Third Federal Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

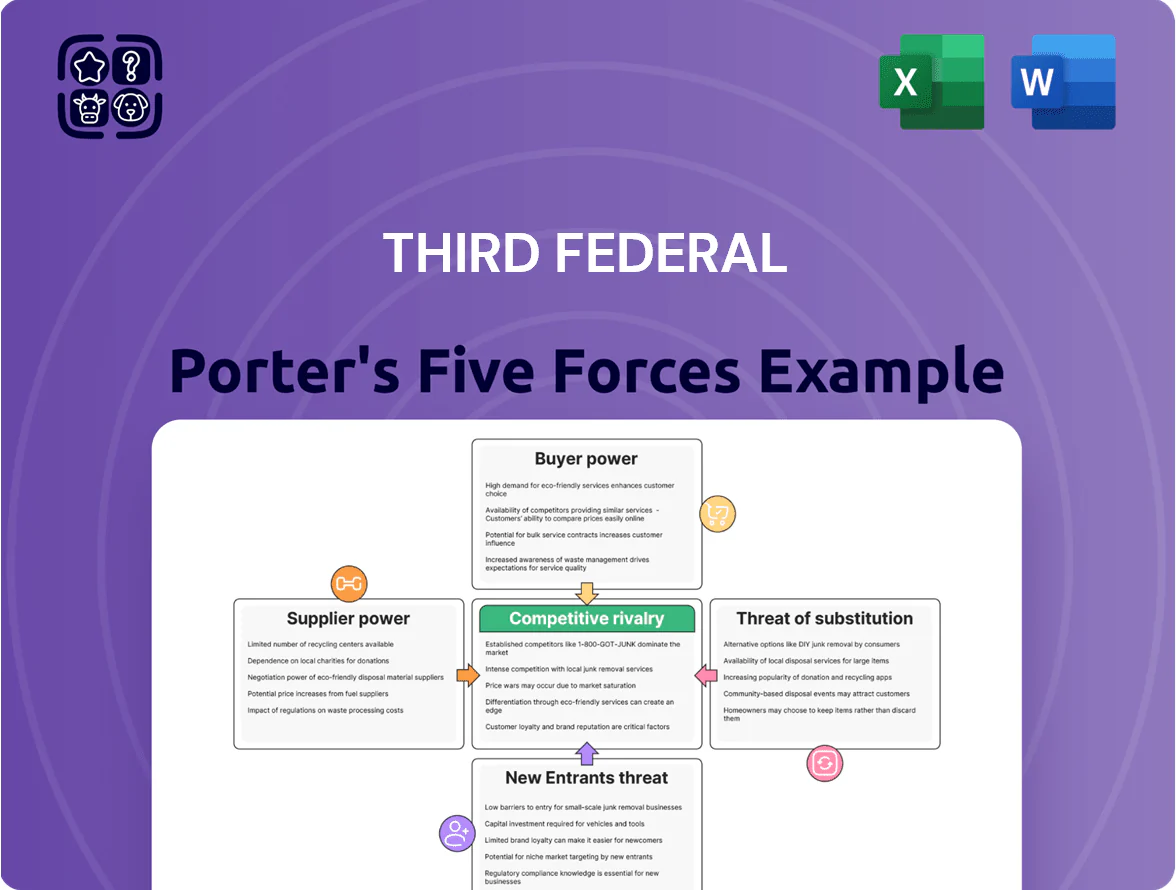

Third Federal faces intense buyer pressure from rate-sensitive savers and moderate threat from digital-first challengers, while regulatory and funding constraints shape its supplier dynamics and competitive moat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Third Federal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cost of retail deposits

Individual depositors are Third Federal's main capital suppliers; by Q4 2025 retail deposits made up about 78% of funding, so their bargaining power rose as interest rates stabilized late 2025 and savers sought higher yields.

To hold liquidity Third Federal must raise rates on CDs and savings: in 2025 the bank's average savings yield climbed toward 1.85% while top 1-year CD market rates hit ~4.5%, forcing competitive repricing to retain funds.

Dependence on fintech providers

Labor market for financial experts

The supply of skilled loan officers and compliance professionals is tight; US Bureau of Labor Statistics data show a 5.8% wage growth for financial specialists in 2024 and a 3.6% shortage rate in mortgage roles, raising hiring costs for Third Federal.

High demand lets employees negotiate higher pay and benefits—median loan officer pay rose to $68,000 in 2024—so Third Federal must match market offers to retain staff.

Investing in training, retention bonuses, and tech tools reduces turnover risk; losing talent to JPMorgan Chase or fintechs like Rocket Mortgage would raise operational and compliance costs.

Access to wholesale funding

The Federal Home Loan Bank and other wholesale credit providers act as essential backup liquidity for Third Federal, and a 100 bp Fed tightening in 2022–23 showed how quickly wholesale costs can rise; by end-2025 FHFA data indicate FHLB advances still fund ~15–25% of mortgage pipeline needs for comparable midsize thrifts.

Shifts in Fed policy or FHLB lending criteria can abruptly raise funding costs or restrict access, increasing hedging and pipeline breakage risk; Third Federal must price pipelines to cover potential wholesale basis wideners.

- FHLB advances ~15–25% of pipeline funding (industry mid-2025)

- 100 bp Fed moves historically raise wholesale spreads 20–60 bps

- Wholesale access is a critical backstop for mortgage pipeline management

Regulatory compliance services

External auditors and legal consultants supply the specialized compliance frameworks Third Federal needs to meet federal mortgage rules; in 2024, regulatory enforcement actions in banking rose 18%, raising the cost of non-compliance materially.

Their bargaining power is high because few firms combine banking law, mortgage servicing, and audit expertise, so fees and contract terms skew toward providers—average hourly rates for top compliance lawyers exceeded $650 in 2024.

Third Federal must sustain these relationships to manage risks: a single enforcement fine can exceed $10 million and harm reputation and capital ratios.

- High supplier power: niche expertise, limited vendors

- 2024: enforcement actions +18%

- Top compliance lawyer rates ~ $650/hr

- Single fine risk > $10M

Supplier squeeze: deposits, FHLB & rising vendor/labor costs tighten margins

Suppliers exert high power: retail deposits funded ~78% of Third Federal by Q4 2025, pushing CD/savings repricing (avg savings ~1.85%, top 1‑yr CD ~4.5%) while FHLB advances covered ~15–25% of mortgage pipelines; fintech/platform vendors and niche compliance firms (top lawyer rates ~$650/hr) and tight labor (loan officer median pay $68k, 5.8% wage growth 2024) raise costs and switching risk.

| Supplier | Key metric | 2024–25 data |

|---|---|---|

| Retail deposits | Share of funding | ~78% (Q4 2025) |

| Savings/CDs | Yields | Avg savings ~1.85%; top 1‑yr CD ~4.5% (2025) |

| FHLB | Pipeline funding | ~15–25% (mid‑2025) |

| Fintech vendors | Global infra spend | ~$150B (2025) |

| Compliance/legal | Top lawyer rates | ~$650/hr (2024) |

| Labor | Loan officer pay | Median $68k; 5.8% wage growth (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Third Federal that uncovers competitive drivers, buyer and supplier power, barriers to entry, and substitution risks to inform strategic positioning and protect market share.

Quickly assess Third Federal's competitive dynamics with a one-sheet Porter’s Five Forces summary—ideal for swift boardroom decisions and investor memos.

Customers Bargaining Power

Mortgage rate sensitivity

Borrowers in 2025 react sharply to small APR moves: a 25-basis-point rise cut application rates industry-wide by ~8% in 2024–25, so Third Federal faces acute sensitivity.

Mortgages are standardized and online comparison sites list rates from 60+ national and regional lenders, raising price transparency and switching probability.

This forces Third Federal to keep net interest margins tight—its 2024 mortgage NIM near 1.6% vs. regional peers at ~1.9% to retain high-quality borrowers.

Low switching costs for savers

The rise of digital banking makes switching savings accounts near effortless: 85% of US consumers used mobile banking in 2024, and 62% switched at least one account for a better rate, so savers can move large sums in minutes. That mobility forces Third Federal Savings and Loan Association to match market-leading yields—its 2025 jumbo and regular savings rates must stay within ~20–50 bps of top online banks—and to invest in service and UX to reduce attrition.

Information transparency

Online comparison tools and aggregators (e.g., NerdWallet, Bankrate) give consumers real-time rates and fees; as of 2024, 42% of US mortgage shoppers used comparison sites at application, raising negotiation leverage. Customers now enter talks armed with market averages—30-year mortgage mean rates and APR spreads—reducing banks’ historical information asymmetry and increasing downward pressure on margins.

Demand for digital integration

- 72% under-35 prefer strong mobile features (2024)

- Digital-first lenders +14% share in 2023 first-time mortgages

- Retention hinges on seamless mortgage/savings integration

Refinancing flexibility

- Refi sensitivity: 38% jump in 2024 refi apps

- Switching friction: avg app 48 minutes (2025)

- Retention levers: price, speed, relationship management

Rate sensitivity, tight NIMs, mobile-first customers force fast pricing & UX

High price transparency and low switching costs give customers strong bargaining power: a 25-bp APR rise cut applications ~8% (2024–25) and 2024 mortgage NIM for Third Federal was ~1.6% vs peers ~1.9%, forcing tight pricing, fast decisions, and better UX; 85% used mobile banking (2024), 62% switched accounts, and refi apps rose 38% when 30-yr <6% (2024).

| Metric | Value |

|---|---|

| APR 25-bp impact | -8% apps |

| Third Fed mortgage NIM (2024) | ~1.6% |

| Regional peer NIM | ~1.9% |

| Mobile banking users (2024) | 85% |

| Account switchers (2024) | 62% |

| Refi app rise (30-yr <6%, 2024) | +38% |

Full Version Awaits

Third Federal Porter's Five Forces Analysis

This preview shows the exact Third Federal Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file and will be available for instant download the moment you buy.

You're viewing the final deliverable: ready to use for decision-making, reporting, or presentation without further setup.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Third Federal faces intense buyer pressure from rate-sensitive savers and moderate threat from digital-first challengers, while regulatory and funding constraints shape its supplier dynamics and competitive moat.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Third Federal’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cost of retail deposits

Individual depositors are Third Federal's main capital suppliers; by Q4 2025 retail deposits made up about 78% of funding, so their bargaining power rose as interest rates stabilized late 2025 and savers sought higher yields.

To hold liquidity Third Federal must raise rates on CDs and savings: in 2025 the bank's average savings yield climbed toward 1.85% while top 1-year CD market rates hit ~4.5%, forcing competitive repricing to retain funds.

Dependence on fintech providers

Labor market for financial experts

The supply of skilled loan officers and compliance professionals is tight; US Bureau of Labor Statistics data show a 5.8% wage growth for financial specialists in 2024 and a 3.6% shortage rate in mortgage roles, raising hiring costs for Third Federal.

High demand lets employees negotiate higher pay and benefits—median loan officer pay rose to $68,000 in 2024—so Third Federal must match market offers to retain staff.

Investing in training, retention bonuses, and tech tools reduces turnover risk; losing talent to JPMorgan Chase or fintechs like Rocket Mortgage would raise operational and compliance costs.

Access to wholesale funding

The Federal Home Loan Bank and other wholesale credit providers act as essential backup liquidity for Third Federal, and a 100 bp Fed tightening in 2022–23 showed how quickly wholesale costs can rise; by end-2025 FHFA data indicate FHLB advances still fund ~15–25% of mortgage pipeline needs for comparable midsize thrifts.

Shifts in Fed policy or FHLB lending criteria can abruptly raise funding costs or restrict access, increasing hedging and pipeline breakage risk; Third Federal must price pipelines to cover potential wholesale basis wideners.

- FHLB advances ~15–25% of pipeline funding (industry mid-2025)

- 100 bp Fed moves historically raise wholesale spreads 20–60 bps

- Wholesale access is a critical backstop for mortgage pipeline management

Regulatory compliance services

External auditors and legal consultants supply the specialized compliance frameworks Third Federal needs to meet federal mortgage rules; in 2024, regulatory enforcement actions in banking rose 18%, raising the cost of non-compliance materially.

Their bargaining power is high because few firms combine banking law, mortgage servicing, and audit expertise, so fees and contract terms skew toward providers—average hourly rates for top compliance lawyers exceeded $650 in 2024.

Third Federal must sustain these relationships to manage risks: a single enforcement fine can exceed $10 million and harm reputation and capital ratios.

- High supplier power: niche expertise, limited vendors

- 2024: enforcement actions +18%

- Top compliance lawyer rates ~ $650/hr

- Single fine risk > $10M

Supplier squeeze: deposits, FHLB & rising vendor/labor costs tighten margins

Suppliers exert high power: retail deposits funded ~78% of Third Federal by Q4 2025, pushing CD/savings repricing (avg savings ~1.85%, top 1‑yr CD ~4.5%) while FHLB advances covered ~15–25% of mortgage pipelines; fintech/platform vendors and niche compliance firms (top lawyer rates ~$650/hr) and tight labor (loan officer median pay $68k, 5.8% wage growth 2024) raise costs and switching risk.

| Supplier | Key metric | 2024–25 data |

|---|---|---|

| Retail deposits | Share of funding | ~78% (Q4 2025) |

| Savings/CDs | Yields | Avg savings ~1.85%; top 1‑yr CD ~4.5% (2025) |

| FHLB | Pipeline funding | ~15–25% (mid‑2025) |

| Fintech vendors | Global infra spend | ~$150B (2025) |

| Compliance/legal | Top lawyer rates | ~$650/hr (2024) |

| Labor | Loan officer pay | Median $68k; 5.8% wage growth (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Third Federal that uncovers competitive drivers, buyer and supplier power, barriers to entry, and substitution risks to inform strategic positioning and protect market share.

Quickly assess Third Federal's competitive dynamics with a one-sheet Porter’s Five Forces summary—ideal for swift boardroom decisions and investor memos.

Customers Bargaining Power

Mortgage rate sensitivity

Borrowers in 2025 react sharply to small APR moves: a 25-basis-point rise cut application rates industry-wide by ~8% in 2024–25, so Third Federal faces acute sensitivity.

Mortgages are standardized and online comparison sites list rates from 60+ national and regional lenders, raising price transparency and switching probability.

This forces Third Federal to keep net interest margins tight—its 2024 mortgage NIM near 1.6% vs. regional peers at ~1.9% to retain high-quality borrowers.

Low switching costs for savers

The rise of digital banking makes switching savings accounts near effortless: 85% of US consumers used mobile banking in 2024, and 62% switched at least one account for a better rate, so savers can move large sums in minutes. That mobility forces Third Federal Savings and Loan Association to match market-leading yields—its 2025 jumbo and regular savings rates must stay within ~20–50 bps of top online banks—and to invest in service and UX to reduce attrition.

Information transparency

Online comparison tools and aggregators (e.g., NerdWallet, Bankrate) give consumers real-time rates and fees; as of 2024, 42% of US mortgage shoppers used comparison sites at application, raising negotiation leverage. Customers now enter talks armed with market averages—30-year mortgage mean rates and APR spreads—reducing banks’ historical information asymmetry and increasing downward pressure on margins.

Demand for digital integration

- 72% under-35 prefer strong mobile features (2024)

- Digital-first lenders +14% share in 2023 first-time mortgages

- Retention hinges on seamless mortgage/savings integration

Refinancing flexibility

- Refi sensitivity: 38% jump in 2024 refi apps

- Switching friction: avg app 48 minutes (2025)

- Retention levers: price, speed, relationship management

Rate sensitivity, tight NIMs, mobile-first customers force fast pricing & UX

High price transparency and low switching costs give customers strong bargaining power: a 25-bp APR rise cut applications ~8% (2024–25) and 2024 mortgage NIM for Third Federal was ~1.6% vs peers ~1.9%, forcing tight pricing, fast decisions, and better UX; 85% used mobile banking (2024), 62% switched accounts, and refi apps rose 38% when 30-yr <6% (2024).

| Metric | Value |

|---|---|

| APR 25-bp impact | -8% apps |

| Third Fed mortgage NIM (2024) | ~1.6% |

| Regional peer NIM | ~1.9% |

| Mobile banking users (2024) | 85% |

| Account switchers (2024) | 62% |

| Refi app rise (30-yr <6%, 2024) | +38% |

Full Version Awaits

Third Federal Porter's Five Forces Analysis

This preview shows the exact Third Federal Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file and will be available for instant download the moment you buy.

You're viewing the final deliverable: ready to use for decision-making, reporting, or presentation without further setup.