The Oncology Institute PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, healthcare economics, and rapid biotech innovation are shaping The Oncology Institute’s strategic outlook—our PESTLE snapshot pinpoints risks and opportunities you can act on immediately; purchase the full analysis to access the complete, editable report with data-driven recommendations for investors, advisors, and executives.

Political factors

Medicare Reimbursement Shifts

As of late 2025 the Oncology Institute remains highly sensitive to Medicare Part B and D reimbursement shifts, with Part B drug reimbursement changes affecting roughly 45% of outpatient oncology revenue and Part D influencing oral oncology access for about 30% of patients.

Federal policy is shifting toward value-based care, with CMS aiming to tie 60% of payments to quality/value models by 2027, pressuring the Institute to adapt away from fee-for-service.

Maintaining top clinical quality scores is critical: a 1% drop in quality metrics can reduce incentive payments by up to $2.5 million annually for comparable regional oncology providers, threatening financial stability.

Impact of the Inflation Reduction Act

The Inflation Reduction Act’s drug pricing provisions have enabled Medicare negotiation for select high-cost oncology drugs, projecting savings of about $100 billion through 2031 and pressuring ASP-based margins for buy-and-bill oncology practices by an estimated 10–20% in early adopter markets.

Negotiation-driven price caps and new rebate transparency rules increase administrative burden and compress gross margins, with community oncology practices reporting 12% revenue declines in sampled 2024 surveys.

Strategic responses—contract renegotiation, shift to oral or lower-cost therapies, and participation in value-based payment models—are increasingly required to sustain profitability under the IRA’s evolving procurement and rebate framework.

State Level Healthcare Regulations

Operating across 12 states, the Oncology Institute must navigate divergent Certificate of Need laws and licensure rules that can add 6–18 months to site openings and increase capex by an estimated $1.2–$3.5 million per facility.

In 2024–25, five states expanded Medicaid, raising payer mix for community clinics by 4–9% while three states added provider taxes that can reduce operating margins by 1.0–2.5 percentage points.

Continuous monitoring of state legislative sessions is essential: a 2023–24 analysis showed regulatory shifts altered projected ROI timelines for expansion projects from 3.5 to 5.2 years in affected states.

Federal Value Based Care Incentives

- APM savings targets: $500–800M; 5–10% benchmarks

- Palliative care: 20–30% fewer readmissions; 10–25% lower EOL costs

- CMS APM adoption: >40% Medicare FFS spending by 2025

- Operational need: multidisciplinary teams, data/reporting investments

Public Health Funding and Policy

Government initiatives like the 2022 Cancer Moonshot and proposed increases to the NCI budget (NCI FY2025 request ~$8.2B vs FY2022 ~$6.9B) expand community trial funding, directly increasing trial slots at The Oncology Institute.

Political shifts in NCI appropriations can quickly raise or cut local research participation; a 10-15% boost in grants historically translated to proportional upticks in community-site enrollment.

The Institute uses these policies to deliver academic-level therapies locally, enrolling patients in targeted therapy and immunotherapy trials otherwise limited to major centers.

- Cancer Moonshot and FY2025 NCI request ~8.2B boost community trial capacity

- 10–15% grant changes correlate with enrollment swings

- Enables access to targeted and immunotherapy trials at community sites

Medicare, IRA, regs squeeze margins & access; NCI boosts community trials with $8.2B

Medicare Part B/D reimbursement shifts threaten ~45% outpatient and ~30% oral access; CMS value‑based targets (60% by 2027) and APMs (>40% FFS by 2025) force care redesign; IRA drug negotiation compresses buy‑and‑bill margins ~10–20%; state CON/licensure adds 6–18 months and $1.2–3.5M capex; NCI FY2025 request ~$8.2B ups community trial slots.

| Factor | Metric |

|---|---|

| Medicare impact | 45% outpatient; 30% oral |

| Value‑based targets | 60% by 2027; >40% APMs 2025 |

| IRA effect | 10–20% margin pressure |

| State regs | 6–18 mo; $1.2–3.5M |

| NCI funding | $8.2B FY2025 |

What is included in the product

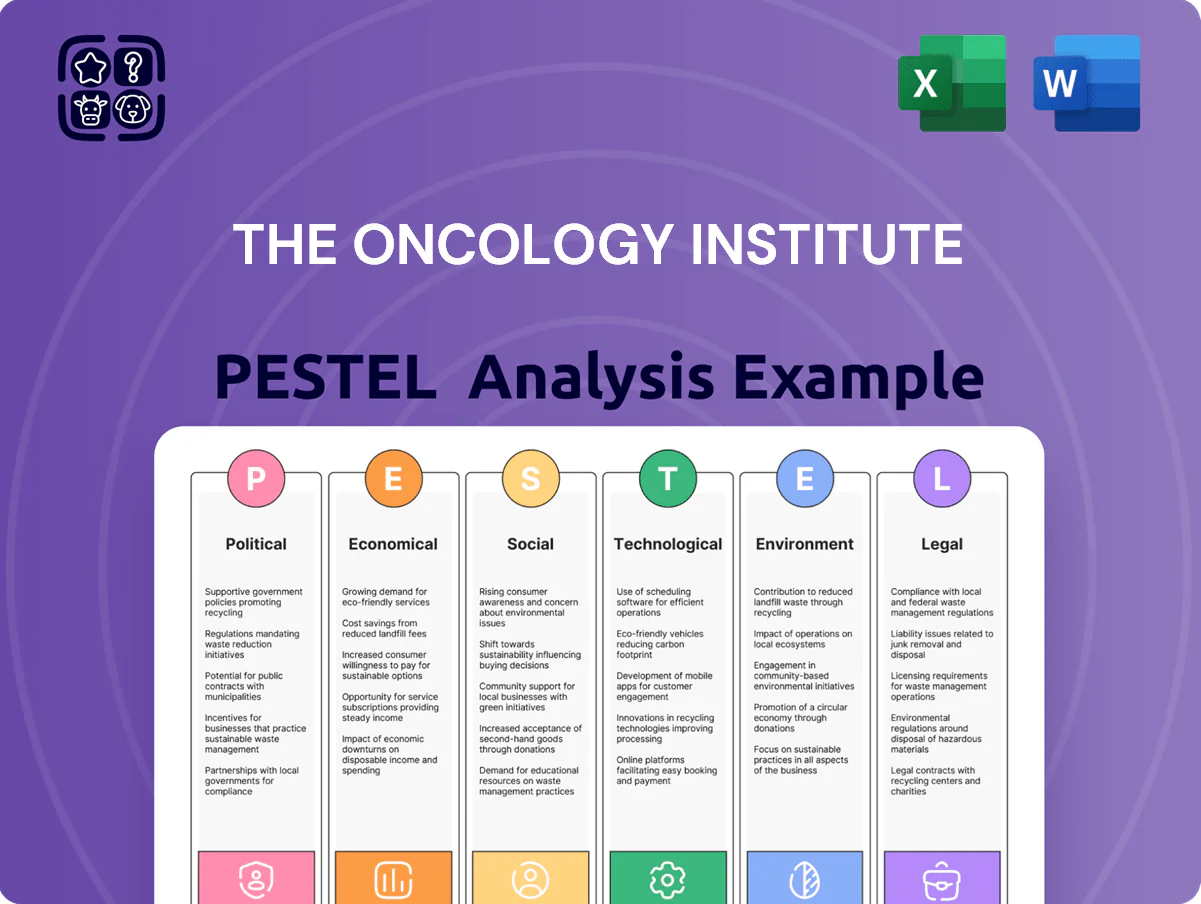

Explores how external macro-environmental factors uniquely affect The Oncology Institute across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trend analysis to identify risks and opportunities.

A concise, visually segmented PESTLE summary for The Oncology Institute that eases stakeholder alignment, supports risk discussions in planning sessions, and can be dropped into presentations or shared across teams for quick decision-making.

Economic factors

Rising Labor and Staffing Costs

The healthcare sector saw average wage growth for registered nurses hit about 6.5% year-over-year in 2024, with oncology-specialized roles commanding 8–12% premiums versus general nurses; physician compensation for oncologists rose ~7% in 2024 as demand outpaced supply.

Competition between community practices and hospital systems increased recruitment costs—median hiring expenses for specialty clinicians rose roughly 20% in 2024—and turnover-related replacement costs can exceed $100,000 per physician.

The Oncology Institute must optimize staffing models, leverage tele-oncology and advanced practice providers, and reduce agency reliance to contain a projected 2025 labor-cost pressure of 5–9% on operating margins.

Oncology Drug Price Inflation

The list prices for novel biologics and immunotherapies rose an average of 7–10% annually from 2019–2024, outpacing US CPI inflation of ~3% in 2023–2024; CAR-T therapies routinely cost $400k–$500k per treatment. Managing inventory and financing these agents ties up working capital—community oncology practices report drug-related days payable outstanding increasing by 15–25% and margin pressure with buy-and-bill reimbursement lagging. Economic volatility in active pharmaceutical ingredient supply and distribution pushed oncology drug shortages to 10–15% of essential SKUs in 2023, necessitating hedging, multi-supplier contracts, and consignment or 340B strategies to preserve patient access.

Interest Rates and Capital Access

By end-2025 US benchmark rates stabilized around 5.25% after Fed pauses, yet effective borrowing costs for healthcare projects average 6.0–7.5% for mid-market lenders, keeping capital expensive for The Oncology Institute.

Opening a new clinic or upgrading linear accelerators typically requires $5–12M per site; high borrowing costs plus supply-chain inflation can extend payback periods beyond 6–8 years.

Consequently, elevated capital costs may slow acquisitions and facility development unless internal cash flow is optimized or alternative financing (tax-exempt bonds, equipment leases, joint ventures) is pursued aggressively.

Transition to Value Based Payment

The shift to value-based payment puts The Oncology Institute at increased financial risk by tying reimbursement to total cost and outcomes; Medicare Oncology Care Model reported average savings of 9.5% in 2020, illustrating potential upside.

To succeed, the Institute must deploy advanced analytics—AI-driven care pathways and predictive risk stratification reduced readmissions by ~12% in 2023 across oncology pilots.

Failure to control costs could compress margins as bundled-payment oncology pilots show per-patient cost variance of ±18%.

- Requires investment in analytics and care management

- Potential savings ~5–10% annually based on OCM/2020–2023 data

- Increased downside risk: cost variance up to 18%

Consumer Disposable Income Trends

Economic downturns cut US real disposable personal income by 1.2% in 2023 and wage growth lagged inflation into 2024, reducing patients' ability to pay for elective supportive oncology care and increasing treatment deferment.

High-deductible plans cover 55% of workers in 2024, raising out-of-pocket exposure and contributing to higher bad-debt write-offs for providers.

The Institute should expand financial counseling, income-based payment plans, and charity care to maintain access during economic stress.

- 2023 US real disposable income -1.2%

- 55% workers in high-deductible plans (2024)

- Measures: financial counseling, income-based plans, charity care

Margins Squeezed: Rising Wages, Drug Costs & Capex Strain Oncology Care

Rising labor and drug costs squeezed margins in 2024–2025: RN wages +6.5% (oncology premium 8–12%), oncologist pay +7%, novel therapy list prices +7–10% annually; CAR-T $400k–$500k. Capital remains costly—borrow rates ~6–7.5% and site buildouts $5–12M delaying expansions. Value-based payment shifts create both 5–10% savings upside and ±18% cost variance risk; 55% workers had high-deductible plans in 2024.

| Metric | 2024–25 |

|---|---|

| RN wage growth | +6.5% |

| Oncologist pay | +7% |

| Drug price growth | +7–10% |

| CAR-T cost | $400k–$500k |

| Borrowing cost | 6.0–7.5% |

| Site capex | $5–12M |

| High-deductible coverage | 55% |

| Value-based savings | ~5–10% |

| Cost variance | ±18% |

Full Version Awaits

The Oncology Institute PESTLE Analysis

The preview shown here is the exact Oncology Institute PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and depth visible now match the final download with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Uncover how political shifts, healthcare economics, and rapid biotech innovation are shaping The Oncology Institute’s strategic outlook—our PESTLE snapshot pinpoints risks and opportunities you can act on immediately; purchase the full analysis to access the complete, editable report with data-driven recommendations for investors, advisors, and executives.

Political factors

Medicare Reimbursement Shifts

As of late 2025 the Oncology Institute remains highly sensitive to Medicare Part B and D reimbursement shifts, with Part B drug reimbursement changes affecting roughly 45% of outpatient oncology revenue and Part D influencing oral oncology access for about 30% of patients.

Federal policy is shifting toward value-based care, with CMS aiming to tie 60% of payments to quality/value models by 2027, pressuring the Institute to adapt away from fee-for-service.

Maintaining top clinical quality scores is critical: a 1% drop in quality metrics can reduce incentive payments by up to $2.5 million annually for comparable regional oncology providers, threatening financial stability.

Impact of the Inflation Reduction Act

The Inflation Reduction Act’s drug pricing provisions have enabled Medicare negotiation for select high-cost oncology drugs, projecting savings of about $100 billion through 2031 and pressuring ASP-based margins for buy-and-bill oncology practices by an estimated 10–20% in early adopter markets.

Negotiation-driven price caps and new rebate transparency rules increase administrative burden and compress gross margins, with community oncology practices reporting 12% revenue declines in sampled 2024 surveys.

Strategic responses—contract renegotiation, shift to oral or lower-cost therapies, and participation in value-based payment models—are increasingly required to sustain profitability under the IRA’s evolving procurement and rebate framework.

State Level Healthcare Regulations

Operating across 12 states, the Oncology Institute must navigate divergent Certificate of Need laws and licensure rules that can add 6–18 months to site openings and increase capex by an estimated $1.2–$3.5 million per facility.

In 2024–25, five states expanded Medicaid, raising payer mix for community clinics by 4–9% while three states added provider taxes that can reduce operating margins by 1.0–2.5 percentage points.

Continuous monitoring of state legislative sessions is essential: a 2023–24 analysis showed regulatory shifts altered projected ROI timelines for expansion projects from 3.5 to 5.2 years in affected states.

Federal Value Based Care Incentives

- APM savings targets: $500–800M; 5–10% benchmarks

- Palliative care: 20–30% fewer readmissions; 10–25% lower EOL costs

- CMS APM adoption: >40% Medicare FFS spending by 2025

- Operational need: multidisciplinary teams, data/reporting investments

Public Health Funding and Policy

Government initiatives like the 2022 Cancer Moonshot and proposed increases to the NCI budget (NCI FY2025 request ~$8.2B vs FY2022 ~$6.9B) expand community trial funding, directly increasing trial slots at The Oncology Institute.

Political shifts in NCI appropriations can quickly raise or cut local research participation; a 10-15% boost in grants historically translated to proportional upticks in community-site enrollment.

The Institute uses these policies to deliver academic-level therapies locally, enrolling patients in targeted therapy and immunotherapy trials otherwise limited to major centers.

- Cancer Moonshot and FY2025 NCI request ~8.2B boost community trial capacity

- 10–15% grant changes correlate with enrollment swings

- Enables access to targeted and immunotherapy trials at community sites

Medicare, IRA, regs squeeze margins & access; NCI boosts community trials with $8.2B

Medicare Part B/D reimbursement shifts threaten ~45% outpatient and ~30% oral access; CMS value‑based targets (60% by 2027) and APMs (>40% FFS by 2025) force care redesign; IRA drug negotiation compresses buy‑and‑bill margins ~10–20%; state CON/licensure adds 6–18 months and $1.2–3.5M capex; NCI FY2025 request ~$8.2B ups community trial slots.

| Factor | Metric |

|---|---|

| Medicare impact | 45% outpatient; 30% oral |

| Value‑based targets | 60% by 2027; >40% APMs 2025 |

| IRA effect | 10–20% margin pressure |

| State regs | 6–18 mo; $1.2–3.5M |

| NCI funding | $8.2B FY2025 |

What is included in the product

Explores how external macro-environmental factors uniquely affect The Oncology Institute across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trend analysis to identify risks and opportunities.

A concise, visually segmented PESTLE summary for The Oncology Institute that eases stakeholder alignment, supports risk discussions in planning sessions, and can be dropped into presentations or shared across teams for quick decision-making.

Economic factors

Rising Labor and Staffing Costs

The healthcare sector saw average wage growth for registered nurses hit about 6.5% year-over-year in 2024, with oncology-specialized roles commanding 8–12% premiums versus general nurses; physician compensation for oncologists rose ~7% in 2024 as demand outpaced supply.

Competition between community practices and hospital systems increased recruitment costs—median hiring expenses for specialty clinicians rose roughly 20% in 2024—and turnover-related replacement costs can exceed $100,000 per physician.

The Oncology Institute must optimize staffing models, leverage tele-oncology and advanced practice providers, and reduce agency reliance to contain a projected 2025 labor-cost pressure of 5–9% on operating margins.

Oncology Drug Price Inflation

The list prices for novel biologics and immunotherapies rose an average of 7–10% annually from 2019–2024, outpacing US CPI inflation of ~3% in 2023–2024; CAR-T therapies routinely cost $400k–$500k per treatment. Managing inventory and financing these agents ties up working capital—community oncology practices report drug-related days payable outstanding increasing by 15–25% and margin pressure with buy-and-bill reimbursement lagging. Economic volatility in active pharmaceutical ingredient supply and distribution pushed oncology drug shortages to 10–15% of essential SKUs in 2023, necessitating hedging, multi-supplier contracts, and consignment or 340B strategies to preserve patient access.

Interest Rates and Capital Access

By end-2025 US benchmark rates stabilized around 5.25% after Fed pauses, yet effective borrowing costs for healthcare projects average 6.0–7.5% for mid-market lenders, keeping capital expensive for The Oncology Institute.

Opening a new clinic or upgrading linear accelerators typically requires $5–12M per site; high borrowing costs plus supply-chain inflation can extend payback periods beyond 6–8 years.

Consequently, elevated capital costs may slow acquisitions and facility development unless internal cash flow is optimized or alternative financing (tax-exempt bonds, equipment leases, joint ventures) is pursued aggressively.

Transition to Value Based Payment

The shift to value-based payment puts The Oncology Institute at increased financial risk by tying reimbursement to total cost and outcomes; Medicare Oncology Care Model reported average savings of 9.5% in 2020, illustrating potential upside.

To succeed, the Institute must deploy advanced analytics—AI-driven care pathways and predictive risk stratification reduced readmissions by ~12% in 2023 across oncology pilots.

Failure to control costs could compress margins as bundled-payment oncology pilots show per-patient cost variance of ±18%.

- Requires investment in analytics and care management

- Potential savings ~5–10% annually based on OCM/2020–2023 data

- Increased downside risk: cost variance up to 18%

Consumer Disposable Income Trends

Economic downturns cut US real disposable personal income by 1.2% in 2023 and wage growth lagged inflation into 2024, reducing patients' ability to pay for elective supportive oncology care and increasing treatment deferment.

High-deductible plans cover 55% of workers in 2024, raising out-of-pocket exposure and contributing to higher bad-debt write-offs for providers.

The Institute should expand financial counseling, income-based payment plans, and charity care to maintain access during economic stress.

- 2023 US real disposable income -1.2%

- 55% workers in high-deductible plans (2024)

- Measures: financial counseling, income-based plans, charity care

Margins Squeezed: Rising Wages, Drug Costs & Capex Strain Oncology Care

Rising labor and drug costs squeezed margins in 2024–2025: RN wages +6.5% (oncology premium 8–12%), oncologist pay +7%, novel therapy list prices +7–10% annually; CAR-T $400k–$500k. Capital remains costly—borrow rates ~6–7.5% and site buildouts $5–12M delaying expansions. Value-based payment shifts create both 5–10% savings upside and ±18% cost variance risk; 55% workers had high-deductible plans in 2024.

| Metric | 2024–25 |

|---|---|

| RN wage growth | +6.5% |

| Oncologist pay | +7% |

| Drug price growth | +7–10% |

| CAR-T cost | $400k–$500k |

| Borrowing cost | 6.0–7.5% |

| Site capex | $5–12M |

| High-deductible coverage | 55% |

| Value-based savings | ~5–10% |

| Cost variance | ±18% |

Full Version Awaits

The Oncology Institute PESTLE Analysis

The preview shown here is the exact Oncology Institute PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and depth visible now match the final download with no placeholders or surprises.