Third Federal PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and regulatory trends are shaping Third Federal’s prospects with our concise PESTLE snapshot—then unlock the full analysis for deep, actionable insights tailored to investors and strategists; purchase now to get the complete, editable report and make smarter decisions faster.

Political factors

Federal Housing Policy Mandates

The political environment at end-2025 is driven by federal initiatives to boost affordability for first-time buyers, including a $10B down payment assistance expansion and proposed tax credits up to $5,000 per eligible purchase that Third Federal must consider in product design.

Third Federal should align mortgage products to leverage subsidies targeting low-to-moderate income lending, where HUD-backed programs grew 12% YoY in 2024–25, to capture subsidized origination volume.

Leadership changes at HUD/FHA can swiftly alter underwriting rules; Third Federal must maintain agile credit policy processes to implement revised debt-to-income or documentation standards within regulatory timelines.

GSE Reform and Privatization Debates

Ongoing political debates over GSE reform and potential privatization of Fannie Mae and Freddie Mac create uncertainty in the secondary mortgage market, with proposals in 2024–25 suggesting changes to guarantee fee structures that could shift funding costs for originators.

Third Federal, which held $24.1 billion in residential mortgage loans and generated a 2024 net interest margin sensitive to secondary-market pricing, is exposed to policy-driven swings in guarantee fees and MBS availability.

Legislative discussions about higher capital requirements for GSEs—estimates in 2025 ranged from an additional $50–150 billion industry-wide—would affect liquidity, tighten spreads, and force private savings and loans to revise pricing and portfolio strategies.

Tax Policy and Mortgage Incentives

Legislative changes to mortgage interest deductions and the $10,000 SALT cap have reduced demand for pricier homes; a 2023 Urban-Brookings Tax Policy Center analysis estimated SALT cap effects lowered high-value housing prices by up to 8% in high-tax states like Florida counties with net in-migration.

Shifts in federal proposals in 2024–25 to expand or roll back mortgage incentives could increase origination volumes; FHFA data show Ohio and Florida saw 2023–24 mortgage originations of roughly $45B and $210B respectively, making Third Federal's Ohio–Florida customer behavior sensitive to tax changes.

The bank must track tax reform bills and the Congressional calendar to advise clients and update stress tests; scenario modeling should incorporate 5–10% swings in demand tied to deduction policy shifts and adjust long-term portfolio growth projections accordingly.

Regional Political Stability

Third Federal's lending is concentrated in 12 metropolitan hubs where municipal projects boosted nearby property values by an average 7.8% in 2024, directly increasing collateral values and loan demand.

Local zoning changes and pro-housing ordinances in 5 key jurisdictions expanded developable lots by 14% in 2023–24, enlarging the bank's mortgage pipeline but also raising regulatory complexity.

Active engagement with city councils and planning departments—reflected in 18 stakeholder meetings and three public-private partnerships in 2024—helped secure lending volume and preserve a 3.2% market-share gain in core markets.

- 12 metro hubs; +7.8% local property value growth (2024)

- 5 jurisdictions with pro-housing zoning changes; +14% developable lots (2023–24)

- 18 stakeholder meetings; 3 PPPs in 2024; +3.2% market share

Trade Policies and Construction Costs

- Tariff-driven material cost rise: +8–12% (2021–2025)

- Added construction cost per home: ~$15k–$25k

- New mortgage applications change: −7% YoY

- Third Federal action: monitoring trade/tariff risk to adjust construction loan exposure

Policy shifts, tariffs, and HUD volatility threaten Third Federal loan demand and pricing

Political shifts through 2025—expanded $10B down‑payment aid, proposed $5k tax credits, GSE reform debates, tariff-driven construction cost rises of 8–12%, and HUD rule volatility—create origination and pricing risk for Third Federal (residential loans $24.1B; NIM sensitivity); monitor policy calendar and model 5–10% demand swings and guarantee‑fee impacts.

| Metric | Value |

|---|---|

| Residential loans | $24.1B |

| Tariff cost rise | 8–12% |

| Demand swing modeled | 5–10% |

What is included in the product

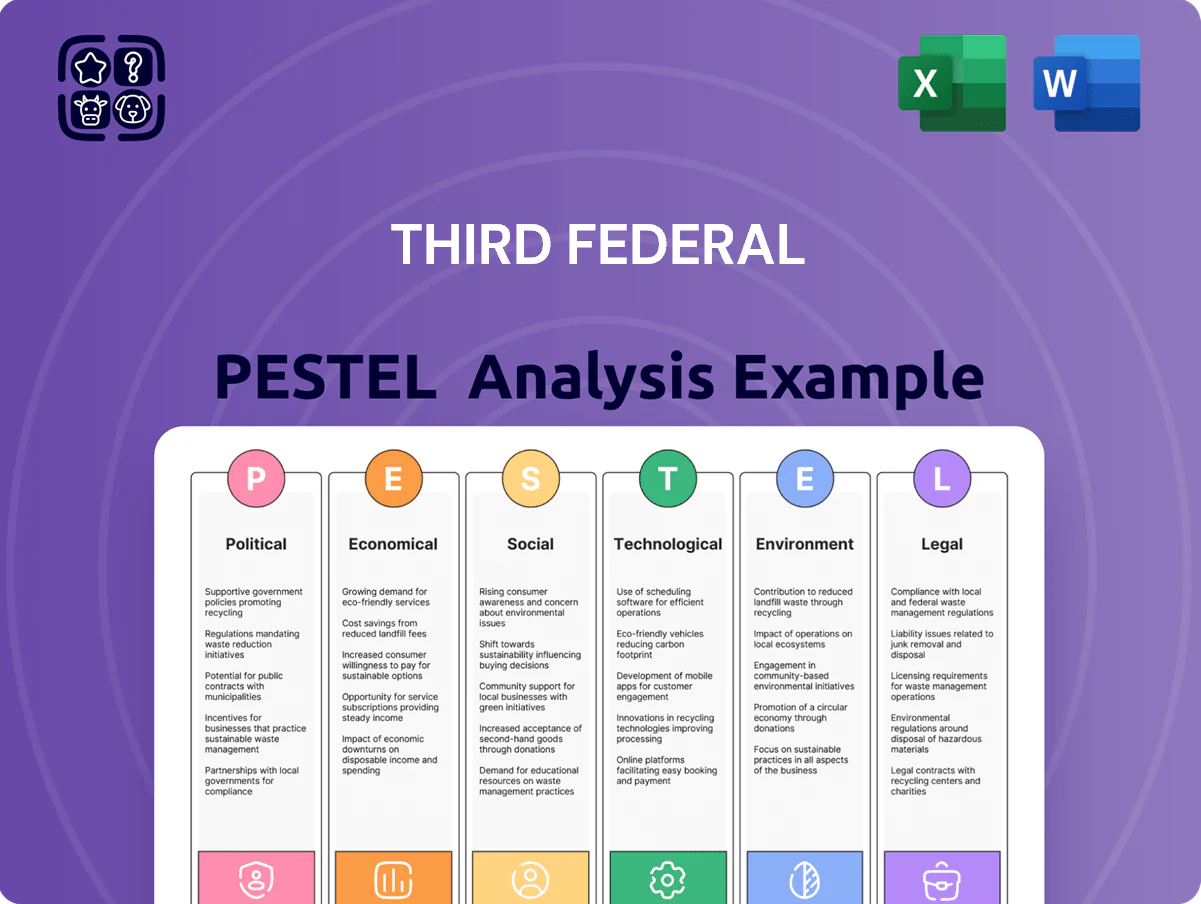

Explores how external macro-environmental factors uniquely affect Third Federal across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and forward-looking insights to support scenario planning.

Condenses the full Third Federal PESTLE into a clear, shareable summary that’s visually segmented by category for quick interpretation during meetings or presentations.

Economic factors

Interest Rate Environment

The Federal Reserve's policy remains the primary driver of Third Federal's net interest margin into late 2025; the fed funds rate held at 5.25–5.50% in 2024–2025 pressure margins on mortgage lenders.

As rates stabilize or oscillate, Third Federal must manage the spread between deposit costs (average savings yield ~1.2% in 2024) and mortgage yields (30-year fixed avg ~6.8% in 2025).

Volatile rates demand advanced asset-liability management—hedging, duration matching, and liquidity buffers—to protect capital ratios and preserve profitability amid margin compression risks.

Housing Market Inventory Levels

Inflationary Pressures on Operating Costs

Persistent inflation through 2025 pushed U.S. CPI to about 3.4% year-on-year in 2025, raising Third Federal’s wages, IT maintenance and branch upkeep costs—industry wage growth averaged ~4–6% in 2024–25, increasing operating expenses materially.

Third Federal must absorb higher costs while avoiding fee hikes to protect its low-cost brand; passing fees risks deposit outflows, given regional peers saw deposit betas of 20–40% in 2024.

Efficiency ratios remain pressured—banking industry median efficiency was ~55% in 2024—forcing Third Federal to prioritize process automation, branch rationalization and cost-effective digital delivery to restore margins.

Employment and Consumer Income Trends

The Midwest unemployment fell to 3.4% in 2025 while Florida averaged 2.9%—strong labor markets that support mortgage repayment capacity for Third Federal borrowers.

Shifts to remote work and manufacturing slowdowns can raise local unemployment; a 1% regional unemployment rise historically increases 30+ day delinquencies by ~0.2–0.4 percentage points.

Third Federal monitors county-level employment and wage data to adjust underwriting and offer loss-mitigation for at-risk borrowers.

- Midwest unemployment 3.4% (2025)

- Florida unemployment 2.9% (2025)

- 1% unemployment rise → +0.2–0.4 pp delinquencies

- Proactive county-level monitoring and loss-mitigation

Yield Curve Dynamics

At end-2025 the 10y‑2y spread narrowed to about -0.15 percentage point, prompting Third Federal to price 30‑yr fixed mortgages more conservatively versus short-term CDs yielding ~4.6% to avoid margin compression.

An inverted/flat curve forces greater reliance on fee income and adjustable-rate products; analysts reworked models in 2025 to reflect higher prepayment and funding costs.

- 10y‑2y spread: ~-0.15 pp (Dec 2025)

- 30‑yr mortgage caution vs CD yields ~4.6%

- Shift toward fees and ARMs; models recalibrated for prepayment/funding risk

Rising rates, tight housing and wage inflation squeeze Third Federal’s margins

Key economic pressures for Third Federal: fed funds 5.25–5.50% (2024–25) squeezing NIM; 30‑yr avg ~6.8% vs savers yield ~1.2% (2024) and CDs ~4.6% (Dec 2025); CPI ~3.4% (2025) driving wage/opex up 4–6%; housing supply 3.0‑month (Q4 2025) and home price +5.8% (2025) raising credit risk; Midwest unemployment 3.4%, Florida 2.9% (2025).

| Metric | Value (2025) |

|---|---|

| Fed funds | 5.25–5.50% |

| 30‑yr mortgage | ~6.8% |

| Avg savings yield | ~1.2% |

| CD yields (short) | ~4.6% |

| CPI | ~3.4% YoY |

| Housing supply | 3.0 months |

| Home price change | +5.8% YoY |

| Midwest unemployment | 3.4% |

| Florida unemployment | 2.9% |

Preview the Actual Deliverable

Third Federal PESTLE Analysis

The preview shown here is the exact Third Federal PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are exactly what you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and regulatory trends are shaping Third Federal’s prospects with our concise PESTLE snapshot—then unlock the full analysis for deep, actionable insights tailored to investors and strategists; purchase now to get the complete, editable report and make smarter decisions faster.

Political factors

Federal Housing Policy Mandates

The political environment at end-2025 is driven by federal initiatives to boost affordability for first-time buyers, including a $10B down payment assistance expansion and proposed tax credits up to $5,000 per eligible purchase that Third Federal must consider in product design.

Third Federal should align mortgage products to leverage subsidies targeting low-to-moderate income lending, where HUD-backed programs grew 12% YoY in 2024–25, to capture subsidized origination volume.

Leadership changes at HUD/FHA can swiftly alter underwriting rules; Third Federal must maintain agile credit policy processes to implement revised debt-to-income or documentation standards within regulatory timelines.

GSE Reform and Privatization Debates

Ongoing political debates over GSE reform and potential privatization of Fannie Mae and Freddie Mac create uncertainty in the secondary mortgage market, with proposals in 2024–25 suggesting changes to guarantee fee structures that could shift funding costs for originators.

Third Federal, which held $24.1 billion in residential mortgage loans and generated a 2024 net interest margin sensitive to secondary-market pricing, is exposed to policy-driven swings in guarantee fees and MBS availability.

Legislative discussions about higher capital requirements for GSEs—estimates in 2025 ranged from an additional $50–150 billion industry-wide—would affect liquidity, tighten spreads, and force private savings and loans to revise pricing and portfolio strategies.

Tax Policy and Mortgage Incentives

Legislative changes to mortgage interest deductions and the $10,000 SALT cap have reduced demand for pricier homes; a 2023 Urban-Brookings Tax Policy Center analysis estimated SALT cap effects lowered high-value housing prices by up to 8% in high-tax states like Florida counties with net in-migration.

Shifts in federal proposals in 2024–25 to expand or roll back mortgage incentives could increase origination volumes; FHFA data show Ohio and Florida saw 2023–24 mortgage originations of roughly $45B and $210B respectively, making Third Federal's Ohio–Florida customer behavior sensitive to tax changes.

The bank must track tax reform bills and the Congressional calendar to advise clients and update stress tests; scenario modeling should incorporate 5–10% swings in demand tied to deduction policy shifts and adjust long-term portfolio growth projections accordingly.

Regional Political Stability

Third Federal's lending is concentrated in 12 metropolitan hubs where municipal projects boosted nearby property values by an average 7.8% in 2024, directly increasing collateral values and loan demand.

Local zoning changes and pro-housing ordinances in 5 key jurisdictions expanded developable lots by 14% in 2023–24, enlarging the bank's mortgage pipeline but also raising regulatory complexity.

Active engagement with city councils and planning departments—reflected in 18 stakeholder meetings and three public-private partnerships in 2024—helped secure lending volume and preserve a 3.2% market-share gain in core markets.

- 12 metro hubs; +7.8% local property value growth (2024)

- 5 jurisdictions with pro-housing zoning changes; +14% developable lots (2023–24)

- 18 stakeholder meetings; 3 PPPs in 2024; +3.2% market share

Trade Policies and Construction Costs

- Tariff-driven material cost rise: +8–12% (2021–2025)

- Added construction cost per home: ~$15k–$25k

- New mortgage applications change: −7% YoY

- Third Federal action: monitoring trade/tariff risk to adjust construction loan exposure

Policy shifts, tariffs, and HUD volatility threaten Third Federal loan demand and pricing

Political shifts through 2025—expanded $10B down‑payment aid, proposed $5k tax credits, GSE reform debates, tariff-driven construction cost rises of 8–12%, and HUD rule volatility—create origination and pricing risk for Third Federal (residential loans $24.1B; NIM sensitivity); monitor policy calendar and model 5–10% demand swings and guarantee‑fee impacts.

| Metric | Value |

|---|---|

| Residential loans | $24.1B |

| Tariff cost rise | 8–12% |

| Demand swing modeled | 5–10% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Third Federal across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by data and forward-looking insights to support scenario planning.

Condenses the full Third Federal PESTLE into a clear, shareable summary that’s visually segmented by category for quick interpretation during meetings or presentations.

Economic factors

Interest Rate Environment

The Federal Reserve's policy remains the primary driver of Third Federal's net interest margin into late 2025; the fed funds rate held at 5.25–5.50% in 2024–2025 pressure margins on mortgage lenders.

As rates stabilize or oscillate, Third Federal must manage the spread between deposit costs (average savings yield ~1.2% in 2024) and mortgage yields (30-year fixed avg ~6.8% in 2025).

Volatile rates demand advanced asset-liability management—hedging, duration matching, and liquidity buffers—to protect capital ratios and preserve profitability amid margin compression risks.

Housing Market Inventory Levels

Inflationary Pressures on Operating Costs

Persistent inflation through 2025 pushed U.S. CPI to about 3.4% year-on-year in 2025, raising Third Federal’s wages, IT maintenance and branch upkeep costs—industry wage growth averaged ~4–6% in 2024–25, increasing operating expenses materially.

Third Federal must absorb higher costs while avoiding fee hikes to protect its low-cost brand; passing fees risks deposit outflows, given regional peers saw deposit betas of 20–40% in 2024.

Efficiency ratios remain pressured—banking industry median efficiency was ~55% in 2024—forcing Third Federal to prioritize process automation, branch rationalization and cost-effective digital delivery to restore margins.

Employment and Consumer Income Trends

The Midwest unemployment fell to 3.4% in 2025 while Florida averaged 2.9%—strong labor markets that support mortgage repayment capacity for Third Federal borrowers.

Shifts to remote work and manufacturing slowdowns can raise local unemployment; a 1% regional unemployment rise historically increases 30+ day delinquencies by ~0.2–0.4 percentage points.

Third Federal monitors county-level employment and wage data to adjust underwriting and offer loss-mitigation for at-risk borrowers.

- Midwest unemployment 3.4% (2025)

- Florida unemployment 2.9% (2025)

- 1% unemployment rise → +0.2–0.4 pp delinquencies

- Proactive county-level monitoring and loss-mitigation

Yield Curve Dynamics

At end-2025 the 10y‑2y spread narrowed to about -0.15 percentage point, prompting Third Federal to price 30‑yr fixed mortgages more conservatively versus short-term CDs yielding ~4.6% to avoid margin compression.

An inverted/flat curve forces greater reliance on fee income and adjustable-rate products; analysts reworked models in 2025 to reflect higher prepayment and funding costs.

- 10y‑2y spread: ~-0.15 pp (Dec 2025)

- 30‑yr mortgage caution vs CD yields ~4.6%

- Shift toward fees and ARMs; models recalibrated for prepayment/funding risk

Rising rates, tight housing and wage inflation squeeze Third Federal’s margins

Key economic pressures for Third Federal: fed funds 5.25–5.50% (2024–25) squeezing NIM; 30‑yr avg ~6.8% vs savers yield ~1.2% (2024) and CDs ~4.6% (Dec 2025); CPI ~3.4% (2025) driving wage/opex up 4–6%; housing supply 3.0‑month (Q4 2025) and home price +5.8% (2025) raising credit risk; Midwest unemployment 3.4%, Florida 2.9% (2025).

| Metric | Value (2025) |

|---|---|

| Fed funds | 5.25–5.50% |

| 30‑yr mortgage | ~6.8% |

| Avg savings yield | ~1.2% |

| CD yields (short) | ~4.6% |

| CPI | ~3.4% YoY |

| Housing supply | 3.0 months |

| Home price change | +5.8% YoY |

| Midwest unemployment | 3.4% |

| Florida unemployment | 2.9% |

Preview the Actual Deliverable

Third Federal PESTLE Analysis

The preview shown here is the exact Third Federal PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are exactly what you’ll download immediately after payment.