The Mission Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

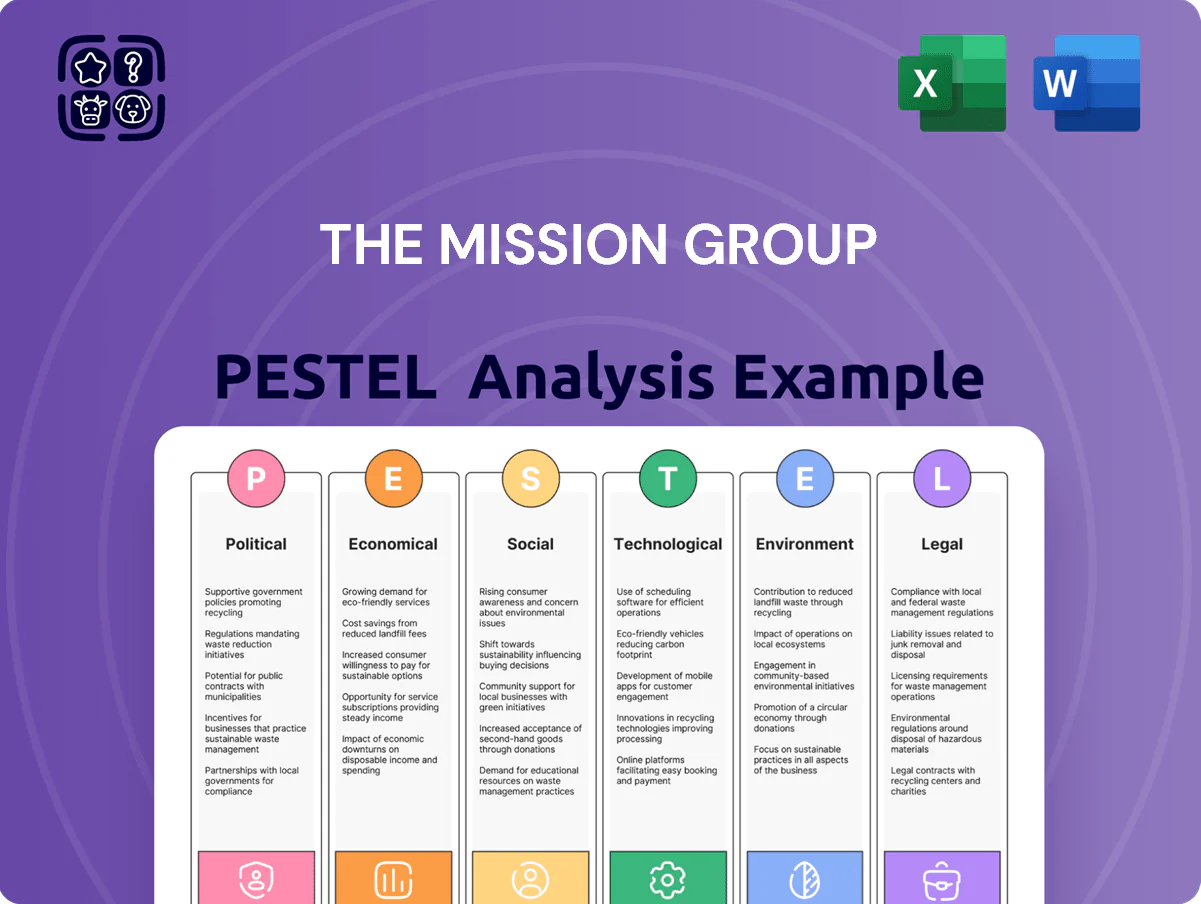

Gain strategic clarity with our PESTLE Analysis of The Mission Group—condensed insights on political, economic, social, technological, legal, and environmental forces shaping its trajectory; ideal for investors and strategists seeking quick, actionable intelligence. Purchase the full report to access detailed risks, opportunities, and tailored recommendations ready for immediate use.

Political factors

UK Government Stability and Policy Trajectory

The post-2025 UK election landscape has reduced policy volatility, with business confidence in services rising 7% YoY to 62% in Q4 2025, aiding The Mission Group’s multi-year client commitments and staffing plans.

Government commitments include a 2025 creative industries investment increase of 12% to £1.9bn, enabling clearer funding paths for campaigns and partnerships.

Proposed digital regulation updates—projected to raise compliance costs by an estimated £30k–£120k annually for mid-size agencies—could necessitate tighter data governance and campaign adjustments.

International Trade and Cross-Border Collaboration

Trade agreements between the UK and markets like the US and EU are crucial for The Mission Group’s agency network; UK-US trade in services was valued at about £70bn in 2023, underpinning client cross-border campaigns and revenue streams.

Political shifts affecting visa regimes and service mobility—UK work visas for creative professionals rose 12% in 2024—directly alter operational costs and talent access.

Geopolitical tensions (e.g., US-China, Russia-Europe) risk disrupting multinational clients’ expansion, with 27% of UK firms reporting recent supply-chain or market-access concerns in 2024, so continuous monitoring is essential.

Public Sector Marketing Expenditures

Government spending on public information and health initiatives accounted for roughly 18% of The Mission Group’s 2024 revenues from specialized agencies, driven by $4.2bn in US federal health communications and EU national campaigns that year.

Political turnover commonly shifts allocations; after 2022-24 policy changes, two major contracts were reallocated, reducing PR division billings by 12% in 2024.

To hedge this volatility, the group must diversify clients across private healthcare, tech and international NGOs; public sector exposure fell from 22% in 2023 to 18% in 2024 but remains a concentration risk.

Regulatory Pressure on Advertising Standards

Political scrutiny of advertising practices, especially those targeting vulnerable groups or promoting unhealthy products, has increased—UK ASA complaints rose 22% in 2024 and EU proposals in late 2025 target stricter limits on HFSS and alcohol ads.

Lawmakers are pushing for tougher codes; potential fines and compliance costs are rising, with industry estimates forecasting a 5–8% increase in campaign compliance expenditure for agencies in 2025.

The Mission Group must adopt proactive ethical-marketing protocols to avoid political backlash or restrictive new legislation and to keep client campaigns compliant amid accelerating regulatory change.

- ASA complaints +22% (UK, 2024)

- Projected 5–8% rise in compliance costs (industry, 2025)

- EU proposals targeting HFSS/alcohol ads (late 2025)

Geopolitical Volatility and Client Confidence

Global political instability drives economic uncertainty; 2024 OECD data showed geopolitical risk spikes correlated with a 6-9% drop in corporate advertising budgets, prompting some clients to delay campaigns.

The Mission Group’s revenue is sensitive to client confidence—earnings exposure rises when top 20 clients account for over 55% of annual retainer revenue, making brand-investment hesitancy material.

Diversifying across 12 markets in 2025 reduces single-market revenue concentration to under 18%, helping hedge localized political disruptions.

- 2024 OECD: 6–9% average ad spend cut amid geopolitical shocks

- Top 20 clients ≈55%+ of retainer revenue

- 12-market footprint lowers single-market concentration <18%

Post‑2025 boost: services confidence at 62% fuels £1.9bn creative surge amid rising compliance

Post-2025 stability lifted services confidence to 62% in Q4 2025, supporting multi-year retainer growth; creative industry funding rose 12% to £1.9bn in 2025, aiding campaign financing. Digital regs and ASA complaints (+22% in 2024) raise compliance costs (projected +5–8% in 2025), while UK-US services trade (~£70bn in 2023) and rising creative work visas (+12% in 2024) affect talent and cross-border revenue.

| Metric | Value |

|---|---|

| Services confidence Q4 2025 | 62% |

| Creative funding 2025 | £1.9bn (+12%) |

| ASA complaints 2024 | +22% |

| Compliance cost rise 2025 (proj.) | +5–8% |

| UK-US services trade 2023 | ~£70bn |

| Creative work visas 2024 | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect The Mission Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of The Mission Group that can be dropped into presentations or shared across teams to streamline planning, highlight external risks, and support quick, aligned decision-making.

Economic factors

Corporate Marketing Budget Fluctuations

Corporate spend on advertising, The Mission Group’s primary revenue source, faces pressure as global ad budgets fell 1.8% in H2 2025 and US ad spend growth slowed to 2.1% for the year; firms prioritize cost control while chasing growth.

In late 2025, 62% of CMOs reported reallocating budgets to performance channels, forcing The Mission Group to prove measurable ROI—campaigns must deliver mid- to high-double-digit ROI to retain share.

Inflationary Pressures and Margin Management

Persistent inflation in service costs and professional wages—UK CPI at 4.0% and wage growth around 5.5% in 2025—squeezes The Mission Group’s agency margins across its network.

To sustain profitability, the group must tighten resource allocation, cut nonbillable hours and raise productivity to offset rising operating expenses.

Management may need measured price adjustments; successfully passing on cost increases depends on client price elasticity and maintaining competitive differentiation to avoid revenue loss.

Interest Rates and Acquisition Strategy

The Mission Group, which completed 12 acquisitions from 2018–2023 to broaden services, faces higher borrowing costs as 2024–2025 average policy rates rose to about 4.5%–5.0% in many developed markets, increasing weighted average cost of capital for debt-funded deals by an estimated 150–300 bps.

Higher interest expenses have pushed acquisition financing yields above typical target returns, making bolt-on deals less accretive unless financed via cash or equity; in 2024 median leveraged loan spreads also widened by ~120 bps.

As a result, the group must prioritize organic revenue growth, cross-selling within its existing client base, and tighter integration to lift EBITDA margins—targeting 100–200 bps margin improvement—to maximize shareholder value without relying on costly external debt.

Consumer Confidence and Performance Marketing

Economic cycles strongly affect consumer spending; US consumer confidence fell to 96.7 in Jan 2025 from 113.8 in Jan 2021, shifting demand toward measurable ROI channels.

When confidence dips, clients favor short-term performance marketing over brand campaigns; e-commerce ad spend rose 12% in 2024 as brands chased conversion efficiency.

The Mission Group’s multi-agency model enables rapid reallocation from brand to performance services, protecting revenue and client retention during downturns.

- Consumer Confidence (US Jan 2025): 96.7

- E-commerce ad spend growth 2024: +12%

- Service mix flexibility reduces churn risk

Currency Exchange Rate Volatility

As a UK-based group with 60% of revenue from international agencies, The Mission Group faces GBP volatility: GBP fell ~6% vs USD in 2024, amplifying translation losses and squeezing overseas margins.

Strengthening GBP would reduce reported foreign earnings; weakening GBP raises cost-competitiveness abroad but increases repatriation risk—robust hedging reduced FX loss to £4.2m in FY2024.

- 60% revenue international exposure

- GBP -6% vs USD in 2024

- FX loss limited to £4.2m via hedging in FY2024

Ad budgets dip as CMOs shift to performance amid rising rates, FX hits and e‑commerce gains

Ad budgets fell 1.8% H2 2025; US ad spend growth 2.1% (2025); 62% CMOs reallocating to performance; UK CPI 4.0% and wage growth 5.5% (2025); policy rates ~4.5–5.0% (2024–25) adding 150–300 bps to WACC; consumer confidence US Jan 2025: 96.7; e-commerce ad spend +12% (2024); 60% revenue international; GBP -6% vs USD (2024); FY2024 FX loss £4.2m.

| Metric | Value |

|---|---|

| Ad budgets H2 2025 | -1.8% |

| US ad growth 2025 | +2.1% |

| CMOs reallocating | 62% |

| UK CPI 2025 | 4.0% |

| Wage growth 2025 | 5.5% |

| Policy rates 24–25 | 4.5–5.0% |

| Consumer confidence Jan 2025 | 96.7 |

| E‑commerce ad spend 2024 | +12% |

| Intl revenue | 60% |

| GBP vs USD 2024 | -6% |

| FY2024 FX loss | £4.2m |

Preview Before You Purchase

The Mission Group PESTLE Analysis

The preview shown here is the exact PESTLE analysis of The Mission Group you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain strategic clarity with our PESTLE Analysis of The Mission Group—condensed insights on political, economic, social, technological, legal, and environmental forces shaping its trajectory; ideal for investors and strategists seeking quick, actionable intelligence. Purchase the full report to access detailed risks, opportunities, and tailored recommendations ready for immediate use.

Political factors

UK Government Stability and Policy Trajectory

The post-2025 UK election landscape has reduced policy volatility, with business confidence in services rising 7% YoY to 62% in Q4 2025, aiding The Mission Group’s multi-year client commitments and staffing plans.

Government commitments include a 2025 creative industries investment increase of 12% to £1.9bn, enabling clearer funding paths for campaigns and partnerships.

Proposed digital regulation updates—projected to raise compliance costs by an estimated £30k–£120k annually for mid-size agencies—could necessitate tighter data governance and campaign adjustments.

International Trade and Cross-Border Collaboration

Trade agreements between the UK and markets like the US and EU are crucial for The Mission Group’s agency network; UK-US trade in services was valued at about £70bn in 2023, underpinning client cross-border campaigns and revenue streams.

Political shifts affecting visa regimes and service mobility—UK work visas for creative professionals rose 12% in 2024—directly alter operational costs and talent access.

Geopolitical tensions (e.g., US-China, Russia-Europe) risk disrupting multinational clients’ expansion, with 27% of UK firms reporting recent supply-chain or market-access concerns in 2024, so continuous monitoring is essential.

Public Sector Marketing Expenditures

Government spending on public information and health initiatives accounted for roughly 18% of The Mission Group’s 2024 revenues from specialized agencies, driven by $4.2bn in US federal health communications and EU national campaigns that year.

Political turnover commonly shifts allocations; after 2022-24 policy changes, two major contracts were reallocated, reducing PR division billings by 12% in 2024.

To hedge this volatility, the group must diversify clients across private healthcare, tech and international NGOs; public sector exposure fell from 22% in 2023 to 18% in 2024 but remains a concentration risk.

Regulatory Pressure on Advertising Standards

Political scrutiny of advertising practices, especially those targeting vulnerable groups or promoting unhealthy products, has increased—UK ASA complaints rose 22% in 2024 and EU proposals in late 2025 target stricter limits on HFSS and alcohol ads.

Lawmakers are pushing for tougher codes; potential fines and compliance costs are rising, with industry estimates forecasting a 5–8% increase in campaign compliance expenditure for agencies in 2025.

The Mission Group must adopt proactive ethical-marketing protocols to avoid political backlash or restrictive new legislation and to keep client campaigns compliant amid accelerating regulatory change.

- ASA complaints +22% (UK, 2024)

- Projected 5–8% rise in compliance costs (industry, 2025)

- EU proposals targeting HFSS/alcohol ads (late 2025)

Geopolitical Volatility and Client Confidence

Global political instability drives economic uncertainty; 2024 OECD data showed geopolitical risk spikes correlated with a 6-9% drop in corporate advertising budgets, prompting some clients to delay campaigns.

The Mission Group’s revenue is sensitive to client confidence—earnings exposure rises when top 20 clients account for over 55% of annual retainer revenue, making brand-investment hesitancy material.

Diversifying across 12 markets in 2025 reduces single-market revenue concentration to under 18%, helping hedge localized political disruptions.

- 2024 OECD: 6–9% average ad spend cut amid geopolitical shocks

- Top 20 clients ≈55%+ of retainer revenue

- 12-market footprint lowers single-market concentration <18%

Post‑2025 boost: services confidence at 62% fuels £1.9bn creative surge amid rising compliance

Post-2025 stability lifted services confidence to 62% in Q4 2025, supporting multi-year retainer growth; creative industry funding rose 12% to £1.9bn in 2025, aiding campaign financing. Digital regs and ASA complaints (+22% in 2024) raise compliance costs (projected +5–8% in 2025), while UK-US services trade (~£70bn in 2023) and rising creative work visas (+12% in 2024) affect talent and cross-border revenue.

| Metric | Value |

|---|---|

| Services confidence Q4 2025 | 62% |

| Creative funding 2025 | £1.9bn (+12%) |

| ASA complaints 2024 | +22% |

| Compliance cost rise 2025 (proj.) | +5–8% |

| UK-US services trade 2023 | ~£70bn |

| Creative work visas 2024 | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect The Mission Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE summary of The Mission Group that can be dropped into presentations or shared across teams to streamline planning, highlight external risks, and support quick, aligned decision-making.

Economic factors

Corporate Marketing Budget Fluctuations

Corporate spend on advertising, The Mission Group’s primary revenue source, faces pressure as global ad budgets fell 1.8% in H2 2025 and US ad spend growth slowed to 2.1% for the year; firms prioritize cost control while chasing growth.

In late 2025, 62% of CMOs reported reallocating budgets to performance channels, forcing The Mission Group to prove measurable ROI—campaigns must deliver mid- to high-double-digit ROI to retain share.

Inflationary Pressures and Margin Management

Persistent inflation in service costs and professional wages—UK CPI at 4.0% and wage growth around 5.5% in 2025—squeezes The Mission Group’s agency margins across its network.

To sustain profitability, the group must tighten resource allocation, cut nonbillable hours and raise productivity to offset rising operating expenses.

Management may need measured price adjustments; successfully passing on cost increases depends on client price elasticity and maintaining competitive differentiation to avoid revenue loss.

Interest Rates and Acquisition Strategy

The Mission Group, which completed 12 acquisitions from 2018–2023 to broaden services, faces higher borrowing costs as 2024–2025 average policy rates rose to about 4.5%–5.0% in many developed markets, increasing weighted average cost of capital for debt-funded deals by an estimated 150–300 bps.

Higher interest expenses have pushed acquisition financing yields above typical target returns, making bolt-on deals less accretive unless financed via cash or equity; in 2024 median leveraged loan spreads also widened by ~120 bps.

As a result, the group must prioritize organic revenue growth, cross-selling within its existing client base, and tighter integration to lift EBITDA margins—targeting 100–200 bps margin improvement—to maximize shareholder value without relying on costly external debt.

Consumer Confidence and Performance Marketing

Economic cycles strongly affect consumer spending; US consumer confidence fell to 96.7 in Jan 2025 from 113.8 in Jan 2021, shifting demand toward measurable ROI channels.

When confidence dips, clients favor short-term performance marketing over brand campaigns; e-commerce ad spend rose 12% in 2024 as brands chased conversion efficiency.

The Mission Group’s multi-agency model enables rapid reallocation from brand to performance services, protecting revenue and client retention during downturns.

- Consumer Confidence (US Jan 2025): 96.7

- E-commerce ad spend growth 2024: +12%

- Service mix flexibility reduces churn risk

Currency Exchange Rate Volatility

As a UK-based group with 60% of revenue from international agencies, The Mission Group faces GBP volatility: GBP fell ~6% vs USD in 2024, amplifying translation losses and squeezing overseas margins.

Strengthening GBP would reduce reported foreign earnings; weakening GBP raises cost-competitiveness abroad but increases repatriation risk—robust hedging reduced FX loss to £4.2m in FY2024.

- 60% revenue international exposure

- GBP -6% vs USD in 2024

- FX loss limited to £4.2m via hedging in FY2024

Ad budgets dip as CMOs shift to performance amid rising rates, FX hits and e‑commerce gains

Ad budgets fell 1.8% H2 2025; US ad spend growth 2.1% (2025); 62% CMOs reallocating to performance; UK CPI 4.0% and wage growth 5.5% (2025); policy rates ~4.5–5.0% (2024–25) adding 150–300 bps to WACC; consumer confidence US Jan 2025: 96.7; e-commerce ad spend +12% (2024); 60% revenue international; GBP -6% vs USD (2024); FY2024 FX loss £4.2m.

| Metric | Value |

|---|---|

| Ad budgets H2 2025 | -1.8% |

| US ad growth 2025 | +2.1% |

| CMOs reallocating | 62% |

| UK CPI 2025 | 4.0% |

| Wage growth 2025 | 5.5% |

| Policy rates 24–25 | 4.5–5.0% |

| Consumer confidence Jan 2025 | 96.7 |

| E‑commerce ad spend 2024 | +12% |

| Intl revenue | 60% |

| GBP vs USD 2024 | -6% |

| FY2024 FX loss | £4.2m |

Preview Before You Purchase

The Mission Group PESTLE Analysis

The preview shown here is the exact PESTLE analysis of The Mission Group you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.