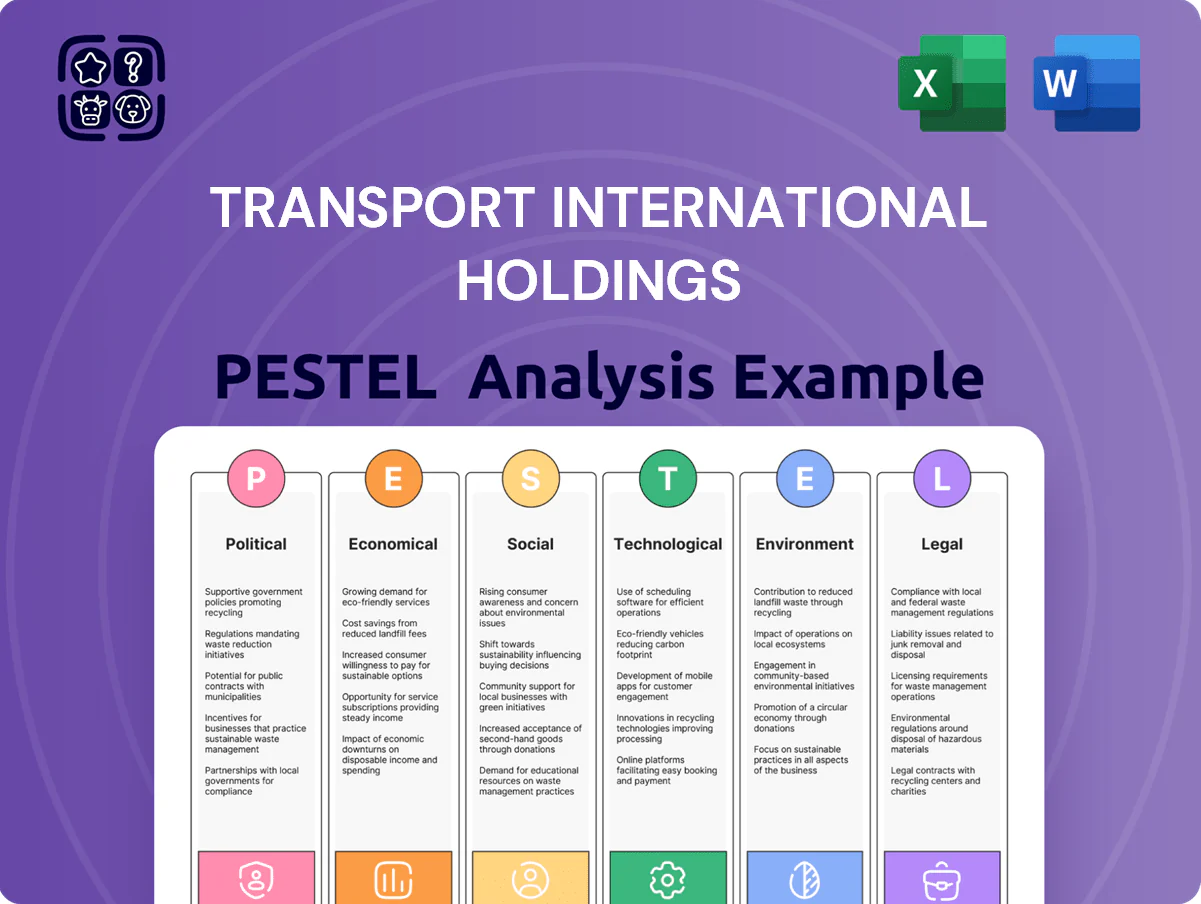

Transport International Holdings PESTLE Analysis

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Transport International Holdings—spot political, economic, social, technological, legal, and environmental forces shaping its prospects and risks. Ideal for investors, advisors, and strategists needing concise, actionable intelligence. Purchase the full report to access deep-dive insights, ready-to-use charts, and recommendations to inform decisions and strengthen your competitive position.

Political factors

Government Transport Subsidies

The Hong Kong government’s Public Transport Fare Subsidy Scheme allocated HK$1.7 billion in 2024, and green transport grants (including EV bus incentives) contributed about HK$450 million to franchised operators that year, underpinning fare stability as Transport International Holdings phases to new-energy buses; executives must watch potential policy adjustments ahead of the 2026–2028 subsidy reviews that could materially affect operating subsidies and capex recovery timelines.

Greater Bay Area Integration

Political initiatives to integrate Hong Kong with the Greater Bay Area (GBA)—backed by a 2023 GBA Infrastructure Plan allocating HK$300 billion to transport links—shape TIH route planning and cross-boundary services.

TIH must align expansion with government projects like the Hong Kong–Shenzhen Western Express Line and increased cross-boundary bus quotas (up 12% in 2024) to ensure smoother intercity movement.

Such alignment positions TIH to capture rising demand: cross-boundary passenger volumes rose 8% in 2024, keeping the company central to the evolving regional transport network.

Public Franchise Stability

Transport International Holdings' stability hinges on Hong Kong's periodic bus franchise renewals, with the current franchise revenue representing about HKD 6.2bn in FY2024, making renewal outcomes material to cash flow predictability.

Maintaining strong ties with the Transport and Logistics Bureau is vital to secure favorable terms and multi-year operational certainty after the 2023-2025 review cycle.

Political pressure over fare adjustments—publicly sensitive after a 2.5% average fare rise proposal in 2024—requires careful negotiation to balance ridership objectives with the group's FY2024 operating margin of roughly 8.7%.

Geopolitical Energy Influence

- Brent avg 86 USD/bbl in 2024; diesel exposure for 14,000+ buses

- Battery-cell lead times +18% in 2024; EV rollout risk

- Recommended: fuel hedging, supplier diversification, contingency inventory

Northern Metropolis Development

The government-led Northern Metropolis initiative presents a major strategic opportunity for Transport International Holdings to expand routes as the plan targets 2.5–3.5 million new residents and adds HKD 300–500 billion in development value by 2035, boosting cross-border commuter demand.

TIH must secure operating rights for emerging residential and commercial hubs near the Shenzhen border to capture projected passenger growth—government forecasts indicate a 15–25% rise in regional transit usage by 2030.

The project is a central political priority and a primary driver of future ridership and farebox revenue, potentially increasing TIH’s passenger yields and network density in high-growth corridors.

- Targets 2.5–3.5M new residents; HKD 300–500B value by 2035

- Projected 15–25% transit demand rise by 2030

- Requires securing operating rights near border hubs

- Key political driver for future ridership and revenue

Policy shifts, GBA push and subsidies to reshape TIH capex, routes and revenue

Government subsidies (HK$1.7bn fare scheme; HK$450m green grants in 2024), GBA integration (HK$300bn 2023 plan), franchise revenue ~HK$6.2bn FY2024, cross-boundary demand +8% in 2024, Brent ~US$86/bbl (2024) and battery lead times +18%—policy shifts, franchise renewals and Northern Metropolis (2.5–3.5M residents) critically affect TIH capex, subsidies and route rights.

| Metric | Value (2024) |

|---|---|

| Fare subsidy | HK$1.7bn |

| Green grants | HK$450m |

| Franchise rev | HK$6.2bn |

| Cross-boundary pax | +8% |

| Brent | US$86/bbl |

| Battery lead times | +18% |

What is included in the product

Explores how macro-environmental forces uniquely impact Transport International Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to inform risk mitigation and opportunity capture for executives, consultants, and investors.

A concise, PESTLE-segmented summary of Transport International Holdings that clarifies regulatory, economic, social, technological, environmental, and legal drivers—ready to drop into presentations or planning sessions to streamline risk discussions and team alignment.

Economic factors

Fuel Price Fluctuations

Despite accelerating electrification, Transport International Holdings still operates a large diesel fleet, leaving it exposed to oil price swings; Brent averaged about USD 88/bbl in 2024, up from USD 75 in 2023, which directly pressures fuel spend.

Fuel cost variability compresses operating margins—fuel can represent 10–18% of bus operating costs—prompting the company to employ fuel hedging and route-efficiency measures to stabilize margins.

Analysts track energy price trajectories and hedge effectiveness to model short-term earnings volatility; consensus 2025 earnings estimates factor in fuel risk with sensitivity scenarios shifting EPS by several percentage points per 10% fuel move.

Labor Market Constraints

Hong Kong faces a persistent shortage of skilled bus drivers and technicians, pushing TIH to raise starting wages—driver median pay rose ~8% to HKD 28,000/month in 2024—and increasing recruitment costs by an estimated 12–15% year-on-year. TIH must invest heavily in retention and training; 2025 workforce upskilling budgets were reported at ~HKD 60–80 million to maintain service frequency and safety. Rising labor costs are among TIH’s largest recurring expenses, comprising roughly 35–40% of annual operating costs in 2024.

Interest Rate Environment

As TIH pursues a HKD 10–15 billion fleet renewal to meet emissions targets, rising interest rates materially raise borrowing costs: Hong Kong Prime Rate rose to 6.75% in 2024, pushing effective yields on corporate debt higher and increasing annual interest expense by an estimated HKD 200–300m versus 2021 rates; analysts must assess TIH’s leverage (net debt/EBITDA ~2.0x in 2024) and S&P/Moody’s outlook amid tightening monetary policy.

Tourism and Airport Recovery

The Long Win Bus segment's revenue closely tracks airport passenger throughput; Hong Kong international arrivals rose to 52% of 2019 levels in 2024, lifting airport express ridership and premium service demand.

Premium airport routes yield higher margins than local lines—Transport International reported a 2024 segment margin uplift correlated with a 38% year-on-year increase in airport-related fares.

Ongoing aviation recovery—HKIA cargo and passenger turnaround—serves as a KPI for the group's diversified portfolio resilience.

- 2024 arrivals ~52% of 2019; airport-related fares +38% YoY

Property Investment Returns

TIH has diversified revenue via commercial property like The Millennity; investment properties contributed HKD 1.2 billion in fair value gains in FY2024, boosting non-fare income.

Hong Kong real estate performance drives TIH valuation—office vacancy rose to ~10.5% in 2024, pressuring rents and potential yields on TIH’s assets.

Economic downturns in office/retail can reduce rental yields and capital appreciation, risking lower recurring income and balance-sheet revaluation losses.

- FY2024 fair value gains HKD 1.2bn

- HK office vacancy ~10.5% (2024)

- Non-fare revenue tied to property performance

Fuel, labor and financing squeeze margins; airport recovery and property soften the blow

Fuel (Brent ~USD 88/bbl in 2024) and labor (driver pay ~HKD 28,000/mo; labor = 35–40% costs) drive margin volatility; fleet renewal (HKD 10–15bn) and higher rates (HK Prime ~6.75% in 2024) raise financing costs; airport recovery (arrivals ~52% of 2019; airport fares +38% YoY) boosts premium revenue; property gains (FY2024 fair value +HKD 1.2bn) diversify income but HK office vacancy ~10.5% risks rent downside.

| Metric | 2024 |

|---|---|

| Brent (USD/bbl) | ~88 |

| Driver median pay (HKD/mo) | ~28,000 |

| Labor % of costs | 35–40% |

| HK Prime Rate | ~6.75% |

| Fleet renewal capex | HKD 10–15bn |

| Airport arrivals vs 2019 | ~52% |

| Airport fares YoY | +38% |

| Property fair value gains | +HKD 1.2bn |

| HK office vacancy | ~10.5% |

Same Document Delivered

Transport International Holdings PESTLE Analysis

The preview shown here is the exact Transport International Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are exactly what you’ll download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Transport International Holdings—spot political, economic, social, technological, legal, and environmental forces shaping its prospects and risks. Ideal for investors, advisors, and strategists needing concise, actionable intelligence. Purchase the full report to access deep-dive insights, ready-to-use charts, and recommendations to inform decisions and strengthen your competitive position.

Political factors

Government Transport Subsidies

The Hong Kong government’s Public Transport Fare Subsidy Scheme allocated HK$1.7 billion in 2024, and green transport grants (including EV bus incentives) contributed about HK$450 million to franchised operators that year, underpinning fare stability as Transport International Holdings phases to new-energy buses; executives must watch potential policy adjustments ahead of the 2026–2028 subsidy reviews that could materially affect operating subsidies and capex recovery timelines.

Greater Bay Area Integration

Political initiatives to integrate Hong Kong with the Greater Bay Area (GBA)—backed by a 2023 GBA Infrastructure Plan allocating HK$300 billion to transport links—shape TIH route planning and cross-boundary services.

TIH must align expansion with government projects like the Hong Kong–Shenzhen Western Express Line and increased cross-boundary bus quotas (up 12% in 2024) to ensure smoother intercity movement.

Such alignment positions TIH to capture rising demand: cross-boundary passenger volumes rose 8% in 2024, keeping the company central to the evolving regional transport network.

Public Franchise Stability

Transport International Holdings' stability hinges on Hong Kong's periodic bus franchise renewals, with the current franchise revenue representing about HKD 6.2bn in FY2024, making renewal outcomes material to cash flow predictability.

Maintaining strong ties with the Transport and Logistics Bureau is vital to secure favorable terms and multi-year operational certainty after the 2023-2025 review cycle.

Political pressure over fare adjustments—publicly sensitive after a 2.5% average fare rise proposal in 2024—requires careful negotiation to balance ridership objectives with the group's FY2024 operating margin of roughly 8.7%.

Geopolitical Energy Influence

- Brent avg 86 USD/bbl in 2024; diesel exposure for 14,000+ buses

- Battery-cell lead times +18% in 2024; EV rollout risk

- Recommended: fuel hedging, supplier diversification, contingency inventory

Northern Metropolis Development

The government-led Northern Metropolis initiative presents a major strategic opportunity for Transport International Holdings to expand routes as the plan targets 2.5–3.5 million new residents and adds HKD 300–500 billion in development value by 2035, boosting cross-border commuter demand.

TIH must secure operating rights for emerging residential and commercial hubs near the Shenzhen border to capture projected passenger growth—government forecasts indicate a 15–25% rise in regional transit usage by 2030.

The project is a central political priority and a primary driver of future ridership and farebox revenue, potentially increasing TIH’s passenger yields and network density in high-growth corridors.

- Targets 2.5–3.5M new residents; HKD 300–500B value by 2035

- Projected 15–25% transit demand rise by 2030

- Requires securing operating rights near border hubs

- Key political driver for future ridership and revenue

Policy shifts, GBA push and subsidies to reshape TIH capex, routes and revenue

Government subsidies (HK$1.7bn fare scheme; HK$450m green grants in 2024), GBA integration (HK$300bn 2023 plan), franchise revenue ~HK$6.2bn FY2024, cross-boundary demand +8% in 2024, Brent ~US$86/bbl (2024) and battery lead times +18%—policy shifts, franchise renewals and Northern Metropolis (2.5–3.5M residents) critically affect TIH capex, subsidies and route rights.

| Metric | Value (2024) |

|---|---|

| Fare subsidy | HK$1.7bn |

| Green grants | HK$450m |

| Franchise rev | HK$6.2bn |

| Cross-boundary pax | +8% |

| Brent | US$86/bbl |

| Battery lead times | +18% |

What is included in the product

Explores how macro-environmental forces uniquely impact Transport International Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to inform risk mitigation and opportunity capture for executives, consultants, and investors.

A concise, PESTLE-segmented summary of Transport International Holdings that clarifies regulatory, economic, social, technological, environmental, and legal drivers—ready to drop into presentations or planning sessions to streamline risk discussions and team alignment.

Economic factors

Fuel Price Fluctuations

Despite accelerating electrification, Transport International Holdings still operates a large diesel fleet, leaving it exposed to oil price swings; Brent averaged about USD 88/bbl in 2024, up from USD 75 in 2023, which directly pressures fuel spend.

Fuel cost variability compresses operating margins—fuel can represent 10–18% of bus operating costs—prompting the company to employ fuel hedging and route-efficiency measures to stabilize margins.

Analysts track energy price trajectories and hedge effectiveness to model short-term earnings volatility; consensus 2025 earnings estimates factor in fuel risk with sensitivity scenarios shifting EPS by several percentage points per 10% fuel move.

Labor Market Constraints

Hong Kong faces a persistent shortage of skilled bus drivers and technicians, pushing TIH to raise starting wages—driver median pay rose ~8% to HKD 28,000/month in 2024—and increasing recruitment costs by an estimated 12–15% year-on-year. TIH must invest heavily in retention and training; 2025 workforce upskilling budgets were reported at ~HKD 60–80 million to maintain service frequency and safety. Rising labor costs are among TIH’s largest recurring expenses, comprising roughly 35–40% of annual operating costs in 2024.

Interest Rate Environment

As TIH pursues a HKD 10–15 billion fleet renewal to meet emissions targets, rising interest rates materially raise borrowing costs: Hong Kong Prime Rate rose to 6.75% in 2024, pushing effective yields on corporate debt higher and increasing annual interest expense by an estimated HKD 200–300m versus 2021 rates; analysts must assess TIH’s leverage (net debt/EBITDA ~2.0x in 2024) and S&P/Moody’s outlook amid tightening monetary policy.

Tourism and Airport Recovery

The Long Win Bus segment's revenue closely tracks airport passenger throughput; Hong Kong international arrivals rose to 52% of 2019 levels in 2024, lifting airport express ridership and premium service demand.

Premium airport routes yield higher margins than local lines—Transport International reported a 2024 segment margin uplift correlated with a 38% year-on-year increase in airport-related fares.

Ongoing aviation recovery—HKIA cargo and passenger turnaround—serves as a KPI for the group's diversified portfolio resilience.

- 2024 arrivals ~52% of 2019; airport-related fares +38% YoY

Property Investment Returns

TIH has diversified revenue via commercial property like The Millennity; investment properties contributed HKD 1.2 billion in fair value gains in FY2024, boosting non-fare income.

Hong Kong real estate performance drives TIH valuation—office vacancy rose to ~10.5% in 2024, pressuring rents and potential yields on TIH’s assets.

Economic downturns in office/retail can reduce rental yields and capital appreciation, risking lower recurring income and balance-sheet revaluation losses.

- FY2024 fair value gains HKD 1.2bn

- HK office vacancy ~10.5% (2024)

- Non-fare revenue tied to property performance

Fuel, labor and financing squeeze margins; airport recovery and property soften the blow

Fuel (Brent ~USD 88/bbl in 2024) and labor (driver pay ~HKD 28,000/mo; labor = 35–40% costs) drive margin volatility; fleet renewal (HKD 10–15bn) and higher rates (HK Prime ~6.75% in 2024) raise financing costs; airport recovery (arrivals ~52% of 2019; airport fares +38% YoY) boosts premium revenue; property gains (FY2024 fair value +HKD 1.2bn) diversify income but HK office vacancy ~10.5% risks rent downside.

| Metric | 2024 |

|---|---|

| Brent (USD/bbl) | ~88 |

| Driver median pay (HKD/mo) | ~28,000 |

| Labor % of costs | 35–40% |

| HK Prime Rate | ~6.75% |

| Fleet renewal capex | HKD 10–15bn |

| Airport arrivals vs 2019 | ~52% |

| Airport fares YoY | +38% |

| Property fair value gains | +HKD 1.2bn |

| HK office vacancy | ~10.5% |

Same Document Delivered

Transport International Holdings PESTLE Analysis

The preview shown here is the exact Transport International Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in this preview are exactly what you’ll download immediately after payment.