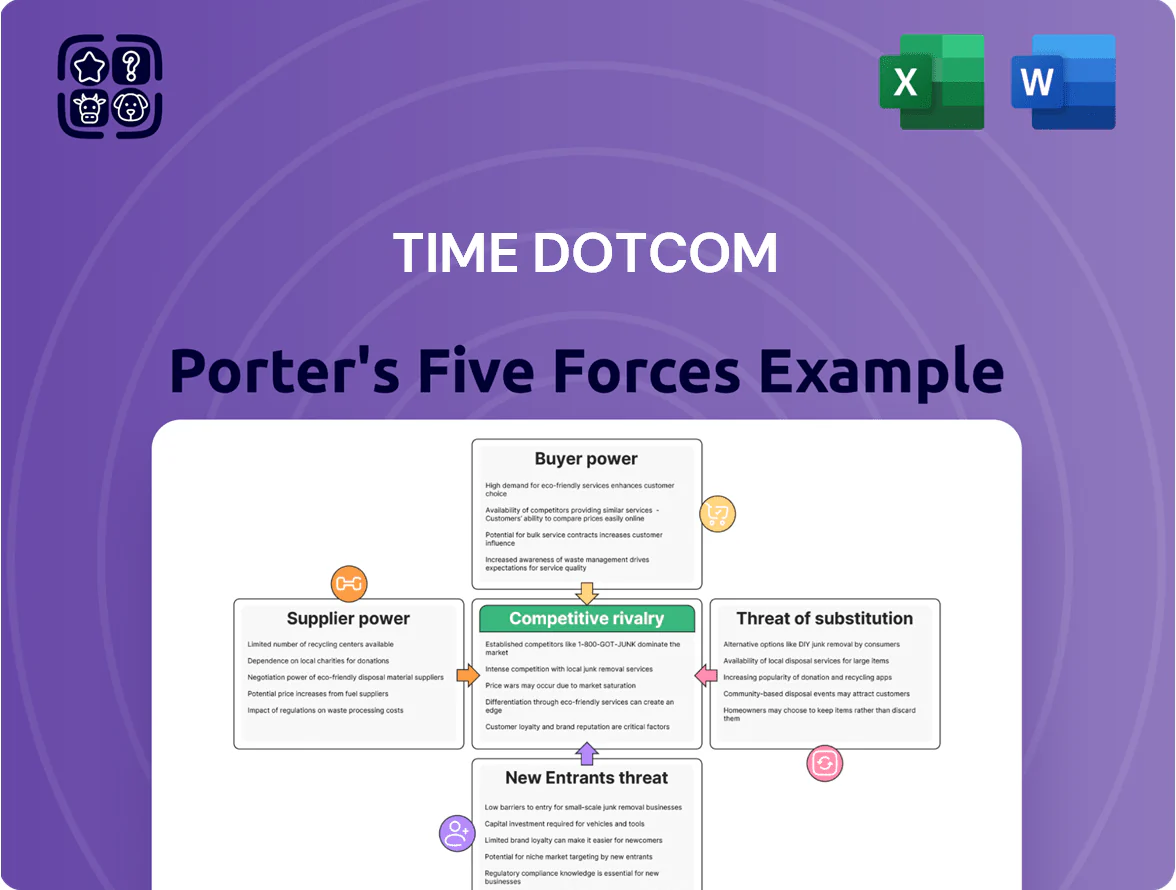

TIME dotCom Porter's Five Forces Analysis

Don't Miss the Bigger Picture

TIME dotCom faces moderate buyer power and high rivalry amid rapid tech shifts and regulatory change, while supplier leverage and substitute threats vary across services; new entrants are constrained by capex and spectrum access. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore TIME dotCom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of global hardware vendors

TIME dotCom depends on a few global vendors—Cisco, Huawei, Nokia—for routers, optical line systems and data‑centre switches; these suppliers held roughly 60–75% share of enterprise optical and switching markets in 2024, giving them bargaining leverage.

High technical specs for subsea and fiber gear plus proprietary software raise switching costs; replacing integrated systems can cost 15–30% of a network upgrade budget and takes 6–18 months, locking TIME into supplier terms.

Dependence on international bandwidth providers

TIME owns key subsea assets but still buys access to international gateways and terrestrial links from foreign incumbents, exposing it to supplier pricing power; in 2024 TIME reported 18% of IP transit costs tied to third-party gateways.

Specialized technical labor scarcity

The Malaysian market faces a tight supply of engineers for fiber‑optic maintenance, cloud architecture and cybersecurity; LinkedIn data (2024) shows 12% annual growth in cloud/security roles while vacancy durations average 45 days, boosting supplier leverage.

As digital transformation rises—Malaysia’s ICT investment grew 8.5% in 2024—competition from telcos and hyperscalers pushes wages up ~7–12%, forcing TIME dotCom to invest in retention, training and premium consultancy contracts.

Energy costs and utility providers

TIME’s data centers and network hubs consume large power loads, making the firm highly dependent on Tenaga Nasional Berhad (TNB) for electricity in Malaysia; TNB’s regulated monopoly status gives it sole control over tariffs.

Any industrial rate rise—TNB raised tariffs 3.0% in July 2024 for large users—would squeeze TIME’s margins directly; negotiation leverage is minimal.

TIME can cut exposure by investing in on-site solar, PPAs, or efficiency upgrades; a 10 MW PPA could lower energy spend by ~12% vs grid rates.

- High dependency on TNB: limited supplier bargaining power

- TNB tariff moves (3.0% July 2024) hit margins

- Negotiation room minimal; regulation centralizes risk

- Mitigation: solar, PPAs, efficiency — example: 10 MW PPA ≈ 12% cost cut

Real estate and right-of-way access

Expanding TIME dotCom’s fiber needs land, buildings, and municipal conduit, where local authorities and developers act as suppliers of space and control access.

Negotiations for right-of-way often face high fees or exclusivity demands; e.g., Malaysian municipal permit fees can add 5–12% to capex and 6–18 month delays.

This geographic dependency gives property owners leverage during deployment, raising costs and slowing retail and enterprise fiber rollouts.

- Permit fees: 5–12% of capex

- Delay: 6–18 months

- Exclusivity risk: higher pricing/limited routes

High supplier leverage (60–75% share); switching costly—PPAs cut energy ~12%

Suppliers (Cisco, Huawei, Nokia, TNB, municipal owners) exert significant leverage via market share, proprietary gear, energy tariffs and right‑of‑way; switching costs (15–30% capex, 6–18 months) and 2024 datapoints (60–75% vendor share, TNB tariff +3.0% July 2024, 18% IP transit via gateways, 5–12% permit capex) keep bargaining power high but renewables/PPAs (10 MW ≈12% energy cut) can mitigate.

| Metric | 2024 value |

|---|---|

| Vendor market share (optical/switch) | 60–75% |

| Switch cost (% upgrade) | 15–30% |

| TNB tariff change | +3.0% Jul 2024 |

| IP transit via 3rd‑party gateways | 18% |

| Permit capex impact | 5–12% |

| 10 MW PPA energy cut | ≈12% |

What is included in the product

Tailored Porter's Five Forces for TIME dotCom that uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and strategic risks—with industry-backed insights to inform investor materials and strategic planning.

A concise Porter's Five Forces one-sheet for TIME dotCom that clarifies competitive pressures at a glance—ideal for rapid strategy decisions and investor briefs.

Customers Bargaining Power

High price sensitivity in retail segments

Residential broadband customers in Malaysia are highly price sensitive, frequently comparing TIME’s monthly fees with TM and Maxis; 2024 MCMC data shows average ARPU for fixed broadband around RM120, so a RM10+ price move risks churn. MSAP (Mandatory Standard on Access Pricing) increased retail price transparency from 2023, easing comparisons and switching, and constrains TIME’s ability to raise consumer prices without notable subscriber loss.

Low switching costs for enterprise services

Enterprise contracts are often multi-year, but commoditization of connectivity (basic MPLS/Internet) means many firms switch providers at renewal; a 2024 B2B survey found 38% of APAC enterprises changed primary providers within three years. Many corporates multi-source for redundancy—TIME dotCom faces clients splitting spend, with top 50 enterprise accounts averaging 1.7 suppliers each. Procurement teams use tenders to force price cuts; benchmark bids in 2023 cut headline rates by ~12% on average, eroding operator margins.

Consolidation of wholesale buyers

The wholesale segment sells bulk bandwidth to telcos and ISPs; with deals like the 2022 Celcom-Digi merger (creating a combined entity serving ~20m subscribers) Malaysia now has fewer large buyers, boosting volume-based bargaining power against TIME dotCom.

These consolidated buyers, often controlling 30%+ market share, use deep market data to push for lower per-Mbps pricing and stricter SLAs, pressuring TIME’s margins and contract terms.

Demand for customized cloud and managed services

Enterprise and government clients now demand bespoke cloud, managed services, and cybersecurity bundled with connectivity, letting them insist on SLAs and integrated performance guarantees; TIME dotCom lost a reported 12% of enterprise RFP wins in 2024 to niche players offering turnkey cloud-plus-connectivity solutions.

Failure to meet those specs risks losing high-value contracts, since 68% of Malaysian enterprises in a 2024 survey prioritized end-to-end cloud integration when choosing vendors.

- Clients demand bundled cloud+connectivity+security

- Higher SLA/performance asks raise switching power

- TIME lost ~12% enterprise RFPs in 2024 to specialists

- 68% of local firms prioritized integrated cloud in 2024 survey

Availability of alternative connectivity technologies

The rise of 5G and satellite internet (Starlink had ~1.5M subscribers worldwide by end-2024) gives TIME dotCom customers credible alternatives to fixed fiber, especially in remote or underserved Malaysian districts where fiber rollout lags.

Fiber still wins on latency and uptime, but competing wireless/non-terrestrial options strengthen buyer negotiating power, pushing TIME to protect margins via differentiated SLAs and bundled services.

- Starlink ~1.5M subs (2024)

- 5G peak speeds 1–3 Gbps, urban coverage ~40–60% Malaysia (2024 estimates)

- Fiber superior: <10 ms latency vs ~20–50 ms satellite

- Alternatives raise churn risk in low-density areas

Rising Alternatives & High Churn Threaten ISPs as RM120 ARPU Limits Price Power

Customers hold strong bargaining power: residential ARPU ~RM120 (2024 MCMC) makes >RM10 price hikes churny; 38% of APAC firms switched vendors within 3 years (2024 B2B survey); TIME lost ~12% enterprise RFPs in 2024 to cloud specialists; Starlink ~1.5M subs (end-2024) and 5G urban coverage ~50% (2024 est.) raise alternatives.

| Metric | Value (2024) |

|---|---|

| Fixed ARPU | RM120 |

| Enterprise churn | 38% |

| RFP losses | 12% |

| Starlink subs | 1.5M |

| 5G urban cov. | ~50% |

Same Document Delivered

TIME dotCom Porter's Five Forces Analysis

This preview shows the exact TIME dotCom Porter’s Five Forces analysis you’ll receive—fully written, professionally formatted, and ready to download the moment you purchase, with no placeholders or mockups.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

TIME dotCom faces moderate buyer power and high rivalry amid rapid tech shifts and regulatory change, while supplier leverage and substitute threats vary across services; new entrants are constrained by capex and spectrum access. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore TIME dotCom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of global hardware vendors

TIME dotCom depends on a few global vendors—Cisco, Huawei, Nokia—for routers, optical line systems and data‑centre switches; these suppliers held roughly 60–75% share of enterprise optical and switching markets in 2024, giving them bargaining leverage.

High technical specs for subsea and fiber gear plus proprietary software raise switching costs; replacing integrated systems can cost 15–30% of a network upgrade budget and takes 6–18 months, locking TIME into supplier terms.

Dependence on international bandwidth providers

TIME owns key subsea assets but still buys access to international gateways and terrestrial links from foreign incumbents, exposing it to supplier pricing power; in 2024 TIME reported 18% of IP transit costs tied to third-party gateways.

Specialized technical labor scarcity

The Malaysian market faces a tight supply of engineers for fiber‑optic maintenance, cloud architecture and cybersecurity; LinkedIn data (2024) shows 12% annual growth in cloud/security roles while vacancy durations average 45 days, boosting supplier leverage.

As digital transformation rises—Malaysia’s ICT investment grew 8.5% in 2024—competition from telcos and hyperscalers pushes wages up ~7–12%, forcing TIME dotCom to invest in retention, training and premium consultancy contracts.

Energy costs and utility providers

TIME’s data centers and network hubs consume large power loads, making the firm highly dependent on Tenaga Nasional Berhad (TNB) for electricity in Malaysia; TNB’s regulated monopoly status gives it sole control over tariffs.

Any industrial rate rise—TNB raised tariffs 3.0% in July 2024 for large users—would squeeze TIME’s margins directly; negotiation leverage is minimal.

TIME can cut exposure by investing in on-site solar, PPAs, or efficiency upgrades; a 10 MW PPA could lower energy spend by ~12% vs grid rates.

- High dependency on TNB: limited supplier bargaining power

- TNB tariff moves (3.0% July 2024) hit margins

- Negotiation room minimal; regulation centralizes risk

- Mitigation: solar, PPAs, efficiency — example: 10 MW PPA ≈ 12% cost cut

Real estate and right-of-way access

Expanding TIME dotCom’s fiber needs land, buildings, and municipal conduit, where local authorities and developers act as suppliers of space and control access.

Negotiations for right-of-way often face high fees or exclusivity demands; e.g., Malaysian municipal permit fees can add 5–12% to capex and 6–18 month delays.

This geographic dependency gives property owners leverage during deployment, raising costs and slowing retail and enterprise fiber rollouts.

- Permit fees: 5–12% of capex

- Delay: 6–18 months

- Exclusivity risk: higher pricing/limited routes

High supplier leverage (60–75% share); switching costly—PPAs cut energy ~12%

Suppliers (Cisco, Huawei, Nokia, TNB, municipal owners) exert significant leverage via market share, proprietary gear, energy tariffs and right‑of‑way; switching costs (15–30% capex, 6–18 months) and 2024 datapoints (60–75% vendor share, TNB tariff +3.0% July 2024, 18% IP transit via gateways, 5–12% permit capex) keep bargaining power high but renewables/PPAs (10 MW ≈12% energy cut) can mitigate.

| Metric | 2024 value |

|---|---|

| Vendor market share (optical/switch) | 60–75% |

| Switch cost (% upgrade) | 15–30% |

| TNB tariff change | +3.0% Jul 2024 |

| IP transit via 3rd‑party gateways | 18% |

| Permit capex impact | 5–12% |

| 10 MW PPA energy cut | ≈12% |

What is included in the product

Tailored Porter's Five Forces for TIME dotCom that uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and strategic risks—with industry-backed insights to inform investor materials and strategic planning.

A concise Porter's Five Forces one-sheet for TIME dotCom that clarifies competitive pressures at a glance—ideal for rapid strategy decisions and investor briefs.

Customers Bargaining Power

High price sensitivity in retail segments

Residential broadband customers in Malaysia are highly price sensitive, frequently comparing TIME’s monthly fees with TM and Maxis; 2024 MCMC data shows average ARPU for fixed broadband around RM120, so a RM10+ price move risks churn. MSAP (Mandatory Standard on Access Pricing) increased retail price transparency from 2023, easing comparisons and switching, and constrains TIME’s ability to raise consumer prices without notable subscriber loss.

Low switching costs for enterprise services

Enterprise contracts are often multi-year, but commoditization of connectivity (basic MPLS/Internet) means many firms switch providers at renewal; a 2024 B2B survey found 38% of APAC enterprises changed primary providers within three years. Many corporates multi-source for redundancy—TIME dotCom faces clients splitting spend, with top 50 enterprise accounts averaging 1.7 suppliers each. Procurement teams use tenders to force price cuts; benchmark bids in 2023 cut headline rates by ~12% on average, eroding operator margins.

Consolidation of wholesale buyers

The wholesale segment sells bulk bandwidth to telcos and ISPs; with deals like the 2022 Celcom-Digi merger (creating a combined entity serving ~20m subscribers) Malaysia now has fewer large buyers, boosting volume-based bargaining power against TIME dotCom.

These consolidated buyers, often controlling 30%+ market share, use deep market data to push for lower per-Mbps pricing and stricter SLAs, pressuring TIME’s margins and contract terms.

Demand for customized cloud and managed services

Enterprise and government clients now demand bespoke cloud, managed services, and cybersecurity bundled with connectivity, letting them insist on SLAs and integrated performance guarantees; TIME dotCom lost a reported 12% of enterprise RFP wins in 2024 to niche players offering turnkey cloud-plus-connectivity solutions.

Failure to meet those specs risks losing high-value contracts, since 68% of Malaysian enterprises in a 2024 survey prioritized end-to-end cloud integration when choosing vendors.

- Clients demand bundled cloud+connectivity+security

- Higher SLA/performance asks raise switching power

- TIME lost ~12% enterprise RFPs in 2024 to specialists

- 68% of local firms prioritized integrated cloud in 2024 survey

Availability of alternative connectivity technologies

The rise of 5G and satellite internet (Starlink had ~1.5M subscribers worldwide by end-2024) gives TIME dotCom customers credible alternatives to fixed fiber, especially in remote or underserved Malaysian districts where fiber rollout lags.

Fiber still wins on latency and uptime, but competing wireless/non-terrestrial options strengthen buyer negotiating power, pushing TIME to protect margins via differentiated SLAs and bundled services.

- Starlink ~1.5M subs (2024)

- 5G peak speeds 1–3 Gbps, urban coverage ~40–60% Malaysia (2024 estimates)

- Fiber superior: <10 ms latency vs ~20–50 ms satellite

- Alternatives raise churn risk in low-density areas

Rising Alternatives & High Churn Threaten ISPs as RM120 ARPU Limits Price Power

Customers hold strong bargaining power: residential ARPU ~RM120 (2024 MCMC) makes >RM10 price hikes churny; 38% of APAC firms switched vendors within 3 years (2024 B2B survey); TIME lost ~12% enterprise RFPs in 2024 to cloud specialists; Starlink ~1.5M subs (end-2024) and 5G urban coverage ~50% (2024 est.) raise alternatives.

| Metric | Value (2024) |

|---|---|

| Fixed ARPU | RM120 |

| Enterprise churn | 38% |

| RFP losses | 12% |

| Starlink subs | 1.5M |

| 5G urban cov. | ~50% |

Same Document Delivered

TIME dotCom Porter's Five Forces Analysis

This preview shows the exact TIME dotCom Porter’s Five Forces analysis you’ll receive—fully written, professionally formatted, and ready to download the moment you purchase, with no placeholders or mockups.