THK PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech advances are reshaping THK’s market position—our concise PESTLE highlights key external risks and opportunities to inform smarter strategies. Ready-made for investors and strategists, the full report delivers deep-dive analysis, editable charts, and actionable recommendations. Purchase now to access the complete, instantly downloadable PESTLE and make decisions with confidence.

Political factors

Global trade tensions and tariff barriers

Ongoing US-China trade tensions have led THK to reconfigure its supply chain, with tariffs on precision machinery rising up to 25% in some categories, contributing to a reported 3–5% margin pressure in 2023–24 for Japanese component exporters.

Government subsidies for domestic semiconductor industries

Many governments have pledged large subsidies—e.g., US CHIPS Act $52.7bn (2022) and EU’s 2023 proposals totaling €43bn—to onshore semiconductor production for national security, directly boosting demand for THK’s high-precision motion components used in lithography and assembly equipment. THK stands to gain as industrial policies push fabs investment; global fab capex reached an estimated $88bn in 2024, driving orders for precision parts tied to technological sovereignty goals.

Export controls on dual-use technologies

Stricter export controls on dual-use technologies raise risks for THK, as Japan tightened lists in 2023 expanding items deemed sensitive; in 2024 over 12% of Japanese machine tool exports faced new screening, threatening revenue from precision components—THK must comply with the Foreign Exchange and Foreign Trade Act and Wassenaar Arrangement norms, any sudden list updates can cut off markets, potentially affecting segments that contributed to ¥45.2bn of FY2024 sales.

Regional stability in manufacturing hubs

Political stability in Southeast Asia and Eastern Europe is vital for THK’s decentralized production; in 2024, 28% of THK’s revenue-linked components originated from ASEAN-linked suppliers, making supply-chain exposure material.

Unrest or sudden leadership changes can disrupt logistics or trigger labor-law shifts—the World Bank recorded a 6% regional labor-cost variance in 2023–24—impacting THK’s assembly efficiency.

THK actively monitors geopolitical shifts via scenario planning and supplier diversification to safeguard a 99% on-time global component delivery target.

- 28% of revenue-linked components sourced from ASEAN suppliers (2024)

- 6% regional labor-cost variance recorded (2023–24)

- 99% on-time component delivery target maintained through diversification

Support for robotics and automation initiatives

- Japan 2024 robotics/AI budget ¥1.7T (~$12.5B)

- Global healthcare/logistics robotics CAGR ~20% to 2028

- THK core products are essential for industrial robot motion systems

THK: Subsidies Fuel Demand as Tariffs, Export Controls and ASEAN Risks Squeeze Margins

Geopolitical tensions, tariffs and export controls (25% tariffs; 12% of machine-tool exports newly screened in 2024) pressure margins and market access, while industrial subsidies (US CHIPS $52.7bn; EU €43bn) and Japan’s ¥1.7T robotics/AI budget boost demand for THK’s precision components; 28% of revenue-linked parts from ASEAN and 6% regional labor-cost variance heighten supply-chain risk despite a 99% on-time delivery target.

| Metric | Value |

|---|---|

| Tariff peak | 25% |

| Machine-export screening (2024) | 12% |

| US CHIPS | $52.7bn |

| EU proposals | €43bn |

| Japan robotics/AI 2024 | ¥1.7T |

| ASEAN-sourced components | 28% |

| Labor-cost variance | 6% |

| On-time target | 99% |

What is included in the product

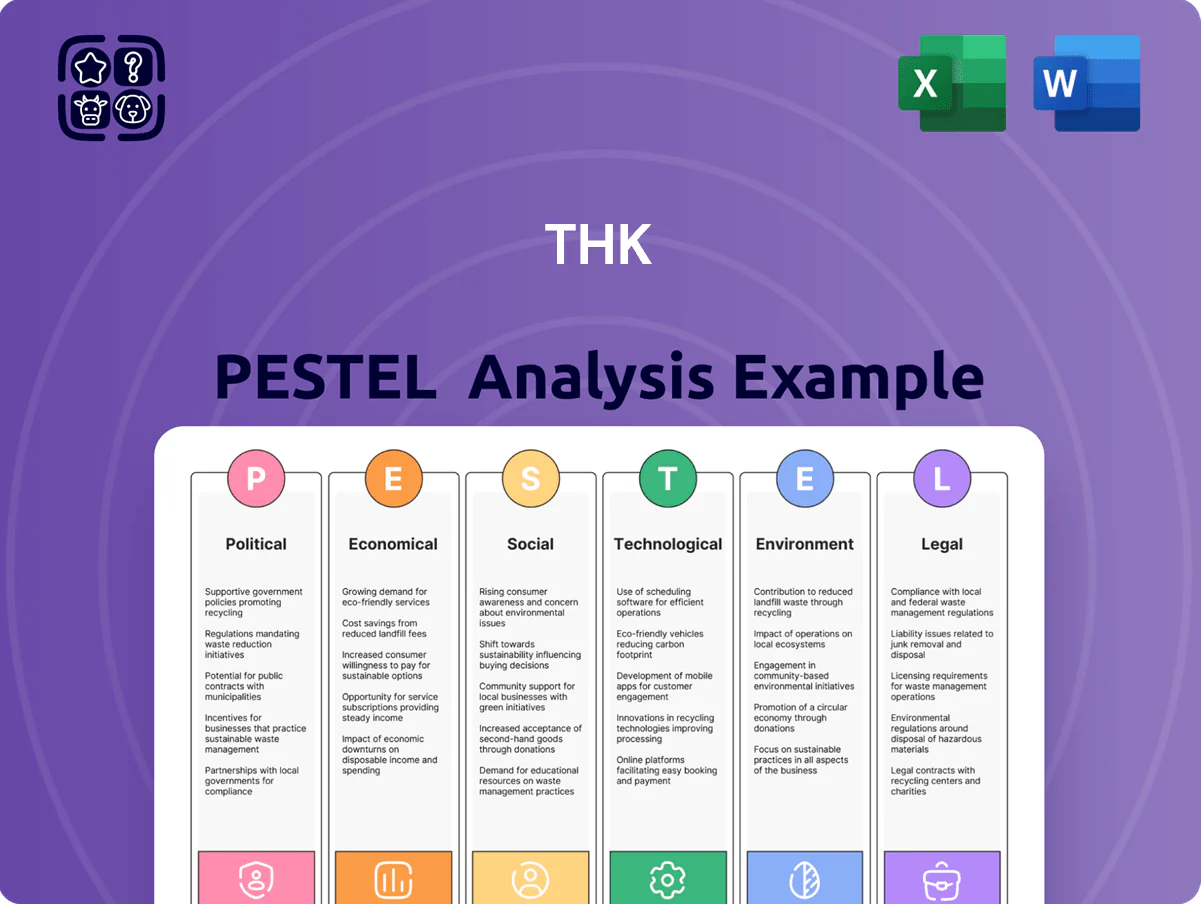

Explores how external macro-environmental factors uniquely affect THK across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities.

Condensed THK PESTLE summary that highlights key political, economic, social, technological, legal, and environmental factors for quick reference during meetings or presentations.

Economic factors

Impact of currency exchange rate volatility

As a Japan-based manufacturer with ~60% of sales outside Japan, THK is highly exposed to JPY/USD and JPY/EUR moves; a 10% weaker yen in 2023 boosted export competitiveness but raised imported steel costs by an estimated 4–6%, pressuring gross margins.

THK reported ¥31.2bn forex gains in FY2023 through hedging and netting; ongoing localized production in US/EU plants (≈30% of capacity by 2024) further insulates earnings from exchange-rate volatility.

Global interest rate environment and CAPEX

Prevailing central bank rates directly affect CAPEX among THK’s machine tool and automotive clients; Japan’s BOJ shift in 2024 and the US Fed funds rate averaging 5.25–5.50% in 2024–2025 coincided with a 10–15% deceleration in global machine tool orders in 2024, delaying purchases of THK-dependent equipment.

A pivot to lower rates typically triggers factory automation upgrades and higher demand for linear-motion components; after rate cuts in late 2023–mid 2024 in some EMs, industrial robotics orders rose ~12–18%, suggesting potential order upside for THK if major central banks ease.

Rising costs of raw materials and energy

The production of LM guides and ball screws is steel- and energy-intensive, leaving THK exposed to raw material inflation; global steel prices rose ~18% YoY in 2024 while Japan industrial electricity prices increased ~7% in 2023–24, pressuring margins if costs cannot be passed to customers. THK reported efforts in 2024 to cut energy use per unit by targeting a ~5% reduction via process optimization and energy-efficient equipment investments to mitigate commodity and energy volatility.

Growth of the electric vehicle market

The global shift to EVs—projected EV sales reaching ~40% of new vehicle sales by 2030 and 14 million EVs sold in 2024—boosts demand for THK’s precision motion components used in steering, braking actuators and battery assembly lines.

EV-specific mechanical layouts require high-performance actuators and linear guides; THK can capture a larger share as automakers increase EV capital expenditure (automotive EV capex up ~20% YoY in 2024).

This structural industry shift offers THK a clear revenue diversification path, with automotive EV component demand potentially offsetting slower ICE-related segments.

- EVs ~40% of new sales by 2030; 14M sold in 2024

- Automotive EV capex +~20% YoY in 2024

- Higher demand for actuators, linear guides, assembly automation

Economic recovery and industrialization in China

China's 2024 industrial output rose 4.6% year-on-year through November, sustaining demand for THK's linear motion products as manufacturers shift toward high-end automation and robotics, boosting orders for precision components.

As Chinese firms climb the value chain, THK's market exposure to premium automation increases; THK Japan reported 2024 China revenue up mid-single digits, reflecting this trend.

Slower real estate investment—down about 6% YTD in 2024—and weaker infrastructure spending could indirectly compress demand for industrial machinery and dampen THK order growth.

- Industrial output +4.6% YTD Nov 2024 — supports THK demand

- THK China revenue: mid-single-digit growth in 2024

- Real estate investment -6% YTD 2024 — risk to equipment demand

THK rides EV capex and forex gains despite weaker tool orders and commodity costs

THK faces FX and commodity exposure: 10% weaker JPY in 2023 lifted exports but raised imported steel costs ~4–6%; FY2023 ¥31.2bn forex gains and ~30% localized capacity by 2024 reduce volatility. Higher rates cut machine-tool orders ~10–15% in 2024; easing could boost automation demand (robot orders +12–18%). EV tailwinds (14m EVs in 2024; EV capex +20% YoY) offset slower China real estate (-6% YTD 2024).

| Metric | 2023–2024 |

|---|---|

| JPY move effect | 10% weaker JPY |

| Forex gains | ¥31.2bn FY2023 |

| Localized capacity | ≈30% by 2024 |

| Machine-tool orders | -10–15% 2024 |

| Robot orders | +12–18% |

| EVs sold | 14m 2024 |

| EV capex | +20% YoY 2024 |

| China industrial output | +4.6% YTD Nov 2024 |

| China real estate | -6% YTD 2024 |

Preview Before You Purchase

THK PESTLE Analysis

The preview shown here is the exact THK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and rapid tech advances are reshaping THK’s market position—our concise PESTLE highlights key external risks and opportunities to inform smarter strategies. Ready-made for investors and strategists, the full report delivers deep-dive analysis, editable charts, and actionable recommendations. Purchase now to access the complete, instantly downloadable PESTLE and make decisions with confidence.

Political factors

Global trade tensions and tariff barriers

Ongoing US-China trade tensions have led THK to reconfigure its supply chain, with tariffs on precision machinery rising up to 25% in some categories, contributing to a reported 3–5% margin pressure in 2023–24 for Japanese component exporters.

Government subsidies for domestic semiconductor industries

Many governments have pledged large subsidies—e.g., US CHIPS Act $52.7bn (2022) and EU’s 2023 proposals totaling €43bn—to onshore semiconductor production for national security, directly boosting demand for THK’s high-precision motion components used in lithography and assembly equipment. THK stands to gain as industrial policies push fabs investment; global fab capex reached an estimated $88bn in 2024, driving orders for precision parts tied to technological sovereignty goals.

Export controls on dual-use technologies

Stricter export controls on dual-use technologies raise risks for THK, as Japan tightened lists in 2023 expanding items deemed sensitive; in 2024 over 12% of Japanese machine tool exports faced new screening, threatening revenue from precision components—THK must comply with the Foreign Exchange and Foreign Trade Act and Wassenaar Arrangement norms, any sudden list updates can cut off markets, potentially affecting segments that contributed to ¥45.2bn of FY2024 sales.

Regional stability in manufacturing hubs

Political stability in Southeast Asia and Eastern Europe is vital for THK’s decentralized production; in 2024, 28% of THK’s revenue-linked components originated from ASEAN-linked suppliers, making supply-chain exposure material.

Unrest or sudden leadership changes can disrupt logistics or trigger labor-law shifts—the World Bank recorded a 6% regional labor-cost variance in 2023–24—impacting THK’s assembly efficiency.

THK actively monitors geopolitical shifts via scenario planning and supplier diversification to safeguard a 99% on-time global component delivery target.

- 28% of revenue-linked components sourced from ASEAN suppliers (2024)

- 6% regional labor-cost variance recorded (2023–24)

- 99% on-time component delivery target maintained through diversification

Support for robotics and automation initiatives

- Japan 2024 robotics/AI budget ¥1.7T (~$12.5B)

- Global healthcare/logistics robotics CAGR ~20% to 2028

- THK core products are essential for industrial robot motion systems

THK: Subsidies Fuel Demand as Tariffs, Export Controls and ASEAN Risks Squeeze Margins

Geopolitical tensions, tariffs and export controls (25% tariffs; 12% of machine-tool exports newly screened in 2024) pressure margins and market access, while industrial subsidies (US CHIPS $52.7bn; EU €43bn) and Japan’s ¥1.7T robotics/AI budget boost demand for THK’s precision components; 28% of revenue-linked parts from ASEAN and 6% regional labor-cost variance heighten supply-chain risk despite a 99% on-time delivery target.

| Metric | Value |

|---|---|

| Tariff peak | 25% |

| Machine-export screening (2024) | 12% |

| US CHIPS | $52.7bn |

| EU proposals | €43bn |

| Japan robotics/AI 2024 | ¥1.7T |

| ASEAN-sourced components | 28% |

| Labor-cost variance | 6% |

| On-time target | 99% |

What is included in the product

Explores how external macro-environmental factors uniquely affect THK across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and current trends to identify threats and opportunities.

Condensed THK PESTLE summary that highlights key political, economic, social, technological, legal, and environmental factors for quick reference during meetings or presentations.

Economic factors

Impact of currency exchange rate volatility

As a Japan-based manufacturer with ~60% of sales outside Japan, THK is highly exposed to JPY/USD and JPY/EUR moves; a 10% weaker yen in 2023 boosted export competitiveness but raised imported steel costs by an estimated 4–6%, pressuring gross margins.

THK reported ¥31.2bn forex gains in FY2023 through hedging and netting; ongoing localized production in US/EU plants (≈30% of capacity by 2024) further insulates earnings from exchange-rate volatility.

Global interest rate environment and CAPEX

Prevailing central bank rates directly affect CAPEX among THK’s machine tool and automotive clients; Japan’s BOJ shift in 2024 and the US Fed funds rate averaging 5.25–5.50% in 2024–2025 coincided with a 10–15% deceleration in global machine tool orders in 2024, delaying purchases of THK-dependent equipment.

A pivot to lower rates typically triggers factory automation upgrades and higher demand for linear-motion components; after rate cuts in late 2023–mid 2024 in some EMs, industrial robotics orders rose ~12–18%, suggesting potential order upside for THK if major central banks ease.

Rising costs of raw materials and energy

The production of LM guides and ball screws is steel- and energy-intensive, leaving THK exposed to raw material inflation; global steel prices rose ~18% YoY in 2024 while Japan industrial electricity prices increased ~7% in 2023–24, pressuring margins if costs cannot be passed to customers. THK reported efforts in 2024 to cut energy use per unit by targeting a ~5% reduction via process optimization and energy-efficient equipment investments to mitigate commodity and energy volatility.

Growth of the electric vehicle market

The global shift to EVs—projected EV sales reaching ~40% of new vehicle sales by 2030 and 14 million EVs sold in 2024—boosts demand for THK’s precision motion components used in steering, braking actuators and battery assembly lines.

EV-specific mechanical layouts require high-performance actuators and linear guides; THK can capture a larger share as automakers increase EV capital expenditure (automotive EV capex up ~20% YoY in 2024).

This structural industry shift offers THK a clear revenue diversification path, with automotive EV component demand potentially offsetting slower ICE-related segments.

- EVs ~40% of new sales by 2030; 14M sold in 2024

- Automotive EV capex +~20% YoY in 2024

- Higher demand for actuators, linear guides, assembly automation

Economic recovery and industrialization in China

China's 2024 industrial output rose 4.6% year-on-year through November, sustaining demand for THK's linear motion products as manufacturers shift toward high-end automation and robotics, boosting orders for precision components.

As Chinese firms climb the value chain, THK's market exposure to premium automation increases; THK Japan reported 2024 China revenue up mid-single digits, reflecting this trend.

Slower real estate investment—down about 6% YTD in 2024—and weaker infrastructure spending could indirectly compress demand for industrial machinery and dampen THK order growth.

- Industrial output +4.6% YTD Nov 2024 — supports THK demand

- THK China revenue: mid-single-digit growth in 2024

- Real estate investment -6% YTD 2024 — risk to equipment demand

THK rides EV capex and forex gains despite weaker tool orders and commodity costs

THK faces FX and commodity exposure: 10% weaker JPY in 2023 lifted exports but raised imported steel costs ~4–6%; FY2023 ¥31.2bn forex gains and ~30% localized capacity by 2024 reduce volatility. Higher rates cut machine-tool orders ~10–15% in 2024; easing could boost automation demand (robot orders +12–18%). EV tailwinds (14m EVs in 2024; EV capex +20% YoY) offset slower China real estate (-6% YTD 2024).

| Metric | 2023–2024 |

|---|---|

| JPY move effect | 10% weaker JPY |

| Forex gains | ¥31.2bn FY2023 |

| Localized capacity | ≈30% by 2024 |

| Machine-tool orders | -10–15% 2024 |

| Robot orders | +12–18% |

| EVs sold | 14m 2024 |

| EV capex | +20% YoY 2024 |

| China industrial output | +4.6% YTD Nov 2024 |

| China real estate | -6% YTD 2024 |

Preview Before You Purchase

THK PESTLE Analysis

The preview shown here is the exact THK PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.