, no samples. The file is fully formatted and ready for download and use the moment you buy. It is the complete, final deliverable covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. Instant access to this precise document upon payment.